Key Insights

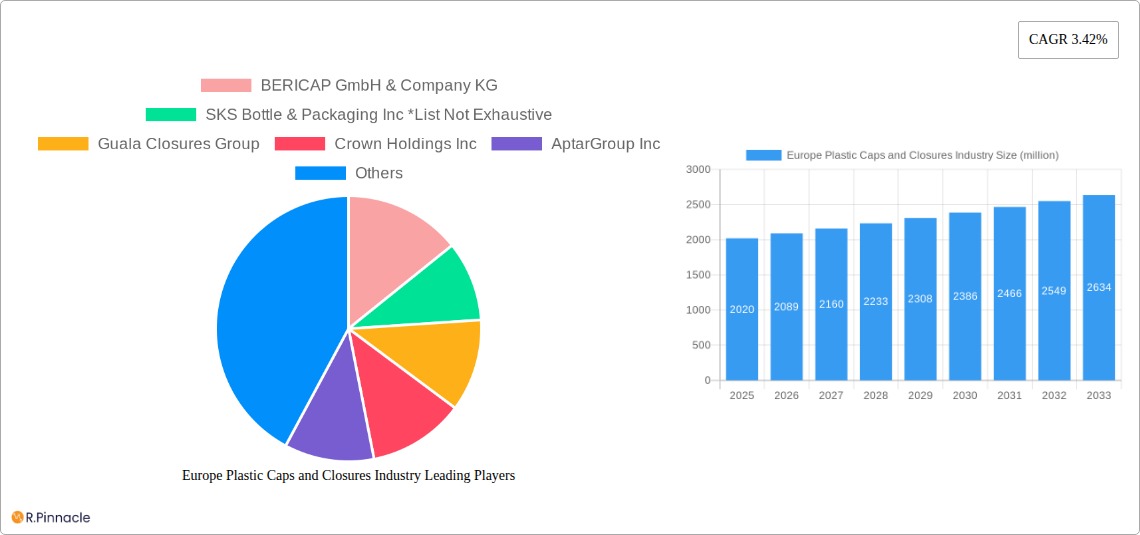

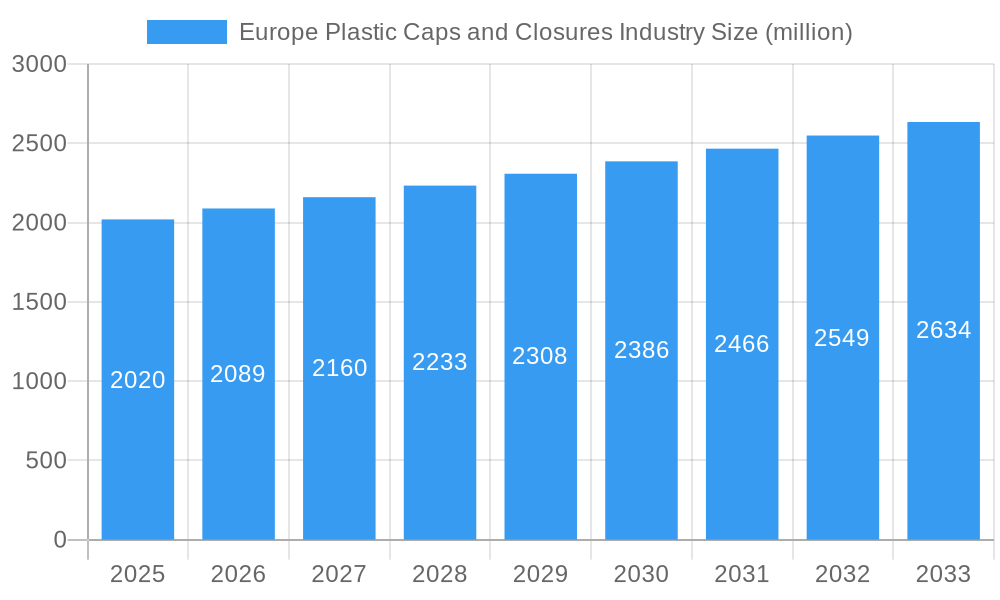

The Europe Plastic Caps and Closures Industry is poised for robust growth, projecting a market size of USD 2.02 billion in 2025 with a projected Compound Annual Growth Rate (CAGR) of 3.42% through 2033. This expansion is primarily fueled by escalating demand from the beverage and food packaging sectors, which represent the largest end-user segments. The convenience, safety, and tamper-evident features offered by plastic caps and closures make them indispensable for protecting and preserving a vast array of consumer goods. Furthermore, the pharmaceutical and healthcare industries are significant contributors to this growth, driven by an increasing need for sterile and secure packaging solutions for medicines and medical devices. The widespread adoption of PET, PP, LDPE, and HDPE as primary materials, owing to their versatility, cost-effectiveness, and recyclability, underpins the industry's stability and innovation.

Europe Plastic Caps and Closures Industry Market Size (In Billion)

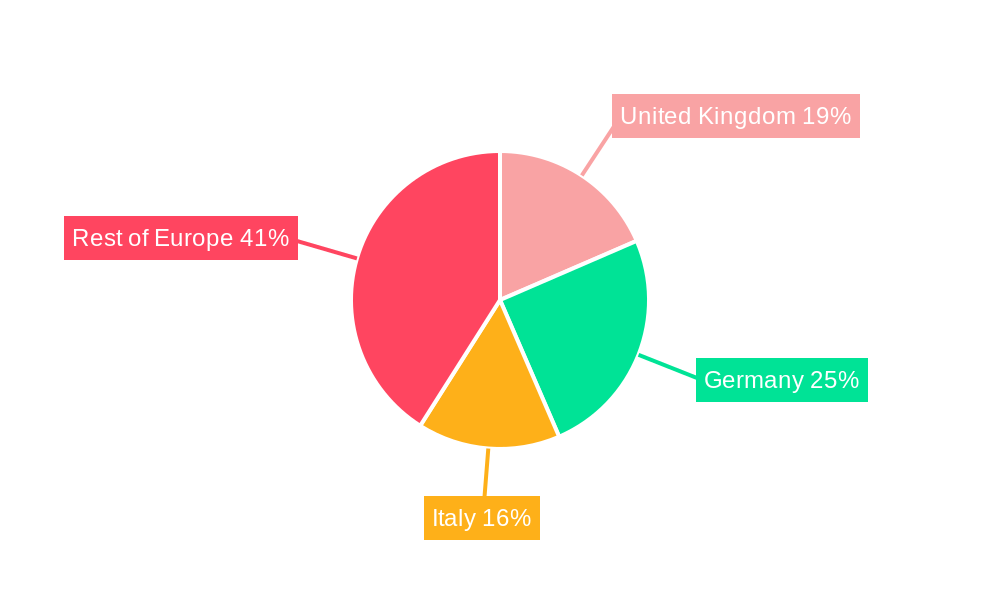

The market is experiencing dynamic shifts influenced by key trends such as the increasing emphasis on sustainable packaging solutions and the development of innovative closure designs that enhance user experience and product shelf-life. For instance, the rise of smart closures with features like authentication and tracking capabilities is a notable trend. However, the industry also faces restraints, including fluctuating raw material prices, which can impact profit margins, and growing regulatory pressures concerning plastic waste management and the promotion of a circular economy. Despite these challenges, the inherent demand for effective and efficient packaging solutions across major European economies like Germany, the United Kingdom, and Italy, coupled with the 'Rest of Europe' region's growing consumption, indicates a sustained upward trajectory for the plastic caps and closures market in the coming years.

Europe Plastic Caps and Closures Industry Company Market Share

Unlock critical insights into the dynamic European plastic caps and closures market. This in-depth report provides a 360-degree view, forecasting market evolution from 2025 to 2033, with a base year of 2025 and historical data from 2019–2024. Gain a competitive edge with expert analysis on market structure, drivers, challenges, and emerging opportunities, crucial for stakeholders in the beverage, food, pharmaceutical, cosmetic, and household industries.

Europe Plastic Caps and Closures Industry Market Structure & Innovation Trends

The Europe plastic caps and closures market exhibits a moderately concentrated structure, with key players like BERICAP GmbH & Company KG, SKS Bottle & Packaging Inc, Guala Closures Group, Crown Holdings Inc, AptarGroup Inc, Amcor PLC, Albea Group, Coral Products PLC, Nippon Closures Co Ltd, Tetra Pak International SA, Berry Global, and Pelliconi & C SPA holding significant market shares. Innovation is a primary driver, with an increasing emphasis on sustainable materials, advanced sealing technologies, and tamper-evident features. Regulatory frameworks, particularly those promoting circular economy principles and reducing plastic waste, significantly influence market strategies. The threat of product substitutes, such as metal closures or alternative packaging formats, is present but mitigated by the cost-effectiveness and versatility of plastic. End-user demographics are diverse, with the beverage and food sectors representing the largest consumers. Mergers and acquisitions (M&A) activity is moderate, with deal values often undisclosed but driven by strategic market expansion and portfolio diversification. Expect a market share increase of approximately 5-7% in M&A activities focused on sustainable solutions and technological advancements.

Europe Plastic Caps and Closures Industry Market Dynamics & Trends

The European plastic caps and closures market is poised for robust growth, driven by an expanding consumer base and an increasing demand for packaged goods across various sectors. The market is anticipated to experience a Compound Annual Growth Rate (CAGR) of approximately 4.5% to 5.5% during the forecast period. This growth is underpinned by several key factors. Firstly, evolving consumer preferences for convenience and safety are fueling the demand for innovative closure solutions that ensure product integrity and ease of use, particularly within the food and beverage industries. Secondly, technological advancements are continuously shaping the market, with a strong focus on lightweighting, material science innovation, and the integration of smart features for traceability and brand protection. The rise of e-commerce and the associated logistics demand for secure and durable packaging further amplify growth prospects.

Sustainability remains a paramount trend, compelling manufacturers to invest in research and development for recyclable, biodegradable, and bio-based plastic alternatives. This shift is not only driven by consumer demand but also by stringent environmental regulations and corporate social responsibility initiatives across Europe. Market penetration of specialized closures, such as those with enhanced barrier properties or child-resistant mechanisms, is expected to rise, particularly in the pharmaceutical and healthcare segments. Competitive dynamics are intensifying, with both established players and emerging companies vying for market share through product differentiation, strategic partnerships, and a commitment to circular economy principles. The adoption of advanced manufacturing techniques, including automation and digitalization, is crucial for optimizing production efficiency and cost-effectiveness in this competitive landscape.

Dominant Regions & Segments in Europe Plastic Caps and Closures Industry

Within the Europe plastic caps and closures industry, Western Europe consistently emerges as the dominant region, driven by its highly developed economies, strong consumer purchasing power, and a mature industrial base. Countries like Germany, France, the United Kingdom, and Italy represent significant markets due to their large-scale food and beverage processing, pharmaceutical manufacturing, and burgeoning cosmetics sectors.

- Key Drivers of Regional Dominance:

- Economic Policies: Favorable trade agreements, robust manufacturing incentives, and established industrial infrastructure within Western European nations.

- Consumer Demographics: High per capita consumption of packaged goods and a sophisticated consumer base demanding quality, safety, and sustainability in packaging.

- Regulatory Landscape: Strict quality control standards and evolving environmental regulations that encourage innovation in sustainable packaging solutions.

- Technological Advancement: Early adoption and development of advanced materials and manufacturing processes for plastic caps and closures.

In terms of material segmentation, PP (Polypropylene) and PET (Polyethylene Terephthalate) dominate the market share, collectively accounting for an estimated 70-75% of the total volume. PP's versatility, excellent chemical resistance, and cost-effectiveness make it ideal for a wide array of applications, especially in food, beverage, and household products. PET, primarily used for bottles, necessitates compatible closures that ensure a secure seal.

PP Dominance Drivers:

- High demand from the food and beverage sector for caps and closures requiring good impact resistance and flexibility.

- Cost-effectiveness and ease of processing for high-volume manufacturing.

- Application in diverse products ranging from dairy to sauces and edible oils.

PET Dominance Drivers:

- Synergy with PET bottles for beverages, particularly carbonated soft drinks and water.

- Excellent sealing properties and resistance to carbonation pressure.

- Continued growth in the bottled water and beverage market.

The Beverage end-user segment represents the largest and most dynamic market for plastic caps and closures, contributing approximately 35-40% to the overall market revenue. This is followed closely by the Food segment, which accounts for around 25-30%. The growth in these sectors is propelled by increasing demand for convenience, portability, and extended shelf life.

Beverage Segment Drivers:

- Massive consumption of bottled water, juices, carbonated soft drinks, and alcoholic beverages.

- Demand for tamper-evident and child-resistant closures for safety and brand integrity.

- Innovation in dispensing closures for enhanced consumer experience.

Food Segment Drivers:

- Growth in the processed food industry, including sauces, condiments, dairy products, and ready-to-eat meals.

- Need for closures that maintain product freshness and prevent spoilage.

- Increasing popularity of single-serving and on-the-go food options.

Europe Plastic Caps and Closures Industry Product Innovations

Product innovations in the Europe plastic caps and closures market are largely centered on sustainability and enhanced functionality. Manufacturers are increasingly developing closures made from recycled plastics (rPET, rPP) and bio-based materials, aligning with circular economy goals and reducing the environmental footprint. Technological advancements include the introduction of lightweight designs that minimize material usage without compromising integrity, as well as smart closures with embedded RFID or NFC tags for improved traceability and supply chain management. Furthermore, there is a growing emphasis on user-centric designs, featuring easy-open mechanisms, one-handed operation, and integrated dispensing features, particularly for the pharmaceutical, cosmetic, and household sectors. These innovations provide a competitive advantage by meeting evolving consumer demands for eco-friendliness and convenience.

Report Scope & Segmentation Analysis

This report encompasses the comprehensive analysis of the Europe plastic caps and closures market, segmenting it by material and end-user. The material segments include PET, PP, LDPE, and HDPE, as well as Other Materials like polymers used in specialized applications. Each material segment is analyzed for its market size, growth projections, and competitive dynamics, with PP and PET expected to lead in market share due to their widespread adoption. The end-user segments are Beverage, Food, Pharmaceutical and Healthcare, Cosmetics and Toiletries, Household, and Other End-Users. The Beverage and Food segments are projected to exhibit the highest growth rates driven by increasing consumption and demand for convenience.

Key Drivers of Europe Plastic Caps and Closures Industry Growth

The Europe plastic caps and closures industry is experiencing significant growth, propelled by several key drivers.

- Rising Demand for Packaged Goods: An expanding population and increasing urbanization are fueling the demand for packaged food, beverages, pharmaceuticals, and personal care products, directly impacting the need for caps and closures.

- Sustainability Initiatives: Growing consumer and regulatory pressure for eco-friendly packaging is driving innovation in recyclable, biodegradable, and post-consumer recycled (PCR) plastic closures.

- Technological Advancements: Innovations in lightweighting, material science, and tamper-evident technologies are enhancing product performance and consumer safety, creating new market opportunities.

- Evolving Consumer Preferences: Demand for convenience, ease of use, and enhanced functionality in packaging, such as easy-open caps and dispensing features, is a major growth catalyst.

- Growth in Key End-Use Industries: The robust expansion of the beverage, food, pharmaceutical, and cosmetic sectors directly translates to increased consumption of plastic caps and closures.

Challenges in the Europe Plastic Caps and Closures Industry Sector

Despite robust growth, the Europe plastic caps and closures industry faces several challenges.

- Regulatory Scrutiny and Environmental Concerns: Increasing regulations around plastic waste and single-use plastics may lead to restrictions or higher compliance costs.

- Volatile Raw Material Prices: Fluctuations in the prices of crude oil and petrochemicals, key feedstocks for plastic production, can impact profitability and pricing strategies.

- Competition from Alternative Materials: While plastic remains dominant, ongoing development in paper-based, metal, and glass alternatives presents a competitive threat in certain applications.

- Supply Chain Disruptions: Global supply chain vulnerabilities, exacerbated by geopolitical events and logistics challenges, can lead to material shortages and increased lead times.

- Recycling Infrastructure Limitations: Inconsistent and underdeveloped recycling infrastructure across different European regions can hinder the widespread adoption and effective management of recycled plastic closures.

Emerging Opportunities in Europe Plastic Caps and Closures Industry

The Europe plastic caps and closures industry is ripe with emerging opportunities.

- Growth in Sustainable and Recycled Materials: The increasing demand for closures made from recycled plastics (rPET, rPP) and bio-based alternatives presents a significant growth avenue. Manufacturers investing in advanced recycling technologies and sustainable material sourcing will gain a competitive advantage.

- Smart and Connected Closures: The integration of IoT technology, such as NFC or QR codes on closures, offers opportunities for enhanced traceability, authentication, and consumer engagement, particularly in the pharmaceutical and premium consumer goods sectors.

- Expansion in Emerging Markets and Niche Applications: Identifying and capitalizing on growth in underserved or rapidly developing sub-segments within existing end-user industries, and exploring new niche applications, can unlock new revenue streams.

- Development of Advanced Dispensing and Functionality Features: Innovations in child-resistant caps, tamper-evident seals with improved usability, and sophisticated dispensing mechanisms for cosmetics and pharmaceuticals will cater to evolving consumer needs.

- Circular Economy Business Models: Developing closed-loop systems and reusable closure solutions aligns with sustainability goals and can create long-term customer loyalty and revenue streams.

Leading Players in the Europe Plastic Caps and Closures Industry Market

- BERICAP GmbH & Company KG

- SKS Bottle & Packaging Inc

- Guala Closures Group

- Crown Holdings Inc

- AptarGroup Inc

- Amcor PLC

- Albea Group

- Coral Products PLC

- Nippon Closures Co Ltd

- Tetra Pak International SA

- Berry Global

- Pelliconi & C SPA

Key Developments in Europe Plastic Caps and Closures Industry Industry

- June 2021: Guala Closures Group launched Divinum Blossom, a new screwcap for wine crafted from recyclable and renewable materials. This launch is part of their extensive eco-design strategy aimed at enhancing sustainability in their product offerings.

- January 2021: Berry Global Inc. introduced the Cyrano, a revolutionary lightweight dual-port blow fill seal closure. This closure is up to 64% lighter than comparable products and is designed for large volume parenteral applications, offering significant plastic reduction and providing a safe, user-friendly solution for intravenous and infusion systems in healthcare settings.

Future Outlook for Europe Plastic Caps and Closures Industry Market

The future outlook for the Europe plastic caps and closures market is exceptionally positive, driven by a confluence of sustained demand and a strong pivot towards sustainability. Market growth will be accelerated by ongoing innovations in material science, leading to an increased adoption of recycled and bio-based plastics, which will be critical for meeting stringent environmental regulations and consumer expectations. The trend towards lightweighting will continue to reduce material consumption and associated costs. Furthermore, the increasing integration of smart technologies in closures, offering enhanced product security, traceability, and consumer interaction, presents significant untapped potential. Strategic investments in advanced manufacturing capabilities, such as automation and digitalization, will be crucial for companies aiming to maintain a competitive edge in terms of efficiency and product quality. The market's trajectory indicates a strong emphasis on circular economy principles, paving the way for innovative business models focused on product lifecycle management and resource optimization.

Europe Plastic Caps and Closures Industry Segmentation

-

1. Material

- 1.1. PET

- 1.2. PP

- 1.3. LDPE and HDPE

- 1.4. Other Materials

-

2. End-user

- 2.1. Beverage

- 2.2. Food

- 2.3. Pharmaceutical and Healthcare

- 2.4. Cosmetics and Toiletries

- 2.5. Househol

- 2.6. Other En

Europe Plastic Caps and Closures Industry Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. Italy

- 4. Rest of Europe

Europe Plastic Caps and Closures Industry Regional Market Share

Geographic Coverage of Europe Plastic Caps and Closures Industry

Europe Plastic Caps and Closures Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. PET

- 5.1.2. PP

- 5.1.3. LDPE and HDPE

- 5.1.4. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by End-user

- 5.2.1. Beverage

- 5.2.2. Food

- 5.2.3. Pharmaceutical and Healthcare

- 5.2.4. Cosmetics and Toiletries

- 5.2.5. Househol

- 5.2.6. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. Germany

- 5.3.3. Italy

- 5.3.4. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Europe Plastic Caps and Closures Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. PET

- 6.1.2. PP

- 6.1.3. LDPE and HDPE

- 6.1.4. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by End-user

- 6.2.1. Beverage

- 6.2.2. Food

- 6.2.3. Pharmaceutical and Healthcare

- 6.2.4. Cosmetics and Toiletries

- 6.2.5. Househol

- 6.2.6. Other En

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. United Kingdom Europe Plastic Caps and Closures Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. PET

- 7.1.2. PP

- 7.1.3. LDPE and HDPE

- 7.1.4. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by End-user

- 7.2.1. Beverage

- 7.2.2. Food

- 7.2.3. Pharmaceutical and Healthcare

- 7.2.4. Cosmetics and Toiletries

- 7.2.5. Househol

- 7.2.6. Other En

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Germany Europe Plastic Caps and Closures Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. PET

- 8.1.2. PP

- 8.1.3. LDPE and HDPE

- 8.1.4. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by End-user

- 8.2.1. Beverage

- 8.2.2. Food

- 8.2.3. Pharmaceutical and Healthcare

- 8.2.4. Cosmetics and Toiletries

- 8.2.5. Househol

- 8.2.6. Other En

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Italy Europe Plastic Caps and Closures Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. PET

- 9.1.2. PP

- 9.1.3. LDPE and HDPE

- 9.1.4. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by End-user

- 9.2.1. Beverage

- 9.2.2. Food

- 9.2.3. Pharmaceutical and Healthcare

- 9.2.4. Cosmetics and Toiletries

- 9.2.5. Househol

- 9.2.6. Other En

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Rest of Europe Europe Plastic Caps and Closures Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. PET

- 10.1.2. PP

- 10.1.3. LDPE and HDPE

- 10.1.4. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by End-user

- 10.2.1. Beverage

- 10.2.2. Food

- 10.2.3. Pharmaceutical and Healthcare

- 10.2.4. Cosmetics and Toiletries

- 10.2.5. Househol

- 10.2.6. Other En

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 BERICAP GmbH & Company KG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 SKS Bottle & Packaging Inc *List Not Exhaustive

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Guala Closures Group

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Crown Holdings Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 AptarGroup Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Amcor PLC

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Albea Group

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Coral Products PLC

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Nippon closures Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Tetra Pak International SA

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Berry Global

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Pelliconi & C SPA

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 BERICAP GmbH & Company KG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Europe Plastic Caps and Closures Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Europe Plastic Caps and Closures Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Material 2020 & 2033

- Table 2: Europe Plastic Caps and Closures Industry Revenue million Forecast, by End-user 2020 & 2033

- Table 3: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Material 2020 & 2033

- Table 5: Europe Plastic Caps and Closures Industry Revenue million Forecast, by End-user 2020 & 2033

- Table 6: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Material 2020 & 2033

- Table 8: Europe Plastic Caps and Closures Industry Revenue million Forecast, by End-user 2020 & 2033

- Table 9: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Country 2020 & 2033

- Table 10: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Material 2020 & 2033

- Table 11: Europe Plastic Caps and Closures Industry Revenue million Forecast, by End-user 2020 & 2033

- Table 12: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Material 2020 & 2033

- Table 14: Europe Plastic Caps and Closures Industry Revenue million Forecast, by End-user 2020 & 2033

- Table 15: Europe Plastic Caps and Closures Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Plastic Caps and Closures Industry?

The projected CAGR is approximately 3.42%.

2. Which companies are prominent players in the Europe Plastic Caps and Closures Industry?

Key companies in the market include BERICAP GmbH & Company KG, SKS Bottle & Packaging Inc *List Not Exhaustive, Guala Closures Group, Crown Holdings Inc, AptarGroup Inc, Amcor PLC, Albea Group, Coral Products PLC, Nippon closures Co Ltd, Tetra Pak International SA, Berry Global, Pelliconi & C SPA.

3. What are the main segments of the Europe Plastic Caps and Closures Industry?

The market segments include Material, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.02 million as of 2022.

5. What are some drivers contributing to market growth?

Product Innovation to Aid Product Differentiation and Branding; Rising Demand for Smaller-sized Packs.

6. What are the notable trends driving market growth?

Beverage Industry is Expected to Grow Significantly.

7. Are there any restraints impacting market growth?

Lightweight and Cost-effective Stand-up Pouch Packaging Alternatives.

8. Can you provide examples of recent developments in the market?

June 2021 - Guala Closures Group launched latest product in its sustainable range: Divinum Blossom, a screwcap for wine made with recyclable and renewable materials as part of its ongoing ambitious eco-design strategy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Plastic Caps and Closures Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Plastic Caps and Closures Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Plastic Caps and Closures Industry?

To stay informed about further developments, trends, and reports in the Europe Plastic Caps and Closures Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence