Key Insights

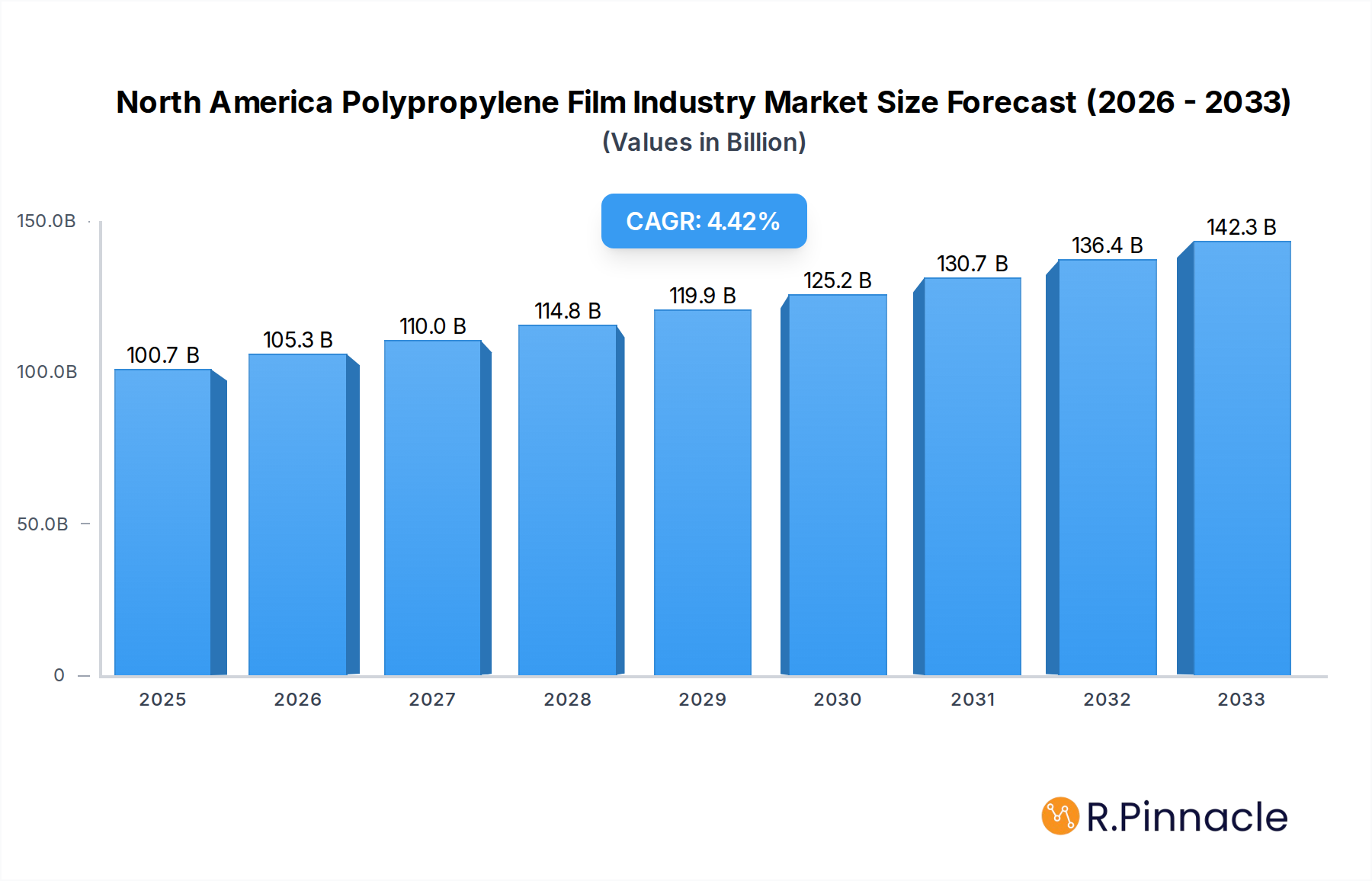

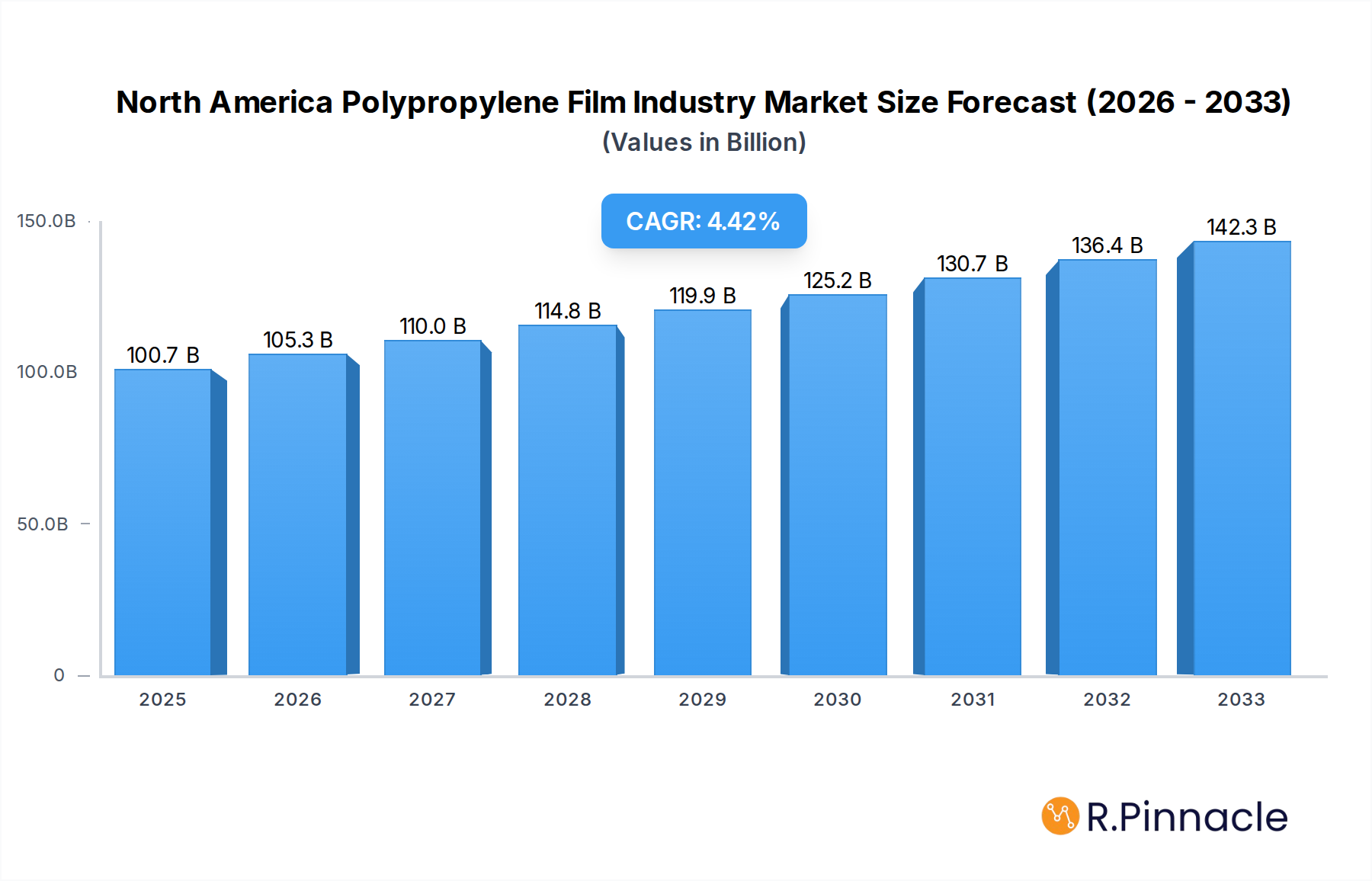

The North America Polypropylene Film Industry is poised for significant expansion, with a projected market size of USD 100.73 billion in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4.5% expected throughout the forecast period (2025-2033). Key drivers fueling this expansion include the escalating demand for versatile and durable packaging solutions across various end-user verticals. The food and beverage sector, in particular, continues to be a dominant force, driven by consumer preferences for convenience, extended shelf life, and visually appealing packaging. The pharmaceuticals and medical industries also present substantial opportunities, with a growing need for high-performance films that offer barrier properties, sterility, and tamper-evidence. Furthermore, the industrial segment, encompassing applications like protective films and specialty tapes, contributes steadily to market buoyancy. Innovations in film technology, such as enhanced barrier properties, recyclability, and customized aesthetics, are also playing a crucial role in meeting evolving market demands and environmental regulations.

North America Polypropylene Film Industry Market Size (In Billion)

The market landscape is characterized by a dynamic interplay of growth drivers and emerging trends. The increasing focus on sustainable packaging solutions is prompting manufacturers to invest in recyclable and biodegradable polypropylene films, aligning with global environmental initiatives and consumer consciousness. Technological advancements are leading to the development of thinner yet stronger films, optimizing material usage and reducing costs. The presence of established players like Dunmore Corporation, Toray Plastics (America) Inc, and Taghleef Industries indicates a competitive yet mature market. However, potential restraints such as fluctuating raw material prices, particularly for propylene, and the stringent regulatory environment surrounding packaging materials could pose challenges. Nevertheless, the overall outlook for the North America Polypropylene Film Industry remains highly positive, with continued innovation and strategic investments expected to propel sustained growth and market penetration across diverse applications.

North America Polypropylene Film Industry Company Market Share

North America Polypropylene Film Industry Market Structure & Innovation Trends

The North America Polypropylene Film Industry report offers a comprehensive analysis of market concentration, innovation drivers, and the intricate regulatory frameworks shaping the sector. We delve into the competitive landscape, examining product substitutes that challenge polypropylene's dominance and the evolving end-user demographics that dictate demand. Mergers and acquisitions (M&A) activity is a key indicator of market consolidation and strategic partnerships. Our analysis forecasts M&A deal values to reach approximately 3.5 billion during the forecast period, reflecting a dynamic environment where industry leaders are actively pursuing growth and market share.

- Market Concentration: The industry exhibits a moderate to high level of concentration, with a few key players holding substantial market share.

- Innovation Drivers: Key innovation drivers include the demand for enhanced barrier properties, recyclability, and customizable film solutions for specialized applications.

- Regulatory Frameworks: Environmental regulations, particularly concerning plastic waste and single-use plastics, are significant influencers of product development and market strategies.

- Product Substitutes: While polypropylene films offer excellent versatility, advanced bioplastics and other flexible packaging materials present emerging competitive threats.

- End-User Demographics: The aging population and the increasing disposable income in certain demographics are influencing demand for packaging solutions in sectors like food and pharmaceuticals.

- M&A Activities: Recent M&A trends indicate a focus on acquiring companies with specialized technology, expanded geographic reach, or diversified product portfolios.

North America Polypropylene Film Industry Market Dynamics & Trends

The North America Polypropylene Film Industry is poised for robust expansion, driven by a confluence of potent market growth drivers, transformative technological disruptions, evolving consumer preferences, and an intensely competitive dynamic. The projected Compound Annual Growth Rate (CAGR) for the industry stands at an impressive 6.5% from the base year of 2025 through 2033, underscoring its significant economic vitality. This growth is intrinsically linked to the escalating demand for flexible packaging solutions across a multitude of end-user verticals. The food and beverage sector, in particular, continues to be a primary consumer of polypropylene films, citing their superior barrier properties, printability, and cost-effectiveness for extending shelf life and ensuring product integrity. Technological advancements are playing a pivotal role in shaping market trends. The development of advanced multilayer films, incorporating novel polymers and additives, is enabling enhanced performance characteristics such as improved moisture and oxygen barriers, UV resistance, and superior heat sealability. These innovations directly address the evolving needs of sophisticated packaging applications.

Furthermore, the increasing consumer emphasis on sustainability and convenience is a powerful catalyst for change. While traditional polypropylene films face scrutiny regarding their environmental impact, the industry is responding with significant investments in developing more recyclable and compostable alternatives. Innovations in mono-material polypropylene structures are gaining traction, offering a more streamlined recycling pathway. Consumer preferences are also shifting towards lightweight, easy-to-open, and resealable packaging formats, all areas where polypropylene films can deliver competitive advantages. The competitive landscape is characterized by a continuous drive for operational efficiency, product differentiation, and strategic partnerships. Companies are investing heavily in research and development to stay ahead of technological curves and anticipate market demands. Market penetration of high-performance polypropylene films is expected to increase as their benefits become more widely recognized and adopted across diverse industrial applications. The integration of smart technologies, such as antimicrobial properties and active packaging features, is another emerging trend that will likely influence market dynamics, further solidifying polypropylene films' position as a versatile and adaptable packaging material. The projected market size for the North America Polypropylene Film Industry is expected to surpass 55 billion by 2033, demonstrating a clear upward trajectory fueled by these multifaceted dynamics.

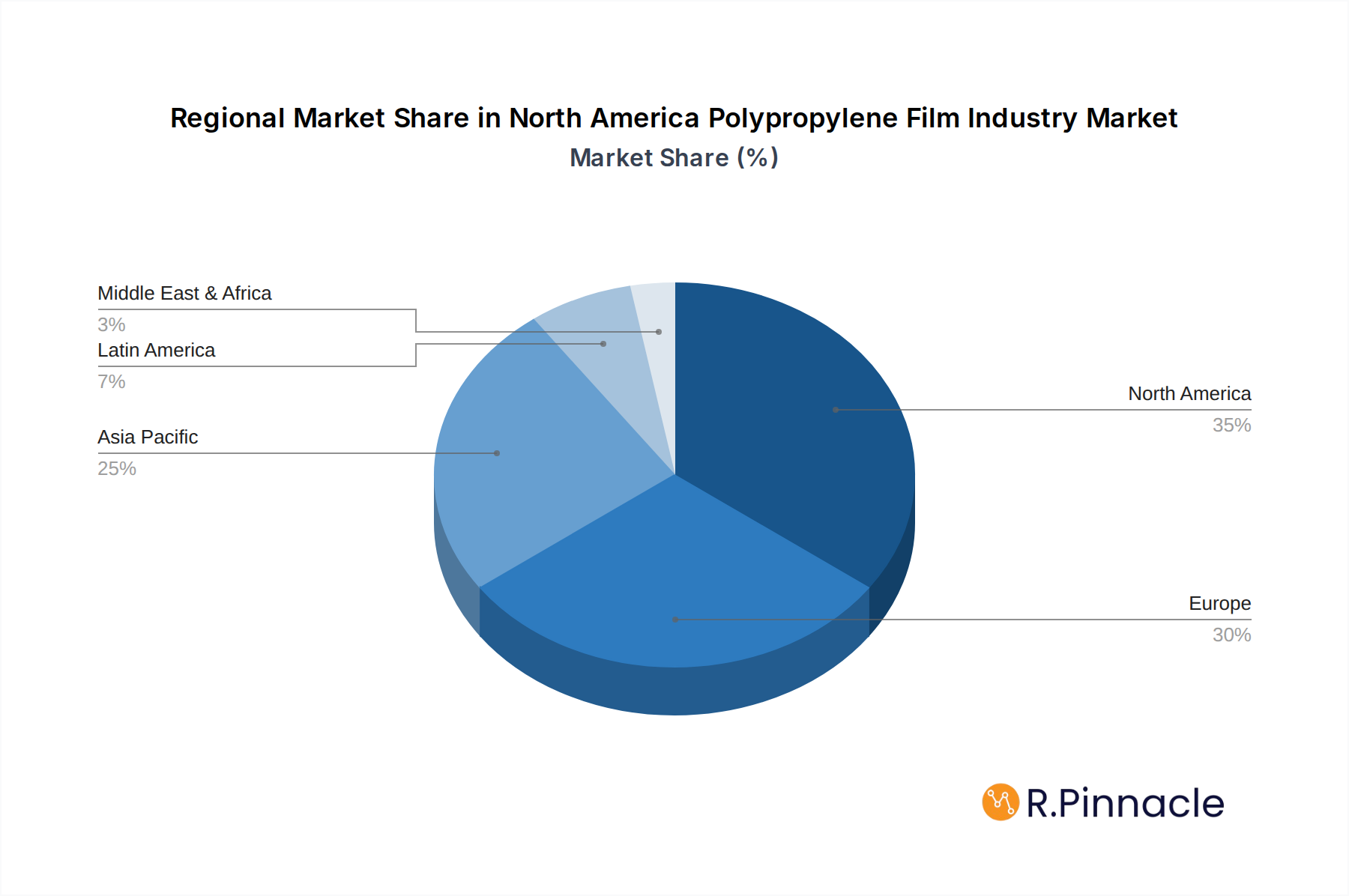

Dominant Regions & Segments in North America Polypropylene Film Industry

The North America Polypropylene Film Industry exhibits a distinct geographical and sectoral dominance, with the United States leading in terms of market size and consumption. The vastness of the US market, coupled with its advanced industrial infrastructure and significant consumer base, positions it as the epicenter of polypropylene film demand. Key drivers for this dominance include robust economic policies that encourage manufacturing and trade, substantial investments in supply chain logistics, and a high level of innovation adoption across various industries. Canada and Mexico also contribute significantly to the regional market, with their own unique economic drivers and industrial focuses.

Leading Region: The United States commands the largest market share within North America, driven by its extensive manufacturing base and high consumer spending.

- Economic Policies: Favorable government policies supporting manufacturing and innovation, alongside a strong consumer market, are key drivers.

- Infrastructure: Well-developed logistics and distribution networks facilitate efficient product delivery across the nation.

- Technological Adoption: High adoption rates of advanced packaging technologies across diverse industries.

Dominant End-User Verticals: Within the broader market, specific end-user verticals showcase pronounced reliance on polypropylene films, each driven by unique market imperatives.

Food: This sector is a perennial leader due to the universal demand for safe, fresh, and appealing food products. Polypropylene films are integral for their excellent moisture barrier properties, printability for branding, and cost-effectiveness. The increasing demand for convenience foods, ready-to-eat meals, and snack packaging further solidifies the food segment's dominance. The market size for polypropylene films in the food sector is projected to reach 25 billion by 2033.

- Key Drivers: Extended shelf-life requirements, consumer preference for visually appealing packaging, and stringent food safety regulations.

- Dominance Analysis: The sheer volume of food consumption and the diverse range of food products requiring specialized packaging make this segment the largest consumer.

Beverage: The beverage industry relies heavily on polypropylene films for various applications, including shrink sleeves, labels, and flexible pouches. The need for durable, tamper-evident, and aesthetically pleasing packaging solutions for water, soft drinks, juices, and alcoholic beverages drives significant demand.

- Key Drivers: Brand differentiation through high-quality printing, product protection from external elements, and the rise of single-serve beverage formats.

- Dominance Analysis: Growth in the bottled beverage market and the increasing use of specialized films for branding and functionality contribute to its strong performance.

Industrial: The industrial segment encompasses a wide array of applications, from protective films for electronics and automotive parts to durable packaging for construction materials and textiles. The demand for robust, protective, and often custom-engineered polypropylene films in this sector is substantial.

- Key Drivers: Need for scratch resistance, cushioning, and protection against environmental factors during transit and storage.

- Dominance Analysis: The breadth of industrial manufacturing in North America ensures a consistent and diverse demand for polypropylene films.

Pharmaceuticals & Medical: This sector demands highly specialized and regulated polypropylene films. Applications include sterile packaging for medical devices, pharmaceutical blister packs, and diagnostic kits. The emphasis on barrier properties, chemical inertness, and compliance with strict regulatory standards is paramount. The market size for polypropylene films in this sector is projected to reach 8 billion by 2033.

- Key Drivers: Stringent regulatory requirements for safety and efficacy, need for sterile and tamper-evident packaging, and advancements in medical device packaging.

- Dominance Analysis: While a smaller segment by volume, its high-value applications and critical nature make it a significant contributor.

Other End-User Verticals: This category includes diverse applications such as personal care products, cosmetics, stationery, and agricultural films. Innovation in these niche areas, driven by specific consumer trends and functional requirements, contributes to the overall market dynamism.

- Key Drivers: Growing demand for aesthetically pleasing packaging in personal care, specialized films for agricultural applications, and e-commerce packaging solutions.

- Dominance Analysis: This segment represents a growing area for specialized polypropylene film development and market expansion.

North America Polypropylene Film Industry Product Innovations

North America's polypropylene film industry is witnessing a surge in product innovations focused on enhancing sustainability and performance. Key developments include the introduction of mono-material polypropylene structures that are fully recyclable, addressing growing environmental concerns. Advanced barrier technologies are being integrated to extend product shelf life in food packaging, while antimicrobial additives are gaining traction for hygiene-sensitive applications in medical and food sectors. High-clarity films with improved printability are enabling enhanced product aesthetics and brand visibility across all segments. These innovations provide a competitive advantage by meeting evolving market demands for both functionality and eco-consciousness.

Report Scope & Segmentation Analysis

This report meticulously analyzes the North America Polypropylene Film Industry, segmenting the market across critical End-User Verticals to provide granular insights. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, utilizing historical data from 2019-2024.

- Food: This segment, projected to reach 25 billion by 2033, is driven by the need for superior barrier properties and extended shelf life. Competitive dynamics involve innovation in sustainable packaging solutions and cost-effectiveness.

- Beverage: Expected to achieve 12 billion by 2033, the beverage segment's growth is fueled by demand for attractive branding and durable packaging. Competition centers on printing capabilities and specialized film functionalities.

- Industrial: With a projected market size of 15 billion by 2033, this segment's growth hinges on demand for protective and durable films. Key competitive factors include customization and performance under harsh conditions.

- Pharmaceuticals & Medical: This high-value segment, forecast to reach 8 billion by 2033, is characterized by stringent regulatory compliance and the demand for sterile, inert packaging. Competition focuses on meeting strict quality standards and advanced material properties.

- Other End-User Verticals: Encompassing a diverse range of applications, this segment is projected to reach 5 billion by 2033. Growth is driven by emerging niche markets and the development of specialized film properties for personal care, agriculture, and e-commerce.

Key Drivers of North America Polypropylene Film Industry Growth

The North America Polypropylene Film Industry's growth is propelled by a multifaceted interplay of technological, economic, and regulatory factors. The escalating demand for flexible and lightweight packaging solutions, driven by consumer preference for convenience and reduced material usage, is a primary economic driver. Technologically, advancements in film extrusion and co-extrusion techniques are enabling the creation of thinner, stronger, and more sustainable polypropylene films with superior barrier properties. Environmental regulations, while posing challenges, are also a significant driver for innovation in recyclable and compostable polypropylene film alternatives. The growth of e-commerce necessitates robust yet lightweight packaging, further boosting demand. The increasing adoption of advanced printing technologies for enhanced product aesthetics also contributes to market expansion.

Challenges in the North America Polypropylene Film Industry Sector

Despite its growth trajectory, the North America Polypropylene Film Industry faces significant challenges. The growing global concern over plastic waste and single-use plastics has led to increased regulatory scrutiny and public pressure for more sustainable alternatives, potentially impacting the demand for traditional polypropylene films. Volatility in raw material prices, particularly polypropylene resin, can affect manufacturing costs and profit margins. Intense competition from alternative packaging materials, including paper, bioplastics, and other polymers, poses a constant threat. Supply chain disruptions, exacerbated by geopolitical events and logistics bottlenecks, can impact production schedules and delivery timelines. Furthermore, the high capital investment required for advanced manufacturing technologies can be a barrier for smaller players.

Emerging Opportunities in North America Polypropylene Film Industry

Emerging opportunities within the North America Polypropylene Film Industry lie in the continuous innovation of sustainable solutions and the expansion into new application areas. The development of advanced mono-material polypropylene films that achieve circularity through effective recycling presents a significant market opportunity. The growing demand for high-performance films in the medical and pharmaceutical sectors, driven by increasing healthcare needs and advancements in drug delivery systems, offers substantial growth potential. Furthermore, the expansion of the e-commerce market requires specialized packaging solutions, creating opportunities for customized and protective polypropylene films. The integration of smart packaging technologies, such as those offering enhanced traceability or active preservation, represents another avenue for innovation and market differentiation.

Leading Players in the North America Polypropylene Film Industry Market

- Dunmore Corporation

- Cheever Specialty Paper & Film

- Toray Plastics (America) Inc

- Oben Holding Group

- Innovia Film

- Cosmo Films Inc

- Copol International Ltd

- Taghleef Industries

- Inteplast Group

Key Developments in North America Polypropylene Film Industry Industry

- 2023 October: Innovia Film launched a new range of ultra-thin, high-barrier BOPP films designed for sustainable food packaging.

- 2023 September: Taghleef Industries announced a significant investment in R&D to develop advanced recyclable polypropylene film solutions.

- 2023 July: Toray Plastics (America) Inc. expanded its production capacity for specialty polypropylene films catering to the medical device sector.

- 2023 March: Cosmo Films Inc. introduced innovative printable BOPP films with enhanced surface properties for vibrant graphics in packaging.

- 2022 December: Oben Holding Group acquired a smaller specialty film manufacturer, bolstering its product portfolio in the industrial segment.

- 2022 June: Dunmore Corporation unveiled a new series of protective polypropylene films with improved scratch and abrasion resistance.

- 2022 February: Cheever Specialty Paper & Film developed a biodegradable polypropylene film alternative for certain niche applications.

Future Outlook for North America Polypropylene Film Industry Market

The future outlook for the North America Polypropylene Film Industry is exceptionally promising, driven by an unwavering demand for versatile, high-performance, and increasingly sustainable packaging solutions. The industry's ability to innovate and adapt to evolving consumer preferences and stringent environmental regulations will be paramount. Continued investment in advanced manufacturing technologies and research into novel polymer formulations will unlock new application possibilities and enhance existing ones. The growing emphasis on circular economy principles will spur the development and adoption of more recyclable and compostable polypropylene films, solidifying their long-term market relevance. As key end-user industries like food, beverage, and healthcare continue to expand, the demand for sophisticated polypropylene film packaging is set to rise, positioning the industry for sustained growth and significant economic contribution in the years to come.

North America Polypropylene Film Industry Segmentation

-

1. End-User Vertical

- 1.1. Food

- 1.2. Beverage

- 1.3. Industrial

- 1.4. Pharmaceuticals & Medical

- 1.5. Other End-User Verticals

North America Polypropylene Film Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Polypropylene Film Industry Regional Market Share

Geographic Coverage of North America Polypropylene Film Industry

North America Polypropylene Film Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 5.1.1. Food

- 5.1.2. Beverage

- 5.1.3. Industrial

- 5.1.4. Pharmaceuticals & Medical

- 5.1.5. Other End-User Verticals

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 6. North America Polypropylene Film Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 6.1.1. Food

- 6.1.2. Beverage

- 6.1.3. Industrial

- 6.1.4. Pharmaceuticals & Medical

- 6.1.5. Other End-User Verticals

- 6.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Dunmore Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Cheever Specialty Paper & Film

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toray Plastics (America) Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Oben Holding Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Innovia Film

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cosmo Films Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Copol International Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Taghleef Industries

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Inteplast Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Dunmore Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Polypropylene Film Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Polypropylene Film Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Polypropylene Film Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 2: North America Polypropylene Film Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: North America Polypropylene Film Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 4: North America Polypropylene Film Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States North America Polypropylene Film Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada North America Polypropylene Film Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico North America Polypropylene Film Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Polypropylene Film Industry?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the North America Polypropylene Film Industry?

Key companies in the market include Dunmore Corporation, Cheever Specialty Paper & Film, Toray Plastics (America) Inc, Oben Holding Group, Innovia Film, Cosmo Films Inc, Copol International Ltd, Taghleef Industries, Inteplast Group.

3. What are the main segments of the North America Polypropylene Film Industry?

The market segments include End-User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 100.73 billion as of 2022.

5. What are some drivers contributing to market growth?

Cost-Effectiveness Of The Outsourcing; Access to the advanced technologies and expertise.

6. What are the notable trends driving market growth?

Food Industry to Hold Major Share.

7. Are there any restraints impacting market growth?

Monitoring issues and lack of standardization.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Polypropylene Film Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Polypropylene Film Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Polypropylene Film Industry?

To stay informed about further developments, trends, and reports in the North America Polypropylene Film Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence