Key Insights

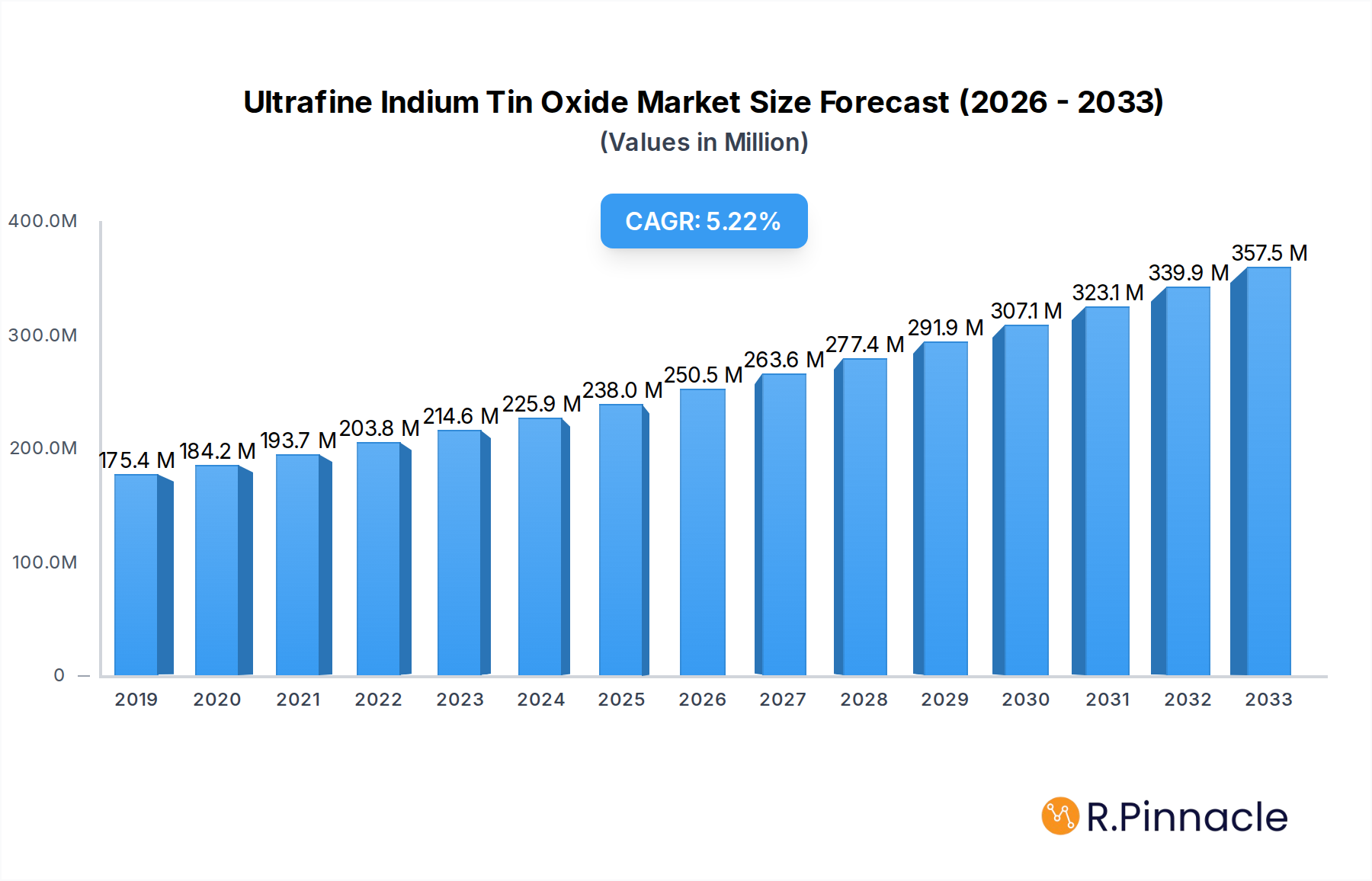

The global market for Ultrafine Indium Tin Oxide (ITO) is poised for robust expansion, driven by the escalating demand from the electronics and renewable energy sectors. The market is projected to reach a significant $229 million by 2025, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 5.6% through 2033. A primary catalyst for this growth is the indispensable role of ITO in the manufacturing of touch-screen sensors, which are increasingly integrated into smartphones, tablets, and a wide array of consumer electronics. Furthermore, the burgeoning photovoltaic industry, with its continuous pursuit of enhanced efficiency in solar cells, presents another substantial growth avenue for ultrafine ITO. The technological advancements leading to higher purity levels, particularly in the >99.99% range, are crucial for meeting the stringent performance requirements of these advanced applications.

Ultrafine Indium Tin Oxide Market Size (In Million)

While the market benefits from strong demand drivers, it also navigates certain challenges. The volatility in the pricing and availability of raw materials like indium can impact profit margins and necessitate strategic sourcing. Supply chain disruptions, as observed in recent years, could also pose short-term hurdles. However, the ongoing innovation in material science, exploring alternative transparent conductive materials, is a long-term trend to monitor, though ITO's established performance and cost-effectiveness in many critical applications ensure its continued dominance. The market segments, categorized by application and purity, reveal a dynamic landscape. Flat Panel Displays and Touch-screen Sensors are expected to remain the leading applications, with a growing emphasis on higher purity ITO for next-generation devices. Regionally, Asia Pacific, particularly China, is anticipated to lead market share due to its extensive manufacturing base in electronics and solar energy.

Ultrafine Indium Tin Oxide Company Market Share

Ultrafine Indium Tin Oxide Market Structure & Innovation Trends

The ultrafine Indium Tin Oxide (ITO) market exhibits a dynamic structure characterized by both concentrated innovation and a broad distribution of specialized manufacturers. Leading companies like Umicore and Guangxi Crystal Union Photoelectric Materials are at the forefront of technological advancements, driving the demand for high-purity ITO for cutting-edge applications. Innovation in synthesis techniques, particle size control, and surface functionalization is a key differentiator, pushing the boundaries of performance in Flat Panel Displays, Touch-screen Sensors, and Photovoltaic Cells. Regulatory frameworks, particularly those concerning hazardous materials and sustainable manufacturing practices, are increasingly influencing product development and market entry strategies. The availability of product substitutes, such as alternative transparent conductive films, poses a moderate threat, necessitating continuous innovation in ITO's cost-effectiveness and performance. End-user demographics, dominated by consumer electronics manufacturers, dictate stringent quality and consistency requirements. Mergers and acquisitions (M&A) activities, while not pervasive, are strategically focused on acquiring niche technologies or expanding market reach. For instance, a recent M&A deal in the past, involving a specialized nano-ITO provider and a larger materials conglomerate, was valued at approximately XX million dollars, signifying a consolidation of intellectual property and production capacity in key growth segments. Understanding these structural elements is crucial for navigating the competitive landscape and identifying strategic growth avenues within the ultrafine ITO sector.

Ultrafine Indium Tin Oxide Market Dynamics & Trends

The ultrafine Indium Tin Oxide (ITO) market is poised for significant expansion, propelled by an escalating demand across its diverse application spectrum. The primary growth driver is the burgeoning consumer electronics industry, particularly the ever-growing demand for advanced Flat Panel Displays (FPDs) and interactive Touch-screen Sensors. These applications necessitate the unique optical and electrical properties of ultrafine ITO, such as high transparency and excellent conductivity. Furthermore, the increasing global focus on renewable energy sources is significantly boosting the demand for ITO in Photovoltaic Cells, where it plays a crucial role in efficient light absorption and charge collection. The market penetration of these technologies, coupled with an anticipated Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025-2033), underscores the robust growth trajectory. Technological disruptions, including advancements in sputtering techniques, atomic layer deposition (ALD), and the development of novel ITO precursor materials, are continuously enhancing the performance and reducing the cost of ultrafine ITO production. Consumer preferences are shifting towards thinner, more flexible, and higher-resolution displays, creating a continuous need for ITO with improved uniformity, lower resistance, and enhanced durability. The competitive dynamics are characterized by a blend of established global players and emerging regional manufacturers, each vying for market share through product innovation, strategic partnerships, and cost optimization. The rising cost and limited availability of indium, a key raw material, also present a significant trend, prompting research and development into indium-reduced or indium-free alternatives, though ultrafine ITO remains the benchmark for many high-performance applications. The market is also witnessing a growing emphasis on sustainable manufacturing processes and the recycling of indium, driven by environmental concerns and regulatory pressures.

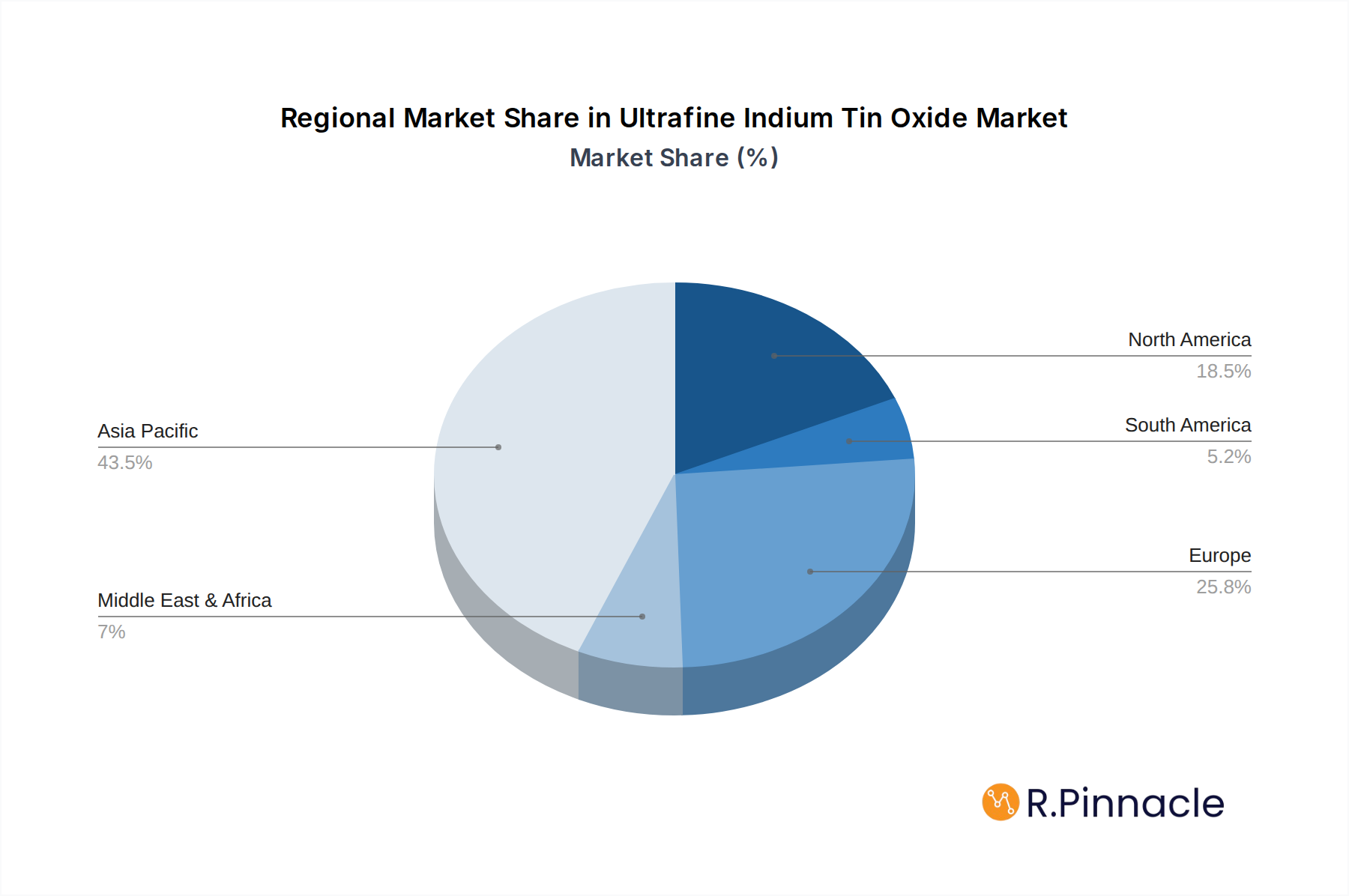

Dominant Regions & Segments in Ultrafine Indium Tin Oxide

The Asia-Pacific region stands as the undisputed dominant force in the ultrafine Indium Tin Oxide (ITO) market, driven by its robust manufacturing capabilities and insatiable demand from the electronics sector. Within this region, China emerges as the leading country, benefiting from a highly developed industrial ecosystem and significant government support for high-tech material production. The dominance of Asia-Pacific is further amplified by the leading application segment: Flat Panel Display (FPD). This segment accounts for the largest market share, estimated at over XX million dollars in 2025, due to the sheer volume of production for televisions, smartphones, tablets, and monitors. Key drivers for this segment's dominance include:

- Economies of Scale: Extensive manufacturing infrastructure in countries like South Korea, Japan, and China allows for cost-effective mass production of FPDs, subsequently driving demand for ultrafine ITO.

- Technological Prowess: Leading display manufacturers in the region continuously invest in R&D, pushing the boundaries of display technology and demanding higher-performance ITO.

- Consumer Electronics Hub: Asia-Pacific is the global epicenter for consumer electronics manufacturing and consumption, creating a sustained and growing market for FPDs.

In terms of product Type, the Purity: >99.99% segment holds a significant lead. This high-purity variant is essential for advanced applications where minimal impurities are critical for optimal optical and electrical performance, particularly in high-end FPDs and sensitive touch sensors. Key drivers for this segment's dominance include:

- Performance Requirements: The ever-increasing resolution and responsiveness demands of modern electronic devices necessitate the superior conductivity and transparency offered by >99.99% pure ITO.

- Technological Advancements: Innovations in manufacturing processes, such as advanced sputtering techniques, enable the consistent production of ultrafine ITO with exceptionally high purity levels.

- Market Premium: Higher purity ITO commands a premium price, reflecting its specialized manufacturing process and critical role in high-value electronic components.

The Touch-screen Sensor application segment also exhibits strong growth, fueled by the pervasive adoption of smartphones and tablets globally. While FPDs lead, touch sensors represent a substantial and expanding market for ultrafine ITO, with an estimated market size of over XX million dollars in 2025. The Photovoltaic Cells segment, though currently smaller in comparison, is experiencing rapid growth due to the global push for sustainable energy solutions, with an estimated market size of over XX million dollars in 2025. The "Others" category for both Application and Type encompasses niche markets and emerging technologies, which are expected to contribute to overall market diversification and future growth.

Ultrafine Indium Tin Oxide Product Innovations

Ultrafine Indium Tin Oxide (ITO) product innovations are primarily focused on enhancing transparency, conductivity, and flexibility for next-generation electronic devices. Developments include novel sputtering targets that enable lower deposition temperatures, crucial for flexible substrates, and improved nano-ITO powders with precisely controlled particle sizes for enhanced ink formulations in printed electronics. Competitive advantages are being gained through the development of indium-reduced or indium-free alternatives, addressing raw material cost volatility. These advancements cater to emerging applications in transparent flexible displays, advanced touch interfaces, and high-efficiency solar cells, ensuring ITO's continued relevance in a rapidly evolving technological landscape.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Ultrafine Indium Tin Oxide (ITO) market, segmented by Application and Type. The Application segmentation includes: Flat Panel Display, Touch-screen Sensor, Photovoltaic Cells, and Others. The Flat Panel Display segment is projected to experience significant growth, driven by the demand for high-resolution displays in consumer electronics, with an estimated market size of XX million dollars in 2025. The Touch-screen Sensor segment is also poised for robust expansion, fueled by the ubiquitous adoption of interactive devices, with an estimated market size of XX million dollars in 2025. The Photovoltaic Cells segment, while currently smaller, is expected to see substantial growth due to the increasing focus on renewable energy, estimated at XX million dollars in 2025. The Others application segment encompasses emerging and niche uses, contributing to market diversification.

The Type segmentation covers: Purity: >99.9%, Purity: >99.99%, and Others. The Purity: >99.9% segment caters to a broad range of industrial applications where high transparency and conductivity are required, with an estimated market size of XX million dollars in 2025. The Purity: >99.99% segment is critical for high-performance applications demanding exceptional optical clarity and electrical performance, particularly in advanced displays and sensors, estimated at XX million dollars in 2025. The Others type category includes specialized ITO formulations and custom purities, offering flexibility for unique market needs. Competitive dynamics within each segment are driven by technological advancements, cost-effectiveness, and supply chain reliability.

Key Drivers of Ultrafine Indium Tin Oxide Growth

The growth of the Ultrafine Indium Tin Oxide (ITO) market is primarily driven by several interconnected factors. Technologically, the relentless advancement in the display industry, particularly the demand for higher resolution, flexibility, and energy efficiency in Flat Panel Displays and Touch-screen Sensors, is a core accelerator. The increasing adoption of photovoltaic technology for sustainable energy solutions fuels demand in the Photovoltaic Cells segment. Economically, the growing global middle class and their increasing purchasing power for consumer electronics, especially in emerging economies, translate into higher unit sales of devices requiring ITO. Regulatory factors, while sometimes posing challenges, can also drive growth by promoting the adoption of energy-efficient technologies (like advanced displays) and encouraging the development of more sustainable manufacturing processes, which can lead to innovative and cost-effective ITO production methods. The expanding use of ITO in smart devices, wearables, and augmented reality applications further contributes to its market expansion.

Challenges in the Ultrafine Indium Tin Oxide Sector

The Ultrafine Indium Tin Oxide (ITO) sector faces several significant challenges that can impact market growth. The primary restraint is the volatility in the price and availability of indium, a critical and finite raw material. Fluctuations in indium prices can directly affect the cost of ITO production, impacting its competitiveness and market penetration, potentially leading to an estimated XX% increase in raw material costs over the forecast period. Supply chain disruptions, geopolitical instability, and the concentration of indium mining in a few geographical locations exacerbate these concerns. Furthermore, the development and increasing adoption of alternative transparent conductive materials, such as graphene, silver nanowires, and conductive polymers, pose a competitive threat, especially in applications where cost is a primary driver. Regulatory hurdles related to environmental compliance and waste management in the production process can also add to operational costs and complexity. Finally, achieving consistent uniformity and defect-free deposition of ultrafine ITO, especially on large-area or flexible substrates, remains a technical challenge for manufacturers, potentially limiting yield and increasing production costs by up to XX%.

Emerging Opportunities in Ultrafine Indium Tin Oxide

Emerging opportunities in the Ultrafine Indium Tin Oxide (ITO) market are centered around technological advancements and expanding application horizons. The growing demand for flexible and transparent electronics, including foldable smartphones, rollable displays, and wearable devices, presents a significant opportunity for ITO with improved mechanical properties and deposition techniques suitable for plastic substrates. The continued expansion of the Internet of Things (IoT) ecosystem, with its myriad of sensor applications, offers new avenues for ultrafine ITO utilization. Furthermore, advancements in quantum dot displays and micro-LED technology require highly specialized transparent conductive films, creating opportunities for innovative ITO formulations with tailored optical and electrical characteristics. The development of more sustainable and cost-effective ITO production methods, including recycling initiatives for indium, can unlock new market segments and enhance competitiveness. The exploration of ITO in novel areas like smart windows, automotive displays, and advanced medical imaging devices also represents untapped potential, promising substantial market growth in the coming years.

Leading Players in the Ultrafine Indium Tin Oxide Market

- Umicore

- Guangxi Crystal Union Photoelectric Materials

- ENAM OPTOELECTRONIC MATERIAL

- Nanoshel

- FUS NANO

- Otto Chemie Pvt. Ltd

- SAT nano Technology Material Co., Ltd.

- Anhui Fitech Materials Co.,Ltd

- Konada New Materials Technology Co.,Ltd

- Guangzhou Hongwu Material Technology Co., Ltd.

Key Developments in Ultrafine Indium Tin Oxide Industry

- 2023 Q4: Launch of enhanced sputtering targets for flexible display applications by Umicore, improving deposition efficiency and reducing costs.

- 2023 Q3: Nanoshel announces a new range of high-purity ITO nanopowders with controlled particle sizes for advanced ink formulations.

- 2023 Q2: Guangxi Crystal Union Photoelectric Materials expands production capacity for high-purity ITO to meet the growing demand from the FPD sector.

- 2022 Q4: SAT nano Technology Material Co., Ltd. collaborates with a research institution to explore ITO's potential in next-generation photovoltaic cells.

- 2022 Q3: ENAM OPTOELECTRONIC MATERIAL introduces a novel ITO solution for enhanced touch response in automotive displays.

- 2021 Q4: FUS NANO develops a new method for synthesizing ultrafine ITO with improved structural integrity for flexible electronics.

- 2021 Q3: Otto Chemie Pvt. Ltd. announces a strategic partnership to enhance the supply chain for indium-based materials.

- 2020 Q4: Anhui Fitech Materials Co.,Ltd focuses on developing environmentally friendly production processes for ultrafine ITO.

- 2020 Q3: Konada New Materials Technology Co.,Ltd introduces a cost-effective ITO solution for emerging market applications.

- 2019 Q4: Guangzhou Hongwu Material Technology Co., Ltd. showcases advancements in ITO for transparent conductive coatings in diverse industrial uses.

Future Outlook for Ultrafine Indium Tin Oxide Market

The future outlook for the Ultrafine Indium Tin Oxide (ITO) market is characterized by sustained growth and technological evolution. The increasing demand for high-performance displays in smartphones, tablets, and televisions, coupled with the burgeoning adoption of flexible electronics, will continue to be primary growth accelerators. The expanding renewable energy sector, with its growing reliance on efficient photovoltaic cells, provides a robust and expanding market for ITO. Strategic opportunities lie in the development of indium-optimized or indium-reduced ITO formulations to mitigate raw material cost volatility and enhance sustainability. Innovations in deposition techniques for flexible and large-area applications will be crucial for market leadership. Furthermore, the exploration of ITO's potential in emerging fields like advanced optics, smart textiles, and bio-integrated electronics presents significant long-term growth prospects, ensuring the continued relevance and expansion of the ultrafine ITO market.

Ultrafine Indium Tin Oxide Segmentation

-

1. Application

- 1.1. Flat Panel Display

- 1.2. Touch-screen Sensor

- 1.3. Photovoltaic Cells

- 1.4. Others

-

2. Type

- 2.1. Purity: >99.9%

- 2.2. Purity: >99.99%

- 2.3. Others

Ultrafine Indium Tin Oxide Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ultrafine Indium Tin Oxide Regional Market Share

Geographic Coverage of Ultrafine Indium Tin Oxide

Ultrafine Indium Tin Oxide REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Flat Panel Display

- 5.1.2. Touch-screen Sensor

- 5.1.3. Photovoltaic Cells

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Purity: >99.9%

- 5.2.2. Purity: >99.99%

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Flat Panel Display

- 6.1.2. Touch-screen Sensor

- 6.1.3. Photovoltaic Cells

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Purity: >99.9%

- 6.2.2. Purity: >99.99%

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Flat Panel Display

- 7.1.2. Touch-screen Sensor

- 7.1.3. Photovoltaic Cells

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Purity: >99.9%

- 7.2.2. Purity: >99.99%

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Flat Panel Display

- 8.1.2. Touch-screen Sensor

- 8.1.3. Photovoltaic Cells

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Purity: >99.9%

- 8.2.2. Purity: >99.99%

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Flat Panel Display

- 9.1.2. Touch-screen Sensor

- 9.1.3. Photovoltaic Cells

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Purity: >99.9%

- 9.2.2. Purity: >99.99%

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ultrafine Indium Tin Oxide Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Flat Panel Display

- 10.1.2. Touch-screen Sensor

- 10.1.3. Photovoltaic Cells

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Purity: >99.9%

- 10.2.2. Purity: >99.99%

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Umicore

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Guangxi Crystal Union Photoelectric Materials

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ENAM OPTOELECTRONIC MATERIAL

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nanoshel

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 FUS NANO

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Otto Chemie Pvt. Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 SAT nano Technology Material Co. Ltd.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Anhui Fitech Materials Co.Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Konada New Materials Technology Co.Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Guangzhou Hongwu Material Technology Co. Ltd.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Umicore

List of Figures

- Figure 1: Global Ultrafine Indium Tin Oxide Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Ultrafine Indium Tin Oxide Revenue (million), by Application 2025 & 2033

- Figure 3: North America Ultrafine Indium Tin Oxide Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ultrafine Indium Tin Oxide Revenue (million), by Type 2025 & 2033

- Figure 5: North America Ultrafine Indium Tin Oxide Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ultrafine Indium Tin Oxide Revenue (million), by Country 2025 & 2033

- Figure 7: North America Ultrafine Indium Tin Oxide Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ultrafine Indium Tin Oxide Revenue (million), by Application 2025 & 2033

- Figure 9: South America Ultrafine Indium Tin Oxide Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ultrafine Indium Tin Oxide Revenue (million), by Type 2025 & 2033

- Figure 11: South America Ultrafine Indium Tin Oxide Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ultrafine Indium Tin Oxide Revenue (million), by Country 2025 & 2033

- Figure 13: South America Ultrafine Indium Tin Oxide Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ultrafine Indium Tin Oxide Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Ultrafine Indium Tin Oxide Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ultrafine Indium Tin Oxide Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Ultrafine Indium Tin Oxide Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ultrafine Indium Tin Oxide Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Ultrafine Indium Tin Oxide Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ultrafine Indium Tin Oxide Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ultrafine Indium Tin Oxide Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ultrafine Indium Tin Oxide Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ultrafine Indium Tin Oxide Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ultrafine Indium Tin Oxide Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ultrafine Indium Tin Oxide Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ultrafine Indium Tin Oxide Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Ultrafine Indium Tin Oxide Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ultrafine Indium Tin Oxide Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Ultrafine Indium Tin Oxide Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ultrafine Indium Tin Oxide Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Ultrafine Indium Tin Oxide Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Ultrafine Indium Tin Oxide Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ultrafine Indium Tin Oxide Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ultrafine Indium Tin Oxide?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Ultrafine Indium Tin Oxide?

Key companies in the market include Umicore, Guangxi Crystal Union Photoelectric Materials, ENAM OPTOELECTRONIC MATERIAL, Nanoshel, FUS NANO, Otto Chemie Pvt. Ltd, SAT nano Technology Material Co., Ltd., Anhui Fitech Materials Co.,Ltd, Konada New Materials Technology Co.,Ltd, Guangzhou Hongwu Material Technology Co., Ltd..

3. What are the main segments of the Ultrafine Indium Tin Oxide?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 229 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ultrafine Indium Tin Oxide," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ultrafine Indium Tin Oxide report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ultrafine Indium Tin Oxide?

To stay informed about further developments, trends, and reports in the Ultrafine Indium Tin Oxide, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence