Key Insights

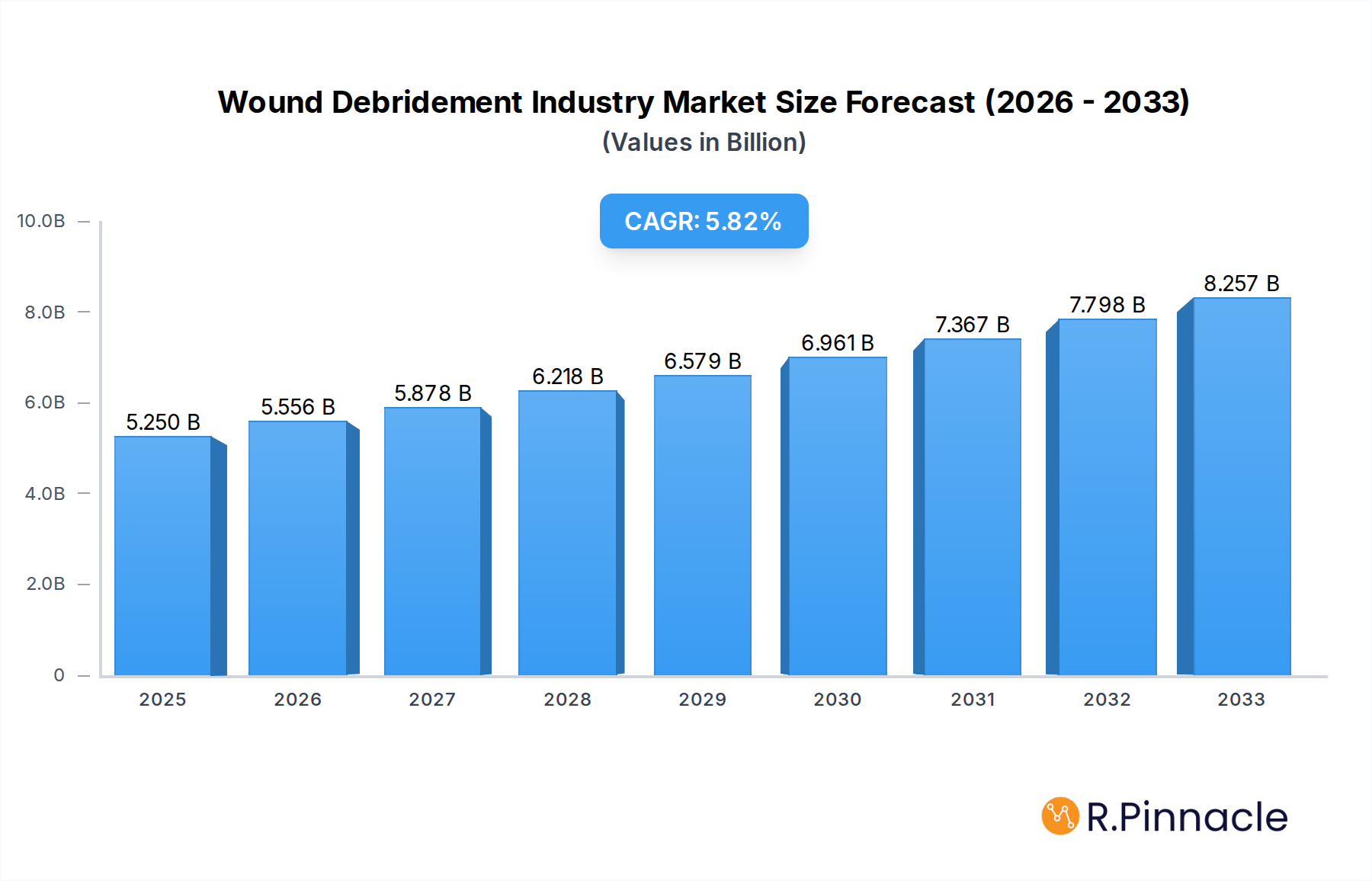

The Wound Debridement Industry is poised for significant expansion, projected to reach a robust $5.25 billion by 2025. This growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 5.97% through 2033, indicating a sustained upward trajectory. A primary driver for this market's ascent is the increasing prevalence of chronic wounds, such as diabetic foot ulcers, venous leg ulcers, and pressure ulcers. These conditions, often exacerbated by an aging global population and rising rates of lifestyle diseases like diabetes and obesity, necessitate advanced debridement techniques for effective healing. Furthermore, the rising incidence of acute wounds, stemming from surgical procedures and trauma, also contributes to market demand. The development and adoption of innovative debridement products, including enzymatic and mechanical solutions, are crucial in facilitating tissue regeneration and preventing infection, thereby fueling market expansion.

Wound Debridement Industry Market Size (In Billion)

The market landscape is characterized by a diverse range of product segments, with collagenase and papain products holding substantial market share due to their targeted enzymatic action and efficacy in breaking down necrotic tissue. The "Others" category, encompassing advanced wound care technologies and multi-functional dressings, is also witnessing considerable growth. End-user segments are dominated by hospitals, which are the primary sites for complex wound management, followed by homecare services as patients are increasingly treated outside traditional clinical settings. Key industry players like Coloplast Corp, Smith & Nephew, and Integra LifeSciences Corporation are actively engaged in research and development, strategic collaborations, and geographical expansion to capitalize on these growth opportunities. While the market is robust, potential restraints such as the high cost of advanced debridement therapies and the need for specialized training for healthcare professionals could present challenges.

Wound Debridement Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global wound debridement market, projected to reach billions by 2033. Leveraging high-ranking keywords such as wound care, chronic wound management, acute wound treatment, surgical debridement, non-surgical debridement, and biologics, this study is meticulously designed for industry professionals seeking actionable insights and strategic guidance. Our analysis spans a detailed historical period (2019-2024), a base year (2025), and an extensive forecast period (2025-2033), providing a robust understanding of current trends and future potential.

Wound Debridement Industry Market Structure & Innovation Trends

The wound debridement market is characterized by a moderate to high level of concentration, driven by a select group of key players who dominate a significant portion of the market share, estimated to be in the hundreds of billions of dollars. Innovation is a primary growth driver, with companies continuously investing in research and development to introduce advanced debridement techniques and products. The regulatory landscape, overseen by bodies like the FDA and EMA, plays a crucial role in product approval and market access, ensuring patient safety and efficacy. While product substitutes, such as advanced wound dressings that promote autolytic debridement, exist, they often complement rather than entirely replace traditional debridement methods. End-user demographics are shifting, with an increasing demand from homecare settings alongside established hospital-based treatments. Merger and acquisition (M&A) activities are prevalent, with deal values frequently reaching hundreds of millions to billions of dollars, as larger companies seek to expand their portfolios and market reach.

- Market Concentration: Dominated by a few leading multinational corporations.

- Innovation Drivers: Development of novel enzymatic, autolytic, and mechanical debridement solutions.

- Regulatory Frameworks: Strict guidelines for product efficacy and safety.

- Product Substitutes: Growing adoption of advanced wound dressings.

- End-User Demographics: Increasing demand from homecare and chronic care facilities.

- M&A Activities: Strategic acquisitions to enhance product portfolios and market presence, with deal values in the hundreds of millions to billions.

Wound Debridement Industry Market Dynamics & Trends

The wound debridement market is experiencing robust growth, propelled by several key dynamics. The increasing prevalence of chronic diseases such as diabetes and peripheral vascular disease, which contribute to the development of chronic wounds, is a significant market expansion driver. This demographic shift, coupled with an aging global population, leads to a higher incidence of non-healing wounds requiring effective debridement. Technological advancements are revolutionizing debridement methods, moving towards less invasive and more precise techniques. Enzymatic debridement and biological debridement products are gaining traction due to their targeted action and reduced patient discomfort compared to traditional surgical methods. The rising healthcare expenditure worldwide, particularly in developed economies, further fuels market growth, enabling greater access to advanced wound care solutions. Consumer preferences are also evolving, with a growing emphasis on patient comfort, faster healing times, and reduced scarring, pushing manufacturers to develop innovative, patient-centric products.

The competitive landscape is dynamic, with established players and emerging startups vying for market share. Companies are focusing on expanding their product portfolios to cater to a wider range of wound types and patient needs. The penetration of advanced debridement products is steadily increasing as healthcare providers become more aware of their benefits and cost-effectiveness in the long run by reducing complications and hospital stays. The CAGR (Compound Annual Growth Rate) for this market is robust, estimated to be in the high single digits, indicating sustained expansion. Furthermore, the increasing adoption of these technologies in homecare settings signifies a crucial trend, driven by the desire for convenient and effective wound management outside of traditional clinical environments. The market is also influenced by the growing understanding of the critical role of timely and effective debridement in preventing infection, reducing healing time, and improving patient outcomes, all contributing to a positive growth trajectory estimated to exceed billions in value.

Dominant Regions & Segments in Wound Debridement Industry

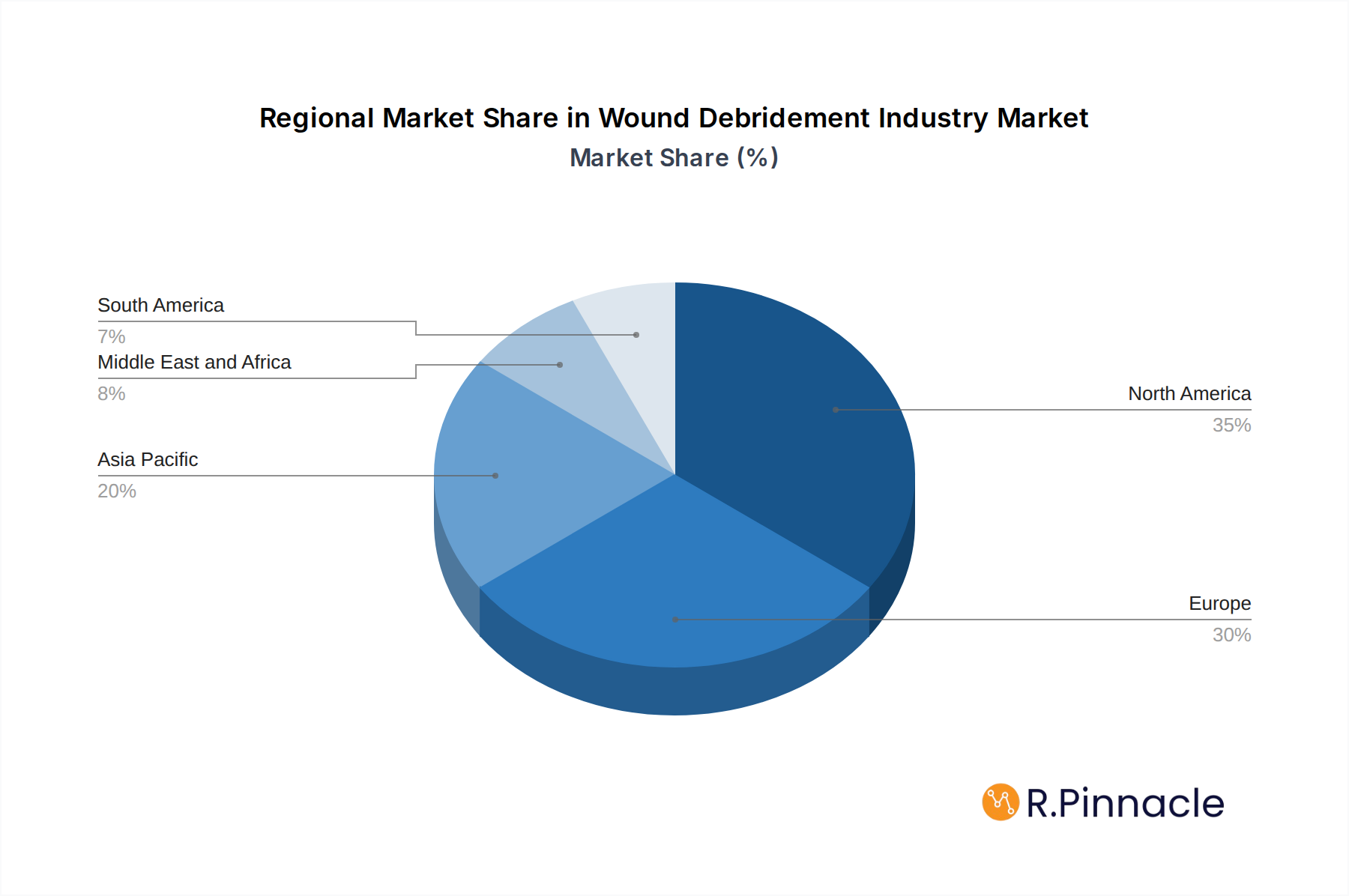

North America currently holds a dominant position in the global wound debridement market, driven by a high prevalence of chronic diseases, advanced healthcare infrastructure, and significant investment in research and development. The United States, in particular, accounts for a substantial portion of the market share, estimated in the tens of billions.

- Dominant Region: North America

- Key Drivers:

- High prevalence of diabetes, cardiovascular diseases, and obesity, leading to increased incidence of chronic wounds.

- Advanced healthcare infrastructure and widespread adoption of innovative wound care technologies.

- Strong government initiatives and funding for wound care research and patient education.

- Reimbursement policies that favor effective wound management solutions.

- Presence of major wound debridement product manufacturers and research institutions.

- Detailed Dominance Analysis: The robust demand for effective wound management solutions, coupled with the accessibility of cutting-edge technologies and a patient population with a high burden of chronic conditions, solidifies North America's lead. The market here is characterized by significant spending on both hospital-based and homecare debridement products, contributing billions to the global market value.

- Key Drivers:

Segments Driving Market Growth:

Type: Chronic Wounds

- Key Drivers:

- Aging population and rising rates of lifestyle-related diseases like diabetes and obesity.

- Longer treatment durations and complexity of managing chronic wounds, such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers.

- Increased awareness of the importance of effective debridement in preventing complications and promoting healing.

- Detailed Dominance Analysis: Chronic wounds represent the largest segment by volume and value within the wound debridement market. The prolonged nature of these wounds necessitates ongoing and often multiple debridement procedures, leading to sustained demand for a variety of debridement products and services. The market for chronic wound debridement is valued in the tens of billions.

- Key Drivers:

Product: Collagenase Product

- Key Drivers:

- High efficacy in breaking down collagen in necrotic tissue, promoting wound bed preparation.

- Growing clinical evidence supporting their use in various wound types.

- Availability of established brands and increasing R&D for improved formulations.

- Detailed Dominance Analysis: Collagenase-based debridement products are a cornerstone of enzymatic debridement therapies. Their ability to selectively target and degrade devitalized tissue without harming healthy cells makes them highly desirable for clinicians. The market for collagenase products is substantial, contributing billions to the overall wound debridement market.

- Key Drivers:

End-User: Hospitals

- Key Drivers:

- Centralized patient care for complex wounds and post-surgical cases.

- Availability of a wide range of debridement modalities and specialist expertise.

- Higher volume of procedures and larger budgets for wound care supplies.

- Detailed Dominance Analysis: Hospitals remain a primary end-user segment for wound debridement products and services. The complexity of cases treated in inpatient settings, including severe trauma, burns, and surgical site infections, requires advanced debridement techniques and a continuous supply of specialized products. This segment consistently generates billions in revenue for the wound debridement industry.

- Key Drivers:

Wound Debridement Industry Product Innovations

Recent product developments in wound debridement focus on enhancing efficacy, reducing patient discomfort, and improving ease of use for clinicians. Innovations include novel enzymatic formulations with broader substrate specificity, advanced biological debridement agents derived from natural sources, and sophisticated mechanical debridement devices offering greater precision. These advancements aim to accelerate wound healing, minimize scar formation, and reduce the risk of infection. The competitive advantage lies in products that demonstrate faster healing times, improved patient outcomes, and cost-effectiveness in managing complex wounds, all of which are critical for market penetration and expansion into billions in global market value.

Report Scope & Segmentation Analysis

This report segments the wound debridement market across Type (Chronic Wounds, Acute Wounds), Product (Collagenase Product, Papain Product, Others), and End-User (Hospitals, Homecare, Others).

- Chronic Wounds: This segment is expected to exhibit significant growth due to the rising incidence of diabetes and an aging population, leading to sustained demand for effective debridement solutions. Market size in this segment is projected to reach billions by 2033.

- Acute Wounds: While generally shorter in duration, acute wounds from trauma or surgery still represent a substantial market, requiring efficient debridement for optimal healing. Growth is steady, contributing billions annually.

- Collagenase Product: This category is a leading segment due to its established efficacy and widespread use in preparing wound beds. Its market share is in the billions, with ongoing innovation.

- Papain Product: Papain-based debridement agents are gaining recognition for their enzymatic properties, offering an alternative for specific wound types. This segment is growing, with potential to reach hundreds of millions.

- Others: This encompasses a variety of debridement products, including mechanical devices, hydrogels, and other enzymatic formulations, contributing significantly to the market's diversification and overall billions in value.

- Hospitals: As a primary care setting for complex wounds, hospitals represent a major market segment, with consistent demand for debridement products and services, contributing billions in revenue.

- Homecare: The growing trend of in-home patient care fuels the demand for user-friendly and effective debridement solutions, representing a rapidly expanding segment with substantial growth potential, reaching hundreds of millions.

- Others: This includes clinics, long-term care facilities, and specialized wound care centers, collectively forming a growing segment that contributes to the market's overall expansion into billions.

Key Drivers of Wound Debridement Industry Growth

The wound debridement market is propelled by several interconnected factors that ensure its sustained growth into the billions.

- Technological Advancements: The development of novel enzymatic, biological, and mechanical debridement methods that offer improved efficacy, patient comfort, and reduced healing times is a primary driver. For example, the introduction of highly selective enzymatic debriders can revolutionize the treatment of sensitive wound areas.

- Increasing Prevalence of Chronic Diseases: A global surge in conditions like diabetes, obesity, and cardiovascular disease directly correlates with a rise in chronic wounds, such as diabetic foot ulcers and venous leg ulcers, creating a consistent demand for debridement.

- Aging Global Population: As the proportion of the elderly population grows, so does the incidence of age-related conditions that impair healing and increase the risk of chronic wounds, thereby expanding the market.

- Growing Awareness and Education: Increased understanding among healthcare professionals and patients about the critical role of timely and effective debridement in preventing complications, reducing infection rates, and accelerating healing is a significant catalyst.

Challenges in the Wound Debridement Industry Sector

Despite its robust growth, the wound debridement industry faces several challenges that can impact market expansion and profitability.

- Regulatory Hurdles: The stringent approval processes for new debridement products by regulatory bodies like the FDA and EMA can lead to lengthy development timelines and high costs, potentially delaying market entry and limiting innovation.

- Reimbursement Policies: Inconsistent or inadequate reimbursement policies in certain regions can hinder the adoption of advanced and often more expensive debridement technologies, impacting market penetration.

- Cost of Advanced Technologies: While offering better outcomes, some of the latest debridement technologies are associated with higher upfront costs, which can be a barrier for healthcare providers with limited budgets.

- Competition from Alternative Therapies: The continuous development of advanced wound dressings that promote autolytic debridement, while often complementary, can sometimes be perceived as substitutes, influencing market share dynamics.

Emerging Opportunities in Wound Debridement Industry

The wound debridement market is ripe with emerging opportunities that promise significant future growth, estimated to add billions to the global market value.

- Expansion in Emerging Economies: As healthcare infrastructure improves and disposable incomes rise in developing nations, there is a vast untapped potential for wound debridement products and services, representing a significant growth avenue.

- Development of Personalized Debridement Solutions: Tailoring debridement treatments based on individual patient needs, wound characteristics, and genetic predispositions offers a pathway to more effective and efficient wound care.

- Integration of Digital Health Technologies: The use of AI-powered wound assessment tools, telemedicine for remote monitoring, and data analytics can optimize debridement protocols and improve patient outcomes, creating new service-based revenue streams.

- Focus on Minimally Invasive and Non-Surgical Debridement: Continued innovation in non-surgical debridement methods, such as advanced enzymatic and biological agents, presents a substantial opportunity to address patient preference for less painful and disruptive treatments.

Leading Players in the Wound Debridement Industry Market

- Coloplast Corp

- Smith & Nephew

- Integra LifeSciences Corporation

- Molnlycke Health Care AB

- 3M Company

- PAUL HARTMANN AG

- Healthpoint Ltd

- B Braun Melsungen AG

- ConvaTec Inc

- MediWound

Key Developments in Wound Debridement Industry Industry

- October 2022: MediWound released positive clinical data from its EscharEx Phase 2 trials. The findings were presented at the Symposium on Advanced Wound Care (SAWC) Fall 2022 Conference, showcasing EscharEx's superiority over existing treatments in debridement efficacy and granulation tissue formation.

- February 2022: Guild Biosciences received an FY19 Military Burn Research Program (MBRP) Idea Development Award to advance the development of a non-surgical burn wound debridement product designed for prolonged field care scenarios.

Future Outlook for Wound Debridement Industry Market

The future outlook for the wound debridement market is exceptionally bright, with projected growth reaching billions by 2033. Continued advancements in enzymatic and biological debridement technologies, coupled with a growing understanding of the critical role of wound bed preparation, will drive market expansion. The increasing global burden of chronic diseases, particularly diabetes, and the aging population will sustain robust demand. Furthermore, the expansion of healthcare access in emerging economies and the increasing preference for minimally invasive treatments present significant opportunities for market players. Strategic collaborations, targeted product development for specific wound etiologies, and a focus on homecare solutions will be key to capitalizing on this dynamic and billion-dollar market.

Wound Debridement Industry Segmentation

-

1. Type

- 1.1. Chronic Wounds

- 1.2. Acute Wounds

-

2. Product

- 2.1. Collagenase Product

- 2.2. Papain Product

- 2.3. Others

-

3. End-User

- 3.1. Hospitals

- 3.2. Homecare

- 3.3. Others

Wound Debridement Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Wound Debridement Industry Regional Market Share

Geographic Coverage of Wound Debridement Industry

Wound Debridement Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.97% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Chronic Wounds

- 5.1.2. Acute Wounds

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Collagenase Product

- 5.2.2. Papain Product

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Hospitals

- 5.3.2. Homecare

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Wound Debridement Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Chronic Wounds

- 6.1.2. Acute Wounds

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Collagenase Product

- 6.2.2. Papain Product

- 6.2.3. Others

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Hospitals

- 6.3.2. Homecare

- 6.3.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Wound Debridement Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Chronic Wounds

- 7.1.2. Acute Wounds

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Collagenase Product

- 7.2.2. Papain Product

- 7.2.3. Others

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. Hospitals

- 7.3.2. Homecare

- 7.3.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Wound Debridement Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Chronic Wounds

- 8.1.2. Acute Wounds

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Collagenase Product

- 8.2.2. Papain Product

- 8.2.3. Others

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. Hospitals

- 8.3.2. Homecare

- 8.3.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Wound Debridement Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Chronic Wounds

- 9.1.2. Acute Wounds

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Collagenase Product

- 9.2.2. Papain Product

- 9.2.3. Others

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. Hospitals

- 9.3.2. Homecare

- 9.3.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Wound Debridement Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Chronic Wounds

- 10.1.2. Acute Wounds

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Collagenase Product

- 10.2.2. Papain Product

- 10.2.3. Others

- 10.3. Market Analysis, Insights and Forecast - by End-User

- 10.3.1. Hospitals

- 10.3.2. Homecare

- 10.3.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Wound Debridement Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Chronic Wounds

- 11.1.2. Acute Wounds

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Collagenase Product

- 11.2.2. Papain Product

- 11.2.3. Others

- 11.3. Market Analysis, Insights and Forecast - by End-User

- 11.3.1. Hospitals

- 11.3.2. Homecare

- 11.3.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Coloplast Corp*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Smith & Nephew

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Integra LifeSciences Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Molnlycke Health Care AB

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 3M Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 PAUL HARTMANN AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Healthpoint Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 B Braun Melsungen AG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ConvaTec Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 MediWound

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Coloplast Corp*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wound Debridement Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Wound Debridement Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Wound Debridement Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Wound Debridement Industry Revenue (billion), by Product 2025 & 2033

- Figure 5: North America Wound Debridement Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Wound Debridement Industry Revenue (billion), by End-User 2025 & 2033

- Figure 7: North America Wound Debridement Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 8: North America Wound Debridement Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Wound Debridement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Wound Debridement Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Wound Debridement Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Wound Debridement Industry Revenue (billion), by Product 2025 & 2033

- Figure 13: Europe Wound Debridement Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Wound Debridement Industry Revenue (billion), by End-User 2025 & 2033

- Figure 15: Europe Wound Debridement Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 16: Europe Wound Debridement Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Wound Debridement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Wound Debridement Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Asia Pacific Wound Debridement Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Wound Debridement Industry Revenue (billion), by Product 2025 & 2033

- Figure 21: Asia Pacific Wound Debridement Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Pacific Wound Debridement Industry Revenue (billion), by End-User 2025 & 2033

- Figure 23: Asia Pacific Wound Debridement Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Asia Pacific Wound Debridement Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Wound Debridement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Wound Debridement Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Wound Debridement Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Wound Debridement Industry Revenue (billion), by Product 2025 & 2033

- Figure 29: Middle East and Africa Wound Debridement Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Middle East and Africa Wound Debridement Industry Revenue (billion), by End-User 2025 & 2033

- Figure 31: Middle East and Africa Wound Debridement Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 32: Middle East and Africa Wound Debridement Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East and Africa Wound Debridement Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Wound Debridement Industry Revenue (billion), by Type 2025 & 2033

- Figure 35: South America Wound Debridement Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: South America Wound Debridement Industry Revenue (billion), by Product 2025 & 2033

- Figure 37: South America Wound Debridement Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: South America Wound Debridement Industry Revenue (billion), by End-User 2025 & 2033

- Figure 39: South America Wound Debridement Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 40: South America Wound Debridement Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Wound Debridement Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 3: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 4: Global Wound Debridement Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 7: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 8: Global Wound Debridement Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 14: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 15: Global Wound Debridement Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Spain Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 24: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 25: Global Wound Debridement Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: China Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: India Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Australia Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Korea Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 34: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 35: Global Wound Debridement Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: GCC Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Africa Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Global Wound Debridement Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 40: Global Wound Debridement Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 41: Global Wound Debridement Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 42: Global Wound Debridement Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 43: Brazil Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Argentina Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Wound Debridement Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wound Debridement Industry?

The projected CAGR is approximately 5.97%.

2. Which companies are prominent players in the Wound Debridement Industry?

Key companies in the market include Coloplast Corp*List Not Exhaustive, Smith & Nephew, Integra LifeSciences Corporation, Molnlycke Health Care AB, 3M Company, PAUL HARTMANN AG, Healthpoint Ltd, B Braun Melsungen AG, ConvaTec Inc, MediWound.

3. What are the main segments of the Wound Debridement Industry?

The market segments include Type, Product, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.25 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidence of Chronic Wounds; Increasing Number of Accidents; Increasing Technologically Advanced Products.

6. What are the notable trends driving market growth?

Collagenase-Based Enzymatic Wound Debridement Products are Expected to Witness Rapid Growth in the Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent regulatory policies.

8. Can you provide examples of recent developments in the market?

In October 2022, MediWound, released positive clinical data from the Company's EscharEx Phase 2 trials and were featured in an oral and two poster presentations at the Symposium on Advanced Wound Care (SAWC) Fall 2022 Conference. The data demonstrated EscharEx to be significantly better than gel vehicle and the non-surgical standard of care across multiple measures including the incidence of complete debridement, time to achieve complete debridement, and granulation tissue formation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wound Debridement Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wound Debridement Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wound Debridement Industry?

To stay informed about further developments, trends, and reports in the Wound Debridement Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence