Key Insights

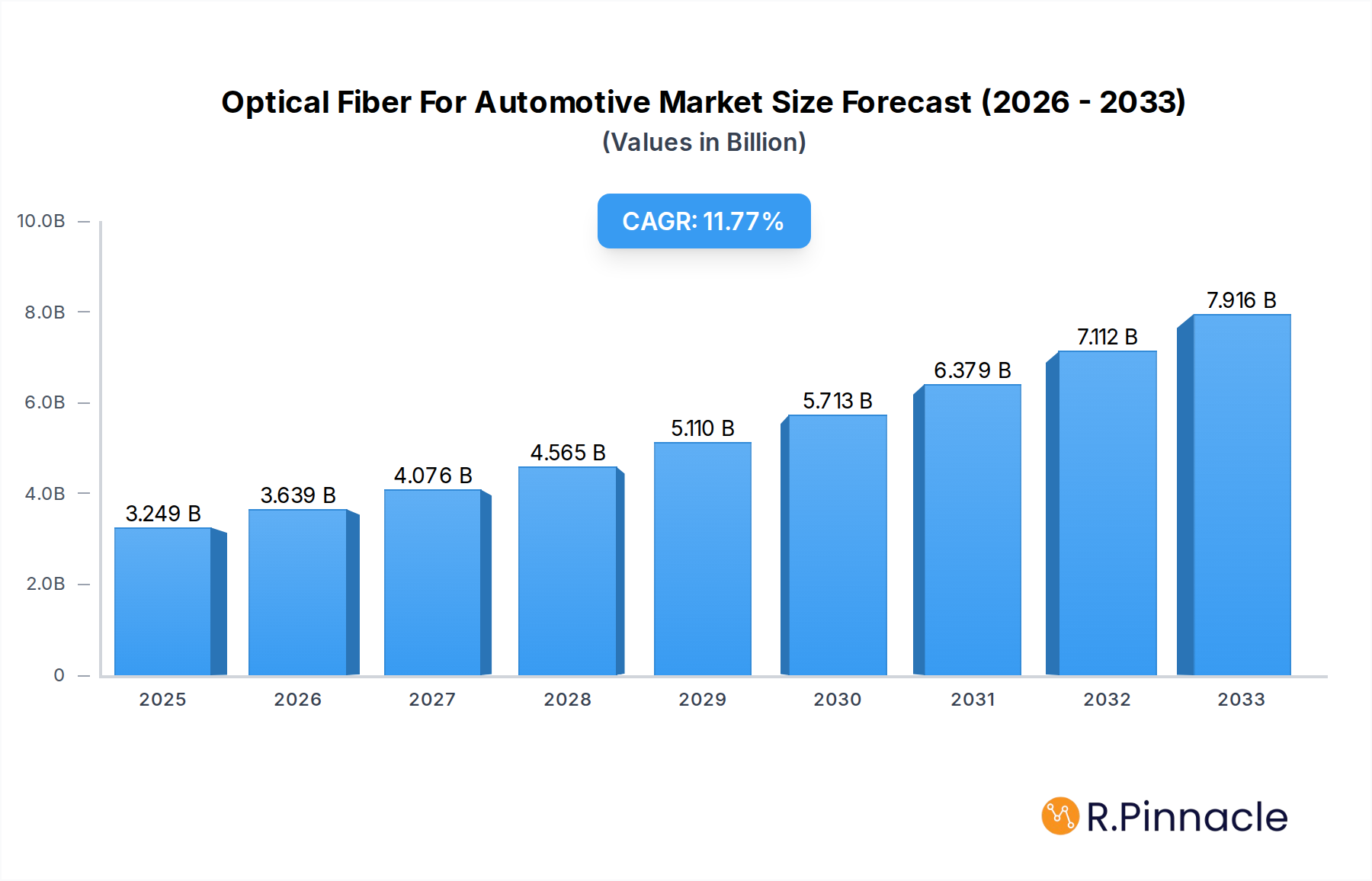

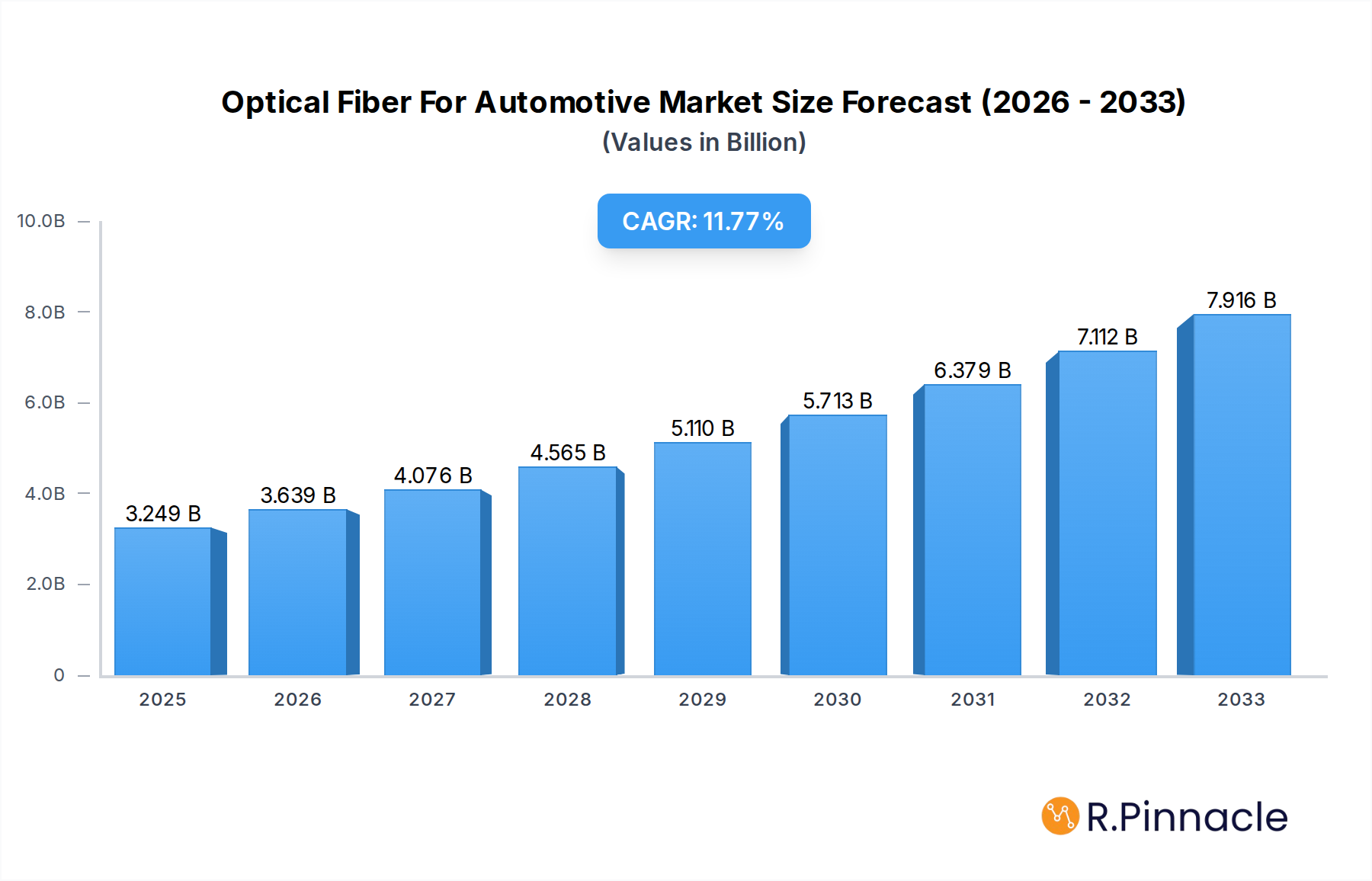

The global Optical Fiber for Automotive market is poised for substantial growth, projected to reach $3249.5 million in 2025 with a robust CAGR of 12% during the forecast period of 2025-2033. This significant expansion is primarily driven by the increasing integration of advanced driver-assistance systems (ADAS), in-vehicle infotainment, and the burgeoning trend of autonomous driving. As vehicles become more sophisticated, the demand for high-speed, reliable data transmission capabilities escalates, making optical fiber an indispensable component. The Passenger Vehicle segment is expected to lead the market, owing to the widespread adoption of these technologies in personal mobility.

Optical Fiber For Automotive Market Size (In Billion)

The market's trajectory is further propelled by ongoing advancements in optical fiber technology, leading to lighter, more durable, and cost-effective solutions for automotive applications. While the widespread adoption of optical fibers offers significant advantages in terms of bandwidth and electromagnetic interference immunity, challenges such as the initial cost of implementation and the need for specialized installation expertise may present moderate restraints. However, the persistent drive towards enhanced vehicle safety, improved driver and passenger experiences, and the evolution of connected car ecosystems are anticipated to outweigh these limitations. Key players like Corning, Fujikura, and TE Connectivity are at the forefront of innovation, developing solutions tailored to the stringent requirements of the automotive industry. The market is segmented into Single-mode and Multi-mode optical fibers, catering to diverse application needs across various vehicle types.

Optical Fiber For Automotive Company Market Share

This in-depth report provides a critical analysis of the Optical Fiber for Automotive market, a rapidly evolving sector poised for exponential growth. With a study period spanning from 2019 to 2033, and a base year of 2025, this research offers unparalleled insights into the market's current state and future trajectory. Dive deep into the burgeoning demand for high-speed, lightweight, and interference-free data transmission solutions within vehicles, driven by advancements in autonomous driving, infotainment systems, and advanced driver-assistance systems (ADAS).

Optical Fiber For Automotive Market Structure & Innovation Trends

The Optical Fiber for Automotive market exhibits a dynamic structure characterized by intense innovation and strategic collaborations. While the market is moderately concentrated, with key players investing heavily in R&D, emerging technologies continue to disrupt established norms. Innovation drivers include the ever-increasing demand for bandwidth-intensive automotive applications, the pursuit of weight reduction for improved fuel efficiency, and the need for robust, interference-immune connectivity. Regulatory frameworks, such as those promoting vehicle safety and emissions standards, indirectly foster the adoption of advanced technologies like optical fiber. Product substitutes, primarily copper-based cabling, are gradually being phased out due to their limitations in speed and weight. End-user demographics are shifting towards younger, tech-savvy consumers who expect seamless digital experiences within their vehicles. Mergers and acquisitions (M&A) activities, with estimated deal values in the hundreds of millions, are shaping the competitive landscape as companies seek to consolidate their market position and acquire critical technological expertise. Notable M&A activities are anticipated to further streamline the supply chain and accelerate product development.

Optical Fiber For Automotive Market Dynamics & Trends

The Optical Fiber for Automotive market is experiencing a period of robust expansion, fueled by a confluence of technological advancements and evolving consumer demands. The relentless progression towards Level 4 and Level 5 autonomous driving systems necessitates data transmission speeds and reliability far exceeding those offered by traditional copper wiring. This intrinsic requirement is a primary growth driver, pushing the adoption of optical fiber solutions in passenger vehicles and commercial vehicles alike. Furthermore, the integration of sophisticated infotainment systems, advanced driver-assistance systems (ADAS), and the increasing prevalence of vehicle-to-everything (V2X) communication demand an infrastructure capable of handling massive data volumes with minimal latency.

Technological disruptions are playing a pivotal role. The development of more robust, cost-effective, and easily installable optical fibers specifically designed for the harsh automotive environment is a key trend. Innovations in connector technology and termination methods are addressing previous installation challenges, thereby improving market penetration. Consumer preferences are increasingly leaning towards feature-rich vehicles, with high-speed connectivity being a non-negotiable expectation. This shift is compelling automotive manufacturers to prioritize advanced connectivity solutions.

The competitive dynamics within the market are intensifying. Established players like Corning, Fujikura, and TE Connectivity are investing billions in research and development, while specialized companies such as Timbercon, AOS, and TX Plastic Optical Fibers are carving out significant niches. The projected Compound Annual Growth Rate (CAGR) for the optical fiber in automotive market is expected to be robust, with market penetration reaching substantial levels by the end of the forecast period. The continuous evolution of in-vehicle networking architectures and the increasing adoption of Ethernet-based solutions further solidify the position of optical fiber as the future of automotive connectivity.

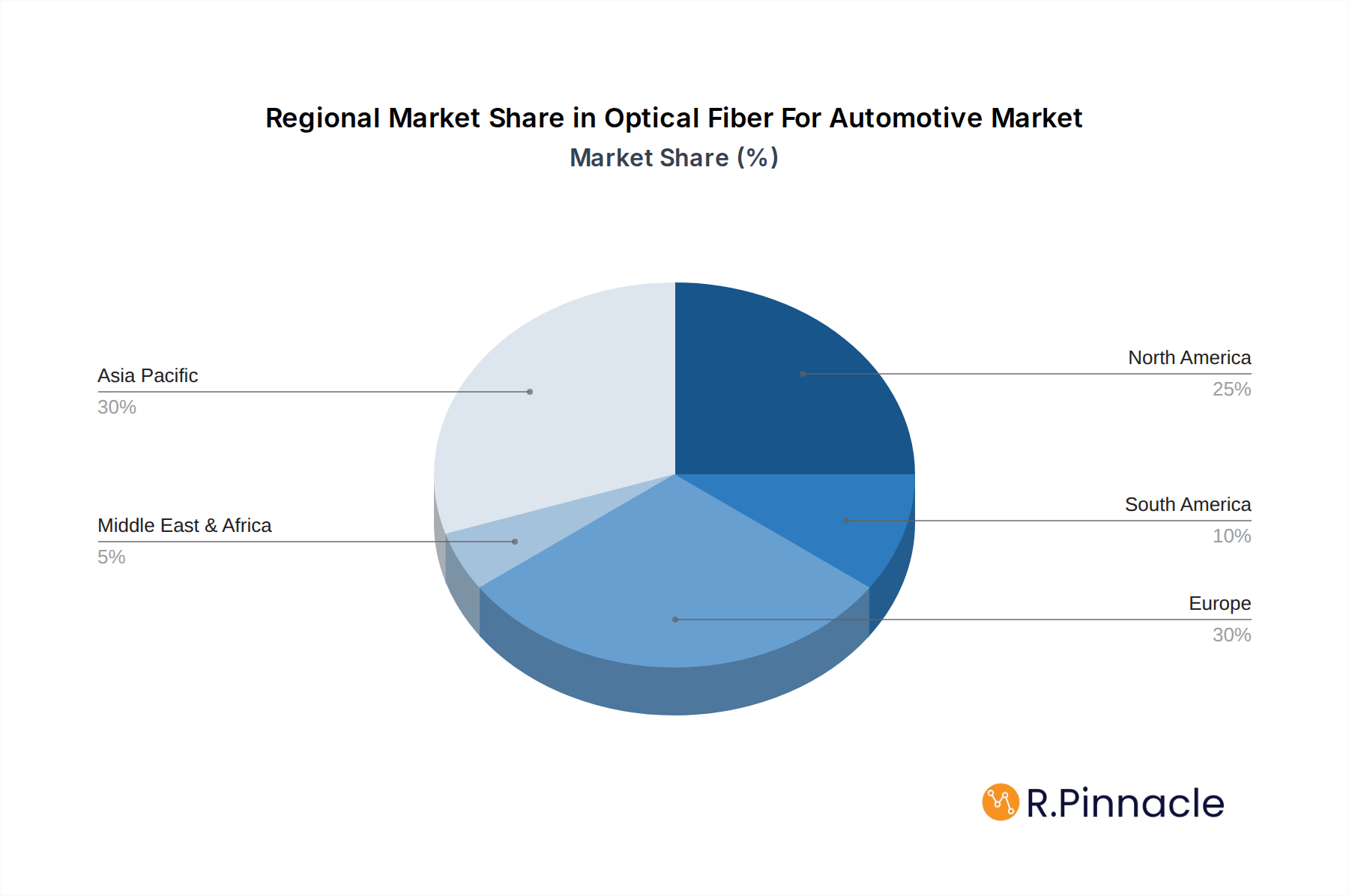

Dominant Regions & Segments in Optical Fiber For Automotive

The Optical Fiber for Automotive market exhibits distinct regional strengths and segment dominance, driven by economic policies, infrastructure development, and vehicle production volumes. Asia-Pacific currently stands as the dominant region, propelled by the immense automotive manufacturing hubs in China, Japan, and South Korea. Strong government initiatives promoting electric vehicles (EVs) and intelligent transportation systems, coupled with substantial investments in automotive R&D and production, contribute significantly to this dominance.

Within applications, the Passenger Vehicle segment holds the largest market share, reflecting the sheer volume of passenger cars produced globally. The integration of advanced infotainment, ADAS, and connectivity features in this segment is a primary catalyst for optical fiber adoption. However, the Commercial Vehicle segment is poised for significant growth, driven by the increasing adoption of telematics, fleet management systems, and autonomous capabilities in trucks and buses, demanding robust and high-bandwidth communication solutions.

In terms of fiber type, Multi-mode Optical Fiber currently dominates, offering a cost-effective solution for many in-vehicle networking requirements. However, the Single-mode Optical Fiber segment is experiencing rapid growth, driven by the escalating bandwidth demands of future automotive architectures, particularly those supporting advanced autonomous driving and high-resolution sensor data processing. The economic policies in leading automotive nations, such as subsidies for EV development and tax incentives for technological advancements, further amplify the demand for optical fiber solutions. Infrastructure development, including the expansion of 5G networks that necessitate seamless in-vehicle connectivity, also plays a crucial role in shaping the market's dominant regions and segments.

Optical Fiber For Automotive Product Innovations

Product innovations in optical fiber for automotive are centered around enhancing performance, durability, and cost-effectiveness for in-vehicle applications. Companies like WEINERT and TORAY INDUSTRIES are developing advanced polymer optical fibers that offer superior flexibility and ease of installation compared to traditional glass fibers, while maintaining excellent signal integrity. Fujikura is at the forefront of miniaturization, creating ultra-slim optical fiber cables that reduce vehicle weight and interior space requirements. These innovations offer significant competitive advantages by enabling the integration of more advanced technologies and improving overall vehicle efficiency and user experience. The focus is on creating plug-and-play solutions that simplify manufacturing processes and reduce assembly times.

Optical Fiber For Automotive Market Scope & Segmentation Analysis

The Optical Fiber for Automotive market is segmented into two primary application types: Passenger Vehicle and Commercial Vehicle. The Passenger Vehicle segment, encompassing sedans, SUVs, and hatchbacks, is projected to hold a substantial market share due to its high production volumes and increasing demand for advanced in-car electronics. Growth projections for this segment are strong, driven by feature upgrades and consumer preference for connected mobility. The Commercial Vehicle segment, including trucks, buses, and vans, is expected to witness rapid growth as these vehicles integrate more sophisticated telematics, fleet management, and autonomous driving features. Market size for commercial vehicles is expanding as regulations and operational efficiencies necessitate advanced connectivity. Competitive dynamics within both segments are characterized by innovation in cable design, connector technology, and integration solutions.

The market also bifurcates by fiber type: Single-mode Optical Fiber and Multi-mode Optical Fiber. While Multi-mode Optical Fiber currently serves a broader range of applications due to its cost-effectiveness, Single-mode Optical Fiber is experiencing accelerated growth. This is driven by the increasing bandwidth requirements for advanced driver-assistance systems (ADAS) and autonomous driving technologies that demand higher data transmission speeds and longer reach within the vehicle. Market size for Single-mode is projected to grow significantly in the coming years, fueled by its suitability for future-generation automotive networks.

Key Drivers of Optical Fiber For Automotive Growth

The growth of the Optical Fiber for Automotive market is propelled by several critical factors. Technologically, the escalating demand for high-bandwidth applications such as advanced infotainment systems, sophisticated ADAS, and the foundational infrastructure for autonomous driving is a primary driver. The increasing need for weight reduction in vehicles to improve fuel efficiency and electric vehicle range directly benefits optical fiber, which is significantly lighter than traditional copper wiring. Economically, government incentives and regulatory mandates promoting vehicle safety, connectivity, and emissions reduction are indirectly fueling adoption. For instance, mandates for advanced safety features often necessitate high-speed data transfer capabilities. Furthermore, the development of new automotive architectures that rely on Ethernet and high-speed data buses inherently favors optical fiber.

Challenges in the Optical Fiber For Automotive Sector

Despite its immense potential, the Optical Fiber for Automotive sector faces several significant challenges. High initial implementation costs for optical fiber infrastructure within vehicles, including specialized connectors and installation tools, remain a barrier to widespread adoption, particularly for lower-cost vehicle segments. Complexity in installation and repair, compared to the established methods for copper cabling, presents another hurdle for automotive manufacturers and service centers. Supply chain disruptions, as experienced globally, can impact the availability and pricing of raw materials and specialized components. Furthermore, established industry standards and legacy systems favoring copper wiring can create inertia and slow down the transition to optical fiber. The perceived fragility of optical fibers in the harsh automotive environment, although increasingly mitigated by technological advancements, can also be a concern for some stakeholders.

Emerging Opportunities in Optical Fiber For Automotive

The Optical Fiber for Automotive market is ripe with emerging opportunities. The rapid advancement of 5G technology and its integration into vehicles creates a demand for higher bandwidth and lower latency communication, a perfect fit for optical fiber. The burgeoning autonomous driving market, with its insatiable need for real-time data processing from multiple sensors, presents a massive opportunity for high-capacity optical fiber networks. Furthermore, the growing trend of in-vehicle connectivity and entertainment for passengers, including streaming services and augmented reality applications, will necessitate robust optical fiber backbones. The increasing focus on vehicle-to-everything (V2X) communication for enhanced safety and traffic management also relies heavily on the high-speed, reliable data transmission offered by optical fiber. The development of smart city initiatives that integrate vehicles into a larger connected ecosystem will further accelerate demand for advanced automotive networking.

Leading Players in the Optical Fiber For Automotive Market

- Timbercon

- AOS

- Corning

- WEINERT

- Fujikura

- TORAY INDUSTRIES

- TE Connectivity

- TX Plastic Optical Fibers

Key Developments in Optical Fiber For Automotive Industry

- 2023/Q4: Corning announces a new generation of lightweight, high-performance optical fiber cables designed for enhanced durability in automotive applications.

- 2024/Q1: TE Connectivity expands its portfolio of automotive-grade fiber optic connectors, focusing on miniaturization and ease of assembly.

- 2024/Q2: Fujikura showcases advancements in polymer optical fiber technology, enabling greater flexibility and cost-effectiveness for in-vehicle networks.

- 2024/Q3: Timbercon partners with a leading automotive Tier 1 supplier to integrate its optical fiber solutions into next-generation vehicle platforms.

- 2024/Q4: TX Plastic Optical Fibers introduces innovative fiber optic solutions optimized for high-speed data transfer in ADAS and infotainment systems.

- 2025/Q1: AOS reports significant progress in developing advanced fiber optic cabling that meets stringent automotive temperature and vibration requirements.

- 2025/Q2: WEINERT unveils new automated termination solutions for optical fiber in automotive manufacturing, reducing assembly times by millions of man-hours.

Future Outlook for Optical Fiber For Automotive Market

The future outlook for the Optical Fiber for Automotive market is exceptionally bright, projecting continued expansion and innovation. The relentless drive towards fully autonomous vehicles, coupled with the ever-increasing sophistication of in-car digital experiences, will serve as primary growth accelerators. Investments in next-generation vehicle architectures that leverage the high bandwidth and low latency of optical fiber are expected to surge. The market will witness a significant shift towards single-mode optical fiber as bandwidth demands escalate. Strategic opportunities lie in the development of integrated optical networking solutions, smart factory implementations for fiber optic cable production, and partnerships that streamline the adoption of optical fiber across the automotive value chain, promising a connected and intelligent automotive future.

Optical Fiber For Automotive Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Single-mode Optical Fiber

- 2.2. Multi-mode Optical Fiber

Optical Fiber For Automotive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Optical Fiber For Automotive Regional Market Share

Geographic Coverage of Optical Fiber For Automotive

Optical Fiber For Automotive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Single-mode Optical Fiber

- 5.2.2. Multi-mode Optical Fiber

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Single-mode Optical Fiber

- 6.2.2. Multi-mode Optical Fiber

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Single-mode Optical Fiber

- 7.2.2. Multi-mode Optical Fiber

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Single-mode Optical Fiber

- 8.2.2. Multi-mode Optical Fiber

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Single-mode Optical Fiber

- 9.2.2. Multi-mode Optical Fiber

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Optical Fiber For Automotive Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Single-mode Optical Fiber

- 10.2.2. Multi-mode Optical Fiber

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Timbercon

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AOS

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Corning

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 WEINERT

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fujikura

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TORAY INDUSTRIES

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 TE Connectivity

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TX Plastic Optical Fibers

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Timbercon

List of Figures

- Figure 1: Global Optical Fiber For Automotive Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Optical Fiber For Automotive Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Optical Fiber For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Optical Fiber For Automotive Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Optical Fiber For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Optical Fiber For Automotive Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Optical Fiber For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Optical Fiber For Automotive Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Optical Fiber For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Optical Fiber For Automotive Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Optical Fiber For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Optical Fiber For Automotive Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Optical Fiber For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Optical Fiber For Automotive Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Optical Fiber For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Optical Fiber For Automotive Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Optical Fiber For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Optical Fiber For Automotive Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Optical Fiber For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Optical Fiber For Automotive Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Optical Fiber For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Optical Fiber For Automotive Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Optical Fiber For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Optical Fiber For Automotive Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Optical Fiber For Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Optical Fiber For Automotive Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Optical Fiber For Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Optical Fiber For Automotive Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Optical Fiber For Automotive Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Optical Fiber For Automotive Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Optical Fiber For Automotive Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Optical Fiber For Automotive Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Optical Fiber For Automotive Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Optical Fiber For Automotive Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Optical Fiber For Automotive Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Optical Fiber For Automotive Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Optical Fiber For Automotive Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Optical Fiber For Automotive Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Optical Fiber For Automotive Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Optical Fiber For Automotive Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optical Fiber For Automotive?

The projected CAGR is approximately 12%.

2. Which companies are prominent players in the Optical Fiber For Automotive?

Key companies in the market include Timbercon, AOS, Corning, WEINERT, Fujikura, TORAY INDUSTRIES, TE Connectivity, TX Plastic Optical Fibers.

3. What are the main segments of the Optical Fiber For Automotive?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optical Fiber For Automotive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optical Fiber For Automotive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optical Fiber For Automotive?

To stay informed about further developments, trends, and reports in the Optical Fiber For Automotive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence