Key Insights

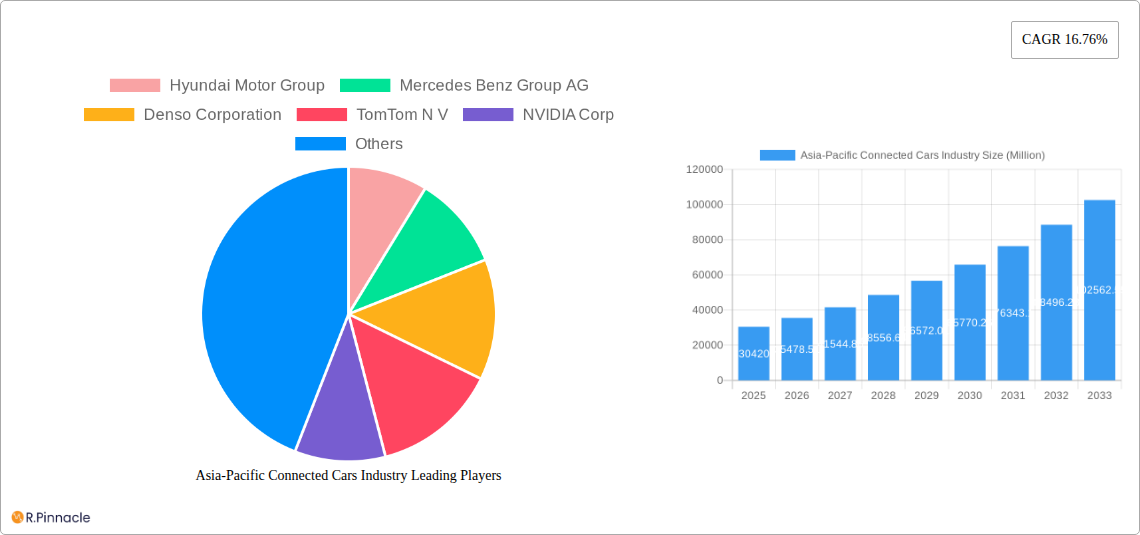

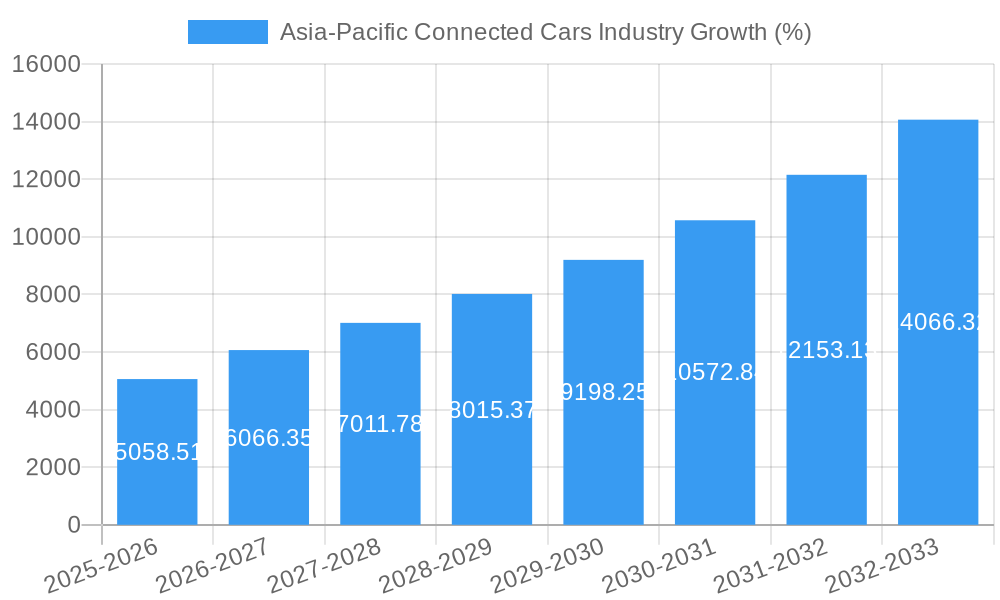

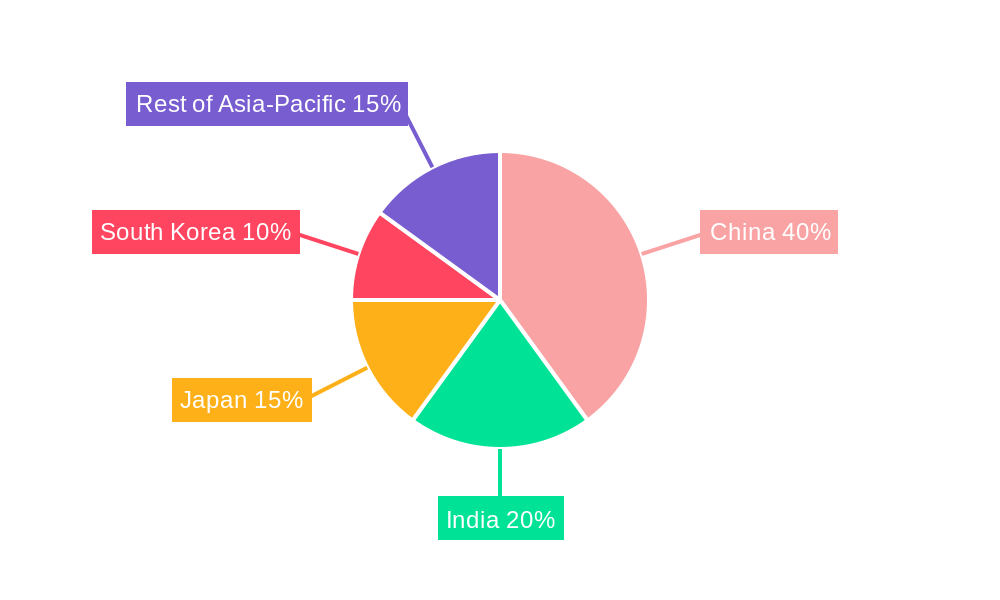

The Asia-Pacific connected cars market is experiencing robust growth, driven by increasing smartphone penetration, rising disposable incomes, and government initiatives promoting technological advancements in the automotive sector. The market, valued at $30.42 billion in 2025, is projected to expand significantly, fueled by a Compound Annual Growth Rate (CAGR) of 16.76% from 2025 to 2033. This growth is largely attributed to the increasing adoption of advanced driver-assistance systems (ADAS), infotainment systems, and vehicle-to-everything (V2X) communication technologies. China, India, and Japan are key contributors to this expansion, representing significant market shares due to their large automotive markets and burgeoning technological infrastructure. The passenger car segment dominates the market, followed by commercial vehicles, reflecting the widespread integration of connectivity features in new car models. While the OEM segment holds a substantial share, the aftermarket/replacement market is also witnessing considerable growth as consumers seek to upgrade existing vehicles with advanced connectivity solutions. Technological advancements such as 5G connectivity and artificial intelligence (AI) are further accelerating market growth by enabling enhanced features like autonomous driving capabilities and improved safety features. However, challenges such as data security concerns, high initial investment costs, and the need for robust infrastructure development to support V2X communication need to be addressed to fully realize the market's potential.

The market segmentation reveals strong growth in various technological areas. Navigation and entertainment systems remain prevalent, while safety features and vehicle management systems are witnessing accelerated adoption due to increasing safety concerns and the desire for efficient vehicle management. The increasing prevalence of V2X communication technologies, particularly V2V and V2I, is contributing to the improvement of road safety and traffic efficiency. The strong presence of major automotive manufacturers and technology companies in the region indicates the competitive landscape and the continuous innovation driving the market forward. Future growth will depend on overcoming infrastructural limitations, addressing cybersecurity risks, and continuing to develop user-friendly and reliable connected car technologies. The Asia-Pacific region's dynamic economic environment and progressive technological landscape are poised to support the continued expansion of the connected cars market in the coming years.

Asia-Pacific Connected Cars Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Asia-Pacific connected cars industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period 2019-2033, with a focus on 2025, this report dissects market dynamics, identifies key players, and forecasts future growth, offering actionable intelligence to navigate this rapidly evolving landscape. The report leverages extensive data and analysis to provide a detailed understanding of market segmentation, technological advancements, and key growth drivers within the Asia-Pacific region.

Asia-Pacific Connected Cars Industry Market Structure & Innovation Trends

The Asia-Pacific connected cars market is characterized by a dynamic interplay of established automotive giants and innovative technology companies. Market concentration is moderate, with several key players holding significant shares, but a fragmented landscape also exists, particularly within the aftermarket segment. Innovation is driven by advancements in 5G/6G technologies, AI, and cloud computing, enabling features like autonomous driving, advanced driver-assistance systems (ADAS), and enhanced infotainment. Regulatory frameworks, varying across countries, are a key influence, impacting data privacy, cybersecurity, and the adoption of connected car technologies. Product substitutes are limited, with the primary competition stemming from traditional vehicles lacking connectivity features. End-user demographics are shifting towards younger, tech-savvy consumers who prioritize connectivity and personalized in-car experiences. Mergers and acquisitions (M&A) activity has been significant, with deal values exceeding xx Million in the last five years, driven by strategic partnerships and the consolidation of the industry.

- Market Share (Estimated 2025): Top 5 players hold approximately xx% of the market.

- M&A Activity (2019-2024): xx deals valued at over xx Million.

- Key Innovation Drivers: 5G/6G, AI, Cloud Computing, ADAS.

- Regulatory Focus: Data privacy, cybersecurity, standardization.

Asia-Pacific Connected Cars Industry Market Dynamics & Trends

The Asia-Pacific connected cars market is experiencing robust growth, driven by increasing smartphone penetration, rising disposable incomes, and government initiatives promoting technological advancements. The Compound Annual Growth Rate (CAGR) is projected to be xx% during the forecast period (2025-2033). Technological disruptions, such as the integration of Artificial Intelligence (AI) and the Internet of Things (IoT), are revolutionizing the automotive industry, leading to the development of autonomous vehicles and advanced driver-assistance systems. Consumer preferences are shifting towards vehicles with seamless connectivity, intuitive user interfaces, and personalized services. The competitive landscape is intense, with both established automotive manufacturers and technology companies vying for market share through strategic partnerships, product innovation, and aggressive marketing strategies. Market penetration of connected cars is expected to reach xx% by 2033.

Dominant Regions & Segments in Asia-Pacific Connected Cars Industry

China and India are the dominant markets in the Asia-Pacific region, fueled by rapid economic growth, increasing vehicle sales, and supportive government policies. Japan and South Korea also hold substantial market shares, owing to their established automotive industries and technological prowess.

- By Vehicle Type: Passenger cars dominate, though commercial vehicles are showing significant growth potential due to fleet management and logistics needs.

- By Technology Type: Safety features (ADAS) and infotainment systems (Navigation and Entertainment) are the leading segments, but Vehicle Management and other emerging technologies (V2X) are rapidly gaining traction.

- By Vehicle Connectivity: V2V and V2I technologies are gaining momentum, while V2X is still emerging, requiring further infrastructure development.

- By End-User Type: OEMs currently dominate, but the aftermarket segment is poised for expansion as the lifespan of vehicles increases.

- Key Drivers (China & India):

- Rapid economic growth

- Increasing vehicle sales

- Government support for technological advancements

- Expanding infrastructure

- Growing middle class with increased disposable income

Asia-Pacific Connected Cars Industry Product Innovations

Recent innovations include the integration of advanced driver-assistance systems (ADAS), such as lane keeping assist and adaptive cruise control, alongside enhanced infotainment systems offering over-the-air (OTA) updates and personalized user experiences. The focus is on improving safety, convenience, and fuel efficiency, while also creating new revenue streams for automotive manufacturers through subscription services and data analytics. The market is witnessing a growing trend towards vehicle-to-everything (V2X) communication, enabling seamless interaction between vehicles, infrastructure, and other devices. These innovations align with the growing demand for safer, more efficient, and connected vehicles in the Asia-Pacific region.

Report Scope & Segmentation Analysis

This report segments the Asia-Pacific connected cars market across various parameters. The Vehicle Type segment comprises Passenger Cars and Commercial Vehicles. Technology Type includes Navigation, Entertainment, Safety, Vehicle Management, and Others. Vehicle Connectivity is segmented into V2V, V2I, and V2X. End-User Type encompasses OEM and Aftermarket/Replacement. Finally, Country segmentation covers India, China, Japan, South Korea, and Rest of Asia-Pacific. Each segment exhibits unique growth trajectories and competitive dynamics; the report provides detailed market size, growth projections, and a comprehensive competitive analysis for each.

Key Drivers of Asia-Pacific Connected Cars Industry Growth

Several factors fuel the growth of the Asia-Pacific connected cars market. These include technological advancements in 5G and AI, creating sophisticated features and functionalities. Government policies promoting digitalization and smart city initiatives incentivize adoption. The increasing prevalence of smartphones and internet connectivity also facilitates widespread access to connected car services. The growing middle class and rising disposable incomes create enhanced buying power and demand for advanced vehicle features.

Challenges in the Asia-Pacific Connected Cars Industry Sector

Significant challenges hinder market expansion. Regulatory inconsistencies across countries and data privacy concerns create hurdles. Supply chain disruptions and the global chip shortage affect production and availability. Intense competition among established players and new entrants influences pricing and market share. The high initial cost of implementing connected car technologies presents a barrier to wider adoption, especially in price-sensitive markets.

Emerging Opportunities in Asia-Pacific Connected Cars Industry

Significant opportunities exist within the Asia-Pacific connected cars market. The expansion of 5G networks presents possibilities for enhanced connectivity and performance. The growing demand for autonomous driving features creates market openings for related technologies and services. The increasing focus on electric vehicles and sustainable transportation offers opportunities for integrating connected car features into eco-friendly models. The rising popularity of subscription-based services creates new revenue streams and business models.

Leading Players in the Asia-Pacific Connected Cars Industry Market

- Hyundai Motor Group

- Mercedes Benz Group AG

- Denso Corporation

- TomTom N V

- NVIDIA Corp

- ZF Friedrichshafen

- Aptiv PLC

- NXP Semiconductors

- Harman International

- Continental AG

- BMW AG

- Robert Bosch GmbH

- SAIC Motor Corporation

- Audi AG

- Volvo AB

- Airbiquity In

Key Developments in Asia-Pacific Connected Cars Industry

- June 2023: Hyundai Motor Group announced 10 Million connected car service subscribers, projecting 20 Million by 2026.

- April 2023: MG Motor India launched the Comet EV with 55+ connected features.

- September 2022: Hyundai Motor Group and KT Corporation formed a joint venture for 6G autonomous driving and AAM communication.

Future Outlook for Asia-Pacific Connected Cars Industry Market

The Asia-Pacific connected cars market is poised for significant growth, driven by technological advancements, supportive government policies, and rising consumer demand. The increasing adoption of 5G technology, the development of autonomous driving capabilities, and the integration of new features and services will contribute to sustained market expansion. Strategic partnerships and investments in research and development will continue to shape the industry landscape, leading to innovative products and services. The market's future growth depends on addressing challenges related to data security, regulatory frameworks, and infrastructure development.

Asia-Pacific Connected Cars Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Technology Type

- 2.1. Navigation

- 2.2. Entertainment

- 2.3. Safety

- 2.4. Vehicle Management

- 2.5. Others (Multimedia Streaming etc.)

-

3. Vehicle Connectivity

- 3.1. Vehicle-to-Vehicle (V2V)

- 3.2. Vehicle-to-Infrastructure (V2I)

- 3.3. Vehicle-to-Everything (V2X)

-

4. End-User Type

- 4.1. Original Equipment Manufacturer (OEM)

- 4.2. Aftermarket/Replacement

Asia-Pacific Connected Cars Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Connected Cars Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 16.76% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Vehicle Safety and User Convenience

- 3.3. Market Restrains

- 3.3.1. Vulnerability to Cyber Attacks

- 3.4. Market Trends

- 3.4.1. Integrated Navigation System to gain significant Traction in the coming years

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Technology Type

- 5.2.1. Navigation

- 5.2.2. Entertainment

- 5.2.3. Safety

- 5.2.4. Vehicle Management

- 5.2.5. Others (Multimedia Streaming etc.)

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Connectivity

- 5.3.1. Vehicle-to-Vehicle (V2V)

- 5.3.2. Vehicle-to-Infrastructure (V2I)

- 5.3.3. Vehicle-to-Everything (V2X)

- 5.4. Market Analysis, Insights and Forecast - by End-User Type

- 5.4.1. Original Equipment Manufacturer (OEM)

- 5.4.2. Aftermarket/Replacement

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. China Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 7. Japan Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 8. India Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 9. South Korea Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 11. Australia Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific Asia-Pacific Connected Cars Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Hyundai Motor Group

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Mercedes Benz Group AG

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Denso Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 TomTom N V

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 NVIDIA Corp

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 ZF Friedrichshafen

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Aptiv PLC

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 NXP Semiconductors

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Harman International

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Continental AG

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 BMW AG

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Robert Bosch GmbH

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 SAIC Motor Corporation

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Audi AG

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 Volvo AB

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.16 Airbiquity In

- 13.2.16.1. Overview

- 13.2.16.2. Products

- 13.2.16.3. SWOT Analysis

- 13.2.16.4. Recent Developments

- 13.2.16.5. Financials (Based on Availability)

- 13.2.1 Hyundai Motor Group

List of Figures

- Figure 1: Asia-Pacific Connected Cars Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Asia-Pacific Connected Cars Industry Share (%) by Company 2024

List of Tables

- Table 1: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 3: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Technology Type 2019 & 2032

- Table 4: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Vehicle Connectivity 2019 & 2032

- Table 5: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by End-User Type 2019 & 2032

- Table 6: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: China Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Japan Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: South Korea Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Taiwan Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Australia Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Asia-Pacific Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 16: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Technology Type 2019 & 2032

- Table 17: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Vehicle Connectivity 2019 & 2032

- Table 18: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by End-User Type 2019 & 2032

- Table 19: Asia-Pacific Connected Cars Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: China Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Japan Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: South Korea Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: India Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Australia Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: New Zealand Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Indonesia Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Malaysia Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Singapore Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Thailand Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Vietnam Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Philippines Asia-Pacific Connected Cars Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Connected Cars Industry?

The projected CAGR is approximately 16.76%.

2. Which companies are prominent players in the Asia-Pacific Connected Cars Industry?

Key companies in the market include Hyundai Motor Group, Mercedes Benz Group AG, Denso Corporation, TomTom N V, NVIDIA Corp, ZF Friedrichshafen, Aptiv PLC, NXP Semiconductors, Harman International, Continental AG, BMW AG, Robert Bosch GmbH, SAIC Motor Corporation, Audi AG, Volvo AB, Airbiquity In.

3. What are the main segments of the Asia-Pacific Connected Cars Industry?

The market segments include Vehicle Type, Technology Type, Vehicle Connectivity, End-User Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.42 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Vehicle Safety and User Convenience.

6. What are the notable trends driving market growth?

Integrated Navigation System to gain significant Traction in the coming years.

7. Are there any restraints impacting market growth?

Vulnerability to Cyber Attacks.

8. Can you provide examples of recent developments in the market?

June 2023: Hyundai Motor Group, a multinational automotive manufacturer based out of South Korea, announced that its connected car services reached 10 million subscribers, owing to the growth in overseas subscribers using Bluelink, Kia Connect, and Genesis Connected Services. The company further stated that it expected that its connected car services would reach 20 million subscribers by the end of 2026.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Connected Cars Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Connected Cars Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Connected Cars Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Connected Cars Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence