Key Insights

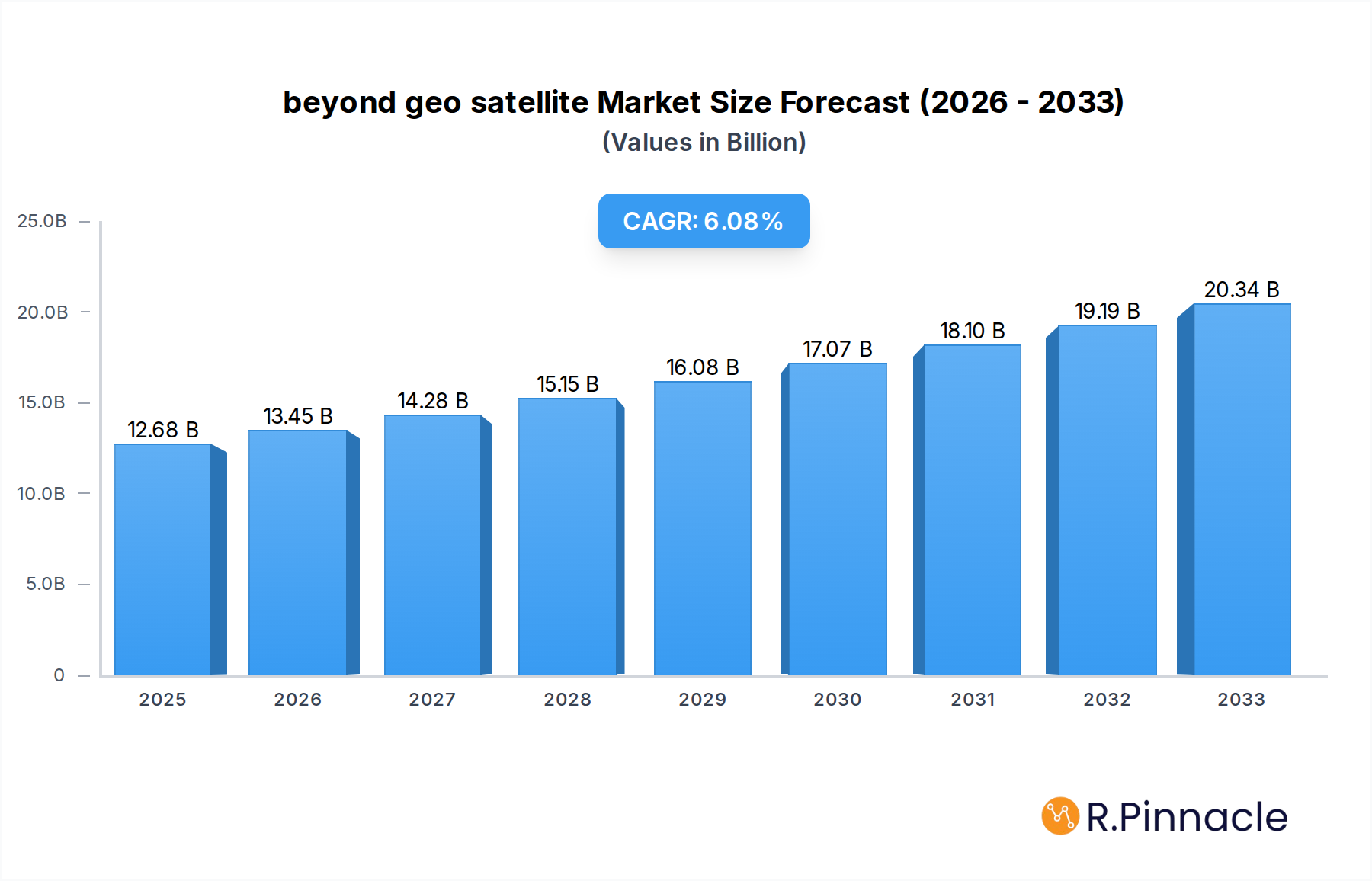

The Beyond Geo Satellite market is poised for significant expansion, projected to reach USD 12.68 billion by 2025, driven by a robust CAGR of 6.22% throughout the forecast period. This growth is underpinned by increasing demand for advanced satellite capabilities beyond traditional geostationary orbits, catering to a spectrum of applications from commercial ventures to critical military operations. The expansion of constellations for various services, including Earth observation, communication, and navigation, is a primary catalyst. Furthermore, the continuous miniaturization of satellite technology and the development of more cost-effective launch solutions are making beyond-geo deployments increasingly accessible and attractive. Emerging trends such as the rise of small satellite constellations for specialized data acquisition and the integration of AI for on-orbit processing are further fueling market momentum. The growing need for resilient and ubiquitous connectivity, particularly in remote and underserved regions, also contributes significantly to this upward trajectory.

beyond geo satellite Market Size (In Billion)

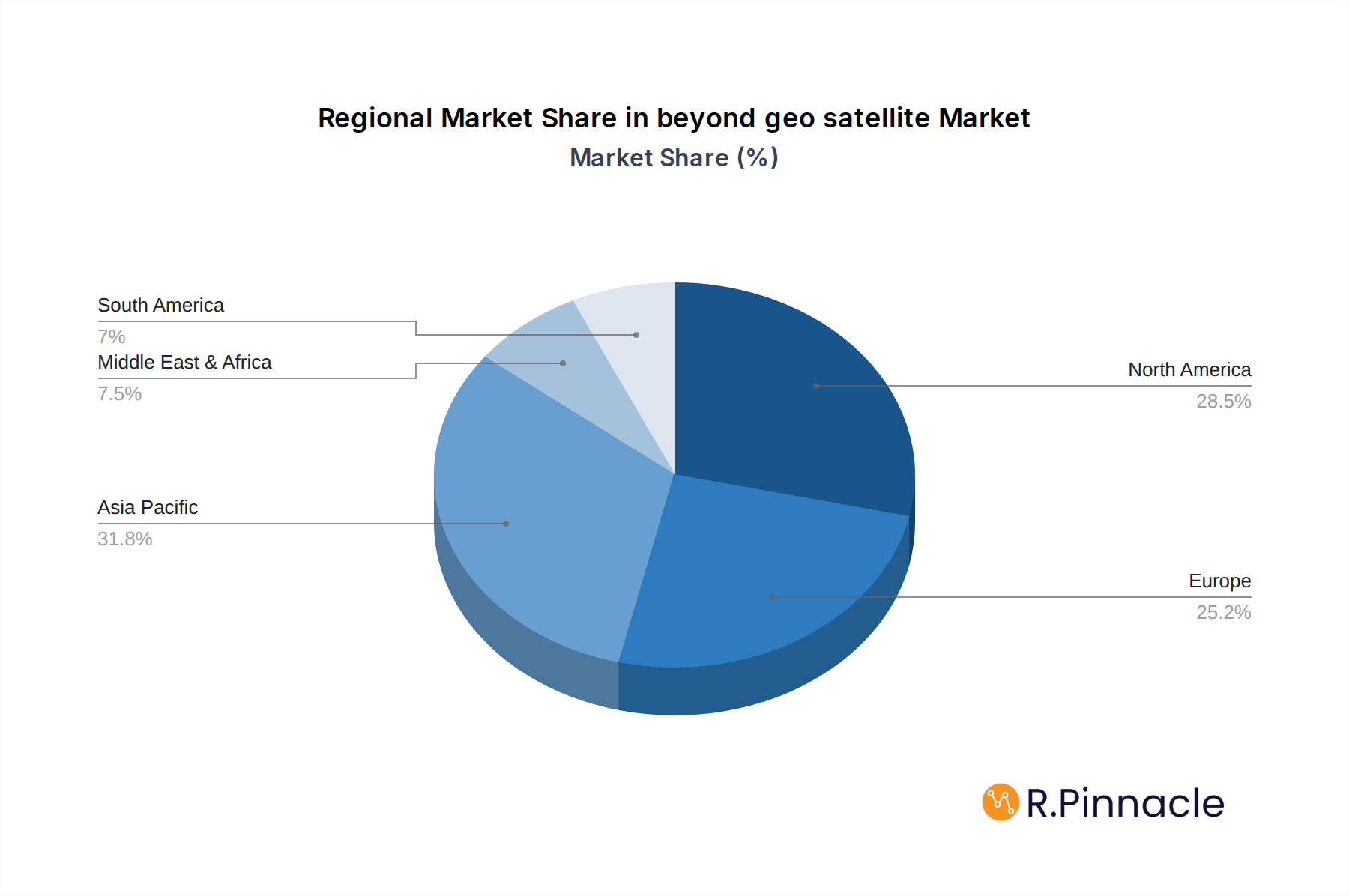

The market segmentation reveals a dynamic landscape, with the 50-500 kg category likely to dominate, reflecting the sweet spot for many commercial and scientific payloads requiring a balance of capability and cost. In terms of applications, the Commercial sector, encompassing telecommunications, remote sensing, and scientific research, is expected to lead the charge, closely followed by the Military segment's consistent demand for advanced surveillance, reconnaissance, and communication systems. Geographically, Asia Pacific, driven by substantial investments from China and India, alongside a rapidly growing space industry in countries like Japan and South Korea, is anticipated to witness the most vigorous growth. North America and Europe, with their established space ecosystems and ongoing modernization programs, will remain substantial markets, while emerging economies in other regions are increasingly exploring beyond-geo satellite solutions. Restraints, such as the high cost of development and deployment, regulatory complexities, and the increasing risk of space debris, are being actively addressed through technological innovation and international cooperation, suggesting a resilient path for market expansion.

beyond geo satellite Company Market Share

Here's an SEO-optimized, reader-centric report description for the Beyond GEO Satellite market, designed for immediate use.

Gain unparalleled insights into the burgeoning beyond GEO satellite market with this comprehensive report. Spanning the crucial study period of 2019–2033, with detailed analysis for the base year 2025 and an estimated year also 2025, this research provides a granular understanding of market dynamics, technological advancements, and strategic opportunities. The forecast period from 2025–2033 offers actionable intelligence for businesses seeking to capitalize on the rapid expansion of non-geostationary satellite constellations and their diverse applications. Covering historical data from 2019–2024, this report is your definitive guide to navigating the future of satellite technology and services.

Beyond GEO Satellite Market Structure & Innovation Trends

The beyond GEO satellite market, while exhibiting dynamic growth, presents a moderately concentrated structure. Key players like Lockheed Martin, Northrop Grumman, and Airbus Defence and Space hold significant market share, driven by substantial R&D investments and established manufacturing capabilities. Innovation trends are predominantly fueled by the demand for lower latency, higher bandwidth, and more cost-effective satellite solutions. The miniaturization of satellites, advancements in propulsion systems, and the development of sophisticated ground segment technologies are critical innovation drivers. Regulatory frameworks, evolving to accommodate the increasing number of satellite launches and debris mitigation, play a pivotal role in market shaping. Product substitutes, while present in some niche applications, are largely outpaced by the unique capabilities offered by beyond GEO constellations. End-user demographics are rapidly expanding beyond traditional defense and government sectors to include commercial internet providers, IoT solutions, and emerging media and entertainment services. Mergers and acquisitions (M&A) activity, valued in the billions, is a notable trend as larger entities seek to consolidate their positions and acquire specialized technologies. For instance, a recent M&A deal in the billions highlighted the strategic importance of integrated satellite solutions.

Beyond GEO Satellite Market Dynamics & Trends

The beyond GEO satellite market is experiencing explosive growth, propelled by a confluence of technological advancements and escalating demand across various sectors. The Compound Annual Growth Rate (CAGR) is projected to be in the double digits throughout the forecast period, indicating a robust expansion trajectory. Key market growth drivers include the insatiable appetite for ubiquitous high-speed internet access, particularly in underserved regions, and the increasing reliance on satellite communication for critical infrastructure and national security. Technological disruptions, such as the advent of mega-constellations offering unprecedented global coverage and capacity, are fundamentally reshaping the market. Furthermore, advancements in small satellite technology (including below 50 kg and 50-500 kg types) have dramatically lowered the cost of deployment, fostering new business models and applications. Consumer preferences are shifting towards seamless connectivity and on-demand services, which beyond GEO satellites are uniquely positioned to deliver. Competitive dynamics are intense, characterized by rapid innovation cycles, strategic partnerships, and a race to achieve market leadership in terms of deployed satellites and service offerings. Market penetration for satellite-based internet services, for example, is expected to surge, driven by affordability and performance improvements. The integration of AI and machine learning in satellite operations and data analysis is another significant trend, optimizing performance and unlocking new service possibilities.

Dominant Regions & Segments in Beyond GEO Satellite

The North American region currently dominates the beyond GEO satellite market, driven by substantial government investment in defense and space exploration, alongside a robust private sector ecosystem. The United States, in particular, is a powerhouse, with major players like Lockheed Martin and Northrop Grumman headquartered there. Economic policies that foster innovation, coupled with extensive existing space infrastructure, further solidify its leading position.

Application: Commercial

- Key Drivers: Growing demand for global broadband internet, expansion of IoT networks, and the rise of the new space economy. Economic incentives and favorable regulatory environments in countries like the USA and those in Europe are also significant.

- Dominance Analysis: The commercial segment is the largest and fastest-growing, fueled by companies seeking to provide satellite internet to consumers and businesses. The development of large constellations by private entities has dramatically increased the number of commercial beyond GEO satellites.

Application: Military

- Key Drivers: National security imperatives, demand for secure and resilient communication, advanced reconnaissance, and intelligence gathering capabilities. Geopolitical tensions and modernization of defense forces contribute to sustained growth.

- Dominance Analysis: Historically a primary driver, the military segment continues to be a significant market. Investments in advanced tactical communication, surveillance, and early warning systems by governments ensure a consistent demand for beyond GEO capabilities.

Application: Others

- Key Drivers: Scientific research, Earth observation for environmental monitoring and climate studies, disaster management, and media broadcasting.

- Dominance Analysis: While smaller than commercial and military applications, this segment is crucial for scientific advancement and global monitoring. The proliferation of small satellites has made space-based research more accessible.

Types: Below 50 kg

- Key Drivers: Reduced launch costs, increased accessibility for research institutions and startups, and the ability to deploy large constellations rapidly.

- Dominance Analysis: This segment, often referred to as 'smallsats' or 'cubesats,' is experiencing exponential growth. Its dominance is attributed to its versatility and cost-effectiveness for various applications, from Earth observation to technology demonstrations.

Types: 50-500 kg

- Key Drivers: Balance of capability and cost, enabling more sophisticated payloads and longer mission durations compared to smaller satellites.

- Dominance Analysis: This mid-sized segment offers a compromise, providing enhanced capabilities for a range of commercial and defense applications, including advanced communication and imaging.

Types: Above 500 kg

- Key Drivers: High-performance requirements for specialized missions, including advanced scientific research, dedicated national security payloads, and large telecommunications satellites.

- Dominance Analysis: While fewer in number, these larger satellites offer significant capabilities and command substantial market value, serving critical applications that demand robust performance and longevity.

Beyond GEO Satellite Product Innovations

Product innovations in the beyond GEO satellite market are transforming connectivity and data services. Key developments include the deployment of mega-constellations for global broadband internet, offering significantly lower latency and higher throughput than traditional geostationary satellites. The miniaturization of satellite technology has led to the proliferation of small satellites (below 50 kg and 50-500 kg), enabling more frequent launches and dedicated missions for Earth observation, IoT, and scientific research. Advanced propulsion systems are enhancing maneuverability and orbit control, while sophisticated antenna designs are improving signal strength and capacity. Competitive advantages are being gained through integrated solutions encompassing satellite manufacturing, launch services, and ground segment operations, providing end-to-end capabilities.

Report Scope & Segmentation Analysis

This report segments the beyond GEO satellite market across key application and satellite type categories.

- Application: Commercial: This segment encompasses satellite services for broadband internet, IoT, navigation, and entertainment. Growth projections are robust, driven by expanding global connectivity needs. Market sizes are expected to reach billions by the forecast period end.

- Application: Military: This segment covers defense applications such as secure communications, intelligence, surveillance, and reconnaissance (ISR). Sustained government investment ensures consistent market demand and competitive dynamics remain focused on advanced technological capabilities.

- Application: Others: This segment includes scientific research, Earth observation, environmental monitoring, and disaster management. Growth is steady, with an increasing number of academic and research institutions utilizing satellite technology.

- Types: Below 50 kg: This segment focuses on small satellites and cubesats, offering cost-effective solutions for specialized missions. Growth is exponential due to declining launch costs and increased accessibility.

- Types: 50-500 kg: This segment represents mid-sized satellites, balancing capability with cost for a broad range of applications including advanced imaging and communication. Market sizes are substantial, with strong growth anticipated.

- Types: Above 500 kg: This segment comprises larger satellites designed for high-performance, dedicated missions requiring significant power and payload capacity. While representing fewer units, their market value is significant.

Key Drivers of Beyond GEO Satellite Growth

The growth of the beyond GEO satellite market is propelled by several critical factors. Technologically, the relentless pursuit of lower latency and higher bandwidth for global internet access, coupled with advancements in small satellite miniaturization and launch technologies, is a primary driver. Economically, the increasing demand for satellite-enabled services in emerging markets and the significant investments by venture capital and established aerospace companies are fueling expansion. Regulatory frameworks are also evolving to accommodate the rapid growth of satellite constellations, streamlining licensing processes and promoting innovation. The push for space-based connectivity for the Internet of Things (IoT) and autonomous systems represents another significant growth accelerator.

Challenges in the Beyond GEO Satellite Sector

Despite its rapid growth, the beyond GEO satellite sector faces considerable challenges. Regulatory hurdles, including spectrum allocation and orbital debris mitigation, can slow down deployment and increase operational costs, potentially impacting market penetration. Supply chain issues, particularly concerning specialized components and skilled labor, can lead to production delays and cost overruns. Intense competitive pressures among numerous players vying for market share can also create pricing pressures and necessitate continuous innovation, demanding substantial capital investment. The significant upfront investment required for developing and launching large constellations, often in the billions, poses a considerable financial barrier for new entrants.

Emerging Opportunities in Beyond GEO Satellite

The beyond GEO satellite market is ripe with emerging opportunities. The increasing demand for global, low-latency internet access in underserved areas presents a vast market potential, especially in developing economies. The proliferation of the Internet of Things (IoT), requiring ubiquitous connectivity for sensors and devices, opens up new service avenues for satellite operators. Advancements in satellite servicing and in-orbit manufacturing promise to extend satellite lifespans and enable more complex space-based operations. Furthermore, the growing need for resilient communication infrastructure in the face of natural disasters and geopolitical instability offers significant opportunities for beyond GEO solutions. The development of integrated space-based platforms offering data analytics and AI-driven insights is another promising frontier.

Leading Players in the Beyond GEO Satellite Market

- Airbus Defence and Space

- OHB SE

- Boeing Defense, Space & Security

- JSC Information Satellite Systems

- Lockheed Martin

- Northrop Grumman

- Space Systems/Loral

- Thales Alenia Space

Key Developments in Beyond GEO Satellite Industry

- 2023/06: Launch of a new mega-constellation by a leading provider, significantly expanding global broadband capacity.

- 2023/09: A major defense contractor secures a multi-billion dollar contract for advanced satellite communication systems for military use.

- 2024/01: A prominent satellite manufacturer announces a breakthrough in miniaturized propulsion technology for small satellites.

- 2024/03: Regulatory body approves new guidelines for orbital debris management, impacting future launch strategies.

- 2024/05: A significant M&A deal, valued in the billions, consolidates players in the Earth observation segment.

- 2024/08: Rollout of enhanced AI-powered ground segment solutions for improved satellite data analysis.

- 2025/XX: Expected major satellite deployment by a new market entrant, aiming to capture a significant share of the commercial broadband market.

Future Outlook for Beyond GEO Satellite Market

The future outlook for the beyond GEO satellite market is exceptionally bright, characterized by sustained high growth and transformative innovation. The increasing integration of satellite technology with terrestrial networks will create a truly seamless global connectivity ecosystem. The expansion of satellite-enabled IoT applications, coupled with advancements in Earth observation and AI-driven data analytics, will unlock unprecedented insights and operational efficiencies across industries. Strategic opportunities lie in addressing the growing demand for sovereign space capabilities, developing advanced in-orbit servicing technologies, and capitalizing on the growing space economy. Continued investments in research and development, alongside supportive regulatory environments, will be crucial for maintaining this upward trajectory and realizing the full potential of beyond GEO satellite solutions.

beyond geo satellite Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Military

- 1.3. Others

-

2. Types

- 2.1. Below 50 kg

- 2.2. 50-500 kg

- 2.3. Above 500 kg

beyond geo satellite Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

beyond geo satellite Regional Market Share

Geographic Coverage of beyond geo satellite

beyond geo satellite REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Military

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Below 50 kg

- 5.2.2. 50-500 kg

- 5.2.3. Above 500 kg

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Military

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Below 50 kg

- 6.2.2. 50-500 kg

- 6.2.3. Above 500 kg

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Military

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Below 50 kg

- 7.2.2. 50-500 kg

- 7.2.3. Above 500 kg

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Military

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Below 50 kg

- 8.2.2. 50-500 kg

- 8.2.3. Above 500 kg

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Military

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Below 50 kg

- 9.2.2. 50-500 kg

- 9.2.3. Above 500 kg

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific beyond geo satellite Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Military

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Below 50 kg

- 10.2.2. 50-500 kg

- 10.2.3. Above 500 kg

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Airbus Defence and Space

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 OHB SE

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Boeing Defense

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Space & Security

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 JSC Information Satellite Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Lockheed Martin

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Northrop Grumman

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Space Systems/Loral

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Thales Alenia Space

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Airbus Defence and Space

List of Figures

- Figure 1: Global beyond geo satellite Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global beyond geo satellite Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America beyond geo satellite Revenue (billion), by Application 2025 & 2033

- Figure 4: North America beyond geo satellite Volume (K), by Application 2025 & 2033

- Figure 5: North America beyond geo satellite Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America beyond geo satellite Volume Share (%), by Application 2025 & 2033

- Figure 7: North America beyond geo satellite Revenue (billion), by Types 2025 & 2033

- Figure 8: North America beyond geo satellite Volume (K), by Types 2025 & 2033

- Figure 9: North America beyond geo satellite Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America beyond geo satellite Volume Share (%), by Types 2025 & 2033

- Figure 11: North America beyond geo satellite Revenue (billion), by Country 2025 & 2033

- Figure 12: North America beyond geo satellite Volume (K), by Country 2025 & 2033

- Figure 13: North America beyond geo satellite Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America beyond geo satellite Volume Share (%), by Country 2025 & 2033

- Figure 15: South America beyond geo satellite Revenue (billion), by Application 2025 & 2033

- Figure 16: South America beyond geo satellite Volume (K), by Application 2025 & 2033

- Figure 17: South America beyond geo satellite Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America beyond geo satellite Volume Share (%), by Application 2025 & 2033

- Figure 19: South America beyond geo satellite Revenue (billion), by Types 2025 & 2033

- Figure 20: South America beyond geo satellite Volume (K), by Types 2025 & 2033

- Figure 21: South America beyond geo satellite Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America beyond geo satellite Volume Share (%), by Types 2025 & 2033

- Figure 23: South America beyond geo satellite Revenue (billion), by Country 2025 & 2033

- Figure 24: South America beyond geo satellite Volume (K), by Country 2025 & 2033

- Figure 25: South America beyond geo satellite Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America beyond geo satellite Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe beyond geo satellite Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe beyond geo satellite Volume (K), by Application 2025 & 2033

- Figure 29: Europe beyond geo satellite Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe beyond geo satellite Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe beyond geo satellite Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe beyond geo satellite Volume (K), by Types 2025 & 2033

- Figure 33: Europe beyond geo satellite Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe beyond geo satellite Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe beyond geo satellite Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe beyond geo satellite Volume (K), by Country 2025 & 2033

- Figure 37: Europe beyond geo satellite Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe beyond geo satellite Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa beyond geo satellite Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa beyond geo satellite Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa beyond geo satellite Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa beyond geo satellite Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa beyond geo satellite Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa beyond geo satellite Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa beyond geo satellite Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa beyond geo satellite Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa beyond geo satellite Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa beyond geo satellite Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa beyond geo satellite Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa beyond geo satellite Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific beyond geo satellite Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific beyond geo satellite Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific beyond geo satellite Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific beyond geo satellite Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific beyond geo satellite Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific beyond geo satellite Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific beyond geo satellite Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific beyond geo satellite Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific beyond geo satellite Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific beyond geo satellite Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific beyond geo satellite Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific beyond geo satellite Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 3: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 5: Global beyond geo satellite Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global beyond geo satellite Volume K Forecast, by Region 2020 & 2033

- Table 7: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 9: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 11: Global beyond geo satellite Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global beyond geo satellite Volume K Forecast, by Country 2020 & 2033

- Table 13: United States beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 21: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 23: Global beyond geo satellite Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global beyond geo satellite Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 33: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 35: Global beyond geo satellite Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global beyond geo satellite Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 57: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 59: Global beyond geo satellite Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global beyond geo satellite Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global beyond geo satellite Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global beyond geo satellite Volume K Forecast, by Application 2020 & 2033

- Table 75: Global beyond geo satellite Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global beyond geo satellite Volume K Forecast, by Types 2020 & 2033

- Table 77: Global beyond geo satellite Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global beyond geo satellite Volume K Forecast, by Country 2020 & 2033

- Table 79: China beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific beyond geo satellite Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific beyond geo satellite Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the beyond geo satellite?

The projected CAGR is approximately 6.22%.

2. Which companies are prominent players in the beyond geo satellite?

Key companies in the market include Airbus Defence and Space, OHB SE, Boeing Defense, Space & Security, JSC Information Satellite Systems, Lockheed Martin, Northrop Grumman, Space Systems/Loral, Thales Alenia Space.

3. What are the main segments of the beyond geo satellite?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.68 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "beyond geo satellite," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the beyond geo satellite report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the beyond geo satellite?

To stay informed about further developments, trends, and reports in the beyond geo satellite, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence