Key Insights

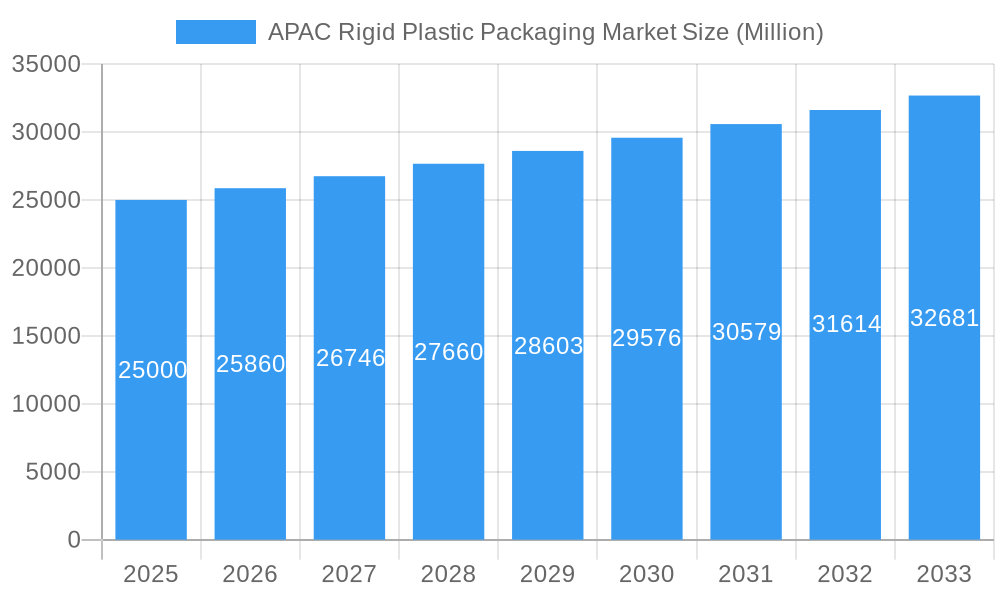

The Asia-Pacific (APAC) rigid plastic packaging market, valued at approximately $XX billion in 2025, is projected to experience robust growth, driven by several key factors. The region's burgeoning food and beverage, healthcare, and cosmetics sectors are significant contributors to this demand, fueled by rising disposable incomes and a growing consumer base. Packaging innovations, such as lightweight designs and improved barrier properties, are further enhancing market prospects. The increasing adoption of e-commerce and a shift towards convenient ready-to-eat meals are also boosting the need for efficient and protective rigid plastic packaging. China, India, and Japan represent the largest national markets within APAC, showcasing substantial growth opportunities due to their vast populations and rapidly expanding economies. While environmental concerns related to plastic waste pose a challenge, the industry is actively responding with initiatives focusing on recyclability and the use of recycled content. This is partially mitigating potential restraints, and further driving adoption of sustainable solutions within the rigid plastic packaging market. The continued expansion of manufacturing across the region, along with supportive government policies in certain countries promoting local production, further contribute to a positive outlook for market expansion in the coming years.

APAC Rigid Plastic Packaging Market Market Size (In Billion)

The market segmentation within APAC reveals significant potential for growth in specific product categories. Bottles and jars remain the dominant product segment, benefiting from the widespread usage in food and beverage applications. However, containers and trays are witnessing substantial growth, particularly in the e-commerce and food delivery sectors. Polyethylene (PE) and Polyethylene Terephthalate (PET) maintain their leading positions as preferred materials due to their cost-effectiveness and versatility. Nevertheless, increased interest in sustainable alternatives and stricter regulations are driving innovation in bio-based and recycled materials. The anticipated growth rate for APAC will slightly exceed the global CAGR of 3.42%, reflecting the region's unique dynamics of rapid economic development and a burgeoning consumer market. The forecast period from 2025-2033 promises continued growth, with projections pointing to a market value exceeding $YY billion by 2033. (Note: XX and YY billion represent estimations based on the provided CAGR and market trends; precise figures require further detailed data.)

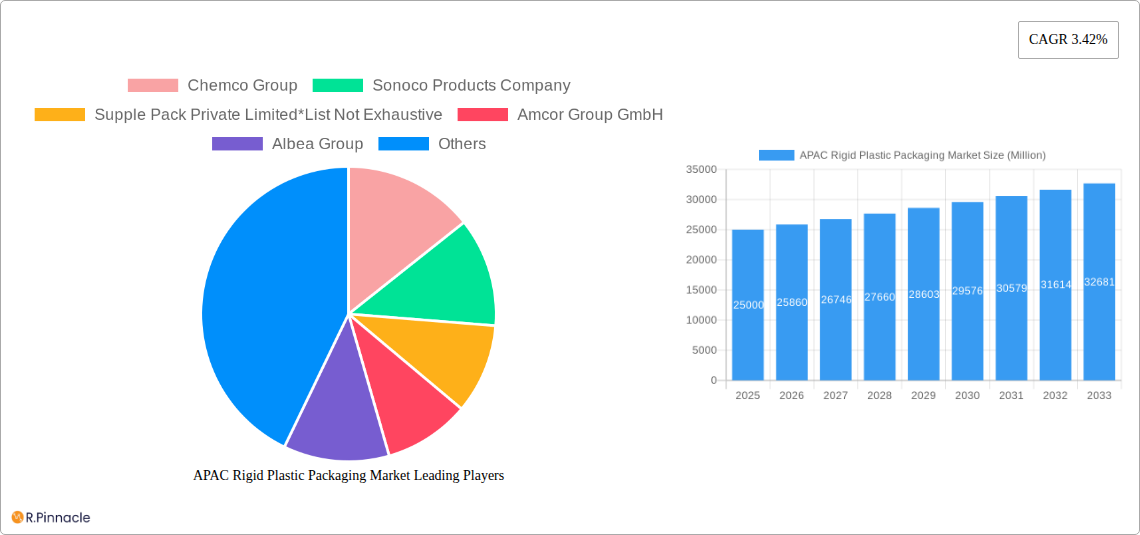

APAC Rigid Plastic Packaging Market Company Market Share

APAC Rigid Plastic Packaging Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Asia-Pacific (APAC) rigid plastic packaging market, offering valuable insights for industry professionals, investors, and stakeholders. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, segmentation, key players, and future trends. The report leverages robust data and analysis to provide a clear understanding of the market's current state and future trajectory.

APAC Rigid Plastic Packaging Market Structure & Innovation Trends

The APAC rigid plastic packaging market is characterized by a moderately concentrated structure, with several large multinational players and numerous regional companies vying for market share. Major players such as Amcor, Berry Global, and Sealed Air hold significant portions, while regional players cater to niche markets. Market share fluctuations are influenced by innovation, acquisitions, and changing consumer preferences. Innovation is driven primarily by sustainability concerns, with a growing demand for recycled and biodegradable materials, lighter weight packaging, and improved barrier properties. Regulatory frameworks, particularly those focusing on single-use plastics, heavily influence market dynamics, pushing for eco-friendly solutions and increasing recycling infrastructure. Product substitutes, such as paper-based alternatives, are gaining traction, but rigid plastic's versatility and cost-effectiveness remain key competitive advantages. End-user demographics, shifting towards a younger, more environmentally conscious population, further fuel demand for sustainable packaging.

M&A activity in the sector is significant, with deal values reaching xx Million in recent years. These activities reshape market landscape and enhance technological capabilities.

- Key Players: Amcor Group GmbH, Berry Global Inc., Sealed Air Corporation, and others.

- Market Concentration: Moderately concentrated with both multinational and regional players.

- Innovation Drivers: Sustainability, lightweighting, improved barrier properties.

- M&A Activity: Significant, contributing to market consolidation. Average deal value: xx Million.

- Regulatory Influence: Stringent regulations on single-use plastics are driving innovation and market shifts.

APAC Rigid Plastic Packaging Market Dynamics & Trends

The APAC rigid plastic packaging market is experiencing robust growth, driven by several factors. The rising population and expanding middle class in major economies like China and India are significantly increasing consumption, boosting demand for packaged goods across various sectors. Rapid urbanization and the growth of e-commerce further fuel packaging demand. Technological advancements, including automation in packaging production, improved barrier technologies, and the incorporation of smart packaging features, contribute to increased efficiency and product innovation. Consumer preferences are shifting towards convenient, sustainable, and visually appealing packaging. Competitive dynamics remain intense, with companies constantly innovating to enhance product offerings, improve cost-effectiveness, and strengthen their market positioning.

The market is expected to register a CAGR of xx% during the forecast period (2025-2033). Market penetration of sustainable packaging solutions is growing steadily, driven by increasing environmental awareness and stricter regulations.

Dominant Regions & Segments in APAC Rigid Plastic Packaging Market

China holds the dominant position within the APAC rigid plastic packaging market, owing to its massive population, thriving manufacturing sector, and extensive food and beverage industry. India demonstrates strong growth potential, fueled by its rapidly expanding economy and young population. Other significant markets include Japan, South Korea, and Australia & New Zealand, each with unique market dynamics.

- By Product: Bottles and jars dominate the market, followed by trays and containers, and caps and closures. Other product types, such as blister packs, are showing promising growth.

- By Material: PET (Polyethylene Terephthalate) leads the market due to its recyclability and versatility. PP (Polypropylene) and PE (Polyethylene) hold significant shares as well.

- By End-user Industry: Food and beverage is the leading end-user sector, followed by healthcare and cosmetics and personal care. Growth in e-commerce is further driving demand across all sectors.

- Key Drivers (China): Large consumer base, robust manufacturing infrastructure, supportive government policies.

- Key Drivers (India): Rapid economic growth, increasing disposable income, rising urbanization.

APAC Rigid Plastic Packaging Market Product Innovations

Recent innovations focus on sustainability, including the use of recycled materials (rPET), biodegradable plastics, and lightweight designs to minimize environmental impact. Advancements in barrier technologies are improving product shelf life and reducing food waste. Smart packaging incorporating features like track and trace capabilities is also gaining traction. These innovations are improving efficiency, sustainability and enhancing consumer experience, leading to increased adoption.

Report Scope & Segmentation Analysis

This report segments the APAC rigid plastic packaging market by product type (bottles and jars, trays and containers, etc.), material (PET, PP, PE, etc.), end-user industry (food and beverage, healthcare, etc.), and country (China, India, Japan, etc.). Each segment is thoroughly analyzed, including market size, growth projections, and competitive dynamics.

- By Product: Each product type shows unique growth trajectories based on consumer preference and industry trends. Market size for each varies, with bottles and jars holding the largest share.

- By Material: PET holds a dominant share, but other materials are witnessing growth depending on specific application requirements.

- By End-user Industry: Food & beverage currently leads, but growth in sectors like healthcare suggests future shifts.

- By Country: China and India show the largest market sizes, with other countries demonstrating steady growth.

Key Drivers of APAC Rigid Plastic Packaging Market Growth

The APAC rigid plastic packaging market's growth is driven by several factors, including increasing consumer demand for packaged goods, rapid urbanization, the expansion of e-commerce, and growing investments in manufacturing and infrastructure. Technological advancements, including automation and smart packaging technologies, further enhance the market's growth. Government initiatives promoting sustainable packaging practices also play a crucial role.

Challenges in the APAP Rigid Plastic Packaging Market Sector

The market faces challenges such as stringent environmental regulations, fluctuating raw material prices, and growing concerns regarding plastic waste. Supply chain disruptions and intense competition from other packaging materials pose additional obstacles. Meeting sustainability targets while maintaining cost-effectiveness requires constant innovation and strategic adaptation.

Emerging Opportunities in APAC Rigid Plastic Packaging Market

Emerging opportunities include the growing demand for sustainable and eco-friendly packaging solutions, the increasing adoption of smart packaging, and the expansion of e-commerce, creating avenues for innovation and growth. New market segments like specialized medical packaging and food delivery applications are also presenting exciting prospects.

Leading Players in the APAC Rigid Plastic Packaging Market Market

Key Developments in APAC Rigid Plastic Packaging Market Industry

- August 2023: Mitsubishi Corporation's agreement with Suntory and ENEOS to produce 35 Million sustainable PET bottles from biomass highlights the growing focus on sustainable materials.

- July 2023: PepsiCo's launch of Pepsi Black in 100% rPET bottles in India demonstrates the increasing adoption of recycled content and aligns with government sustainability initiatives.

- September 2022: Initiatives focusing on carbon neutrality and a circular economy indicate a wider industry shift towards sustainability.

Future Outlook for APAC Rigid Plastic Packaging Market Market

The APAC rigid plastic packaging market is poised for continued growth, driven by increasing consumer demand, technological advancements, and a growing focus on sustainability. Companies focusing on innovative, eco-friendly solutions and efficient supply chains are expected to thrive. The market will likely see an increasing adoption of recycled and bio-based materials, smart packaging technologies, and a greater focus on circular economy principles.

APAC Rigid Plastic Packaging Market Segmentation

-

1. Resin Type

-

1.1. Polyethylene (PE)

- 1.1.1. Low-Dens

- 1.1.2. High Density Polyethylene (HDPE)

- 1.2. Polyethylene terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 1.5. Polyvinyl chloride (PVC)

- 1.6. Other Resin Types

-

1.1. Polyethylene (PE)

-

2. Product Type

- 2.1. Bottles and Jars

- 2.2. Trays and Containers

- 2.3. Caps and Closures

- 2.4. Intermediate Bulk Containers (IBCs)

- 2.5. Drums

- 2.6. Pallets

- 2.7. Other Product Types

-

3. End-use Industries

-

3.1. Food**

- 3.1.1. Candy & Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, and Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Food Products

-

3.2. Foodservice**

- 3.2.1. Quick Service Restaurants (QSRs)

- 3.2.2. Full-Service Restaurants (FSRs)

- 3.2.3. Coffee and Snack Outlets

- 3.2.4. Retail Establishments

- 3.2.5. Institutional

- 3.2.6. Hospitality

- 3.2.7. Others Food Service Sectors

- 3.3. Beverage

- 3.4. Healthcare

- 3.5. Cosmetics and Personal Care

- 3.6. Industrial

- 3.7. Building and Construction

- 3.8. Automotive

- 3.9. Other End User Industries

-

3.1. Food**

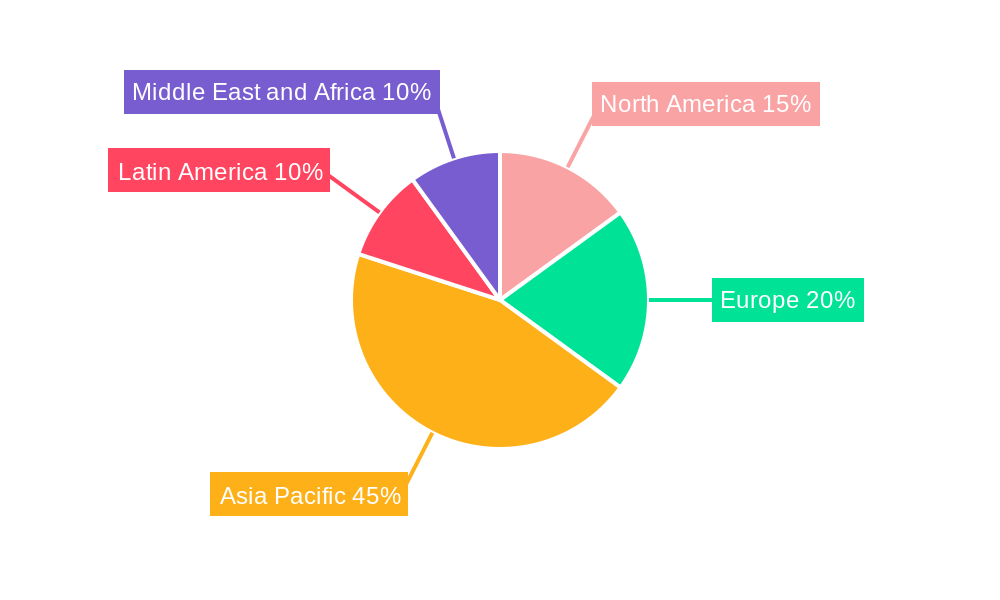

APAC Rigid Plastic Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

APAC Rigid Plastic Packaging Market Regional Market Share

Geographic Coverage of APAC Rigid Plastic Packaging Market

APAC Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Polyethylene (PE)

- 5.1.1.1. Low-Dens

- 5.1.1.2. High Density Polyethylene (HDPE)

- 5.1.2. Polyethylene terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 5.1.5. Polyvinyl chloride (PVC)

- 5.1.6. Other Resin Types

- 5.1.1. Polyethylene (PE)

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles and Jars

- 5.2.2. Trays and Containers

- 5.2.3. Caps and Closures

- 5.2.4. Intermediate Bulk Containers (IBCs)

- 5.2.5. Drums

- 5.2.6. Pallets

- 5.2.7. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by End-use Industries

- 5.3.1. Food**

- 5.3.1.1. Candy & Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, and Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Food Products

- 5.3.2. Foodservice**

- 5.3.2.1. Quick Service Restaurants (QSRs)

- 5.3.2.2. Full-Service Restaurants (FSRs)

- 5.3.2.3. Coffee and Snack Outlets

- 5.3.2.4. Retail Establishments

- 5.3.2.5. Institutional

- 5.3.2.6. Hospitality

- 5.3.2.7. Others Food Service Sectors

- 5.3.3. Beverage

- 5.3.4. Healthcare

- 5.3.5. Cosmetics and Personal Care

- 5.3.6. Industrial

- 5.3.7. Building and Construction

- 5.3.8. Automotive

- 5.3.9. Other End User Industries

- 5.3.1. Food**

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. Global APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Polyethylene (PE)

- 6.1.1.1. Low-Dens

- 6.1.1.2. High Density Polyethylene (HDPE)

- 6.1.2. Polyethylene terephthalate (PET)

- 6.1.3. Polypropylene (PP)

- 6.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 6.1.5. Polyvinyl chloride (PVC)

- 6.1.6. Other Resin Types

- 6.1.1. Polyethylene (PE)

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Bottles and Jars

- 6.2.2. Trays and Containers

- 6.2.3. Caps and Closures

- 6.2.4. Intermediate Bulk Containers (IBCs)

- 6.2.5. Drums

- 6.2.6. Pallets

- 6.2.7. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by End-use Industries

- 6.3.1. Food**

- 6.3.1.1. Candy & Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, and Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Food Products

- 6.3.2. Foodservice**

- 6.3.2.1. Quick Service Restaurants (QSRs)

- 6.3.2.2. Full-Service Restaurants (FSRs)

- 6.3.2.3. Coffee and Snack Outlets

- 6.3.2.4. Retail Establishments

- 6.3.2.5. Institutional

- 6.3.2.6. Hospitality

- 6.3.2.7. Others Food Service Sectors

- 6.3.3. Beverage

- 6.3.4. Healthcare

- 6.3.5. Cosmetics and Personal Care

- 6.3.6. Industrial

- 6.3.7. Building and Construction

- 6.3.8. Automotive

- 6.3.9. Other End User Industries

- 6.3.1. Food**

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. North America APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Polyethylene (PE)

- 7.1.1.1. Low-Dens

- 7.1.1.2. High Density Polyethylene (HDPE)

- 7.1.2. Polyethylene terephthalate (PET)

- 7.1.3. Polypropylene (PP)

- 7.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 7.1.5. Polyvinyl chloride (PVC)

- 7.1.6. Other Resin Types

- 7.1.1. Polyethylene (PE)

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Bottles and Jars

- 7.2.2. Trays and Containers

- 7.2.3. Caps and Closures

- 7.2.4. Intermediate Bulk Containers (IBCs)

- 7.2.5. Drums

- 7.2.6. Pallets

- 7.2.7. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by End-use Industries

- 7.3.1. Food**

- 7.3.1.1. Candy & Confectionery

- 7.3.1.2. Frozen Foods

- 7.3.1.3. Fresh Produce

- 7.3.1.4. Dairy Products

- 7.3.1.5. Dry Foods

- 7.3.1.6. Meat, Poultry, and Seafood

- 7.3.1.7. Pet Food

- 7.3.1.8. Other Food Products

- 7.3.2. Foodservice**

- 7.3.2.1. Quick Service Restaurants (QSRs)

- 7.3.2.2. Full-Service Restaurants (FSRs)

- 7.3.2.3. Coffee and Snack Outlets

- 7.3.2.4. Retail Establishments

- 7.3.2.5. Institutional

- 7.3.2.6. Hospitality

- 7.3.2.7. Others Food Service Sectors

- 7.3.3. Beverage

- 7.3.4. Healthcare

- 7.3.5. Cosmetics and Personal Care

- 7.3.6. Industrial

- 7.3.7. Building and Construction

- 7.3.8. Automotive

- 7.3.9. Other End User Industries

- 7.3.1. Food**

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. South America APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Polyethylene (PE)

- 8.1.1.1. Low-Dens

- 8.1.1.2. High Density Polyethylene (HDPE)

- 8.1.2. Polyethylene terephthalate (PET)

- 8.1.3. Polypropylene (PP)

- 8.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 8.1.5. Polyvinyl chloride (PVC)

- 8.1.6. Other Resin Types

- 8.1.1. Polyethylene (PE)

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Bottles and Jars

- 8.2.2. Trays and Containers

- 8.2.3. Caps and Closures

- 8.2.4. Intermediate Bulk Containers (IBCs)

- 8.2.5. Drums

- 8.2.6. Pallets

- 8.2.7. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by End-use Industries

- 8.3.1. Food**

- 8.3.1.1. Candy & Confectionery

- 8.3.1.2. Frozen Foods

- 8.3.1.3. Fresh Produce

- 8.3.1.4. Dairy Products

- 8.3.1.5. Dry Foods

- 8.3.1.6. Meat, Poultry, and Seafood

- 8.3.1.7. Pet Food

- 8.3.1.8. Other Food Products

- 8.3.2. Foodservice**

- 8.3.2.1. Quick Service Restaurants (QSRs)

- 8.3.2.2. Full-Service Restaurants (FSRs)

- 8.3.2.3. Coffee and Snack Outlets

- 8.3.2.4. Retail Establishments

- 8.3.2.5. Institutional

- 8.3.2.6. Hospitality

- 8.3.2.7. Others Food Service Sectors

- 8.3.3. Beverage

- 8.3.4. Healthcare

- 8.3.5. Cosmetics and Personal Care

- 8.3.6. Industrial

- 8.3.7. Building and Construction

- 8.3.8. Automotive

- 8.3.9. Other End User Industries

- 8.3.1. Food**

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. Europe APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 9.1.1. Polyethylene (PE)

- 9.1.1.1. Low-Dens

- 9.1.1.2. High Density Polyethylene (HDPE)

- 9.1.2. Polyethylene terephthalate (PET)

- 9.1.3. Polypropylene (PP)

- 9.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 9.1.5. Polyvinyl chloride (PVC)

- 9.1.6. Other Resin Types

- 9.1.1. Polyethylene (PE)

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Bottles and Jars

- 9.2.2. Trays and Containers

- 9.2.3. Caps and Closures

- 9.2.4. Intermediate Bulk Containers (IBCs)

- 9.2.5. Drums

- 9.2.6. Pallets

- 9.2.7. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by End-use Industries

- 9.3.1. Food**

- 9.3.1.1. Candy & Confectionery

- 9.3.1.2. Frozen Foods

- 9.3.1.3. Fresh Produce

- 9.3.1.4. Dairy Products

- 9.3.1.5. Dry Foods

- 9.3.1.6. Meat, Poultry, and Seafood

- 9.3.1.7. Pet Food

- 9.3.1.8. Other Food Products

- 9.3.2. Foodservice**

- 9.3.2.1. Quick Service Restaurants (QSRs)

- 9.3.2.2. Full-Service Restaurants (FSRs)

- 9.3.2.3. Coffee and Snack Outlets

- 9.3.2.4. Retail Establishments

- 9.3.2.5. Institutional

- 9.3.2.6. Hospitality

- 9.3.2.7. Others Food Service Sectors

- 9.3.3. Beverage

- 9.3.4. Healthcare

- 9.3.5. Cosmetics and Personal Care

- 9.3.6. Industrial

- 9.3.7. Building and Construction

- 9.3.8. Automotive

- 9.3.9. Other End User Industries

- 9.3.1. Food**

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 10. Middle East & Africa APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 10.1.1. Polyethylene (PE)

- 10.1.1.1. Low-Dens

- 10.1.1.2. High Density Polyethylene (HDPE)

- 10.1.2. Polyethylene terephthalate (PET)

- 10.1.3. Polypropylene (PP)

- 10.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 10.1.5. Polyvinyl chloride (PVC)

- 10.1.6. Other Resin Types

- 10.1.1. Polyethylene (PE)

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Bottles and Jars

- 10.2.2. Trays and Containers

- 10.2.3. Caps and Closures

- 10.2.4. Intermediate Bulk Containers (IBCs)

- 10.2.5. Drums

- 10.2.6. Pallets

- 10.2.7. Other Product Types

- 10.3. Market Analysis, Insights and Forecast - by End-use Industries

- 10.3.1. Food**

- 10.3.1.1. Candy & Confectionery

- 10.3.1.2. Frozen Foods

- 10.3.1.3. Fresh Produce

- 10.3.1.4. Dairy Products

- 10.3.1.5. Dry Foods

- 10.3.1.6. Meat, Poultry, and Seafood

- 10.3.1.7. Pet Food

- 10.3.1.8. Other Food Products

- 10.3.2. Foodservice**

- 10.3.2.1. Quick Service Restaurants (QSRs)

- 10.3.2.2. Full-Service Restaurants (FSRs)

- 10.3.2.3. Coffee and Snack Outlets

- 10.3.2.4. Retail Establishments

- 10.3.2.5. Institutional

- 10.3.2.6. Hospitality

- 10.3.2.7. Others Food Service Sectors

- 10.3.3. Beverage

- 10.3.4. Healthcare

- 10.3.5. Cosmetics and Personal Care

- 10.3.6. Industrial

- 10.3.7. Building and Construction

- 10.3.8. Automotive

- 10.3.9. Other End User Industries

- 10.3.1. Food**

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 11. Asia Pacific APAC Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 11.1.1. Polyethylene (PE)

- 11.1.1.1. Low-Dens

- 11.1.1.2. High Density Polyethylene (HDPE)

- 11.1.2. Polyethylene terephthalate (PET)

- 11.1.3. Polypropylene (PP)

- 11.1.4. Polystyrene (PS) and Expanded polystyrene (EPS

- 11.1.5. Polyvinyl chloride (PVC)

- 11.1.6. Other Resin Types

- 11.1.1. Polyethylene (PE)

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Bottles and Jars

- 11.2.2. Trays and Containers

- 11.2.3. Caps and Closures

- 11.2.4. Intermediate Bulk Containers (IBCs)

- 11.2.5. Drums

- 11.2.6. Pallets

- 11.2.7. Other Product Types

- 11.3. Market Analysis, Insights and Forecast - by End-use Industries

- 11.3.1. Food**

- 11.3.1.1. Candy & Confectionery

- 11.3.1.2. Frozen Foods

- 11.3.1.3. Fresh Produce

- 11.3.1.4. Dairy Products

- 11.3.1.5. Dry Foods

- 11.3.1.6. Meat, Poultry, and Seafood

- 11.3.1.7. Pet Food

- 11.3.1.8. Other Food Products

- 11.3.2. Foodservice**

- 11.3.2.1. Quick Service Restaurants (QSRs)

- 11.3.2.2. Full-Service Restaurants (FSRs)

- 11.3.2.3. Coffee and Snack Outlets

- 11.3.2.4. Retail Establishments

- 11.3.2.5. Institutional

- 11.3.2.6. Hospitality

- 11.3.2.7. Others Food Service Sectors

- 11.3.3. Beverage

- 11.3.4. Healthcare

- 11.3.5. Cosmetics and Personal Care

- 11.3.6. Industrial

- 11.3.7. Building and Construction

- 11.3.8. Automotive

- 11.3.9. Other End User Industries

- 11.3.1. Food**

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Chemco Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sonoco Products Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Supple Pack Private Limited*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amcor Group GmbH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Albea Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Berry Global Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Silgan Holdings Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Plastipak Holding Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sealed Air Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Alpla Werke Alwin Lehner GmbH & Co KG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Chemco Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global APAC Rigid Plastic Packaging Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America APAC Rigid Plastic Packaging Market Revenue (Million), by Resin Type 2025 & 2033

- Figure 3: North America APAC Rigid Plastic Packaging Market Revenue Share (%), by Resin Type 2025 & 2033

- Figure 4: North America APAC Rigid Plastic Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 5: North America APAC Rigid Plastic Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America APAC Rigid Plastic Packaging Market Revenue (Million), by End-use Industries 2025 & 2033

- Figure 7: North America APAC Rigid Plastic Packaging Market Revenue Share (%), by End-use Industries 2025 & 2033

- Figure 8: North America APAC Rigid Plastic Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 9: North America APAC Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America APAC Rigid Plastic Packaging Market Revenue (Million), by Resin Type 2025 & 2033

- Figure 11: South America APAC Rigid Plastic Packaging Market Revenue Share (%), by Resin Type 2025 & 2033

- Figure 12: South America APAC Rigid Plastic Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 13: South America APAC Rigid Plastic Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: South America APAC Rigid Plastic Packaging Market Revenue (Million), by End-use Industries 2025 & 2033

- Figure 15: South America APAC Rigid Plastic Packaging Market Revenue Share (%), by End-use Industries 2025 & 2033

- Figure 16: South America APAC Rigid Plastic Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 17: South America APAC Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe APAC Rigid Plastic Packaging Market Revenue (Million), by Resin Type 2025 & 2033

- Figure 19: Europe APAC Rigid Plastic Packaging Market Revenue Share (%), by Resin Type 2025 & 2033

- Figure 20: Europe APAC Rigid Plastic Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 21: Europe APAC Rigid Plastic Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe APAC Rigid Plastic Packaging Market Revenue (Million), by End-use Industries 2025 & 2033

- Figure 23: Europe APAC Rigid Plastic Packaging Market Revenue Share (%), by End-use Industries 2025 & 2033

- Figure 24: Europe APAC Rigid Plastic Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe APAC Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue (Million), by Resin Type 2025 & 2033

- Figure 27: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue Share (%), by Resin Type 2025 & 2033

- Figure 28: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 29: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue (Million), by End-use Industries 2025 & 2033

- Figure 31: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue Share (%), by End-use Industries 2025 & 2033

- Figure 32: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 33: Middle East & Africa APAC Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific APAC Rigid Plastic Packaging Market Revenue (Million), by Resin Type 2025 & 2033

- Figure 35: Asia Pacific APAC Rigid Plastic Packaging Market Revenue Share (%), by Resin Type 2025 & 2033

- Figure 36: Asia Pacific APAC Rigid Plastic Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 37: Asia Pacific APAC Rigid Plastic Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific APAC Rigid Plastic Packaging Market Revenue (Million), by End-use Industries 2025 & 2033

- Figure 39: Asia Pacific APAC Rigid Plastic Packaging Market Revenue Share (%), by End-use Industries 2025 & 2033

- Figure 40: Asia Pacific APAC Rigid Plastic Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 41: Asia Pacific APAC Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 2: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 3: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 4: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 6: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 7: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 8: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 13: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 14: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 15: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Brazil APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Argentina APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 20: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 21: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 22: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 23: United Kingdom APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Germany APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: France APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Italy APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Spain APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Russia APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Benelux APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Nordics APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 33: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 34: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 35: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Turkey APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Israel APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: GCC APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: North Africa APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: South Africa APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 43: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 45: Global APAC Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 46: China APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 47: India APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Japan APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 49: South Korea APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: ASEAN APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 51: Oceania APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific APAC Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Rigid Plastic Packaging Market?

The projected CAGR is approximately 3.42%.

2. Which companies are prominent players in the APAC Rigid Plastic Packaging Market?

Key companies in the market include Chemco Group, Sonoco Products Company, Supple Pack Private Limited*List Not Exhaustive, Amcor Group GmbH, Albea Group, Berry Global Inc, Silgan Holdings Inc, Plastipak Holding Inc, Sealed Air Corporation, Alpla Werke Alwin Lehner GmbH & Co KG.

3. What are the main segments of the APAC Rigid Plastic Packaging Market?

The market segments include Resin Type, Product Type, End-use Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 87.80 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from E-commerce Industry; Rising Consumption of Packaged Food.

6. What are the notable trends driving market growth?

Polyethylene terephthalate (PET) to Show a Significant Growth.

7. Are there any restraints impacting market growth?

Rising Adoption of Alternative Packaging Solutions.

8. Can you provide examples of recent developments in the market?

August 2023: Mitsubishi Corporation, a Japanese conglomerate, declared that it entered into a supply chain agreement with consumer goods firm Suntory Holdings Ltd. and energy firm ENEOS Corporation, with the aim of constructing a supply chain for sustainable PET plastic bottles made from biomass. Mitsubishi anticipates that the agreement will result in the production of Bio-PX equivalent to 35 million PET bottles in 2024, which will be used as raw material for the production of Suntory's sustainable PET bottles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the APAC Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence