Key Insights

The Australia and New Zealand rigid plastic packaging market is projected for steady growth, with a Compound Annual Growth Rate (CAGR) of 3.6% between 2025 and 2033. Key drivers include the expanding e-commerce sector, which demands secure packaging, and the increasing demand for convenient food options necessitating lightweight, durable, and recyclable plastic solutions. Advancements in sustainable materials are further supporting market expansion by addressing environmental concerns and aligning with consumer preferences for eco-friendly products. However, the market faces challenges from volatile raw material costs, stringent environmental regulations, and the rising adoption of alternative packaging materials. Competitive intensity is also notable, with established global and regional players competing for market share.

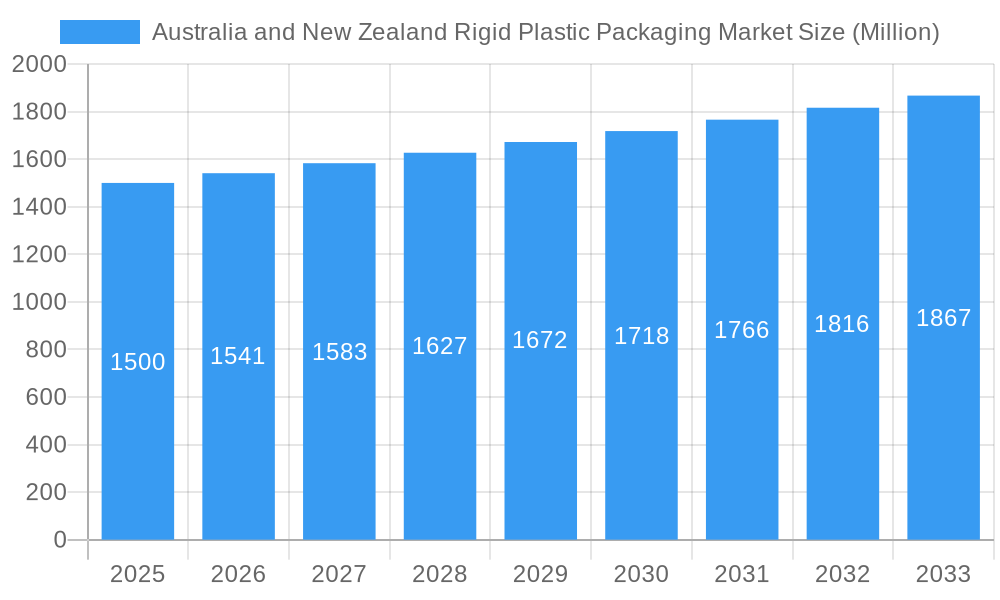

Australia and New Zealand Rigid Plastic Packaging Market Market Size (In Billion)

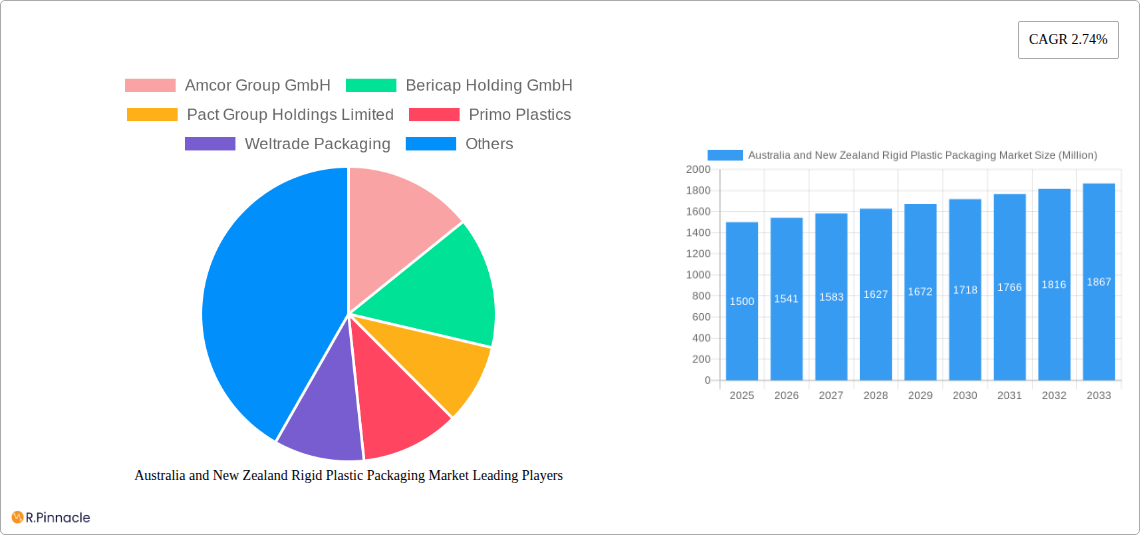

Market segmentation within Australia and New Zealand is diverse, serving various end-use industries. The food and beverage sector is the largest, driven by robust processing and export activities. Other significant contributors include personal care, cosmetics, pharmaceuticals, and industrial goods. Leading companies such as Amcor, Bericap, Pact Group, and Primo Plastics currently hold substantial market positions due to their established infrastructure and distribution networks. The market size was estimated at 220.2 billion in the base year 2025. Emerging specialized players are gaining traction through innovative designs and sustainable materials, catering to environmentally conscious consumers. The forecast period (2025-2033) offers significant potential for businesses prioritizing sustainable and innovative rigid plastic packaging. Success will hinge on adapting to evolving consumer demands and regulatory frameworks.

Australia and New Zealand Rigid Plastic Packaging Market Company Market Share

Australia and New Zealand Rigid Plastic Packaging Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Australia and New Zealand rigid plastic packaging market, offering valuable insights for industry professionals, investors, and stakeholders. The study covers the period 2019-2033, with a focus on the forecast period 2025-2033 and a base year of 2025. Discover key trends, growth drivers, challenges, and opportunities shaping this dynamic market.

Australia and New Zealand Rigid Plastic Packaging Market Structure & Innovation Trends

This section analyzes the market structure, highlighting key players, concentration levels, and innovation trends within the Australian and New Zealand rigid plastic packaging industry. We examine the regulatory landscape impacting the sector and explore the influence of product substitutes and end-user demographics on market dynamics. The analysis includes a review of mergers and acquisitions (M&A) activities, quantifying deal values where possible.

- Market Concentration: The market exhibits a [xx]% concentration ratio, with [xx] players holding a significant share.

- Innovation Drivers: Sustainability initiatives, lightweighting technologies, and advancements in barrier properties are key innovation drivers.

- Regulatory Framework: Stringent environmental regulations and increasing focus on recyclability significantly influence market dynamics.

- Product Substitutes: Growing interest in alternative packaging materials (e.g., biodegradable plastics, paper-based packaging) poses a challenge.

- End-User Demographics: The food and beverage sector, followed by the pharmaceuticals and consumer goods industries, dominate demand.

- M&A Activity: Recent M&A activity includes the acquisition of Plas-Pak WA by TricorBraun in January 2024, valuing approximately xx Million. Further deals totaling xx Million occurred in the period 2019-2024, illustrating the increasing consolidation within the industry.

Australia and New Zealand Rigid Plastic Packaging Market Dynamics & Trends

This section delves into the market dynamics, encompassing growth drivers, technological disruptions, consumer preferences, and competitive dynamics within the Australian and New Zealand rigid plastic packaging market.

The market is projected to experience a CAGR of [xx]% during the forecast period (2025-2033), driven by factors such as [Explain key drivers here, e.g., rising demand for packaged food and beverages, growth in e-commerce driving demand for protective packaging, increasing adoption of sustainable packaging solutions]. Technological disruptions, including automation in manufacturing and the introduction of advanced barrier materials, are influencing production efficiency and product quality. Consumer preference for sustainable and convenient packaging is also a major driver, increasing the demand for recyclable and compostable alternatives. Competitive dynamics are characterized by ongoing innovation, strategic partnerships, and price competition amongst established and emerging players. Market penetration of [specific type of packaging, e.g., recyclable PET bottles] is expected to reach [xx]% by 2033.

Dominant Regions & Segments in Australia and New Zealand Rigid Plastic Packaging Market

This section identifies the leading regions, countries, and segments within the Australia and New Zealand rigid plastic packaging market.

- Dominant Region: [Identify the dominant region, e.g., New South Wales].

- Key Drivers: Strong economic growth, well-established infrastructure, and a high concentration of manufacturing and distribution hubs contribute to its dominance.

- Dominant Segment: [Identify the dominant segment, e.g., Food and Beverage Packaging]

- Key Drivers: High demand for packaged food and beverages, coupled with increasing consumer preference for convenient and shelf-stable packaging, drives this segment's growth. [Add other relevant drivers in paragraph form.]

[Add a detailed analysis of the dominance of the chosen region and segment].

Australia and New Zealand Rigid Plastic Packaging Market Product Innovations

The market is witnessing significant product innovations, with a focus on sustainable and lightweight packaging solutions. Advancements in material science are leading to the development of recyclable and compostable plastics, while improvements in barrier properties are enhancing product shelf life and reducing food waste. The integration of smart packaging technologies, offering features such as tamper-evidence and traceability, is gaining traction, improving supply chain efficiency and consumer confidence. This aligns with broader trends toward increased transparency and sustainability within the packaging industry, enhancing the market fit for innovative products.

Report Scope & Segmentation Analysis

The report segments the market based on material type (e.g., PET, HDPE, PP), packaging type (e.g., bottles, containers, tubs), end-use industry (e.g., food and beverage, pharmaceuticals, personal care), and region (e.g., Australia, New Zealand). Each segment's market size, growth projection, and competitive landscape are thoroughly analyzed. [Include a paragraph for each segment, following the template above. Add predicted values for market sizes and growth projections].

Key Drivers of Australia and New Zealand Rigid Plastic Packaging Market Growth

Several factors drive the growth of the Australian and New Zealand rigid plastic packaging market. These include:

- Growing demand for packaged consumer goods, fueled by population growth and changing lifestyles.

- Increasing adoption of sustainable and eco-friendly packaging solutions in response to stricter environmental regulations and heightened consumer awareness.

- Technological advancements leading to the development of innovative and efficient packaging materials.

- Expansion of the e-commerce sector, driving demand for protective packaging solutions.

Challenges in the Australia and New Zealand Rigid Plastic Packaging Market Sector

The market faces several challenges including:

- Fluctuating raw material prices impacting profitability.

- Stringent environmental regulations increasing compliance costs and potentially limiting material choices.

- Growing competition from alternative packaging materials, such as paper-based and biodegradable options.

- Maintaining a secure and efficient supply chain, especially given global disruptions. [Add quantifiable impacts where possible].

Emerging Opportunities in Australia and New Zealand Rigid Plastic Packaging Market

Significant opportunities exist for market players. These include:

- Increasing demand for sustainable packaging solutions presents opportunities for companies offering recyclable and compostable alternatives.

- The growing e-commerce sector creates demand for innovative protective packaging solutions to ensure product safety during transit.

- Advancements in packaging technology offer opportunities to incorporate smart packaging features that enhance product traceability and consumer experience.

- Expanding into niche markets, such as specialized food packaging or medical packaging, can provide profitable growth avenues.

Leading Players in the Australia and New Zealand Rigid Plastic Packaging Market Market

- Amcor Group GmbH

- Bericap Holding GmbH

- Pact Group Holdings Limited

- Primo Plastics

- Weltrade Packaging

- Forward Plastics Ltd

- Flexicon Plastics

- Sonoco Products Company

- Waipak Packaging

Key Developments in Australia and New Zealand Rigid Plastic Packaging Market Industry

- August 2024: Colgate Palmolive's adoption of a circular packaging strategy for its Palmolive personal care line in Australia and New Zealand, using rHDPE and rPET, is expected to reduce virgin plastic use by over 1,900 tonnes annually. This highlights the growing importance of sustainability initiatives.

- January 2024: TricorBraun's acquisition of Plas-Pak WA strengthens its presence in the Australian market and expands its product offerings across various sectors. This acquisition showcases the ongoing consolidation within the industry.

Future Outlook for Australia and New Zealand Rigid Plastic Packaging Market Market

The Australian and New Zealand rigid plastic packaging market is poised for continued growth, driven by increasing consumer demand, technological advancements, and a growing focus on sustainability. Strategic opportunities exist for companies that can innovate in sustainable packaging solutions, leverage technological advancements to enhance efficiency and product quality, and cater to the evolving needs of specific market segments. The market's future success hinges on adapting to evolving consumer preferences and navigating the challenges associated with environmental regulations and supply chain complexities. The forecast period suggests significant growth potential, particularly within the sustainable packaging segment.

Australia and New Zealand Rigid Plastic Packaging Market Segmentation

-

1. Product Type

- 1.1. Bottles and Jars

- 1.2. Trays and Containers

- 1.3. Caps and Closures

- 1.4. Intermediate Bulk Containers (IBCs)

- 1.5. Drums

- 1.6. Pallets

- 1.7. Other Product Types

-

2. Material

-

2.1. Polyethylene (PE)

- 2.1.1. LDPE & LLDPE

- 2.1.2. HDPE

- 2.2. Polyethylene Terephthalate (PET)

- 2.3. Polypropylene (PP)

- 2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 2.5. Polyvinyl Chloride (PVC)

- 2.6. Other Rigid Plastic Packaging Materials

-

2.1. Polyethylene (PE)

-

3. End-Use Industries

-

3.1. Food**

- 3.1.1. Candy & Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, And Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Food Products

-

3.2. Foodservice**

- 3.2.1. Quick Service Restaurants (QSRs)

- 3.2.2. Full-Service Restaurants (FSRs)

- 3.2.3. Coffee and Snack Outlets

- 3.2.4. Retail Establishments

- 3.2.5. Institutional

- 3.2.6. Hospitality

- 3.2.7. Other Foodservice End-Uses

- 3.3. Beverage

- 3.4. Healthcare

- 3.5. Cosmetics and Personal Care

- 3.6. Industrial

- 3.7. Building and Construction

- 3.8. Automotive

- 3.9. Other En

-

3.1. Food**

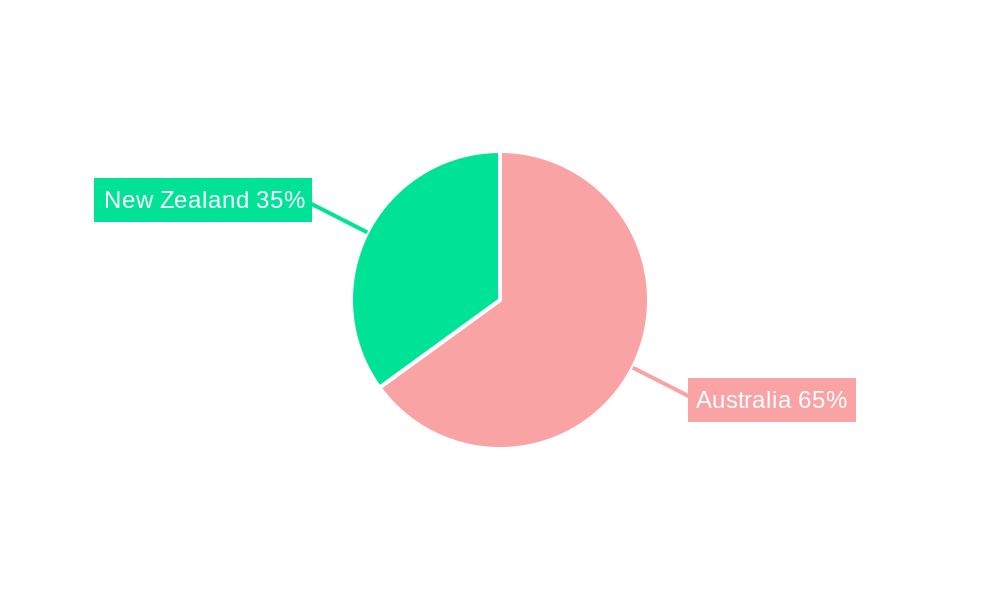

Australia and New Zealand Rigid Plastic Packaging Market Segmentation By Geography

- 1. Australia

Australia and New Zealand Rigid Plastic Packaging Market Regional Market Share

Geographic Coverage of Australia and New Zealand Rigid Plastic Packaging Market

Australia and New Zealand Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bottles and Jars

- 5.1.2. Trays and Containers

- 5.1.3. Caps and Closures

- 5.1.4. Intermediate Bulk Containers (IBCs)

- 5.1.5. Drums

- 5.1.6. Pallets

- 5.1.7. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Polyethylene (PE)

- 5.2.1.1. LDPE & LLDPE

- 5.2.1.2. HDPE

- 5.2.2. Polyethylene Terephthalate (PET)

- 5.2.3. Polypropylene (PP)

- 5.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.2.5. Polyvinyl Chloride (PVC)

- 5.2.6. Other Rigid Plastic Packaging Materials

- 5.2.1. Polyethylene (PE)

- 5.3. Market Analysis, Insights and Forecast - by End-Use Industries

- 5.3.1. Food**

- 5.3.1.1. Candy & Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, And Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Food Products

- 5.3.2. Foodservice**

- 5.3.2.1. Quick Service Restaurants (QSRs)

- 5.3.2.2. Full-Service Restaurants (FSRs)

- 5.3.2.3. Coffee and Snack Outlets

- 5.3.2.4. Retail Establishments

- 5.3.2.5. Institutional

- 5.3.2.6. Hospitality

- 5.3.2.7. Other Foodservice End-Uses

- 5.3.3. Beverage

- 5.3.4. Healthcare

- 5.3.5. Cosmetics and Personal Care

- 5.3.6. Industrial

- 5.3.7. Building and Construction

- 5.3.8. Automotive

- 5.3.9. Other En

- 5.3.1. Food**

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Australia and New Zealand Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Bottles and Jars

- 6.1.2. Trays and Containers

- 6.1.3. Caps and Closures

- 6.1.4. Intermediate Bulk Containers (IBCs)

- 6.1.5. Drums

- 6.1.6. Pallets

- 6.1.7. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Polyethylene (PE)

- 6.2.1.1. LDPE & LLDPE

- 6.2.1.2. HDPE

- 6.2.2. Polyethylene Terephthalate (PET)

- 6.2.3. Polypropylene (PP)

- 6.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.2.5. Polyvinyl Chloride (PVC)

- 6.2.6. Other Rigid Plastic Packaging Materials

- 6.2.1. Polyethylene (PE)

- 6.3. Market Analysis, Insights and Forecast - by End-Use Industries

- 6.3.1. Food**

- 6.3.1.1. Candy & Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, And Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Food Products

- 6.3.2. Foodservice**

- 6.3.2.1. Quick Service Restaurants (QSRs)

- 6.3.2.2. Full-Service Restaurants (FSRs)

- 6.3.2.3. Coffee and Snack Outlets

- 6.3.2.4. Retail Establishments

- 6.3.2.5. Institutional

- 6.3.2.6. Hospitality

- 6.3.2.7. Other Foodservice End-Uses

- 6.3.3. Beverage

- 6.3.4. Healthcare

- 6.3.5. Cosmetics and Personal Care

- 6.3.6. Industrial

- 6.3.7. Building and Construction

- 6.3.8. Automotive

- 6.3.9. Other En

- 6.3.1. Food**

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bericap Holding GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Pact Group Holdings Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Primo Plastics

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Weltrade Packaging

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Forward Plastics Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Flexicon Plastics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sonoco Products Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Waipak Packaging8 2 Heat Map Analysis8 3 Competitor Analysis - Emerging vs Established Player

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Amcor Group GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia and New Zealand Rigid Plastic Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia and New Zealand Rigid Plastic Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 3: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by End-Use Industries 2020 & 2033

- Table 4: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 7: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by End-Use Industries 2020 & 2033

- Table 8: Australia and New Zealand Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia and New Zealand Rigid Plastic Packaging Market?

The projected CAGR is approximately 3.6%.

2. Which companies are prominent players in the Australia and New Zealand Rigid Plastic Packaging Market?

Key companies in the market include Amcor Group GmbH, Bericap Holding GmbH, Pact Group Holdings Limited, Primo Plastics, Weltrade Packaging, Forward Plastics Ltd, Flexicon Plastics, Sonoco Products Company, Waipak Packaging8 2 Heat Map Analysis8 3 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the Australia and New Zealand Rigid Plastic Packaging Market?

The market segments include Product Type, Material, End-Use Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 220.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Proliferation of the Food and Beverage Industry in the Region; Availability of a Diverse Raneg of Products in the Rigid Plastic Packaging Sector.

6. What are the notable trends driving market growth?

Bottles and Jars Segment is Estimated to Have the Largest Market Share.

7. Are there any restraints impacting market growth?

Proliferation of the Food and Beverage Industry in the Region; Availability of a Diverse Raneg of Products in the Rigid Plastic Packaging Sector.

8. Can you provide examples of recent developments in the market?

August 2024: Colgate Palmolive, a US-based consumer products company, adopted a circular packaging strategy. The company introduced bottles made entirely from recycled plastics for its Palmolive personal care line in Australia and New Zealand. Constructed from rHDPE and rPET, these bottles will likely prevent the annual use of over 1,900 tonnes of virgin plastic in the region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia and New Zealand Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia and New Zealand Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia and New Zealand Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the Australia and New Zealand Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence