Key Insights

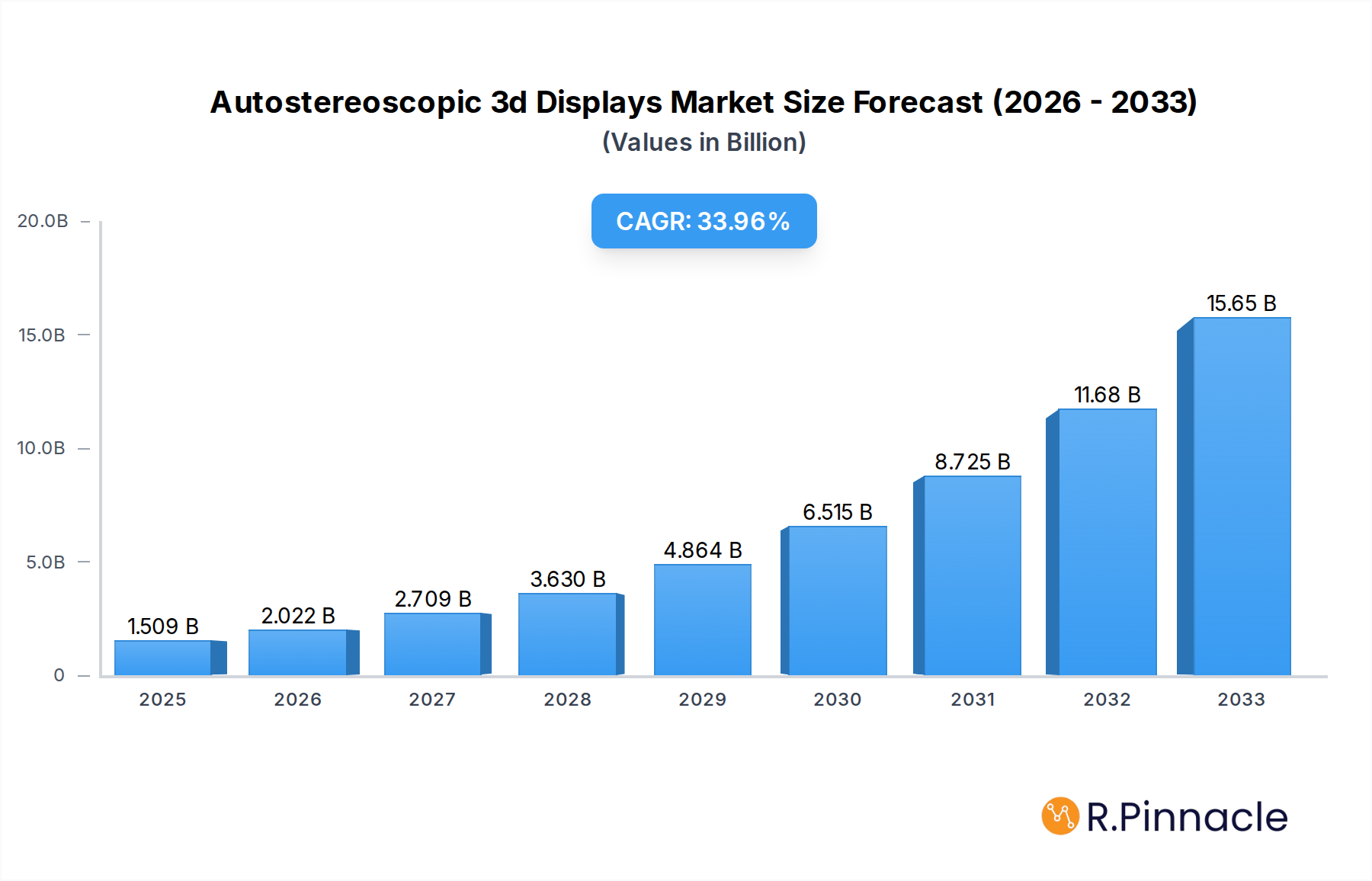

The Autostereoscopic 3D Displays market is poised for remarkable expansion, projected to reach $1509 million by 2025 with an impressive Compound Annual Growth Rate (CAGR) of 34% through 2033. This robust growth is primarily fueled by the increasing demand for immersive entertainment and gaming experiences, where autostereoscopic displays offer a captivating glasses-free 3D viewing dimension. Advancements in technology, leading to higher resolution, wider viewing angles, and improved depth perception, are further stimulating market adoption. The healthcare sector is also emerging as a significant driver, leveraging these displays for enhanced visualization in surgical planning, medical imaging, and training simulations, leading to more precise diagnostics and improved patient outcomes. Furthermore, the education sector is exploring autostereoscopic displays for interactive learning modules and virtual field trips, offering students a more engaging and memorable educational journey.

Autostereoscopic 3d Displays Market Size (In Billion)

The market is segmented by application and technology type, with Entertainment & Gaming and Healthcare representing key growth areas. Parallax Barrier and Lenticular Display Technologies are the dominant types, continually evolving to overcome previous limitations like narrow viewing angles and reduced image brightness. While the market exhibits strong upward momentum, potential restraints include the high initial cost of advanced autostereoscopic displays and the ongoing need for content creators to develop glasses-free 3D material. However, ongoing innovation, strategic collaborations among key players like Samsung, LG, and Royal Philips, and the expanding reach into emerging economies, particularly in the Asia Pacific region, are expected to mitigate these challenges. The continuous development of more affordable and user-friendly autostereoscopic solutions will be crucial in unlocking the full market potential and solidifying its position as a transformative display technology across various industries.

Autostereoscopic 3d Displays Company Market Share

Here is an SEO-optimized, reader-centric report description for Autostereoscopic 3D Displays, designed for industry professionals and maximizing search visibility.

This comprehensive market research report delves into the dynamic landscape of Autostereoscopic 3D Displays, offering deep insights into market structure, innovation trends, growth drivers, challenges, and future outlook. With a robust study period spanning from 2019 to 2033, this report provides an unparalleled analysis for industry stakeholders seeking to capitalize on the evolving 3D display technology market. Our analysis, centered on the Base Year 2025, includes an Estimated Year of 2025 and a Forecast Period from 2025 to 2033, leveraging Historical Period data from 2019 to 2024.

Autostereoscopic 3D Displays Market Structure & Innovation Trends

The autostereoscopic 3D displays market exhibits a moderate to high concentration, with key players like Samsung, LG, and Toshiba investing heavily in research and development. Innovation is primarily driven by advancements in display resolution, reduced crosstalk, wider viewing angles, and the development of glasses-free 3D experiences. Regulatory frameworks, while not overly stringent, are evolving to address consumer safety and content standards, particularly in the entertainment sector. Product substitutes, such as virtual reality (VR) and augmented reality (AR) headsets, present a growing competitive pressure, albeit with different use cases. End-user demographics are expanding beyond early adopters to include mainstream consumers and enterprise solutions. Mergers and acquisitions (M&A) activities are anticipated to increase as larger companies seek to acquire niche technologies and expand their market presence. Estimated M&A deal values are projected to reach XX million in the coming years. The market share of leading companies is estimated to be between 10% and 20% for the top three players.

Autostereoscopic 3D Displays Market Dynamics & Trends

The autostereoscopic 3D displays market is poised for significant growth, driven by an increasing demand for immersive entertainment and enhanced educational experiences. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is approximately XX%. Technological disruptions, including the integration of advanced optics and micro-display technologies, are continuously improving the quality and accessibility of glasses-free 3D. Consumer preferences are shifting towards more intuitive and comfortable 3D viewing, reducing motion sickness and eye strain. This trend is fueled by the growing penetration of 3D content across various platforms, from gaming to professional visualization. Competitive dynamics are characterized by intense innovation, with companies vying to offer superior visual fidelity and unique features. Market penetration is expected to rise from an estimated XX% in 2025 to over XX% by 2033, driven by wider adoption in consumer electronics, automotive displays, and medical imaging. The development of more affordable and energy-efficient autostereoscopic displays will further accelerate market growth, making these advanced visual solutions accessible to a broader audience. The ongoing refinement of parallax barrier and lenticular display technologies, alongside the exploration of novel approaches, will continue to shape the competitive landscape and unlock new application frontiers, contributing to a robust market expansion. The increasing convergence of 3D display technology with AI and machine learning will also unlock new avenues for personalized and interactive 3D experiences.

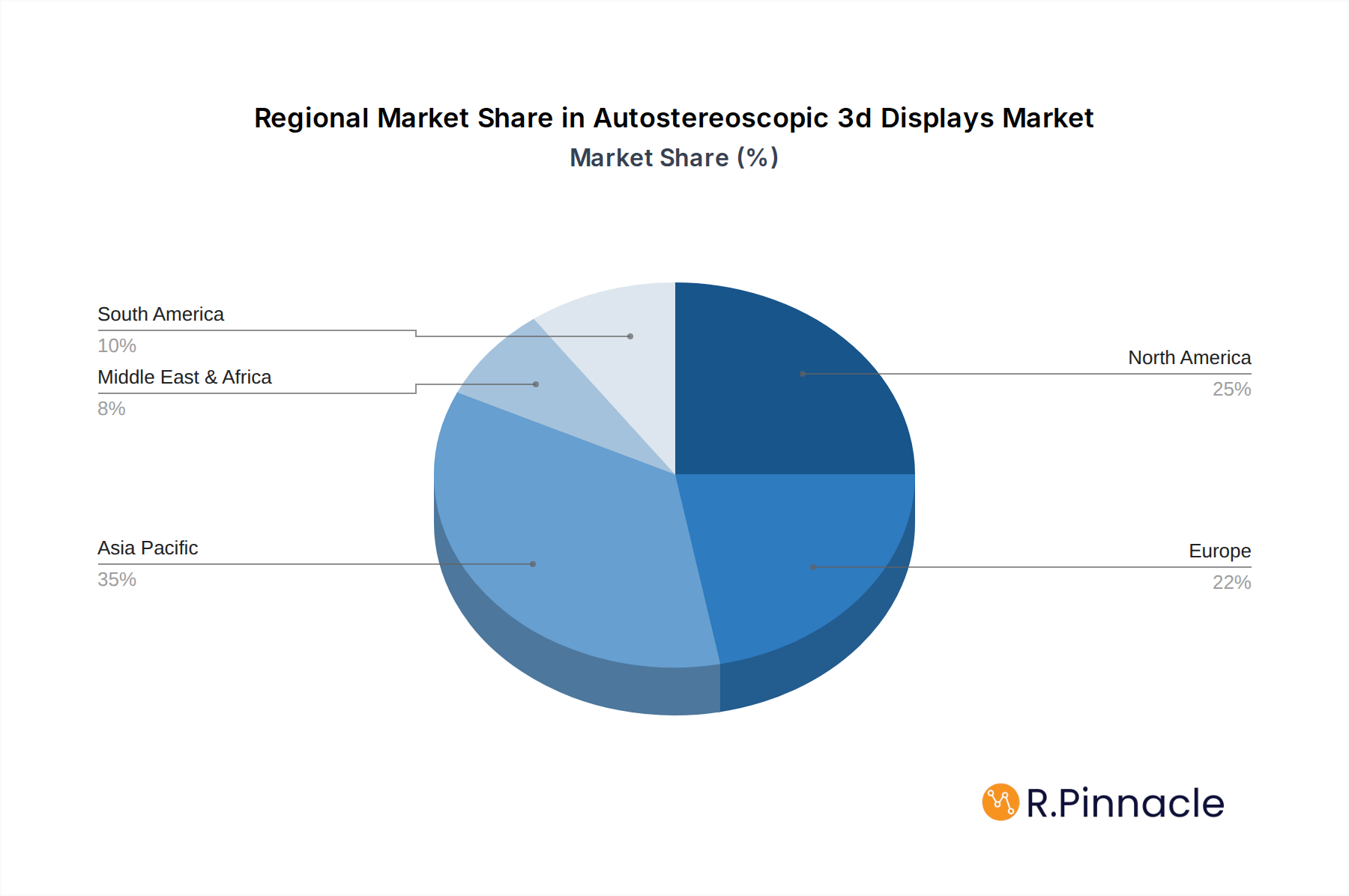

Dominant Regions & Segments in Autostereoscopic 3D Displays

North America is currently the dominant region in the autostereoscopic 3D displays market, driven by strong consumer spending on entertainment and advanced technology adoption. The United States, in particular, leads in the adoption of 3D gaming and home theater systems.

- Application: Entertainment & Gaming: This segment is the largest and fastest-growing, propelled by the demand for immersive gaming experiences and 3D movie playback. High disposable incomes and a strong appetite for cutting-edge technology in North America and parts of Asia contribute to its dominance.

- Key Drivers: High consumer entertainment spending, proliferation of 3D-enabled gaming consoles and PCs, development of compelling 3D game content, and the growing popularity of 3D cinemas.

- Type: Lenticular Display Technology: While Parallax Barrier Technology has seen widespread adoption, Lenticular Display Technology is gaining traction due to its ability to offer wider viewing angles and higher resolution, making it suitable for professional applications and certain consumer devices.

- Key Drivers: Superior viewing angle performance, advancements in lenticular lens manufacturing, and suitability for high-resolution displays.

Asia Pacific is emerging as a significant growth hub, driven by increasing disposable incomes, rapid technological adoption, and a burgeoning entertainment industry in countries like China and South Korea. Economic policies supporting technological innovation and substantial investments in display manufacturing infrastructure are key accelerators in this region. The healthcare and education sectors in these regions are also showing increased interest in autostereoscopic 3D for enhanced training and visualization tools.

Autostereoscopic 3D Displays Product Innovations

Recent product innovations in autostereoscopic 3D displays are focused on enhancing visual clarity, reducing eye strain, and expanding viewing angles without the need for glasses. Companies are developing ultra-high-definition displays with improved pixel density and advanced optical layers to minimize crosstalk. New applications are emerging in automotive dashboards, medical imaging, and digital signage, offering a more engaging and informative user experience. These innovations provide a competitive advantage by differentiating products and catering to specific market needs for immersive and intuitive visual interfaces.

Report Scope & Segmentation Analysis

This report meticulously segments the autostereoscopic 3D displays market across key dimensions. The Application segment is broken down into Entertainment & Gaming, Healthcare, Education & Training, and Others, with Entertainment & Gaming projected to hold the largest market share. The Type segment includes Parallax Barrier Technology, Lenticular Display Technology, and Others. Parallax Barrier Technology is expected to maintain a significant market presence due to its established use, while Lenticular Display Technology is anticipated to experience robust growth, particularly in high-end applications. Growth projections and competitive dynamics for each sub-segment are thoroughly analyzed.

Key Drivers of Autostereoscopic 3D Displays Growth

Several factors are propelling the growth of the autostereoscopic 3D displays market. Technological advancements in display panel manufacturing, including higher resolutions and improved optical elements, are making glasses-free 3D more viable and appealing. The increasing demand for immersive entertainment, particularly in gaming and home cinema, serves as a major catalyst. Furthermore, the growing adoption of 3D visualization in sectors like healthcare for surgical planning and medical training, and in education for interactive learning, is significantly expanding the market's reach. Government initiatives promoting technological innovation and digital transformation also play a crucial role.

Challenges in the Autostereoscopic 3D Displays Sector

Despite its potential, the autostereoscopic 3D displays sector faces several challenges. The cost of manufacturing high-quality glasses-free 3D displays remains a barrier for widespread consumer adoption compared to traditional 2D displays. Technical limitations such as limited viewing angles and crosstalk can still impact the user experience. The relatively slower development of native 3D content compared to 2D content also poses a restraint. Supply chain complexities and the need for specialized components can lead to production bottlenecks and increased costs. Intense competition from other immersive technologies like VR and AR also requires continuous innovation to maintain market relevance.

Emerging Opportunities in Autostereoscopic 3D Displays

Emerging opportunities in the autostereoscopic 3D displays market lie in the expansion into new application areas and the integration of advanced technologies. The automotive sector presents a significant opportunity for heads-up displays (HUDs) and in-car entertainment systems that leverage 3D visualization for enhanced safety and passenger experience. Medical imaging and surgical simulation are also ripe for disruption with autostereoscopic displays offering more intuitive visualization of complex anatomical structures. The development of more affordable and user-friendly devices for consumers, coupled with an increased availability of high-quality 3D content, will further unlock market potential.

Leading Players in the Autostereoscopic 3D Displays Market

- Exceptional 3D

- Royal Philips

- Samsung

- LG

- Alioscopy

- Dolby Laboratories

- Toshiba

- Magnetic Media Holdings

- Leia

- Leyard Opto-Electronic

- Kangde Xin Composite Material Group

- HIKVISION

- Marvel Digital

- Ledman

- Evistek

- TCL

- 3D Global Solutions GmbH

Key Developments in Autostereoscopic 3D Displays Industry

- 2023/01: Samsung unveils new generation of QLED TVs with enhanced 3D capabilities and wider viewing angles.

- 2023/05: LG introduces advanced autostereoscopic displays for professional medical imaging applications, improving diagnostic accuracy.

- 2024/02: Leia showcases innovative foldable 3D displays for smartphones, hinting at future mobile 3D experiences.

- 2024/08: Royal Philips partners with leading content providers to expand 3D medical visualization content library.

- 2024/11: Alioscopy demonstrates breakthrough in glasses-free 3D for large-format signage and advertising.

Future Outlook for Autostereoscopic 3D Displays Market

The future outlook for the autostereoscopic 3D displays market is exceptionally bright, driven by continuous technological advancements and expanding application horizons. The increasing demand for immersive and interactive experiences across consumer electronics, automotive, healthcare, and education sectors will fuel sustained growth. Strategic investments in R&D, coupled with a focus on improving display quality, reducing costs, and developing compelling 3D content, will be crucial for capturing market share. The convergence of autostereoscopic technology with AI and other emerging technologies will unlock unprecedented opportunities, positioning the market for robust expansion in the coming years.

Autostereoscopic 3d Displays Segmentation

-

1. Application

- 1.1. Entertainment & Gaming

- 1.2. Healthcare

- 1.3. Education & Training

- 1.4. Others

-

2. Type

- 2.1. Parallax Barrier Technology

- 2.2. Lenticular Display Technology

- 2.3. Others

Autostereoscopic 3d Displays Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Autostereoscopic 3d Displays Regional Market Share

Geographic Coverage of Autostereoscopic 3d Displays

Autostereoscopic 3d Displays REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Entertainment & Gaming

- 5.1.2. Healthcare

- 5.1.3. Education & Training

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Parallax Barrier Technology

- 5.2.2. Lenticular Display Technology

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Entertainment & Gaming

- 6.1.2. Healthcare

- 6.1.3. Education & Training

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Parallax Barrier Technology

- 6.2.2. Lenticular Display Technology

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Entertainment & Gaming

- 7.1.2. Healthcare

- 7.1.3. Education & Training

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Parallax Barrier Technology

- 7.2.2. Lenticular Display Technology

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Entertainment & Gaming

- 8.1.2. Healthcare

- 8.1.3. Education & Training

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Parallax Barrier Technology

- 8.2.2. Lenticular Display Technology

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Entertainment & Gaming

- 9.1.2. Healthcare

- 9.1.3. Education & Training

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Parallax Barrier Technology

- 9.2.2. Lenticular Display Technology

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Autostereoscopic 3d Displays Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Entertainment & Gaming

- 10.1.2. Healthcare

- 10.1.3. Education & Training

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Parallax Barrier Technology

- 10.2.2. Lenticular Display Technology

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Exceptional 3D

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Royal Philips

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Samsung

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 LG

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Alioscopy

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Dolby Laboratories

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Toshiba

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Magnetic Media Holdings

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Leia

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Leyard Opto-Electronic

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Kangde Xin Composite Material Group

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 HIKVISION

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Marvel Digital

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ledman

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Evistek

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 TCL

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 3D Global Solutions GmbH

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Exceptional 3D

List of Figures

- Figure 1: Global Autostereoscopic 3d Displays Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Autostereoscopic 3d Displays Revenue (million), by Application 2025 & 2033

- Figure 3: North America Autostereoscopic 3d Displays Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Autostereoscopic 3d Displays Revenue (million), by Type 2025 & 2033

- Figure 5: North America Autostereoscopic 3d Displays Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Autostereoscopic 3d Displays Revenue (million), by Country 2025 & 2033

- Figure 7: North America Autostereoscopic 3d Displays Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Autostereoscopic 3d Displays Revenue (million), by Application 2025 & 2033

- Figure 9: South America Autostereoscopic 3d Displays Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Autostereoscopic 3d Displays Revenue (million), by Type 2025 & 2033

- Figure 11: South America Autostereoscopic 3d Displays Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Autostereoscopic 3d Displays Revenue (million), by Country 2025 & 2033

- Figure 13: South America Autostereoscopic 3d Displays Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Autostereoscopic 3d Displays Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Autostereoscopic 3d Displays Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autostereoscopic 3d Displays Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Autostereoscopic 3d Displays Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Autostereoscopic 3d Displays Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Autostereoscopic 3d Displays Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Autostereoscopic 3d Displays Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Autostereoscopic 3d Displays Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Autostereoscopic 3d Displays Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Autostereoscopic 3d Displays Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Autostereoscopic 3d Displays Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Autostereoscopic 3d Displays Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Autostereoscopic 3d Displays Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Autostereoscopic 3d Displays Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Autostereoscopic 3d Displays Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Autostereoscopic 3d Displays Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Autostereoscopic 3d Displays Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Autostereoscopic 3d Displays Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Autostereoscopic 3d Displays Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Autostereoscopic 3d Displays Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Autostereoscopic 3d Displays Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Autostereoscopic 3d Displays Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Autostereoscopic 3d Displays Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Autostereoscopic 3d Displays Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Autostereoscopic 3d Displays Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Autostereoscopic 3d Displays Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Autostereoscopic 3d Displays Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autostereoscopic 3d Displays?

The projected CAGR is approximately 34%.

2. Which companies are prominent players in the Autostereoscopic 3d Displays?

Key companies in the market include Exceptional 3D, Royal Philips, Samsung, LG, Alioscopy, Dolby Laboratories, Toshiba, Magnetic Media Holdings, Leia, Leyard Opto-Electronic, Kangde Xin Composite Material Group, HIKVISION, Marvel Digital, Ledman, Evistek, TCL, 3D Global Solutions GmbH.

3. What are the main segments of the Autostereoscopic 3d Displays?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1509 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autostereoscopic 3d Displays," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autostereoscopic 3d Displays report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autostereoscopic 3d Displays?

To stay informed about further developments, trends, and reports in the Autostereoscopic 3d Displays, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence