Key Insights

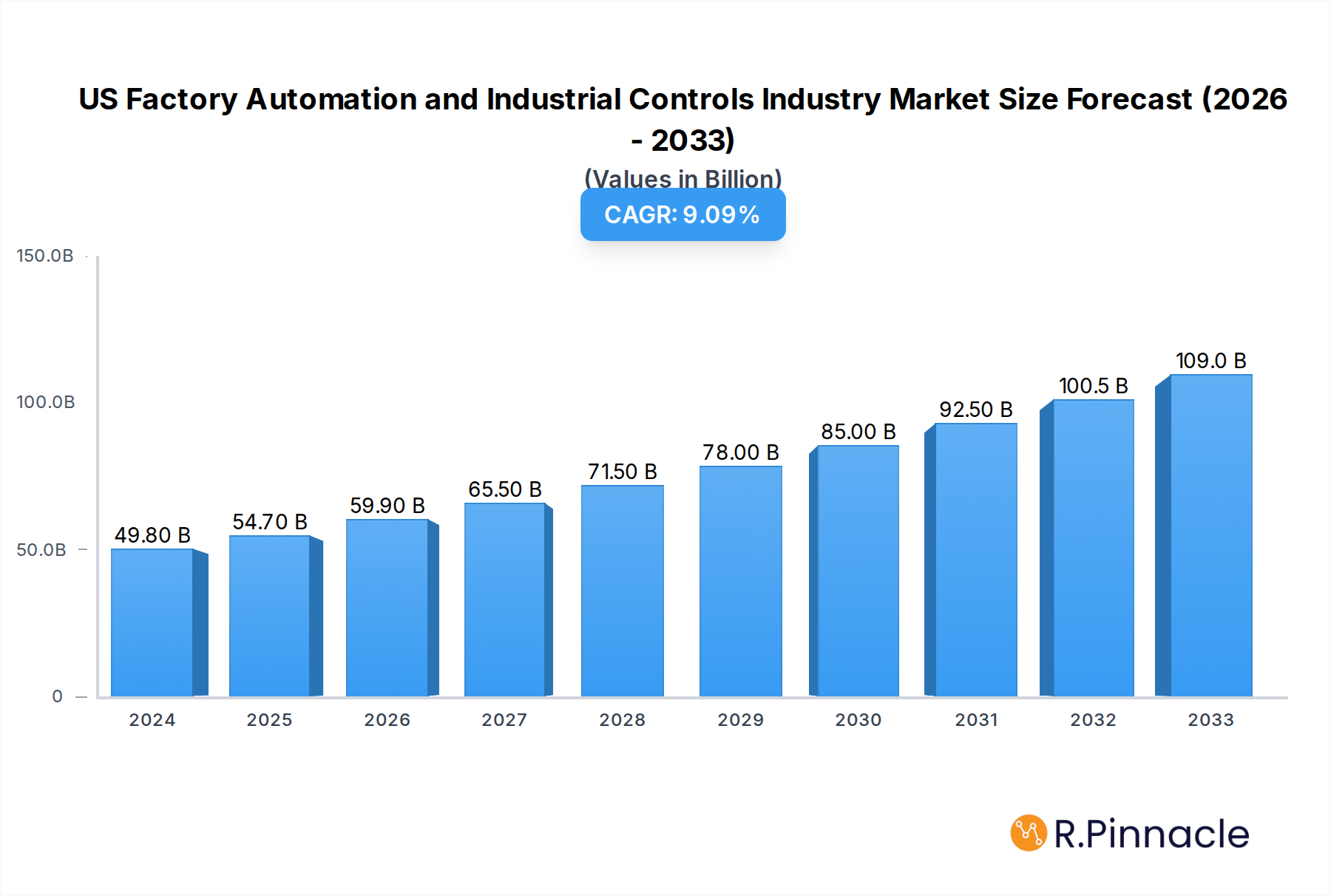

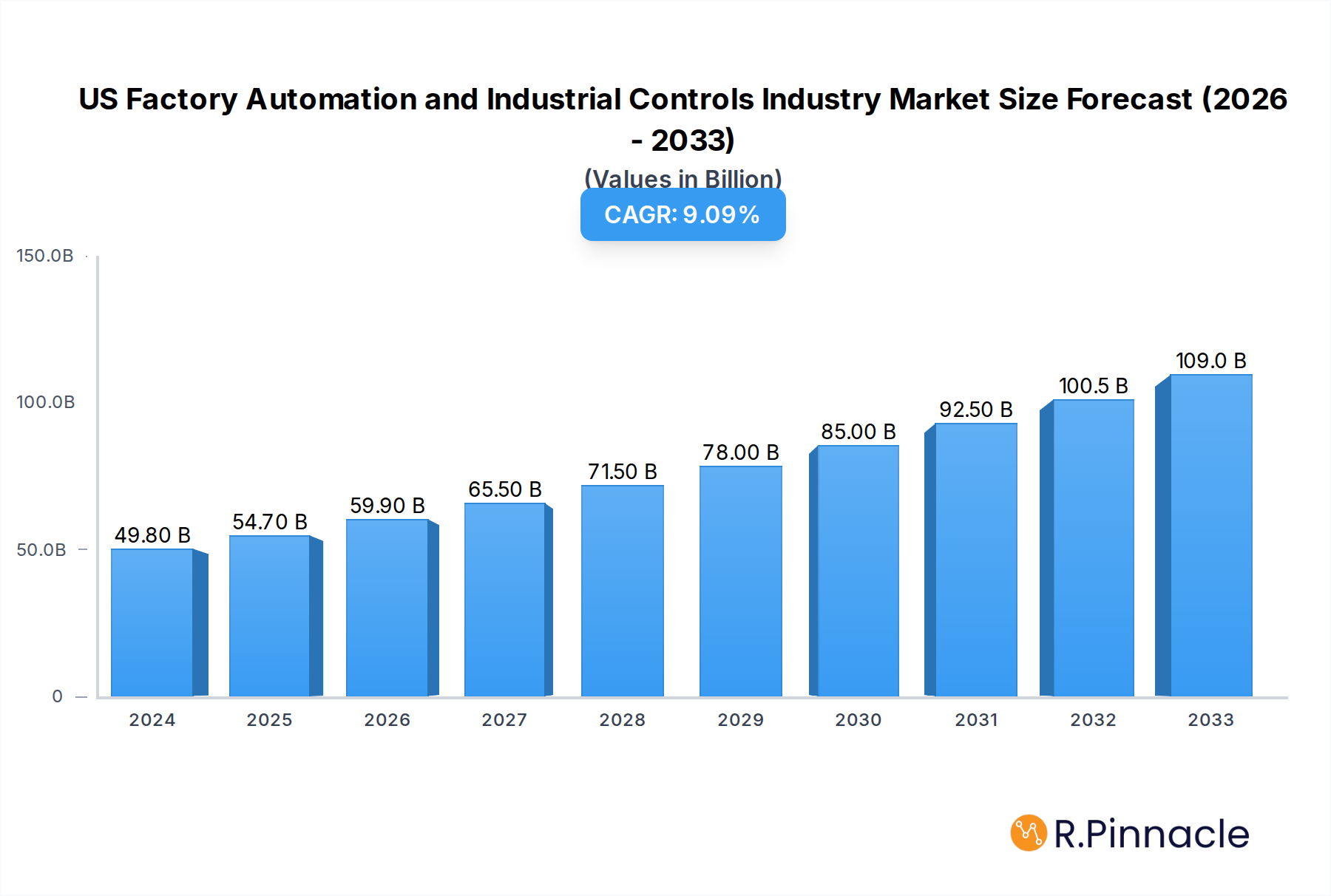

The US factory automation and industrial controls market is experiencing robust expansion, driven by the critical need for enhanced operational efficiency, improved product quality, and stringent safety regulations across various manufacturing sectors. In 2024, the market size stands at an estimated $49.8 billion, projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% through 2033. This upward trajectory is fueled by the increasing adoption of Industry 4.0 technologies, including the Internet of Things (IoT), artificial intelligence (AI), and advanced robotics, which are transforming traditional manufacturing paradigms. The push for greater automation is particularly evident in sectors like automotive and transportation, food and beverage, and pharmaceuticals, where precision, speed, and traceability are paramount. Furthermore, the growing emphasis on energy efficiency and sustainability in industrial operations is also a significant catalyst, as automated systems can optimize resource consumption and reduce waste. The integration of sophisticated software solutions such as Manufacturing Execution Systems (MES) and Product Lifecycle Management (PLM) is further bolstering market growth by enabling better process control and data-driven decision-making.

US Factory Automation and Industrial Controls Industry Market Size (In Billion)

Key market drivers include the relentless pursuit of increased productivity and reduced labor costs, coupled with the demand for more flexible and adaptable manufacturing processes capable of handling diverse product lines and customization. Emerging trends such as the rise of collaborative robots (cobots), the expansion of edge computing for real-time data analysis, and the increasing sophistication of industrial sensors are shaping the future of factory automation. While the market benefits from these powerful growth engines, potential restraints like the high initial investment costs for advanced automation solutions and the shortage of skilled personnel to manage and maintain these complex systems could pose challenges. However, the long-term outlook remains overwhelmingly positive, supported by ongoing technological advancements and a strong competitive landscape featuring major players like Siemens AG, Rockwell Automation, and Honeywell International Inc., all actively innovating and expanding their offerings to meet evolving industry demands.

US Factory Automation and Industrial Controls Industry Company Market Share

US Factory Automation and Industrial Controls Industry Report: Market Analysis and Future Projections (2019–2033)

This comprehensive report delves into the dynamic US Factory Automation and Industrial Controls Industry, offering in-depth analysis of market structures, trends, and future outlook. Spanning from 2019–2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report provides actionable insights for industry stakeholders. The historical period covers 2019–2024. The market is projected to reach $XXX billion by 2033, with a Compound Annual Growth Rate (CAGR) of XX.XX%.

US Factory Automation and Industrial Controls Industry Market Structure & Innovation Trends

The US Factory Automation and Industrial Controls Industry exhibits a moderately concentrated market structure, with key players like Honeywell International Inc, ABB Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, Omron Corporation, Rockwell Automation Inc, Yokogawa Electric Corporation, Fanuc Corporation, and Emerson Electric Company dominating significant market shares. Innovation is a critical driver, fueled by advancements in Artificial Intelligence (AI), the Internet of Things (IoT), and cloud computing, enabling smarter, more connected manufacturing environments. Regulatory frameworks, such as those concerning cybersecurity and environmental compliance, are increasingly shaping industry practices. Product substitutes are emerging with the rise of software-defined automation solutions, though traditional hardware remains robust. End-user demographics are shifting towards a greater demand for customized, flexible, and data-driven manufacturing processes across various sectors. Mergers and acquisitions (M&A) activity remains robust, with recent deals valued at over $XX billion aimed at consolidating market positions and acquiring technological capabilities. For example, Rockwell Automation's acquisition of Plex Systems for $XXX million exemplifies strategic moves to enhance cloud-delivered intelligent manufacturing solutions.

- Market Concentration: Moderately concentrated with leading global players.

- Innovation Drivers: AI, IoT, Cloud Computing, Edge Computing.

- Regulatory Frameworks: Cybersecurity standards (e.g., ISA/IEC 62443), environmental regulations, data privacy laws.

- Product Substitutes: Software-defined automation, advanced analytics platforms.

- End-User Demographics: Demand for customization, flexibility, predictive maintenance, and operational efficiency.

- M&A Activities: Strategic acquisitions to gain market share, technology, and expand service offerings. Notable deals include Rockwell Automation's acquisition of Plex Systems for $XXX million.

US Factory Automation and Industrial Controls Industry Market Dynamics & Trends

The US Factory Automation and Industrial Controls Industry is experiencing robust growth, propelled by a confluence of factors. A primary growth driver is the relentless pursuit of operational efficiency and cost reduction by manufacturers across all sectors. The adoption of Industry 4.0 principles and the digital transformation imperative are significantly accelerating market penetration. Technological disruptions, particularly in areas like AI-powered predictive maintenance, advanced robotics, and the Industrial Internet of Things (IIoT), are revolutionizing manufacturing processes. These technologies enable real-time data analysis, optimized production scheduling, and enhanced quality control, leading to substantial improvements in productivity and reduced downtime. Consumer preferences are increasingly dictating a need for faster production cycles, greater product customization, and higher quality standards, all of which are directly addressed by advanced automation solutions.

The competitive landscape is characterized by intense innovation and strategic partnerships. Companies are heavily investing in research and development to offer integrated solutions that encompass everything from design and engineering to production and after-sales service. The rise of smart factories, where interconnected machines and systems communicate seamlessly, is a defining trend. This shift is driven by the need for greater agility to respond to market fluctuations and evolving consumer demands. Furthermore, the increasing focus on sustainability and energy efficiency is pushing the adoption of automation solutions that can optimize resource utilization and reduce environmental impact. The cybersecurity of industrial control systems is also a growing concern, leading to increased investment in secure automation technologies and protocols. The market penetration of advanced automation solutions is expected to continue its upward trajectory, with an estimated market penetration rate of XX% by 2033. The projected market size is estimated to reach $XXX billion by 2033, growing at a CAGR of XX.XX%.

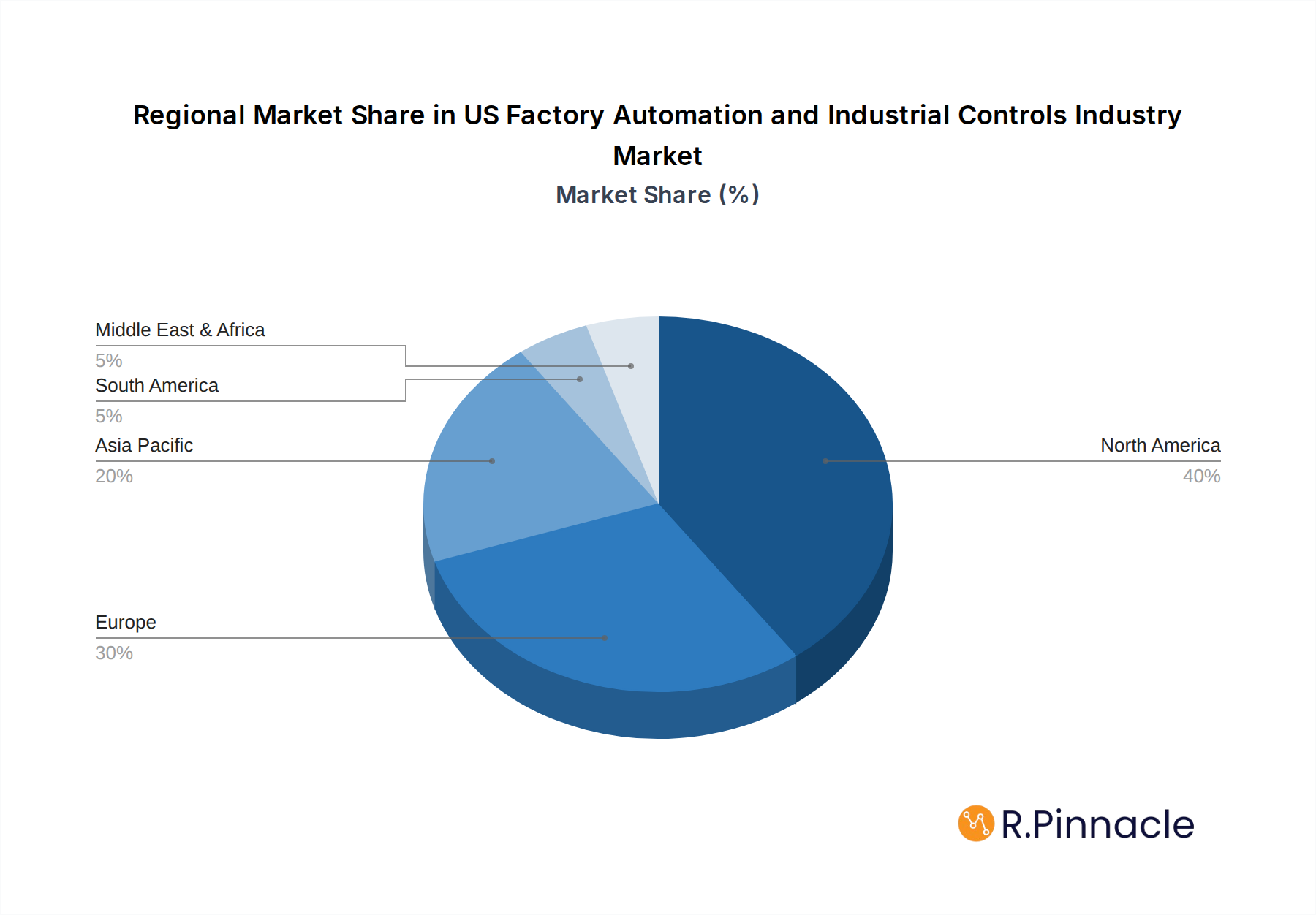

Dominant Regions & Segments in US Factory Automation and Industrial Controls Industry

The US Factory Automation and Industrial Controls Industry is characterized by its dominance across several key segments and its widespread adoption across various end-user industries. The Industrial Control Systems segment, particularly Programmable Logic Controllers (PLCs) and Supervisory Control and Data Acquisition (SCADA) systems, forms the backbone of modern manufacturing automation, experiencing significant demand due to their versatility and reliability in managing complex industrial processes. Manufacturing Execution Systems (MES) and Human Machine Interfaces (HMIs) are also critical, facilitating seamless integration between plant floor operations and enterprise-level management.

Within Field Devices, Industrial Robotics and Machine Vision are leading the charge, driven by the automotive and aerospace sectors' need for precision, speed, and enhanced safety in production lines. The adoption of advanced sensors and transmitters, alongside sophisticated Safety Systems, is crucial for maintaining operational integrity and compliance.

The Oil and Gas and Power and Utilities sectors continue to be significant end-users, requiring robust and reliable automation solutions for critical infrastructure management and resource extraction. However, the Automotive and Transportation industry is emerging as a major growth driver, heavily investing in advanced robotics and intelligent systems to enhance production efficiency and introduce electric vehicle manufacturing capabilities. The Pharmaceutical industry is also witnessing rapid automation adoption for stringent quality control and compliance requirements.

- Key Drivers for Dominance:

- Economic Policies: Government initiatives promoting manufacturing reshoring and technological advancement.

- Infrastructure Development: Significant investments in upgrading industrial infrastructure to support Industry 4.0 adoption.

- Skilled Workforce Availability: Growing availability of skilled labor in automation engineering and maintenance.

- Technological Innovation: Continuous advancements in AI, IoT, and robotics driving demand for advanced solutions.

The North American region, specifically the United States, holds a dominant position in this market due to its advanced industrial base, high R&D spending, and strong adoption of cutting-edge technologies. The market size for the US is projected to reach $XXX billion by 2033.

US Factory Automation and Industrial Controls Industry Product Innovations

Product innovations in the US Factory Automation and Industrial Controls Industry are increasingly focused on delivering integrated, intelligent, and adaptable solutions. Key advancements include the development of AI-powered predictive maintenance platforms that reduce downtime and optimize equipment lifespan, and sophisticated robotics capable of collaborative tasks with human workers. The integration of IIoT capabilities into field devices and control systems allows for real-time data collection and analysis, enabling smarter decision-making and enhanced operational efficiency. Edge computing is also gaining traction, enabling faster processing of critical data closer to the source, thereby improving response times and system reliability. These innovations offer significant competitive advantages by enhancing productivity, improving product quality, and enabling greater manufacturing flexibility to meet evolving market demands.

Report Scope & Segmentation Analysis

This report provides a granular analysis of the US Factory Automation and Industrial Controls Industry segmented across various critical dimensions. The Industrial Control Systems segment encompasses Distributed Control Systems (DCS), Programmable Logic Controllers (PLCs), Supervisory Control and Data Acquisition (SCADA), Product Lifecycle Management (PLM), Manufacturing Execution Systems (MES), and Human Machine Interfaces (HMIs). The Field Devices segment includes Machine Vision, Industrial Robotics, Motors and Drives, Safety Systems, and Sensors & Transmitters. Furthermore, the report meticulously examines the market across key End-user Industries: Oil and Gas, Chemical and Petrochemical, Power and Utilities, Food and Beverage, Automotive and Transportation, and Pharmaceutical.

The Industrial Control Systems segment is projected to reach $XXX billion by 2033. Field Devices are estimated to reach $XXX billion by 2033. The Automotive and Transportation end-user industry is expected to show the highest CAGR of XX.XX%, reaching $XXX billion by 2033. The Oil and Gas sector, a mature market, is expected to grow at XX.XX%, reaching $XXX billion.

Key Drivers of US Factory Automation and Industrial Controls Industry Growth

The growth of the US Factory Automation and Industrial Controls Industry is propelled by several key factors. The ongoing digital transformation and the adoption of Industry 4.0 principles are driving demand for smart manufacturing solutions. A persistent need for enhanced operational efficiency, reduced production costs, and improved product quality across manufacturing sectors is a major catalyst. Technological advancements, including AI, IoT, and robotics, are enabling more sophisticated and automated processes. Furthermore, government initiatives promoting manufacturing competitiveness and reshoring are providing a supportive ecosystem for industry expansion.

Challenges in the US Factory Automation and Industrial Controls Industry Sector

Despite robust growth, the US Factory Automation and Industrial Controls Industry faces several challenges. The increasing complexity of integrated automation systems necessitates a skilled workforce, and shortages in automation engineers and technicians can hinder implementation. Cybersecurity threats to connected industrial systems pose a significant risk, requiring continuous investment in robust security measures. Supply chain disruptions, exacerbated by geopolitical factors and global demand fluctuations, can impact the availability and cost of critical components. Moreover, the initial capital investment for advanced automation solutions can be a barrier for small and medium-sized enterprises (SMEs).

Emerging Opportunities in US Factory Automation and Industrial Controls Industry

Emerging opportunities in the US Factory Automation and Industrial Controls Industry are vast. The growing demand for sustainable and energy-efficient manufacturing processes presents a significant avenue for growth. The expansion of the electric vehicle (EV) market is driving substantial investment in automation for battery manufacturing and vehicle assembly. The increasing adoption of AI and machine learning for predictive maintenance and process optimization offers opportunities for data-driven service models. Furthermore, the integration of augmented reality (AR) and virtual reality (VR) in training and maintenance is creating new application areas and enhancing user experience.

Leading Players in the US Factory Automation and Industrial Controls Industry Market

- Honeywell International Inc

- ABB Ltd

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- Rockwell Automation Inc

- Yokogawa Electric Corporation

- Fanuc Corporation

- Emerson Electric Company

Key Developments in US Factory Automation and Industrial Controls Industry Industry

- April 2022: Critical Manufacturing unveiled the latest version of its Manufacturing Execution System (MES) at Hannover Messe 2022. Advancements in Critical Manufacturing MES (V9) help high-tech manufacturers prevail amidst changing market conditions.

- September 2021: Rockwell Automation, Inc., the digital transformation and industrial automation company completed the Plex Systems acquisition for $XXX million. This acquisition could allow Rockwell to strengthen their cloud-delivered intelligent manufacturing solutions and provide smart manufacturing in customer operations.

Future Outlook for US Factory Automation and Industrial Controls Industry Market

The future outlook for the US Factory Automation and Industrial Controls Industry is exceptionally promising, driven by continued technological innovation and an increasing imperative for manufacturers to remain competitive. The pervasive adoption of AI, IIoT, and robotics will lead to hyper-connected and self-optimizing factories. Strategic opportunities lie in developing integrated solutions that address the entire product lifecycle, from design to end-of-life management. The demand for flexible, scalable, and secure automation systems will remain paramount, especially as industries navigate evolving consumer preferences and global economic shifts. Investments in cybersecurity and sustainable automation practices will be crucial for long-term success, positioning the industry for sustained growth and value creation.

US Factory Automation and Industrial Controls Industry Segmentation

-

1. Type

-

1.1. Industrial Control Systems

- 1.1.1. Distributed Control System (DCS)

- 1.1.2. Programable Logic Controller (PLC)

- 1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 1.1.4. Product Lifecycle Management (PLM)

- 1.1.5. Manufacturing Execution System (MES)

- 1.1.6. Human Machine Interface (HMI)

- 1.1.7. Other Industrial Control Systems

-

1.2. Field Devices

- 1.2.1. Machine Vision

- 1.2.2. Industrial Robotics

- 1.2.3. Motors and Drives

- 1.2.4. Safety Systems

- 1.2.5. Sensors & Transmitters

- 1.2.6. Other Field Devices

-

1.1. Industrial Control Systems

-

2. End-user Industry

- 2.1. Oil and Gas

- 2.2. Chemical and Petrochemical

- 2.3. Power and Utilities

- 2.4. Food and Beverage

- 2.5. Automotive and Transportation

- 2.6. Pharmaceutical

- 2.7. Other End-user Industries

US Factory Automation and Industrial Controls Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Factory Automation and Industrial Controls Industry Regional Market Share

Geographic Coverage of US Factory Automation and Industrial Controls Industry

US Factory Automation and Industrial Controls Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Industrial Control Systems

- 5.1.1.1. Distributed Control System (DCS)

- 5.1.1.2. Programable Logic Controller (PLC)

- 5.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 5.1.1.4. Product Lifecycle Management (PLM)

- 5.1.1.5. Manufacturing Execution System (MES)

- 5.1.1.6. Human Machine Interface (HMI)

- 5.1.1.7. Other Industrial Control Systems

- 5.1.2. Field Devices

- 5.1.2.1. Machine Vision

- 5.1.2.2. Industrial Robotics

- 5.1.2.3. Motors and Drives

- 5.1.2.4. Safety Systems

- 5.1.2.5. Sensors & Transmitters

- 5.1.2.6. Other Field Devices

- 5.1.1. Industrial Control Systems

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Oil and Gas

- 5.2.2. Chemical and Petrochemical

- 5.2.3. Power and Utilities

- 5.2.4. Food and Beverage

- 5.2.5. Automotive and Transportation

- 5.2.6. Pharmaceutical

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Industrial Control Systems

- 6.1.1.1. Distributed Control System (DCS)

- 6.1.1.2. Programable Logic Controller (PLC)

- 6.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.4. Product Lifecycle Management (PLM)

- 6.1.1.5. Manufacturing Execution System (MES)

- 6.1.1.6. Human Machine Interface (HMI)

- 6.1.1.7. Other Industrial Control Systems

- 6.1.2. Field Devices

- 6.1.2.1. Machine Vision

- 6.1.2.2. Industrial Robotics

- 6.1.2.3. Motors and Drives

- 6.1.2.4. Safety Systems

- 6.1.2.5. Sensors & Transmitters

- 6.1.2.6. Other Field Devices

- 6.1.1. Industrial Control Systems

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Oil and Gas

- 6.2.2. Chemical and Petrochemical

- 6.2.3. Power and Utilities

- 6.2.4. Food and Beverage

- 6.2.5. Automotive and Transportation

- 6.2.6. Pharmaceutical

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Industrial Control Systems

- 7.1.1.1. Distributed Control System (DCS)

- 7.1.1.2. Programable Logic Controller (PLC)

- 7.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 7.1.1.4. Product Lifecycle Management (PLM)

- 7.1.1.5. Manufacturing Execution System (MES)

- 7.1.1.6. Human Machine Interface (HMI)

- 7.1.1.7. Other Industrial Control Systems

- 7.1.2. Field Devices

- 7.1.2.1. Machine Vision

- 7.1.2.2. Industrial Robotics

- 7.1.2.3. Motors and Drives

- 7.1.2.4. Safety Systems

- 7.1.2.5. Sensors & Transmitters

- 7.1.2.6. Other Field Devices

- 7.1.1. Industrial Control Systems

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Oil and Gas

- 7.2.2. Chemical and Petrochemical

- 7.2.3. Power and Utilities

- 7.2.4. Food and Beverage

- 7.2.5. Automotive and Transportation

- 7.2.6. Pharmaceutical

- 7.2.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Industrial Control Systems

- 8.1.1.1. Distributed Control System (DCS)

- 8.1.1.2. Programable Logic Controller (PLC)

- 8.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 8.1.1.4. Product Lifecycle Management (PLM)

- 8.1.1.5. Manufacturing Execution System (MES)

- 8.1.1.6. Human Machine Interface (HMI)

- 8.1.1.7. Other Industrial Control Systems

- 8.1.2. Field Devices

- 8.1.2.1. Machine Vision

- 8.1.2.2. Industrial Robotics

- 8.1.2.3. Motors and Drives

- 8.1.2.4. Safety Systems

- 8.1.2.5. Sensors & Transmitters

- 8.1.2.6. Other Field Devices

- 8.1.1. Industrial Control Systems

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Oil and Gas

- 8.2.2. Chemical and Petrochemical

- 8.2.3. Power and Utilities

- 8.2.4. Food and Beverage

- 8.2.5. Automotive and Transportation

- 8.2.6. Pharmaceutical

- 8.2.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Industrial Control Systems

- 9.1.1.1. Distributed Control System (DCS)

- 9.1.1.2. Programable Logic Controller (PLC)

- 9.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 9.1.1.4. Product Lifecycle Management (PLM)

- 9.1.1.5. Manufacturing Execution System (MES)

- 9.1.1.6. Human Machine Interface (HMI)

- 9.1.1.7. Other Industrial Control Systems

- 9.1.2. Field Devices

- 9.1.2.1. Machine Vision

- 9.1.2.2. Industrial Robotics

- 9.1.2.3. Motors and Drives

- 9.1.2.4. Safety Systems

- 9.1.2.5. Sensors & Transmitters

- 9.1.2.6. Other Field Devices

- 9.1.1. Industrial Control Systems

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Oil and Gas

- 9.2.2. Chemical and Petrochemical

- 9.2.3. Power and Utilities

- 9.2.4. Food and Beverage

- 9.2.5. Automotive and Transportation

- 9.2.6. Pharmaceutical

- 9.2.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Industrial Control Systems

- 10.1.1.1. Distributed Control System (DCS)

- 10.1.1.2. Programable Logic Controller (PLC)

- 10.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 10.1.1.4. Product Lifecycle Management (PLM)

- 10.1.1.5. Manufacturing Execution System (MES)

- 10.1.1.6. Human Machine Interface (HMI)

- 10.1.1.7. Other Industrial Control Systems

- 10.1.2. Field Devices

- 10.1.2.1. Machine Vision

- 10.1.2.2. Industrial Robotics

- 10.1.2.3. Motors and Drives

- 10.1.2.4. Safety Systems

- 10.1.2.5. Sensors & Transmitters

- 10.1.2.6. Other Field Devices

- 10.1.1. Industrial Control Systems

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Oil and Gas

- 10.2.2. Chemical and Petrochemical

- 10.2.3. Power and Utilities

- 10.2.4. Food and Beverage

- 10.2.5. Automotive and Transportation

- 10.2.6. Pharmaceutical

- 10.2.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific US Factory Automation and Industrial Controls Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Industrial Control Systems

- 11.1.1.1. Distributed Control System (DCS)

- 11.1.1.2. Programable Logic Controller (PLC)

- 11.1.1.3. Supervisory Control and Data Acquisition (SCADA)

- 11.1.1.4. Product Lifecycle Management (PLM)

- 11.1.1.5. Manufacturing Execution System (MES)

- 11.1.1.6. Human Machine Interface (HMI)

- 11.1.1.7. Other Industrial Control Systems

- 11.1.2. Field Devices

- 11.1.2.1. Machine Vision

- 11.1.2.2. Industrial Robotics

- 11.1.2.3. Motors and Drives

- 11.1.2.4. Safety Systems

- 11.1.2.5. Sensors & Transmitters

- 11.1.2.6. Other Field Devices

- 11.1.1. Industrial Control Systems

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Oil and Gas

- 11.2.2. Chemical and Petrochemical

- 11.2.3. Power and Utilities

- 11.2.4. Food and Beverage

- 11.2.5. Automotive and Transportation

- 11.2.6. Pharmaceutical

- 11.2.7. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Honeywell International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ABB Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mitsubishi Electric Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Siemens AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Schneider Electric SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Omron Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Rockwell Automation Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Yokogawa Electric Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Fanuc Corporation*List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Emerson Electric Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Honeywell International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Factory Automation and Industrial Controls Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Factory Automation and Industrial Controls Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America US Factory Automation and Industrial Controls Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America US Factory Automation and Industrial Controls Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: North America US Factory Automation and Industrial Controls Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America US Factory Automation and Industrial Controls Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Factory Automation and Industrial Controls Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Factory Automation and Industrial Controls Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America US Factory Automation and Industrial Controls Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America US Factory Automation and Industrial Controls Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: South America US Factory Automation and Industrial Controls Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: South America US Factory Automation and Industrial Controls Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Factory Automation and Industrial Controls Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Factory Automation and Industrial Controls Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe US Factory Automation and Industrial Controls Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe US Factory Automation and Industrial Controls Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe US Factory Automation and Industrial Controls Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe US Factory Automation and Industrial Controls Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Factory Automation and Industrial Controls Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Factory Automation and Industrial Controls Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 30: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 39: Global US Factory Automation and Industrial Controls Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Factory Automation and Industrial Controls Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Factory Automation and Industrial Controls Industry?

The projected CAGR is approximately 9.8%.

2. Which companies are prominent players in the US Factory Automation and Industrial Controls Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, Omron Corporation, Rockwell Automation Inc, Yokogawa Electric Corporation, Fanuc Corporation*List Not Exhaustive, Emerson Electric Company.

3. What are the main segments of the US Factory Automation and Industrial Controls Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 49.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Gaining Prominence for Automation Technologies; Proactive Government Policies and a Vibrant Startup Ecosystem.

6. What are the notable trends driving market growth?

Distributed Control Systems (DCS) are Expected to Witness Significant Adoption.

7. Are there any restraints impacting market growth?

; Trade Tensions and Implementation Challenges.

8. Can you provide examples of recent developments in the market?

April 2022 - Critical Manufacturing unveiled the latest version of its Manufacturing Execution System (MES) at Hannover Messe 2022. Advancements in Critical Manufacturing MES (V9) help high-tech manufacturers prevail amidst changing market conditions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Factory Automation and Industrial Controls Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Factory Automation and Industrial Controls Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Factory Automation and Industrial Controls Industry?

To stay informed about further developments, trends, and reports in the US Factory Automation and Industrial Controls Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence