Key Insights

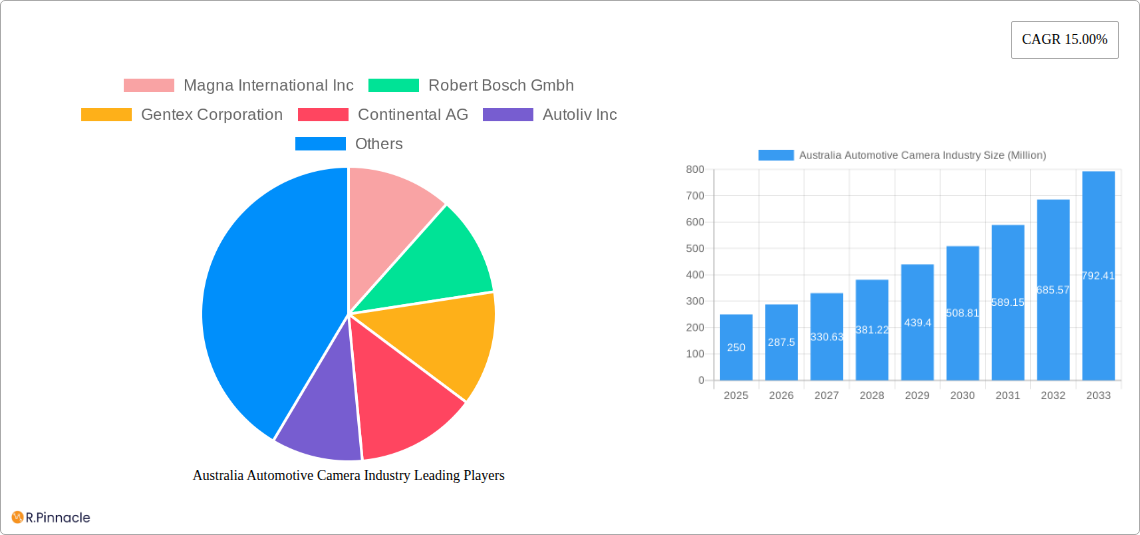

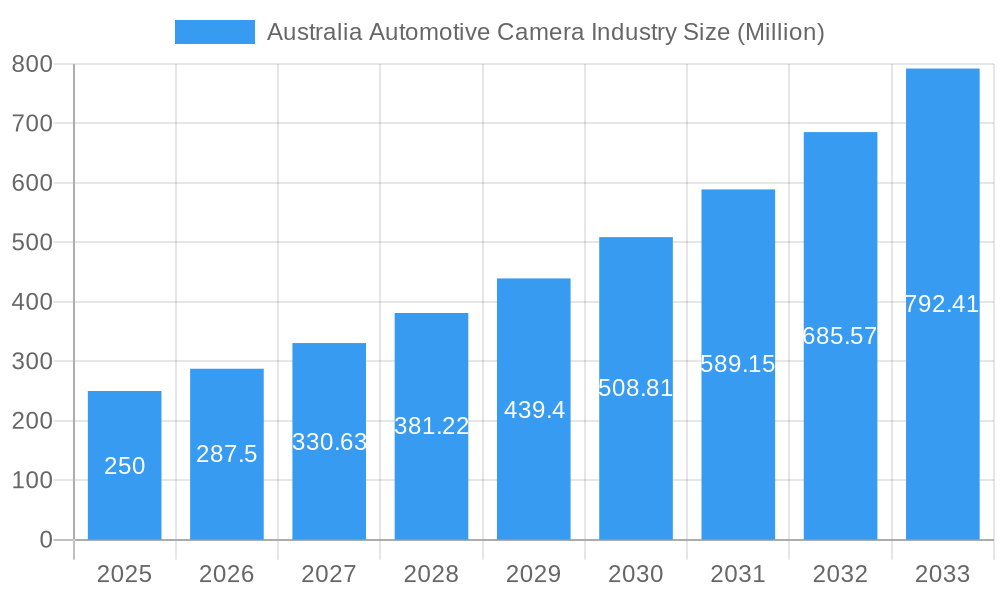

The Australian automotive camera market, valued at $19.1 billion in 2025, is poised for significant expansion. Projected to grow at a compound annual growth rate (CAGR) of 19.5% from 2025 to 2033, this surge is driven by the widespread integration of Advanced Driver-Assistance Systems (ADAS) in passenger and commercial vehicles. Key growth drivers include escalating demand for enhanced vehicle safety, stringent government mandates for road safety, and the rapid evolution of autonomous driving technologies. While viewing cameras currently lead market share, sensing cameras are expected to experience accelerated growth as ADAS functionalities become more sophisticated. The passenger vehicle segment remains dominant, but the commercial vehicle sector presents substantial opportunities, particularly with the increasing emphasis on fleet management and safety within logistics. Leading industry players, including Magna International, Bosch, and Gentex, are actively investing in research and development to innovate camera technologies and ensure seamless vehicle integration, fostering competition and cost-effectiveness.

Australia Automotive Camera Industry Market Size (In Billion)

The market is forecast to exceed $19.1 billion by 2033. Challenges include the substantial initial investment required for advanced camera system integration and the critical need for robust cybersecurity to safeguard against data breaches and system failures. However, continuous technological advancements in image processing and artificial intelligence are expected to overcome these hurdles, propelling the market forward. The Australian government's dedication to fostering automotive sector innovation will further support this growth trajectory.

Australia Automotive Camera Industry Company Market Share

Australia Automotive Camera Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Australian automotive camera market, offering invaluable insights for industry professionals, investors, and strategic planners. Projected to reach \$xx Million by 2033, the market presents significant opportunities despite challenges. This report covers the period 2019-2033, with a focus on 2025 as the base and estimated year. We delve into market structure, dynamics, dominant segments, leading players, and future outlooks, offering actionable intelligence to navigate this rapidly evolving landscape.

Australia Automotive Camera Industry Market Structure & Innovation Trends

The Australian automotive camera market exhibits a moderately concentrated structure, with key players like Magna International Inc, Robert Bosch GmbH, Gentex Corporation, Continental AG, Autoliv Inc, Valeo SA, Hella KGaA Hueck & Co, Garmin Ltd, and Panasonic Corporation holding significant market share. Market share data for 2025 suggests that the top five players collectively account for approximately 65% of the market. Innovation is driven by advancements in sensor technology, image processing, and artificial intelligence (AI), fostering the development of sophisticated ADAS (Advanced Driver Assistance Systems). Regulatory frameworks, such as the increasing adoption of mandatory safety features, are significant market drivers. Product substitutes, such as radar and lidar systems, present some competitive pressure. The market has witnessed several M&A activities in recent years, with deal values exceeding \$xx Million in the period 2019-2024. End-user demographics are shifting towards a preference for vehicles equipped with advanced safety and driver-assistance features.

- Market Concentration: Moderately concentrated, top 5 players holding ~65% market share in 2025.

- Innovation Drivers: Sensor technology, AI, ADAS advancements.

- Regulatory Influence: Mandatory safety features drive demand.

- M&A Activity: Deal values exceeding \$xx Million (2019-2024).

Australia Automotive Camera Industry Market Dynamics & Trends

The Australian automotive camera market is experiencing robust growth, driven by increasing vehicle production, rising consumer preference for safety features, and government regulations mandating ADAS. The market is projected to register a CAGR of xx% during the forecast period (2025-2033). Technological disruptions, such as the integration of 5G connectivity and the development of high-resolution cameras, are shaping market dynamics. Consumer preferences are leaning towards enhanced safety and convenience features, fueling demand for advanced parking assistance systems and driver monitoring systems. Competitive dynamics are characterized by intense innovation and strategic partnerships to improve product offerings and market penetration. Market penetration of automotive cameras in passenger vehicles is estimated at xx% in 2025, expected to grow to xx% by 2033.

Dominant Regions & Segments in Australia Automotive Camera Industry

The major automotive camera market in Australia is concentrated in the populous states of New South Wales and Victoria, driven by higher vehicle ownership and robust infrastructure development.

- Vehicle Type: Passenger vehicles dominate the market due to higher sales volumes and increasing consumer preference for safety and convenience features.

- Camera Type: Sensing cameras hold a larger market share compared to viewing cameras, reflecting the growing demand for ADAS.

- Application: ADAS constitutes the largest segment due to its crucial role in improving road safety. Parking assistance systems also represent a significant segment.

The dominance of passenger vehicles is attributed to larger sales volumes and rising consumer demand for advanced safety technologies. Economic policies supporting sustainable transportation and infrastructure investments further boost market growth.

Australia Automotive Camera Industry Product Innovations

Recent innovations include the introduction of high-resolution cameras with improved low-light performance, fusion of camera data with other sensor inputs for enhanced accuracy, and the development of compact and cost-effective camera modules. These innovations are crucial for meeting evolving market demands and enhancing the safety and convenience of vehicles. The market is also witnessing the emergence of AI-powered cameras capable of object recognition and driver behavior monitoring.

Report Scope & Segmentation Analysis

This report segments the Australian automotive camera market by vehicle type (passenger vehicles, commercial vehicles), camera type (viewing cameras, sensing cameras), and application (ADAS, parking assistance). Each segment's growth projections, market sizes, and competitive dynamics are analyzed, providing a comprehensive understanding of the market landscape. Passenger vehicle segment is expected to grow at a higher CAGR than commercial vehicles, while sensing cameras are projected to witness faster growth due to increased adoption of ADAS features.

Key Drivers of Australia Automotive Camera Industry Growth

Growth is fueled by several factors: increasing vehicle production, stricter government regulations mandating advanced safety features, growing consumer preference for enhanced safety and driver-assistance systems, and technological advancements in sensor technology and image processing. The rising adoption of ADAS across different vehicle segments and the increasing focus on autonomous driving technology are also contributing to market expansion.

Challenges in the Australia Automotive Camera Industry Sector

Challenges include supply chain disruptions impacting component availability and cost, high initial investment costs for advanced camera technologies, and intense competition from established and emerging players. Regulatory compliance requirements also pose challenges. These factors can potentially impact market growth and profitability.

Emerging Opportunities in Australia Automotive Camera Industry

Emerging opportunities lie in the growing adoption of autonomous driving technology, the integration of camera data with other sensor modalities (e.g., radar, lidar), and the development of new applications like driver monitoring systems and advanced parking assistance features. The increasing demand for connected car technologies also presents significant growth potential.

Leading Players in the Australia Automotive Camera Industry Market

Key Developments in Australia Automotive Camera Industry Industry

- 2022 Q3: Magna International announced a new partnership to develop advanced camera systems for autonomous vehicles.

- 2023 Q1: Bosch launched a new generation of high-resolution cameras with improved night vision capabilities. (Further developments can be added here)

Future Outlook for Australia Automotive Camera Industry Market

The Australian automotive camera market is poised for continued strong growth, driven by technological advancements, rising demand for safety features, and supportive government regulations. The increasing integration of cameras into autonomous driving systems and the expansion of ADAS features will further stimulate market expansion. Strategic partnerships and technological innovations will be crucial for players to maintain a competitive edge in this dynamic market.

Australia Automotive Camera Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Viewing Camera

- 2.2. Sensing Camera

-

3. Application

- 3.1. Advanced Driver Assistance Systems

- 3.2. Parking

Australia Automotive Camera Industry Segmentation By Geography

- 1. Australia

Australia Automotive Camera Industry Regional Market Share

Geographic Coverage of Australia Automotive Camera Industry

Australia Automotive Camera Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Viewing Camera

- 5.2.2. Sensing Camera

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Advanced Driver Assistance Systems

- 5.3.2. Parking

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Australia Automotive Camera Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Viewing Camera

- 6.2.2. Sensing Camera

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Advanced Driver Assistance Systems

- 6.3.2. Parking

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Magna International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Robert Bosch Gmbh

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Gentex Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Continental AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Autoliv Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Valeo SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hella KGaA Hueck & Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Garmin Lt

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Panasonic Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Magna International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Automotive Camera Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia Automotive Camera Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Automotive Camera Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Australia Automotive Camera Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Australia Automotive Camera Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Australia Automotive Camera Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Australia Automotive Camera Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Australia Automotive Camera Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 7: Australia Automotive Camera Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Australia Automotive Camera Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Automotive Camera Industry?

The projected CAGR is approximately 19.5%.

2. Which companies are prominent players in the Australia Automotive Camera Industry?

Key companies in the market include Magna International Inc, Robert Bosch Gmbh, Gentex Corporation, Continental AG, Autoliv Inc, Valeo SA, Hella KGaA Hueck & Co, Garmin Lt, Panasonic Corporation.

3. What are the main segments of the Australia Automotive Camera Industry?

The market segments include Vehicle Type, Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Surge in Awareness About the Benefits of Leasing; Shift in Trends Towards Rental.

6. What are the notable trends driving market growth?

Sensing Camera to Witness the Fastest Growth.

7. Are there any restraints impacting market growth?

Labor Shortage may obstruct the market growth; The economic downturn in the equipment leasing sector will impede market expansion.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Automotive Camera Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Automotive Camera Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Automotive Camera Industry?

To stay informed about further developments, trends, and reports in the Australia Automotive Camera Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence