Key Insights

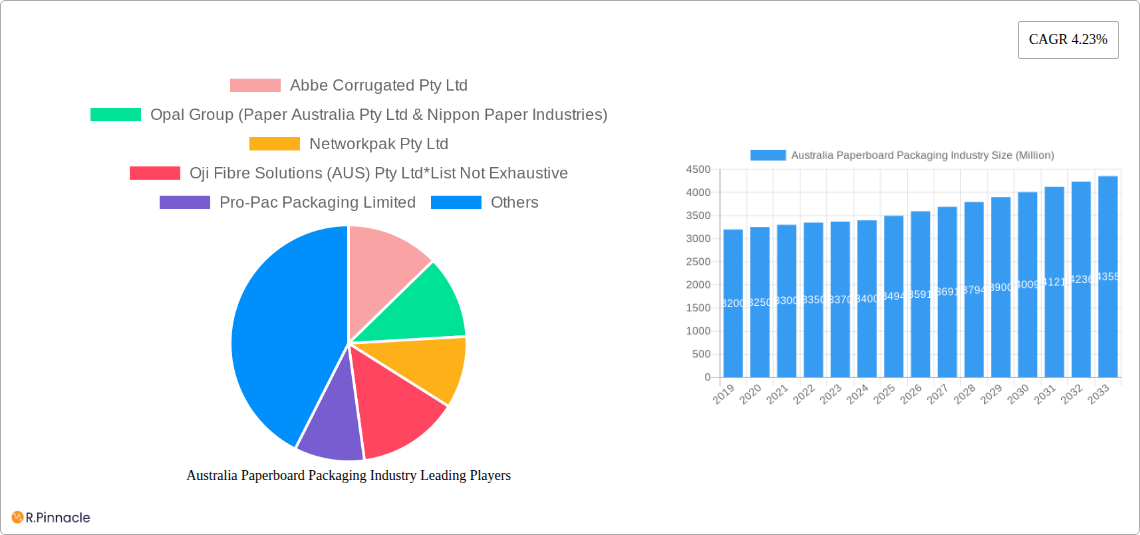

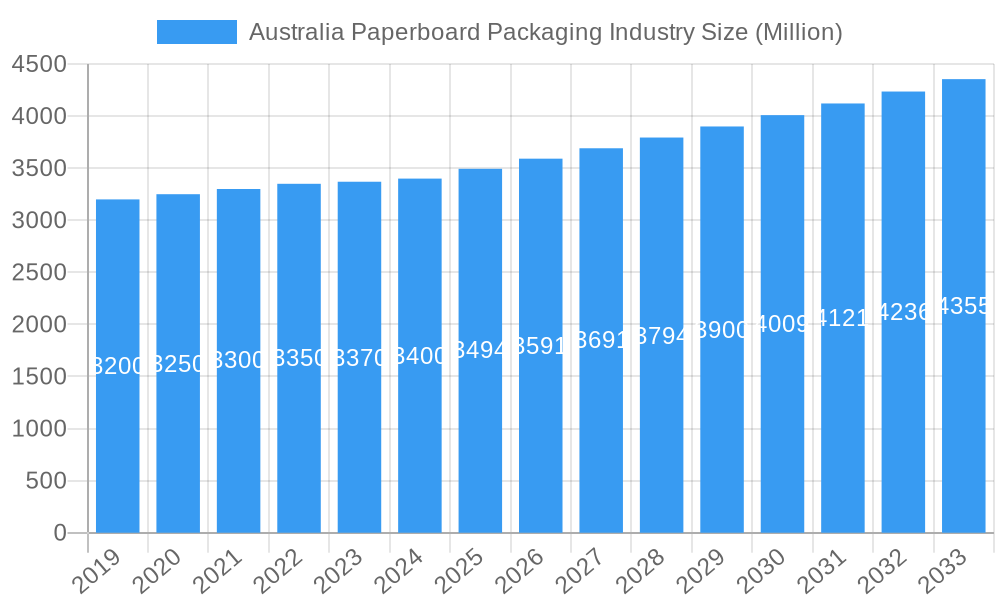

The Australian paperboard packaging market is poised for steady growth, currently valued at approximately USD 3.4 billion in 2024. This expansion is driven by a robust CAGR of 2.9% projected from 2025 to 2033. Key growth catalysts include the increasing demand for sustainable and eco-friendly packaging solutions across major industries. The food and beverage sector, a dominant force in the Australian economy, continues to be the primary consumer of paperboard packaging, propelled by evolving consumer preferences for convenience and single-serve portions, as well as a rising focus on product safety and shelf appeal. The pharmaceutical and healthcare industry also presents a significant growth avenue, influenced by an aging population and increased healthcare awareness, necessitating reliable and protective packaging. Furthermore, the personal care and household care segments are witnessing a surge in demand for aesthetically pleasing and environmentally conscious packaging, directly benefiting the paperboard market.

Australia Paperboard Packaging Industry Market Size (In Billion)

While the market demonstrates resilience, certain factors could influence its trajectory. The increasing adoption of alternative packaging materials and the fluctuating costs of raw materials, such as recycled paper and virgin pulp, represent potential restraints. However, ongoing innovation in paperboard technology, including advancements in barrier properties and printability, alongside a strong regulatory push towards recyclable and compostable materials, are expected to mitigate these challenges. The market is segmented by material, with folding cartons and corrugated boxes holding the largest shares due to their versatility and widespread application. Other materials like flexible paper and liquid cartons are also gaining traction. Key players in the Australian market, including Visy Industries, Opal Group, and Oji Fibre Solutions, are actively investing in R&D and capacity expansion to meet the growing demand and capitalize on emerging trends. The focus remains on delivering cost-effective, sustainable, and high-performance packaging solutions to a diverse range of end-user industries.

Australia Paperboard Packaging Industry Company Market Share

Australia Paperboard Packaging Industry Market: Comprehensive Growth & Innovation Report (2019–2033)

Unlock critical insights into the thriving Australian paperboard packaging sector with our in-depth market analysis. This report, covering the study period of 2019–2033, provides a granular view of market structure, dynamics, regional dominance, and key players. Leveraging high-ranking keywords such as "Australian packaging market," "corrugated box industry Australia," "folding carton manufacturers Australia," and "sustainable packaging Australia," this report is an essential resource for industry professionals, investors, and strategists seeking to capitalize on the market's substantial growth. With a base year of 2025 and a forecast period extending to 2033, this analysis delivers actionable intelligence for strategic decision-making.

Australia Paperboard Packaging Industry Market Structure & Innovation Trends

The Australian paperboard packaging market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, particularly in the corrugated boxes segment. Innovation is primarily driven by the increasing demand for sustainable and eco-friendly packaging solutions, alongside advancements in printing and material science. Regulatory frameworks, such as those promoting recycling and waste reduction, are shaping product development and manufacturing processes. Product substitutes include plastics and other rigid packaging materials, but paperboard's recyclability and biodegradability are key competitive advantages. End-user demographics are shifting towards environmentally conscious consumers and businesses prioritizing brand image and sustainability. Mergers and acquisitions (M&A) activities, while not always publicly disclosed with specific values, are present as companies seek to expand their market reach and integrate their supply chains.

- Market Concentration: Dominated by key players with substantial market share in corrugated and folding carton segments.

- Innovation Drivers: Sustainability, circular economy principles, advanced printing technologies, and lightweighting.

- Regulatory Frameworks: Focus on waste management, recycling rates, and reduced environmental impact.

- Product Substitutes: Plastics, metal cans, and glass containers, with paperboard's eco-friendliness as a differentiator.

- End-User Demographics: Growing demand from e-commerce, food & beverage, and healthcare sectors.

- M&A Activities: Strategic acquisitions to enhance capabilities, market access, and sustainability portfolios.

Australia Paperboard Packaging Industry Market Dynamics & Trends

The Australian paperboard packaging market is poised for robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) through the forecast period. This expansion is propelled by a confluence of powerful market growth drivers, including the burgeoning e-commerce sector, which necessitates efficient and protective packaging solutions. The increasing consumer preference for sustainable and recyclable materials is a critical trend, pushing manufacturers towards innovative fiber-based packaging that minimizes environmental impact. Technological disruptions are evident in the adoption of advanced printing techniques, digital printing for customization, and the development of smart packaging solutions that offer enhanced functionality. Competitive dynamics are characterized by intense competition among established players and the emergence of niche manufacturers focusing on specialized applications. Market penetration is high across major end-user industries, with significant opportunities for further growth in emerging sectors and regions. The adoption of circular economy principles is reshaping the industry's approach to resource utilization and waste reduction.

The food and beverage industry continues to be a cornerstone of demand, driven by consistent consumption and the need for safe, attractive packaging. The pharmaceutical and healthcare sector's demand is fueled by an aging population and increased healthcare awareness, requiring specialized and secure packaging. The personal care and household care segments are influenced by consumer trends towards premiumization and eco-conscious product choices, translating into demand for aesthetically pleasing and sustainable paperboard packaging. The rise of online retail has dramatically amplified the need for durable and efficient corrugated boxes, while folding cartons remain vital for consumer goods requiring shelf appeal. The broader economic landscape, including government initiatives supporting local manufacturing and sustainability targets, also plays a pivotal role in shaping market trajectories. Furthermore, ongoing research and development in paperboard coatings and barrier properties are addressing the challenges of moisture and grease resistance, expanding the applicability of paperboard across a wider range of products. The industry's ability to adapt to evolving consumer preferences, regulatory mandates, and technological advancements will be key to sustained growth and competitive advantage.

Dominant Regions & Segments in Australia Paperboard Packaging Industry

The Australian paperboard packaging industry is characterized by significant regional and segmental dominance, driven by distinct economic, demographic, and industry-specific factors.

Dominant Regions

- New South Wales (NSW) and Victoria: These eastern states are the industrial heartlands of Australia, boasting the largest populations, highest economic activity, and the most developed infrastructure. This concentration of consumers and businesses translates into the highest demand for paperboard packaging across all segments. Major manufacturing hubs and distribution networks are located here, facilitating efficient production and delivery. Government support for manufacturing and innovation in these regions further bolsters their dominance.

- Queensland: With a growing population and a strong agricultural and food production base, Queensland represents a significant and expanding market for paperboard packaging, particularly for food and beverage exports. Infrastructure development in key logistical hubs is enhancing its market potential.

- Western Australia: Driven by its resource-based economy and increasing population, Western Australia demonstrates a strong demand for industrial and consumer packaging. Its geographical isolation also emphasizes the need for robust and reliable packaging solutions.

Dominant Segments

Material:

- Corrugated Boxes: This segment holds the largest market share due to its widespread use in e-commerce, logistics, and the transportation of goods across all industries. Its durability, cost-effectiveness, and recyclability make it the preferred choice for protective packaging. Key drivers include the explosive growth of online retail and the need for efficient supply chain solutions.

- Folding Cartons: This segment is crucial for consumer-facing products, offering excellent printability for branding and product information. The food & beverage, pharmaceutical, and personal care industries are major consumers. The demand for attractive and informative packaging to enhance shelf appeal and convey product value drives this segment's dominance.

- Other Materials (Flexible Paper, Liquid Cartons): While smaller in market share compared to corrugated and folding cartons, this segment is experiencing steady growth. Flexible paper packaging is gaining traction for its versatility and lightweight properties, especially in food packaging. Liquid cartons are vital for the dairy, juice, and beverage sectors, with increasing demand for shelf-stable and convenient packaging solutions.

End-User Industry:

- Food: This is the largest end-user industry, encompassing a vast range of products from fresh produce to processed goods. Paperboard packaging is essential for product protection, shelf life extension, and consumer appeal. The demand for sustainable food packaging is particularly high.

- Beverage: This sector relies heavily on paperboard for multipacks, cartons for juices and milk, and outer packaging for bottled and canned beverages. Convenience and brand visibility are key drivers.

- Pharmaceutical and Healthcare: Stringent requirements for product safety, tamper-evidence, and information dissemination make paperboard packaging critical for medicines, medical devices, and healthcare products. Growth is driven by an aging population and increasing health awareness.

- Personal Care and Household Care: This segment demands visually appealing and informative packaging to attract consumers. Paperboard is widely used for cosmetics, toiletries, cleaning products, and other household essentials, with a growing emphasis on sustainable and premium presentations.

Australia Paperboard Packaging Industry Product Innovations

Product innovations in the Australian paperboard packaging industry are increasingly focused on enhancing sustainability, functionality, and consumer engagement. Advancements include the development of biodegradable and compostable paperboard materials, alongside improved barrier coatings to extend product shelf life for food and beverages. Digital printing technologies are enabling greater customization and on-demand production of folding cartons and corrugated boxes, catering to the personalized demands of e-commerce and promotional campaigns. Smart packaging solutions, incorporating QR codes or NFC tags, are emerging to provide consumers with product information, traceability, and interactive experiences. These innovations provide competitive advantages by meeting evolving market demands for eco-friendly, efficient, and engaging packaging.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Australian paperboard packaging industry, segmented by material and end-user industry.

Material Segmentation:

- Folding Cartons: This segment, vital for consumer goods, is projected for steady growth driven by demand from the food, beverage, pharmaceutical, and personal care sectors. Its aesthetic appeal and printability are key market advantages.

- Corrugated Boxes: Expected to witness substantial growth, primarily fueled by the booming e-commerce sector and the ongoing need for robust transit packaging. Its durability and cost-effectiveness are major contributors to its market share.

- Other Materials (Flexible Paper, Liquid Cartons): This segment, encompassing niche applications, is anticipated to grow as demand for specialized packaging solutions like liquid cartons for beverages and flexible paper for food packaging increases.

End-User Industry Segmentation:

- Beverage: A consistently strong market, driven by the demand for multipack solutions and cartons for various beverages. Sustainable packaging trends are influencing product innovation.

- Food: The largest end-user, with paperboard being essential for a wide array of food products. Growth is propelled by consumer preferences for safe, convenient, and eco-friendly packaging.

- Pharmaceutical and Healthcare: This segment, characterized by stringent regulatory requirements, will see continued growth due to an aging population and increased healthcare spending.

- Personal Care and Household Care: Demand in this segment is influenced by premiumization and the growing consumer preference for aesthetically pleasing and sustainable packaging.

- Other End-user Industries: This includes sectors like electronics, automotive, and industrial goods, where paperboard packaging serves protective and transit needs.

Key Drivers of Australia Paperboard Packaging Industry Growth

The growth of the Australian paperboard packaging industry is propelled by several key drivers. The escalating demand for sustainable and recyclable packaging solutions, driven by consumer awareness and regulatory pressures, is a primary catalyst. The robust expansion of the e-commerce sector necessitates efficient, protective, and cost-effective shipping solutions, heavily favoring corrugated boxes. Technological advancements in printing and material science, leading to enhanced product appeal and functionality, also contribute significantly. Furthermore, supportive government policies promoting local manufacturing and circular economy principles are creating a favorable business environment for paperboard packaging producers.

Challenges in the Australia Paperboard Packaging Industry Sector

Despite strong growth prospects, the Australian paperboard packaging industry faces several challenges. Fluctuations in raw material costs, particularly for pulp and paper, can impact profitability. Intense competition from both domestic and international players, as well as from alternative packaging materials like plastics, exerts price pressure. Stringent environmental regulations, while driving innovation, can also increase compliance costs and require significant investment in new technologies. Supply chain disruptions, including logistics and transportation issues, can affect timely delivery and operational efficiency. Additionally, the need for continuous investment in machinery and technology to keep pace with innovation and sustainability demands presents a capital expenditure challenge.

Emerging Opportunities in Australia Paperboard Packaging Industry

Emerging opportunities within the Australian paperboard packaging industry are centered around innovation and sustainability. The growing consumer demand for eco-friendly products is creating significant opportunities for compostable and biodegradable paperboard solutions. The expansion of niche markets, such as specialized packaging for organic foods or premium artisanal products, offers higher value propositions. Advancements in smart packaging, including track-and-trace capabilities and interactive features, present avenues for differentiation and value-added services. Furthermore, the increasing focus on a circular economy is driving opportunities in advanced recycling technologies and the development of closed-loop systems, fostering innovation in material recovery and reuse.

Leading Players in the Australia Paperboard Packaging Industry Market

- Abbe Corrugated Pty Ltd

- Opal Group (Paper Australia Pty Ltd & Nippon Paper Industries)

- Networkpak Pty Ltd

- Oji Fibre Solutions (AUS) Pty Ltd

- Pro-Pac Packaging Limited

- Austcor Packaging Pty Ltd

- JacPak Pty Ltd

- Visy Industries (Visy Industries Holdings Pty Ltd)

- United Printing & Packaging Company

List Not Exhaustive

Key Developments in Australia Paperboard Packaging Industry Industry

- August 2022: Opal, a part of the Nippon Paper Group, invested in building a high-speed regional cardboard packaging manufacturing facility in Barnawartha, Victoria, Australia, with more than AUD 140 billion (USD 93.35 billion) investment. The Victorian government will support the development of the new manufacturing facility, allowing the company to serve growing markets and cater to increasing customer demands. It will be in tandem with the company's circular economy approach and vision to drive growth in sustainable fiber packaging.

Future Outlook for Australia Paperboard Packaging Industry Market

The future outlook for the Australian paperboard packaging industry remains exceptionally positive, fueled by an unwavering commitment to sustainability and the continued growth of key end-user sectors. The market is expected to be driven by innovations in biodegradable and recyclable materials, aligning with global environmental imperatives and increasingly stringent government regulations. The burgeoning e-commerce landscape will continue to demand robust and efficient corrugated packaging solutions, while folding cartons will see sustained demand for their role in consumer engagement and brand storytelling. Strategic investments in advanced manufacturing technologies and the adoption of circular economy principles will further enhance the industry's competitiveness and environmental credentials, positioning Australia as a leader in responsible and innovative paperboard packaging solutions.

Australia Paperboard Packaging Industry Segmentation

-

1. Material

- 1.1. Folding Cartons

- 1.2. Corrugated Boxes

- 1.3. Other Materials (Flexible Paper, Liquid Cartons)

-

2. End-User Industry

- 2.1. Beverage

- 2.2. Food

- 2.3. Pharmaceutical and Healthcare

- 2.4. Personal Care and Household Care

- 2.5. Other End-user Industries

Australia Paperboard Packaging Industry Segmentation By Geography

- 1. Australia

Australia Paperboard Packaging Industry Regional Market Share

Geographic Coverage of Australia Paperboard Packaging Industry

Australia Paperboard Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Folding Cartons

- 5.1.2. Corrugated Boxes

- 5.1.3. Other Materials (Flexible Paper, Liquid Cartons)

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Beverage

- 5.2.2. Food

- 5.2.3. Pharmaceutical and Healthcare

- 5.2.4. Personal Care and Household Care

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Australia Paperboard Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Folding Cartons

- 6.1.2. Corrugated Boxes

- 6.1.3. Other Materials (Flexible Paper, Liquid Cartons)

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Beverage

- 6.2.2. Food

- 6.2.3. Pharmaceutical and Healthcare

- 6.2.4. Personal Care and Household Care

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Abbe Corrugated Pty Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Opal Group (Paper Australia Pty Ltd & Nippon Paper Industries)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Networkpak Pty Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Oji Fibre Solutions (AUS) Pty Ltd*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Pro-Pac Packaging Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Austcor Packaging Pty Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 JacPak Pty Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Visy Industries (Visy Industries Holdings Pty Ltd)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 United Printing & Packaging Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Abbe Corrugated Pty Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Paperboard Packaging Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Australia Paperboard Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Paperboard Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Australia Paperboard Packaging Industry Revenue undefined Forecast, by End-User Industry 2020 & 2033

- Table 3: Australia Paperboard Packaging Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Australia Paperboard Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 5: Australia Paperboard Packaging Industry Revenue undefined Forecast, by End-User Industry 2020 & 2033

- Table 6: Australia Paperboard Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Paperboard Packaging Industry?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the Australia Paperboard Packaging Industry?

Key companies in the market include Abbe Corrugated Pty Ltd, Opal Group (Paper Australia Pty Ltd & Nippon Paper Industries), Networkpak Pty Ltd, Oji Fibre Solutions (AUS) Pty Ltd*List Not Exhaustive, Pro-Pac Packaging Limited, Austcor Packaging Pty Ltd, JacPak Pty Ltd, Visy Industries (Visy Industries Holdings Pty Ltd), United Printing & Packaging Company.

3. What are the main segments of the Australia Paperboard Packaging Industry?

The market segments include Material, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand from the Food and Beverage Sector; Increasing Growth of E-commerce Creating Demand for Various Paper and Paperboard Packaging Types.

6. What are the notable trends driving market growth?

Corrugated Boxes are Expected to Hold Significant Share.

7. Are there any restraints impacting market growth?

Growing Usage of Substitute Products.

8. Can you provide examples of recent developments in the market?

August 2022: Opal, a part of the Nippon Paper Group, invested in building a high-speed regional cardboard packaging manufacturing facility in Barnawartha, Victoria, Australia, with more than AUD 140 million (USD 93.35 million) investment. The Victorian government will support the development of the new manufacturing facility, allowing the company to serve growing markets and cater to increasing customer demands. It will be in tandem with the company's circular economy approach and vision to drive growth in sustainable fiber packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Paperboard Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Paperboard Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Paperboard Packaging Industry?

To stay informed about further developments, trends, and reports in the Australia Paperboard Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence