Key Insights

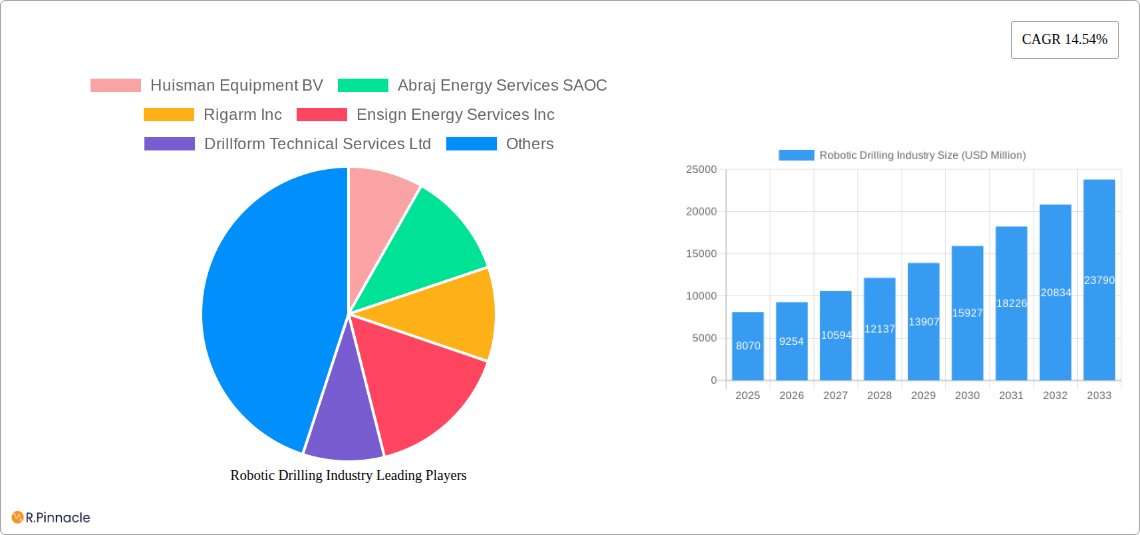

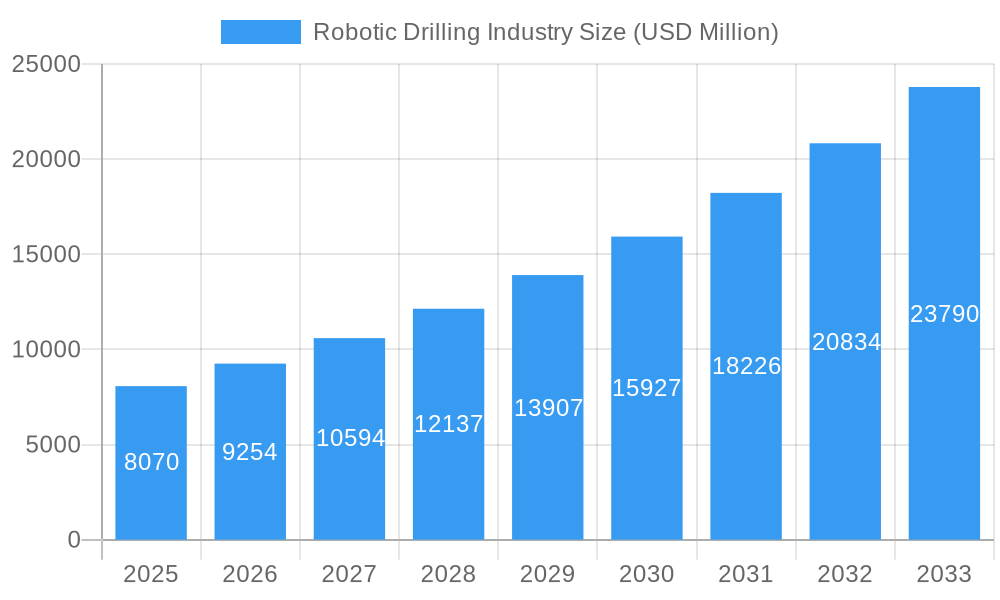

The global Robotic Drilling Industry is poised for substantial expansion, with a projected market size of $8.07 billion in 2025, driven by a compelling CAGR of 14.54% through 2033. This robust growth is fueled by the increasing demand for enhanced operational efficiency, reduced human intervention in hazardous environments, and the integration of advanced automation technologies in oil and gas exploration and production. Key market drivers include the imperative to improve safety standards, minimize human exposure to risk, and boost productivity through precise and consistent robotic operations. The industry is also benefiting from advancements in artificial intelligence, machine learning, and IoT, which are enabling more sophisticated autonomous drilling solutions. Furthermore, the continuous pursuit of cost optimization in exploration activities, coupled with the need to access challenging geological formations, further propels the adoption of robotic drilling systems.

Robotic Drilling Industry Market Size (In Billion)

The market is segmented into onshore and offshore deployments, with both segments exhibiting significant growth potential as companies seek to leverage automation across diverse operational landscapes. Hardware and software components are critical to the functionality of these robotic systems, with ongoing innovation in both areas contributing to market expansion. Prominent companies such as National-Oilwell Varco Inc., Nabors Industries Ltd., and Huisman Equipment BV are at the forefront of developing and deploying cutting-edge robotic drilling solutions. Emerging trends point towards increased adoption of AI-powered predictive maintenance for drilling equipment, the development of swarm robotics for complex drilling tasks, and the expansion of remote operational capabilities. While the substantial investment required for initial setup and the need for specialized skilled labor can be considered restraints, the long-term benefits in terms of safety, efficiency, and cost reduction are expected to outweigh these challenges, leading to sustained market penetration.

Robotic Drilling Industry Company Market Share

This in-depth report provides a definitive analysis of the global Robotic Drilling Industry, a sector poised for transformative growth driven by automation, safety enhancements, and efficiency gains. Spanning the historical period of 2019-2024, the base year of 2025, and extending through an extensive forecast period of 2025-2033, this research equips industry stakeholders with actionable intelligence. Discover intricate details on market structure, dynamics, regional dominance, product innovations, and key strategic developments shaping the future of automated drilling operations.

Robotic Drilling Industry Market Structure & Innovation Trends

The Robotic Drilling Industry exhibits a moderate to high degree of market concentration, with a few key players dominating the landscape while emerging companies are rapidly innovating. The primary innovation drivers revolve around enhancing operational efficiency, improving safety by removing personnel from hazardous zones, and reducing overall drilling costs. Regulatory frameworks are progressively adapting to accommodate advanced automation, though regional variations persist. Product substitutes are limited, primarily comprising conventional drilling methods, but the inherent advantages of robotics are steadily marginalizing them. End-user demographics are predominantly oil and gas exploration and production companies seeking to optimize their drilling operations. Merger and acquisition (M&A) activities are moderately prevalent, with companies seeking to acquire innovative technologies or expand their market reach. For instance, recent M&A deals have aimed at integrating advanced robotics and AI capabilities into existing drilling platforms, with deal values estimated to be in the high hundreds of millions to low billions. The market share of leading robotic drilling solution providers is continuously evolving, with significant investments being channeled into R&D for next-generation autonomous systems.

Robotic Drilling Industry Market Dynamics & Trends

The Robotic Drilling Industry is experiencing robust growth, propelled by a confluence of powerful market dynamics and evolving trends. The paramount growth driver is the escalating demand for enhanced operational efficiency and reduced costs in oil and gas extraction. Robotic drilling systems automate complex and repetitive tasks, leading to faster drilling times, improved wellbore accuracy, and minimized downtime. This translates directly into significant cost savings for E&P companies. Technological disruptions are at the forefront of this revolution. Advancements in artificial intelligence (AI), machine learning (ML), sensor technology, and advanced robotics are enabling the development of increasingly sophisticated and autonomous drilling rigs. These technologies facilitate real-time data analysis, predictive maintenance, and optimized drilling parameter adjustments, leading to unparalleled performance. Consumer preferences are shifting decisively towards solutions that prioritize safety and environmental responsibility. Robotic drilling significantly reduces human exposure to hazardous environments, thereby decreasing accident rates and improving worker well-being. Furthermore, optimized drilling processes contribute to a smaller environmental footprint. The competitive landscape is characterized by intense innovation and strategic partnerships. Established players are investing heavily in R&D to maintain their competitive edge, while new entrants are disrupting the market with novel solutions. The CAGR of the robotic drilling market is projected to be in the double digits, with market penetration expected to surge as the economic and safety benefits become more widely recognized. The ability to operate in remote and challenging terrains, coupled with the inherent precision of automated systems, further fuels market expansion. The ongoing digital transformation within the energy sector, encompassing the Industrial Internet of Things (IIoT) and data analytics, is intrinsically linked to the growth of robotic drilling, creating a synergistic ecosystem for innovation and deployment.

Dominant Regions & Segments in Robotic Drilling Industry

The Onshore Deployment segment is currently dominant within the Robotic Drilling Industry. This dominance is largely attributed to the widespread existing infrastructure, accessibility for technological integration, and the sheer volume of onshore drilling activities globally.

- Key Drivers for Onshore Dominance:

- Established Infrastructure: Extensive existing onshore oil and gas fields provide a ready market for robotic drilling solutions.

- Cost-Effectiveness: Onshore operations generally have lower logistical costs, making the initial investment in robotic systems more attractive.

- Technological Adoption: Oil and gas companies operating onshore are actively seeking ways to improve efficiency and safety, making them receptive to advanced automation.

- Skilled Workforce Availability: While robotics reduces the need for certain manual labor, the availability of a technically proficient workforce for operation and maintenance of robotic systems is crucial and often more readily available onshore.

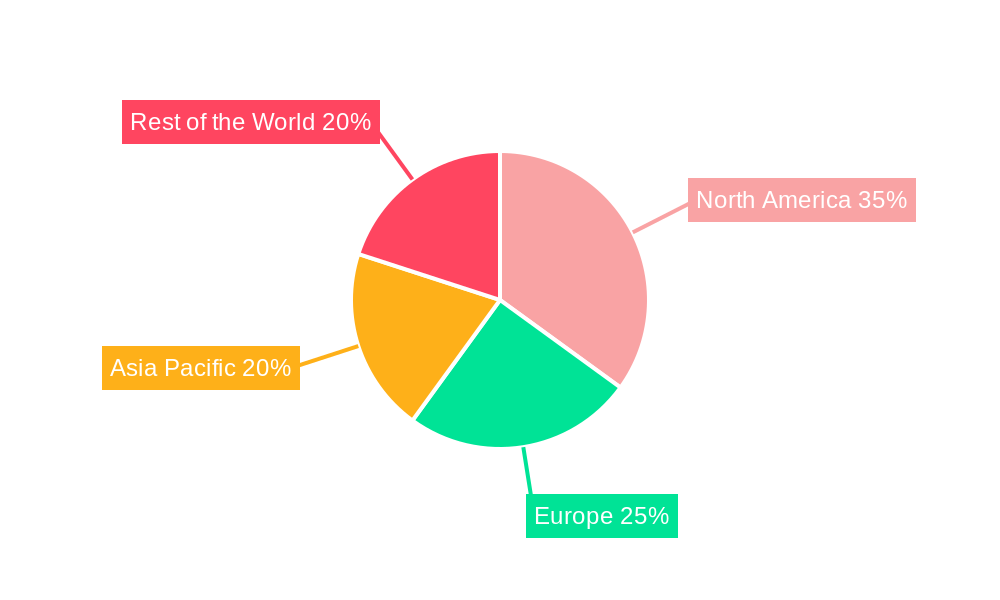

The North America region, particularly the United States, stands out as the leading geographical market for robotic drilling. This leadership is driven by its vast shale plays, significant investments in technological innovation, and a proactive regulatory environment that encourages the adoption of advanced drilling technologies. The economic policies in North America, coupled with the competitive nature of its oil and gas sector, foster rapid adoption of efficiency-enhancing solutions like robotic drilling. The strong presence of major oilfield service companies and drilling contractors, coupled with substantial capital expenditure in the upstream sector, further solidifies its leading position.

Within the Component segmentation, Hardware currently holds the larger market share, encompassing the physical robotic arms, automated drill string handling systems, remote-controlled equipment, and advanced sensor arrays. However, the Software segment is experiencing a faster growth rate, driven by the increasing sophistication of AI algorithms, machine learning for predictive analytics, drilling optimization software, and integrated control systems that are essential for the autonomous operation of these hardware components. The synergy between advanced hardware and intelligent software is critical for unlocking the full potential of robotic drilling.

Robotic Drilling Industry Product Innovations

Product innovations in the Robotic Drilling Industry are centered on enhancing autonomy, safety, and efficiency. Key developments include the integration of advanced AI and machine learning for real-time drilling optimization, predictive maintenance, and automated decision-making. Robotic arms are becoming more dexterous and capable of handling heavier loads, while improved sensor technologies provide real-time data on downhole conditions. The development of modular and scalable robotic drilling systems allows for greater flexibility in deployment across various well types and environments. These innovations offer significant competitive advantages by reducing operational costs, minimizing human exposure to hazardous environments, and improving drilling performance consistency.

Report Scope & Segmentation Analysis

This report provides a comprehensive market segmentation analysis of the Robotic Drilling Industry. The Deployment segment is divided into Onshore and Offshore. The Onshore segment, driven by vast existing infrastructure and cost-effectiveness, is projected to maintain a substantial market share throughout the forecast period, with growth fueled by continuous technological upgrades and efficiency demands. The Offshore segment, while currently smaller, is expected to witness robust growth as the industry seeks to deploy advanced robotic solutions in more challenging deepwater and harsh environments, driven by the need for enhanced safety and remote operation capabilities.

The Component segment is further bifurcated into Hardware and Software. The Hardware segment, encompassing the physical robotic systems and equipment, is a foundational element with steady growth anticipated. The Software segment, including AI, ML, and control systems, is forecast to experience a significantly higher compound annual growth rate due to its crucial role in enabling advanced automation and intelligent decision-making, directly impacting drilling efficiency and overall system performance.

Key Drivers of Robotic Drilling Industry Growth

The growth of the Robotic Drilling Industry is propelled by several key factors. Technological Advancements in AI, robotics, and sensor technology are enabling more sophisticated and autonomous drilling operations, leading to increased efficiency and precision. Enhanced Safety Standards are a significant driver, as robotic systems minimize human exposure to hazardous environments, reducing accident rates and associated costs. Economic Imperatives, such as the need to reduce operational expenditure and maximize hydrocarbon recovery, are pushing companies towards automation. Furthermore, Environmental Regulations promoting safer and more efficient drilling practices indirectly support the adoption of robotic solutions. The successful integration of these technologies by leading players like Nabors Industries Ltd, with its PACE-R801 automated rig, exemplifies the tangible benefits driving market expansion.

Challenges in the Robotic Drilling Industry Sector

Despite its promising outlook, the Robotic Drilling Industry faces several challenges. High Initial Investment Costs for advanced robotic systems can be a significant barrier for some companies, especially smaller operators. Integration Complexity with existing infrastructure and legacy systems can pose technical hurdles. Regulatory Hurdles and the need for standardized safety protocols for autonomous operations are still evolving in many regions. Cybersecurity Risks associated with connected and automated systems require robust protection measures. Lastly, Workforce Adaptation and the need for retraining skilled personnel to operate and maintain robotic equipment present a continuous challenge. Quantifiable impacts include potential delays in project timelines and increased risk if these challenges are not adequately addressed.

Emerging Opportunities in Robotic Drilling Industry

Emerging opportunities within the Robotic Drilling Industry are vast and transformative. The growing demand for autonomous drilling operations in remote and challenging environments, such as deepwater and Arctic regions, presents a significant growth avenue. Advancements in AI and machine learning offer opportunities for predictive maintenance, optimized drilling performance, and real-time operational adjustments, leading to substantial cost savings. The integration of digital twins and advanced simulation technologies can further enhance planning and execution. Furthermore, the increasing focus on decarbonization and ESG (Environmental, Social, and Governance) initiatives creates opportunities for robotic drilling solutions that offer greater efficiency and reduced environmental impact. The potential for unmanned drilling operations is also a key emerging trend.

Leading Players in the Robotic Drilling Industry Market

- Huisman Equipment BV

- Abraj Energy Services SAOC

- Rigarm Inc

- Ensign Energy Services Inc

- Drillform Technical Services Ltd

- Automated Rig Technologies Ltd

- Nabors Industries Ltd

- Drillmec Inc

- National-Oilwell Varco Inc

- Sekal AS

Key Developments in Robotic Drilling Industry Industry

- March 2021: Schlumberger secured a USD 480 million contract to drill 96 oil wells in southern Iraq for Basra Oil Company and ExxonMobil, highlighting the significant contracts being awarded for large-scale drilling projects that are increasingly incorporating advanced technologies.

- October 2021: Nabors Industries Ltd unveiled PACE-R801, the world's first fully automated land drilling rig integrated with Canrig robotics. This groundbreaking development achieved total depth on its inaugural well in the Permian Basin, featuring an unmanned rig floor designed to enhance crew safety and ensure consistent drilling performance.

Future Outlook for Robotic Drilling Industry Market

The future outlook for the Robotic Drilling Industry is exceptionally bright, marked by accelerated growth and strategic expansion. Continued advancements in artificial intelligence, machine learning, and sophisticated robotics will drive the development of fully autonomous drilling systems capable of operating with minimal human intervention. This will unlock new efficiencies, significantly reduce operational costs, and enhance safety profiles across the industry. The increasing global demand for energy, coupled with a stringent focus on optimizing production and minimizing environmental impact, will further propel the adoption of robotic drilling solutions. Opportunities for market penetration in unexplored regions and deepwater environments are expected to surge, driven by the technological capabilities of robotic systems to operate in extreme conditions. Strategic collaborations and acquisitions will continue to shape the market, fostering innovation and consolidating market leadership. The industry is poised for a period of sustained, high-paced growth, fundamentally transforming the landscape of oil and gas exploration and production.

Robotic Drilling Industry Segmentation

-

1. Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Component

- 2.1. Hardware

- 2.2. Software

Robotic Drilling Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Robotic Drilling Industry Regional Market Share

Geographic Coverage of Robotic Drilling Industry

Robotic Drilling Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Hardware

- 5.2.2. Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global Robotic Drilling Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Hardware

- 6.2.2. Software

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. North America Robotic Drilling Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Component

- 7.2.1. Hardware

- 7.2.2. Software

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Europe Robotic Drilling Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Component

- 8.2.1. Hardware

- 8.2.2. Software

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Asia Pacific Robotic Drilling Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Component

- 9.2.1. Hardware

- 9.2.2. Software

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Rest of the World Robotic Drilling Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. Onshore

- 10.1.2. Offshore

- 10.2. Market Analysis, Insights and Forecast - by Component

- 10.2.1. Hardware

- 10.2.2. Software

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Huisman Equipment BV

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Abraj Energy Services SAOC

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Rigarm Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Ensign Energy Services Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Drillform Technical Services Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Automated Rig Technologies Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Nabors Industries Ltd*List Not Exhaustive

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Drillmec Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 National-Oilwell Varco Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Sekal AS

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Huisman Equipment BV

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Robotic Drilling Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Robotic Drilling Industry Revenue (million), by Deployment 2025 & 2033

- Figure 3: North America Robotic Drilling Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: North America Robotic Drilling Industry Revenue (million), by Component 2025 & 2033

- Figure 5: North America Robotic Drilling Industry Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Robotic Drilling Industry Revenue (million), by Country 2025 & 2033

- Figure 7: North America Robotic Drilling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Robotic Drilling Industry Revenue (million), by Deployment 2025 & 2033

- Figure 9: Europe Robotic Drilling Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 10: Europe Robotic Drilling Industry Revenue (million), by Component 2025 & 2033

- Figure 11: Europe Robotic Drilling Industry Revenue Share (%), by Component 2025 & 2033

- Figure 12: Europe Robotic Drilling Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Europe Robotic Drilling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Robotic Drilling Industry Revenue (million), by Deployment 2025 & 2033

- Figure 15: Asia Pacific Robotic Drilling Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 16: Asia Pacific Robotic Drilling Industry Revenue (million), by Component 2025 & 2033

- Figure 17: Asia Pacific Robotic Drilling Industry Revenue Share (%), by Component 2025 & 2033

- Figure 18: Asia Pacific Robotic Drilling Industry Revenue (million), by Country 2025 & 2033

- Figure 19: Asia Pacific Robotic Drilling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Robotic Drilling Industry Revenue (million), by Deployment 2025 & 2033

- Figure 21: Rest of the World Robotic Drilling Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 22: Rest of the World Robotic Drilling Industry Revenue (million), by Component 2025 & 2033

- Figure 23: Rest of the World Robotic Drilling Industry Revenue Share (%), by Component 2025 & 2033

- Figure 24: Rest of the World Robotic Drilling Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Rest of the World Robotic Drilling Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Robotic Drilling Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 2: Global Robotic Drilling Industry Revenue million Forecast, by Component 2020 & 2033

- Table 3: Global Robotic Drilling Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Robotic Drilling Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 5: Global Robotic Drilling Industry Revenue million Forecast, by Component 2020 & 2033

- Table 6: Global Robotic Drilling Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Global Robotic Drilling Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 8: Global Robotic Drilling Industry Revenue million Forecast, by Component 2020 & 2033

- Table 9: Global Robotic Drilling Industry Revenue million Forecast, by Country 2020 & 2033

- Table 10: Global Robotic Drilling Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 11: Global Robotic Drilling Industry Revenue million Forecast, by Component 2020 & 2033

- Table 12: Global Robotic Drilling Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Global Robotic Drilling Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 14: Global Robotic Drilling Industry Revenue million Forecast, by Component 2020 & 2033

- Table 15: Global Robotic Drilling Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robotic Drilling Industry?

The projected CAGR is approximately 7.5%.

2. Which companies are prominent players in the Robotic Drilling Industry?

Key companies in the market include Huisman Equipment BV, Abraj Energy Services SAOC, Rigarm Inc, Ensign Energy Services Inc, Drillform Technical Services Ltd, Automated Rig Technologies Ltd, Nabors Industries Ltd*List Not Exhaustive, Drillmec Inc, National-Oilwell Varco Inc, Sekal AS.

3. What are the main segments of the Robotic Drilling Industry?

The market segments include Deployment, Component.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.46 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Higher Demand for Oil and Gas in the Country4.; Growing Infrastructure Development.

6. What are the notable trends driving market growth?

Onshore to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Competition from Renewable Energy.

8. Can you provide examples of recent developments in the market?

In March 2021, Schlumberger won a USD 480 million contract to drill 96 oil wells in southern Iraq for Basra Oil Company and ExxonMobil, which operates the giant West Qurna-1 field with partners from Iraq, Japan, Indonesia, and China.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Robotic Drilling Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Robotic Drilling Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Robotic Drilling Industry?

To stay informed about further developments, trends, and reports in the Robotic Drilling Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence