Key Insights

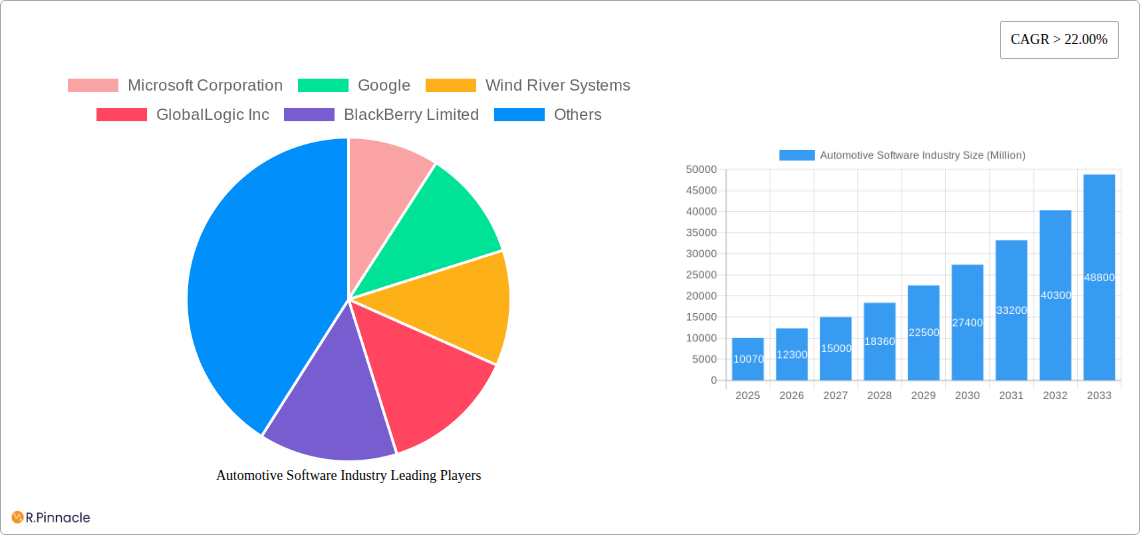

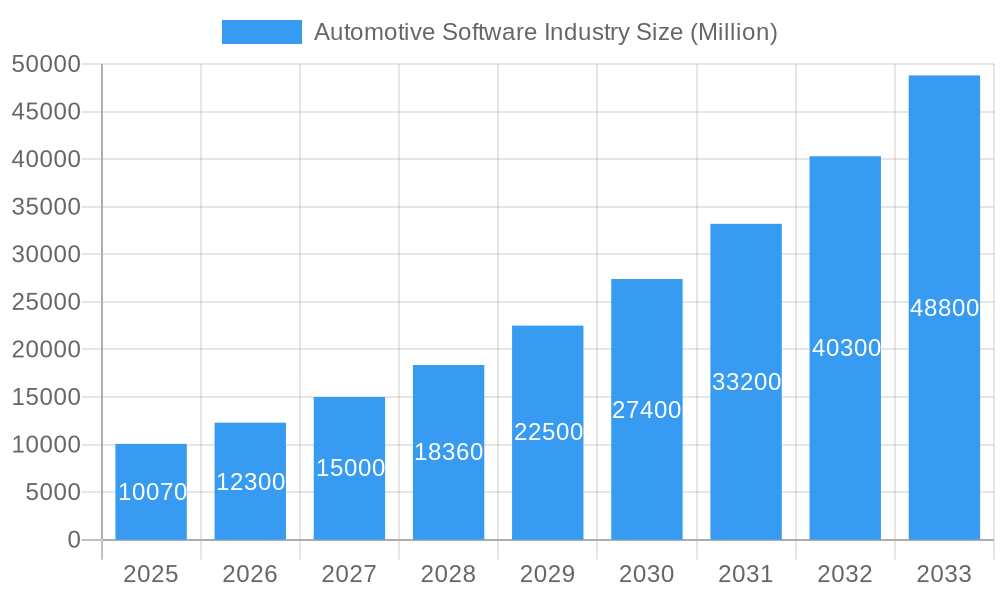

The automotive software market is experiencing explosive growth, projected to reach $10.07 billion in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) exceeding 22% from 2025 to 2033. This surge is driven by several key factors. The increasing demand for advanced driver-assistance systems (ADAS), encompassing features like autonomous emergency braking and lane-keeping assist, is a major catalyst. Furthermore, the proliferation of infotainment systems, offering connected navigation, entertainment streaming, and in-car communication, significantly fuels market expansion. The growing integration of vehicle connectivity solutions, enabling features like remote diagnostics and over-the-air updates, further contributes to this upward trajectory. The shift towards electric vehicles (EVs) also presents a significant opportunity, requiring sophisticated software for battery management, powertrain control, and charging optimization. Segmentation reveals a strong presence across both passenger cars and commercial vehicles, with safety and security applications leading the charge. Key players like Microsoft, Google, and Bosch are actively shaping the market landscape through innovation and strategic partnerships. Geographic analysis indicates strong growth across North America, Europe, and the Asia-Pacific region, fueled by varying levels of technological adoption and government regulations.

Automotive Software Industry Market Size (In Billion)

The market's rapid expansion is expected to continue throughout the forecast period, primarily due to ongoing advancements in artificial intelligence (AI) and machine learning (ML) technologies. These innovations are paving the way for more sophisticated driver assistance features, enhanced autonomous driving capabilities, and improved vehicle safety systems. The increasing focus on cybersecurity within the automotive industry is another critical driver, prompting greater investment in secure software solutions to mitigate potential vulnerabilities. The integration of software-defined vehicles (SDVs) is also a game-changer, enabling greater flexibility, customization, and functionality. However, challenges remain, including the high cost of development and integration of complex software systems and the need for robust cybersecurity measures to prevent potential attacks. Overcoming these hurdles will be essential for sustained and responsible growth in the automotive software sector.

Automotive Software Industry Company Market Share

Automotive Software Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Automotive Software Industry, offering valuable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, key players, emerging trends, and future growth potential. The global market is projected to reach xx Million by 2033, showcasing substantial growth opportunities.

Automotive Software Industry Market Structure & Innovation Trends

The automotive software market is characterized by a dynamic and evolving landscape. While a few prominent technology giants such as Microsoft Corporation, Google, and Robert Bosch GmbH exert significant influence, holding a substantial portion of the market share, a vibrant ecosystem of specialized companies actively fuels innovation and growth. Companies like Wind River Systems, GlobalLogic Inc, BlackBerry Limited, Intellias Ltd, KPIT Technologies Limited, HARMAN International, MontaVista Software LLC, and Airbiquity Inc are at the forefront of developing cutting-edge solutions.

The relentless pursuit of innovation is primarily propelled by the escalating demand for sophisticated Advanced Driver-Assistance Systems (ADAS), the transformative capabilities of autonomous driving, and the ubiquitous integration of connected car technologies. Furthermore, stringent regulatory mandates governing vehicle safety and emissions serve as powerful catalysts for advancements in automotive software. The market currently exhibits limited direct product substitutes, with competition largely centered around differentiated software solutions and integrated hardware-software platforms from various vendors. The end-user base is remarkably diverse, encompassing individual car owners, ride-sharing services, and large-scale fleet operators, each with unique software requirements.

The industry is witnessing a surge in Mergers and Acquisitions (M&A) activity. In recent years, deal values have consistently surpassed significant financial thresholds, underscoring the strategic imperative of software in modern vehicle development. These M&A transactions are instrumental in driving technological progress, consolidating market expertise, and accelerating the realization of future mobility concepts.

- Market Concentration: The market is moderately consolidated, with a concentration of market share among a few key players, yet a broad base of innovative contributors.

- Innovation Drivers: Key innovation drivers include the development of ADAS, autonomous driving systems, pervasive connected car features, and adherence to evolving regulatory standards for safety and environmental impact.

- M&A Activity: Significant M&A activity is a defining characteristic, with substantial annual deal values reflecting the strategic value of software in the automotive sector.

Automotive Software Industry Market Dynamics & Trends

The automotive software market is experiencing rapid growth, driven by the increasing adoption of software-defined vehicles (SDVs) and the rising demand for advanced functionalities. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological disruptions, such as the proliferation of artificial intelligence (AI), machine learning (ML), and 5G connectivity, are accelerating this growth. Consumer preferences are shifting towards vehicles with sophisticated infotainment systems, enhanced safety features, and seamless connectivity.

Competitive dynamics are intense, with established players facing challenges from emerging technology companies and startups. Market penetration of advanced software features varies across regions and vehicle types, with passenger cars currently leading the adoption rate. The increasing integration of over-the-air (OTA) updates is transforming the automotive landscape and improving customer experience. Market penetration of these features is expected to significantly increase throughout the forecast period.

Dominant Regions & Segments in Automotive Software Industry

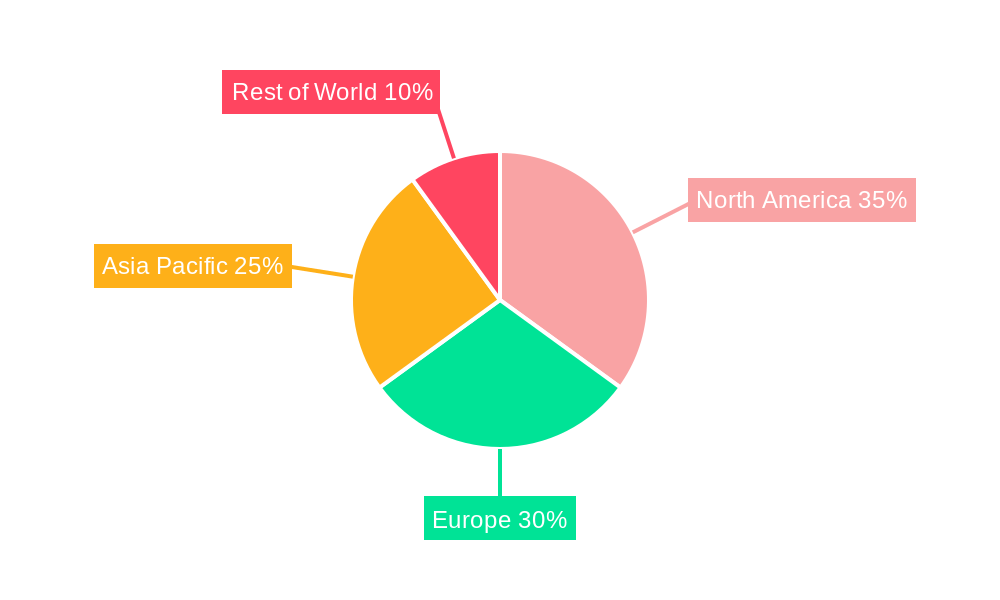

Geographically, the automotive software market exhibits distinct regional strengths. North America and Europe currently lead in market dominance, propelled by established automotive industries, high vehicle ownership, robust technological infrastructure, and supportive government initiatives. However, the Asia-Pacific region is emerging as a powerhouse of rapid growth, driven by its expanding economies, escalating vehicle production volumes, and a burgeoning middle class keen on advanced automotive technologies.

-

By Application:

- Safety and Security: This segment stands out as the fastest-growing, driven by increasingly stringent safety regulations and the demand for advanced cybersecurity solutions.

- Infotainment and Instrument Cluster: This segment commands a substantial market share, fueled by consumers' growing expectations for sophisticated and integrated in-car entertainment and information systems.

- Vehicle Connectivity: The proliferation of connected car technologies, enabling V2X communication, remote diagnostics, and enhanced user experiences, is spurring significant growth in this segment.

- Other Applications (Powertrain): This segment demonstrates steady growth, influenced by the global shift towards vehicle electrification and the continuous innovation in advanced powertrain management systems for optimal performance and efficiency.

-

By Vehicle Type:

- Passenger Cars: This segment constitutes the largest portion of the market, driven by the demand for premium features, comfort, and advanced driving technologies in personal vehicles.

- Commercial Vehicles: This segment is experiencing notable growth, propelled by the adoption of fleet management solutions, enhanced safety features for professional drivers, and the integration of telematics for operational efficiency.

Automotive Software Industry Product Innovations

Recent product developments focus on enhancing vehicle safety, improving driver assistance systems, integrating advanced infotainment features, and streamlining vehicle connectivity. The integration of AI and machine learning allows for the development of adaptive and predictive software applications, improving efficiency and user experience. The transition to software-defined vehicles is a key technological trend, providing manufacturers with more flexibility and agility in updating and enhancing vehicle functionalities. This innovation addresses consumer demands for greater personalization and feature upgrades throughout the vehicle's lifecycle.

Report Scope & Segmentation Analysis

This report offers an in-depth analysis of the automotive software market, meticulously segmented by application categories including Safety and Security, Infotainment and Instrument Cluster, Vehicle Connectivity, and Other Applications. Additionally, it provides a detailed breakdown by vehicle type, covering Passenger Cars and Commercial Vehicles. Within each segment, the report delves into growth projections, current market sizes, and the intricate competitive dynamics at play. Furthermore, it explores various sub-segments, offering granular insights into their unique growth trajectories and untapped market potential. The analysis also considers how regional technological advancements and shifting demand patterns influence the growth rates of each segment.

Key Drivers of Automotive Software Industry Growth

Several factors drive the growth of the automotive software industry. These include the increasing demand for advanced driver-assistance systems (ADAS), the rise of connected and autonomous vehicles, stringent government regulations promoting vehicle safety and emissions reduction, and the growing adoption of software-defined vehicles (SDVs) enabling over-the-air updates. Furthermore, technological advancements in artificial intelligence, machine learning, and 5G connectivity provide new opportunities for innovation and growth in this sector. The increasing consumer preference for enhanced in-vehicle infotainment systems and connectivity is an important factor propelling growth as well.

Challenges in the Automotive Software Industry Sector

Despite significant growth opportunities, the automotive software industry faces several challenges. These include the high cost of software development and integration, ensuring software safety and security in vehicles, complex and evolving regulatory landscapes, maintaining robust supply chains during global shortages of components, and the intensifying competition from both established players and new entrants. These factors can significantly impact production timelines, product development costs, and ultimately, the bottom line. The cyber security threats associated with connected vehicles is another notable challenge for the industry.

Emerging Opportunities in Automotive Software Industry

The automotive software industry is ripe with emerging opportunities that promise significant growth and transformative innovation. The widespread adoption of Software-Defined Vehicles (SDVs), where vehicle functionality is increasingly dictated by software rather than hardware, is a primary growth avenue. The exponential rise of electric and autonomous vehicles necessitates sophisticated software for battery management, powertrain control, and autonomous navigation. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into vehicle systems is unlocking new possibilities for predictive maintenance, personalized driving experiences, and enhanced safety features. The development of new revenue streams from data-driven services, such as predictive analytics and personalized infotainment, alongside the increasing reliance on over-the-air (OTA) updates and in-vehicle commerce, represent lucrative opportunities for forward-thinking companies.

Leading Players in the Automotive Software Industry Market

- Microsoft Corporation

- Wind River Systems

- GlobalLogic Inc

- BlackBerry Limited

- Robert Bosch GmbH

- Intellias Ltd

- KPIT Technologies Limited

- HARMAN International

- MontaVista Software LLC

- Airbiquity Inc

Key Developments in Automotive Software Industry

March 2023: Honda Motor and KPIT Technologies Ltd. signed a basic agreement for software development collaboration, focusing on next-generation E/E architecture, electrified powertrains, enhanced safety, automated driving, and IVI. This partnership significantly strengthens KPIT Technologies' position in the market and expands its reach into the high-growth areas of electric vehicles and automated driving.

January 2023: Luxoft and Microsoft partnered for the Connected Fleets project, enhancing Luxoft's capabilities in providing fleet management solutions and accelerating the transition to software-defined cars for its clients. This collaboration leverages Microsoft’s Azure cloud platform and expands Luxoft’s reach within the connected car market.

January 2023: Marelli Corporation selected BlackBerry's QNX Acoustics Management Platform (AMP) for enhanced in-car audio experiences in software-defined vehicles. This highlights the growing importance of advanced audio technologies and the adoption of BlackBerry's QNX platform in the automotive industry.

Future Outlook for Automotive Software Industry Market

The automotive software market is on a trajectory for sustained and robust growth. This upward trend is underpinned by the accelerating shift towards software-defined vehicles, the ever-increasing demand for advanced driver-assistance systems, and the widespread integration of cutting-edge connectivity features that are redefining the driving experience. Strategic opportunities abound for developers of innovative software solutions that adeptly cater to evolving consumer preferences while effectively addressing the critical challenges of vehicle safety, cybersecurity, and seamless scalability. The market is anticipated to witness continued consolidation, with leading players likely to expand their capabilities and market reach through strategic partnerships and targeted acquisitions. The long-term outlook for the automotive software industry remains exceptionally positive, driven by continuous technological advancements and the escalating consumer desire for smarter, safer, and more intrinsically connected automotive experiences.

Automotive Software Industry Segmentation

-

1. Application

- 1.1. Safety and Security

- 1.2. Infotainment and Instrument Cluster

- 1.3. Vehicle Connectivity

- 1.4. Other Applications (Powertrain)

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

Automotive Software Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Automotive Software Industry Regional Market Share

Geographic Coverage of Automotive Software Industry

Automotive Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 22.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Safety and Security

- 5.1.2. Infotainment and Instrument Cluster

- 5.1.3. Vehicle Connectivity

- 5.1.4. Other Applications (Powertrain)

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Safety and Security

- 6.1.2. Infotainment and Instrument Cluster

- 6.1.3. Vehicle Connectivity

- 6.1.4. Other Applications (Powertrain)

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Software Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Safety and Security

- 7.1.2. Infotainment and Instrument Cluster

- 7.1.3. Vehicle Connectivity

- 7.1.4. Other Applications (Powertrain)

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Software Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Safety and Security

- 8.1.2. Infotainment and Instrument Cluster

- 8.1.3. Vehicle Connectivity

- 8.1.4. Other Applications (Powertrain)

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Pacific Automotive Software Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Safety and Security

- 9.1.2. Infotainment and Instrument Cluster

- 9.1.3. Vehicle Connectivity

- 9.1.4. Other Applications (Powertrain)

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Rest of the World Automotive Software Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Safety and Security

- 10.1.2. Infotainment and Instrument Cluster

- 10.1.3. Vehicle Connectivity

- 10.1.4. Other Applications (Powertrain)

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Microsoft Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Google

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Wind River Systems

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 GlobalLogic Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 BlackBerry Limited

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Robert Bosch GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Intellias Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 KPIT Technologies Limited

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 HARMAN International

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 MontaVista Software LLC

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Airbiquity Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.1 Microsoft Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Software Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 9: Europe Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: Europe Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Europe Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Asia Pacific Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Asia Pacific Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 17: Asia Pacific Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 18: Asia Pacific Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Automotive Software Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Rest of the World Automotive Software Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Rest of the World Automotive Software Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 23: Rest of the World Automotive Software Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Rest of the World Automotive Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Rest of the World Automotive Software Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Automotive Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 19: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 20: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: India Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Automotive Software Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 27: Global Automotive Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 28: Global Automotive Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: South America Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa Automotive Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Software Industry?

The projected CAGR is approximately > 22.00%.

2. Which companies are prominent players in the Automotive Software Industry?

Key companies in the market include Microsoft Corporation, Google, Wind River Systems, GlobalLogic Inc, BlackBerry Limited, Robert Bosch GmbH, Intellias Ltd, KPIT Technologies Limited, HARMAN International, MontaVista Software LLC, Airbiquity Inc.

3. What are the main segments of the Automotive Software Industry?

The market segments include Application, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.07 Million as of 2022.

5. What are some drivers contributing to market growth?

The Growth of The Global Automotive Turbocharger Market.

6. What are the notable trends driving market growth?

Growth of Connected Car Technology Aiding the Market's Growth.

7. Are there any restraints impacting market growth?

Increasing Complexity of Modern Vehicles.

8. Can you provide examples of recent developments in the market?

March 2023: Honda Motor signed a basic agreement for a software development relationship with KPIT Technologies Ltd (KPIT Technologies), one of the major software integration partners for the automotive and mobility industries. Through this collaboration, the two companies will pool their respective strengths, particularly Honda's software architecture, control and safety technologies, and KPIT Technologies' software development capabilities, to generate new value through software. As a result of this collaboration, the two companies will collaborate on software development in the following areas: next-generation electrical/electronic (E&E) architecture operating system (OS), electrified powertrains, enhanced safety and automated driving, and IVI (in-vehicle infotainment) and linked technologies.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Software Industry?

To stay informed about further developments, trends, and reports in the Automotive Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence