Key Insights

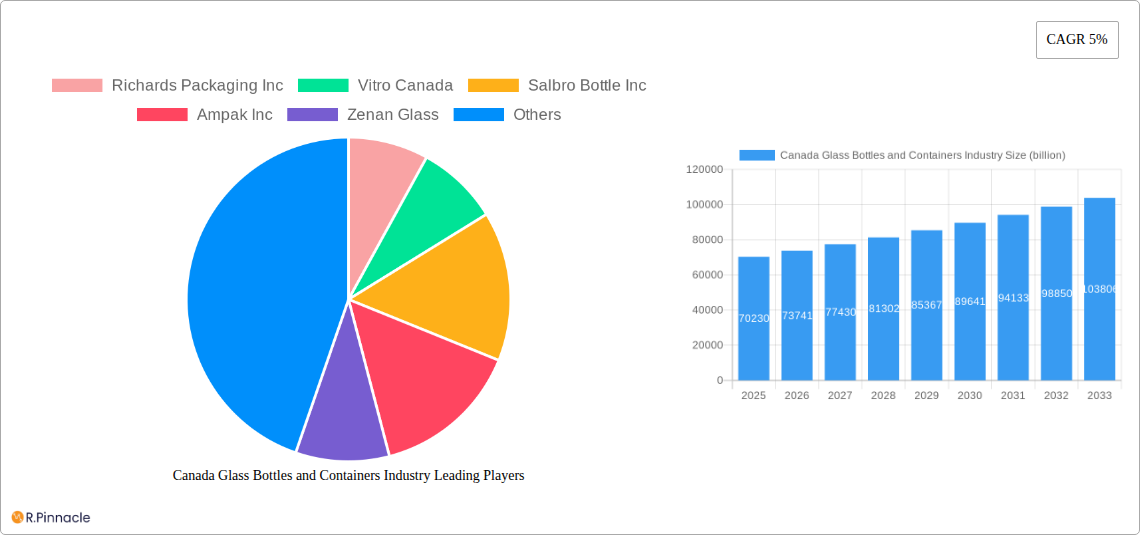

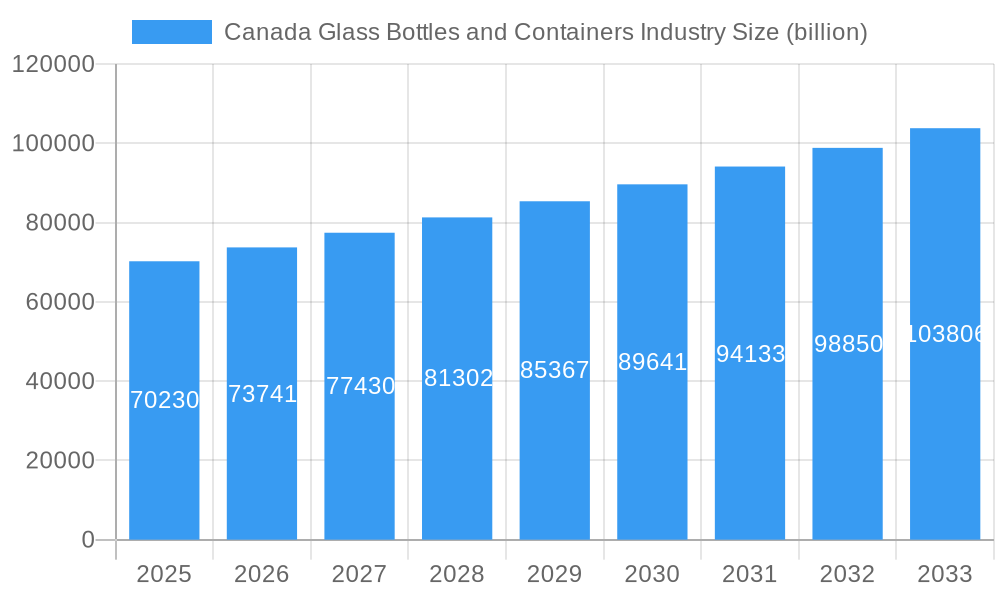

The Canada Glass Bottles and Containers Industry is poised for substantial growth, projected to reach $70.23 billion in 2025. This expansion is driven by a burgeoning demand for sustainable packaging solutions across key end-user verticals. The food and beverage sector, in particular, continues to be a dominant force, fueled by consumer preference for glass packaging due to its inertness, reusability, and premium perception. The pharmaceutical industry also presents a significant growth avenue, with a consistent need for sterile and protective glass containers for medicines and health products. Furthermore, the cosmetics industry is increasingly adopting glass for its aesthetic appeal and perceived quality, contributing to the overall market uplift. These strong underlying demands, coupled with an estimated Compound Annual Growth Rate (CAGR) of 5%, indicate a robust and expanding market.

Canada Glass Bottles and Containers Industry Market Size (In Billion)

Emerging trends in the Canadian market highlight a shift towards enhanced design, specialized glass treatments, and a focus on circular economy principles. Innovations in lightweight glass and decorative capabilities are further stimulating market adoption. While the market benefits from strong consumer and industry preferences, certain factors could influence its trajectory. The initial cost of glass packaging compared to alternatives like plastic or metal, and the energy-intensive nature of glass production, represent potential restraints. However, these are increasingly being offset by advancements in manufacturing efficiency and a growing societal emphasis on environmental responsibility, which favors the inherent recyclability and reusability of glass. Companies like Richards Packaging Inc. and Owens-Illinois Inc. are at the forefront, investing in sustainable practices and product innovation to meet the evolving demands of the Canadian market.

Canada Glass Bottles and Containers Industry Company Market Share

Unlock critical insights into the burgeoning Canadian glass bottles and containers market with this comprehensive, data-driven report. Spanning 2019 to 2033, with a detailed analysis of the 2025 base and estimated year, this report offers an in-depth understanding of market structure, dynamics, innovations, and future potential. Discover actionable strategies for capitalizing on growth opportunities in the food, beverage, pharmaceutical, cosmetic, and other end-user sectors. This report is essential for manufacturers, suppliers, investors, and industry stakeholders seeking to navigate the competitive landscape and drive growth in this vital Canadian industry. All values are presented in billions.

Canada Glass Bottles and Containers Industry Market Structure & Innovation Trends

The Canadian glass bottles and containers industry exhibits a moderate market concentration, with key players like Richards Packaging Inc, Vitro Canada, Salbro Bottle Inc, Ampak Inc, Zenan Glass, and Owens-Illinois Inc holding significant market share, estimated at approximately 75% collectively. Innovation is a primary driver, fueled by advancements in glass manufacturing technology, increased demand for sustainable packaging solutions, and evolving consumer preferences for premium and eco-friendly products. Regulatory frameworks, particularly those concerning environmental impact and food safety, play a crucial role in shaping market trends and product development. The threat of product substitutes, primarily from plastic and metal packaging, remains a consideration, though glass offers distinct advantages in terms of inertness, recyclability, and aesthetic appeal. End-user demographics reveal a strong reliance on the food and beverage sectors, followed by pharmaceuticals and cosmetics, each with specific packaging requirements. Mergers and acquisitions (M&A) activities, valued in the hundreds of millions of dollars annually, continue to reshape the competitive landscape as companies seek to expand their product portfolios, geographic reach, and technological capabilities.

Canada Glass Bottles and Containers Industry Market Dynamics & Trends

The Canadian glass bottles and containers industry is poised for robust growth, projected to experience a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025–2033. This expansion is propelled by several key market growth drivers. A significant contributor is the escalating consumer demand for sustainable and recyclable packaging. As environmental consciousness rises, consumers increasingly favor glass over single-use plastics, a trend that directly benefits the glass containers sector. Furthermore, the growing popularity of premium and artisanal products across the food and beverage industries necessitates high-quality, aesthetically pleasing packaging, where glass excels. Technological disruptions are also playing a pivotal role. Innovations in manufacturing processes, such as lightweighting techniques and advanced decorative coatings, are enhancing the efficiency and appeal of glass containers, making them more competitive. The pharmaceutical sector's consistent demand for sterile, non-reactive packaging for medicines and healthcare products provides a stable and growing segment. The cosmetics industry also contributes significantly, leveraging glass for its perceived luxury and quality, enhancing brand image and consumer appeal. E-commerce growth, while presenting challenges in terms of breakage, also opens new distribution avenues for glass packaged goods, provided appropriate protective measures are implemented. Competitive dynamics are characterized by a mix of established multinational corporations and agile local manufacturers, all vying for market share through product differentiation, cost optimization, and strategic partnerships. The market penetration of specialized glass containers, designed for specific applications like specialty beverages or pharmaceutical delivery systems, is on the rise, indicating a maturation of the market towards niche solutions. The increasing focus on health and wellness also drives demand for glass packaging in food and beverage products perceived as healthier or more natural. The industry's ability to adapt to evolving consumer lifestyles and stringent regulatory requirements will be crucial for sustained market penetration and growth in the coming years.

Dominant Regions & Segments in Canada Glass Bottles and Containers Industry

The Food and Beverage end-user verticals emerge as the dominant segments within the Canadian glass bottles and containers industry, collectively accounting for an estimated 65% of the total market value. This dominance is underpinned by several critical drivers.

- Economic Policies: Favorable government policies supporting domestic manufacturing and agricultural output, coupled with initiatives promoting local food and beverage production, directly stimulate demand for glass packaging. The widespread availability of resources and a robust supply chain further enhance production capabilities.

- Infrastructure: Well-developed transportation networks, including roads, rail, and ports, facilitate the efficient distribution of both raw materials and finished glass containers across Canada and for export markets. This logistical efficiency is paramount for the high-volume nature of the food and beverage industries.

- Consumer Preferences: A strong and growing consumer preference for natural, healthy, and premium food and beverage products translates into a higher demand for glass packaging. Consumers associate glass with quality, freshness, and sustainability, especially for products like craft beers, artisanal spirits, specialty oils, and organic juices.

- Product Diversification: The sheer diversity of products within the food and beverage categories, ranging from dairy and sauces to beverages and preserved goods, requires a wide array of glass container shapes, sizes, and functionalities, all of which are readily available from Canadian manufacturers.

The Pharmaceuticals segment holds significant importance, representing approximately 20% of the market. This dominance is driven by the stringent requirements for sterility, inertness, and tamper-evident packaging of medicines, vaccines, and other healthcare products. The reliability and proven safety profile of glass make it the preferred choice for these critical applications.

The Cosmetics segment, accounting for around 10% of the market, benefits from glass's premium perception, aesthetic appeal, and its inertness, which preserves the integrity of delicate cosmetic formulations. Luxury beauty brands, in particular, frequently opt for glass packaging to enhance their brand image.

The Other End-User Verticals segment, comprising approximately 5% of the market, includes diverse applications such as home and personal care products, candles, and specialty industrial chemicals. While smaller in aggregate, these niche markets often demand specialized glass container designs and functionalities, contributing to market innovation.

The overall dominance of the food and beverage sectors is further solidified by their consistent demand throughout economic cycles, making them the bedrock of the Canadian glass bottles and containers industry. The interplay of supportive economic policies, advanced infrastructure, and evolving consumer tastes ensures these segments will continue to lead market growth.

Canada Glass Bottles and Containers Industry Product Innovations

Product innovations in the Canadian glass bottles and containers industry are largely driven by the pursuit of enhanced sustainability, improved functionality, and superior aesthetics. Manufacturers are developing lighter-weight glass formulations to reduce shipping costs and environmental impact, while simultaneously exploring advanced coating technologies for improved scratch resistance and barrier properties. Smart packaging solutions, incorporating QR codes or NFC tags, are also emerging, enabling enhanced traceability and consumer engagement. The application of these innovations spans across all end-user verticals, from creating more durable and visually appealing bottles for premium beverages to developing specialized vials with enhanced UV protection for pharmaceuticals. These advancements provide a significant competitive advantage by meeting evolving market demands for eco-friendly, functional, and high-performance packaging solutions.

Report Scope & Segmentation Analysis

This report segments the Canada Glass Bottles and Containers Industry by End-User Vertical. The Food segment is a substantial market, projected for significant growth driven by increased consumer demand for preserved and packaged foods, with an estimated market size of over $2 billion. The Beverage segment, expected to reach over $3 billion by 2025, is fueled by the demand for alcoholic and non-alcoholic drinks, including a rising preference for artisanal and craft products, with strong growth projected. The Pharmaceuticals segment, estimated at over $1 billion, is characterized by consistent demand for sterile and safe packaging for medicines and healthcare products, with steady growth anticipated. The Cosmetics segment, valued at over $500 million, leverages glass for its premium appeal and inertness, with moderate growth expected as luxury beauty brands continue to expand. The Other End-User Verticals segment, encompassing a range of applications, is projected to grow steadily, reflecting diversification in industrial and consumer goods packaging needs.

Key Drivers of Canada Glass Bottles and Containers Industry Growth

The Canadian glass bottles and containers industry's growth is propelled by several interconnected factors. A primary driver is the increasing consumer preference for sustainable and environmentally friendly packaging options, leading to a shift away from plastics towards recyclable glass. Technological advancements in manufacturing, such as lightweighting and energy-efficient production, are enhancing cost-competitiveness and reducing the environmental footprint of glass containers. The robust performance of key end-user sectors, particularly the food and beverage industries, which consistently require high-quality packaging for product preservation and market appeal, provides a stable demand base. Furthermore, evolving regulatory landscapes often favor materials like glass for their recyclability and safety, thereby indirectly supporting industry growth.

Challenges in the Canada Glass Bottles and Containers Industry Sector

Despite its growth potential, the Canadian glass bottles and containers industry faces several challenges. The primary restraint is the persistent competition from lower-cost alternative packaging materials, such as plastic and aluminum, which often have lower production and transportation costs. Volatility in raw material prices, particularly for sand and soda ash, can impact profit margins. Additionally, the inherent fragility of glass presents logistical challenges, leading to increased costs associated with breakage during transportation and handling, estimated to contribute up to 3% in losses annually. Stringent environmental regulations, while promoting glass, also necessitate significant investment in emission control and waste management technologies.

Emerging Opportunities in Canada Glass Bottles and Containers Industry

Emerging opportunities within the Canadian glass bottles and containers industry are ripe for exploitation. The growing demand for premium and artisanal products across the food, beverage, and cosmetic sectors presents a significant opportunity for manufacturers specializing in high-end, custom-designed glass packaging. The increasing focus on circular economy principles and the rise of the refillable packaging model offer new avenues for innovation and market differentiation. Furthermore, the expansion of e-commerce necessitates the development of more robust and shock-absorbent glass packaging solutions, presenting a niche but growing market. Advancements in glass manufacturing technology, such as the development of antimicrobial glass or smart glass with integrated sensors, also offer promising future applications.

Leading Players in the Canada Glass Bottles and Containers Industry Market

- Richards Packaging Inc

- Vitro Canada

- Salbro Bottle Inc

- Ampak Inc

- Zenan Glass

- Owens-Illinois Inc

Key Developments in Canada Glass Bottles and Containers Industry Industry

- 2023, October: Richards Packaging Inc. announced a significant investment in advanced recycling technology for glass, aiming to increase recycled content by 30% in their products.

- 2023, July: Vitro Canada expanded its production capacity for lightweight beverage bottles, responding to increasing demand for sustainable packaging solutions in the Canadian market.

- 2023, April: Salbro Bottle Inc. launched a new line of custom-designed cosmetic glass containers, focusing on unique shapes and finishes for premium beauty brands.

- 2022, November: Owens-Illinois Inc. partnered with a leading Canadian beverage producer to develop innovative, shatter-resistant glass bottles for wider distribution.

- 2022, August: Zenan Glass introduced eco-friendly manufacturing processes, reducing water consumption by 15% and energy usage by 10% in their operations.

Future Outlook for Canada Glass Bottles and Containers Industry Market

The future outlook for the Canadian glass bottles and containers industry is exceptionally positive, driven by a confluence of sustained consumer demand for sustainable packaging and ongoing technological advancements. The shift towards a circular economy and the increasing emphasis on premiumization across consumer goods will continue to bolster the market. Strategic investments in innovative manufacturing processes, such as lightweighting and energy efficiency, will enhance competitiveness. Furthermore, the industry's ability to adapt to evolving regulatory environments and capitalize on niche market opportunities, like specialized pharmaceutical packaging and aesthetically driven cosmetic containers, will be key to unlocking its full growth potential in the coming decade.

Canada Glass Bottles and Containers Industry Segmentation

-

1. End-User Vertical

- 1.1. Food

- 1.2. Beverage

- 1.3. Pharmaceuticals

- 1.4. Cosmetics

- 1.5. Other End-User Verticals

Canada Glass Bottles and Containers Industry Segmentation By Geography

- 1. Canada

Canada Glass Bottles and Containers Industry Regional Market Share

Geographic Coverage of Canada Glass Bottles and Containers Industry

Canada Glass Bottles and Containers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 5.1.1. Food

- 5.1.2. Beverage

- 5.1.3. Pharmaceuticals

- 5.1.4. Cosmetics

- 5.1.5. Other End-User Verticals

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 6. Canada Glass Bottles and Containers Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 6.1.1. Food

- 6.1.2. Beverage

- 6.1.3. Pharmaceuticals

- 6.1.4. Cosmetics

- 6.1.5. Other End-User Verticals

- 6.1. Market Analysis, Insights and Forecast - by End-User Vertical

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Richards Packaging Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vitro Canada

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Salbro Bottle Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ampak Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zenan Glass

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Owens-Illinois Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 Richards Packaging Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Glass Bottles and Containers Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Glass Bottles and Containers Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Glass Bottles and Containers Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 2: Canada Glass Bottles and Containers Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Canada Glass Bottles and Containers Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 4: Canada Glass Bottles and Containers Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Glass Bottles and Containers Industry?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Canada Glass Bottles and Containers Industry?

Key companies in the market include Richards Packaging Inc, Vitro Canada, Salbro Bottle Inc, Ampak Inc, Zenan Glass, Owens-Illinois Inc.

3. What are the main segments of the Canada Glass Bottles and Containers Industry?

The market segments include End-User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 70.23 billion as of 2022.

5. What are some drivers contributing to market growth?

; Improved Technology Offering Better Solutions; Higher Disposable Income and Integration in Premium Packaging.

6. What are the notable trends driving market growth?

Beverage is Expected to Hold Major Share.

7. Are there any restraints impacting market growth?

Environmental Regulations from Government Bodies over Single-use Plastic Packaging; High Dependence on Raw Material Availability and Pricing.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Glass Bottles and Containers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Glass Bottles and Containers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Glass Bottles and Containers Industry?

To stay informed about further developments, trends, and reports in the Canada Glass Bottles and Containers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence