Key Insights

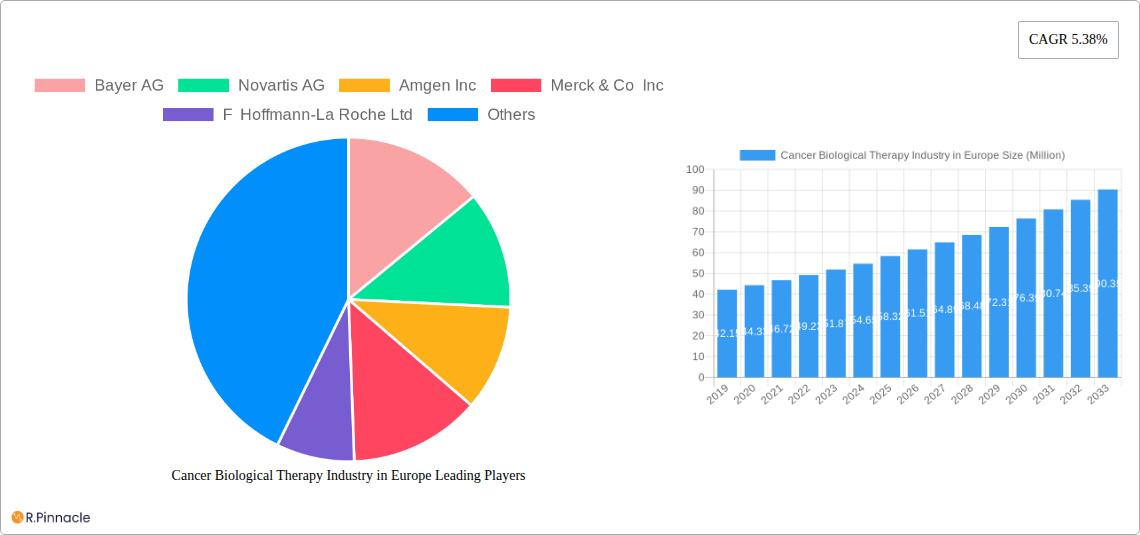

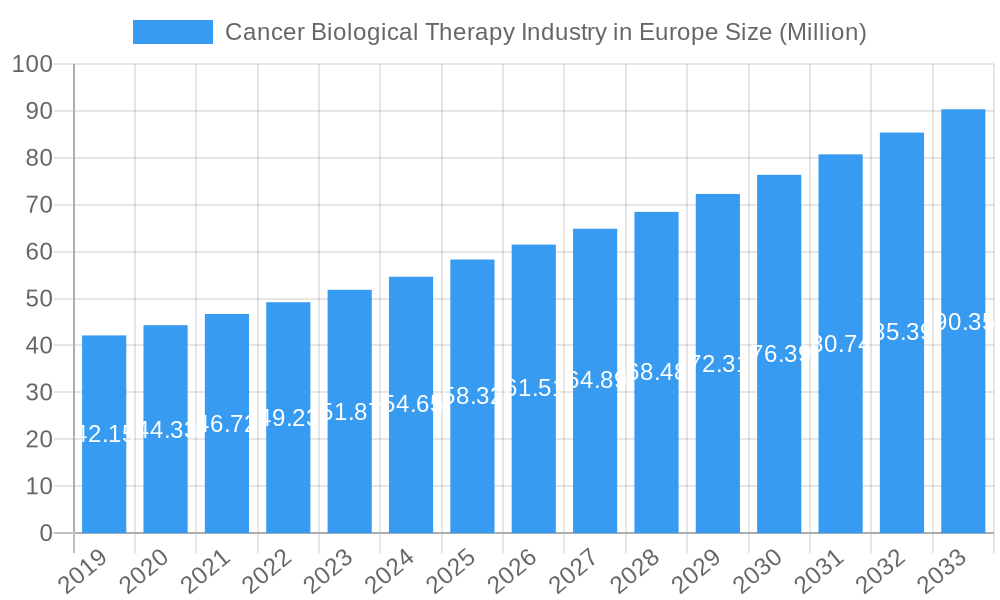

The European Cancer Biological Therapy Market is poised for substantial growth, projected to reach $58.32 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 5.38% through 2033. This robust expansion is driven by a confluence of factors, including the increasing incidence of various cancer types across the continent, such as blood, breast, prostate, and gastrointestinal cancers. Advances in research and development are leading to more targeted and effective biological therapies, offering improved patient outcomes and reduced side effects compared to traditional treatments. Key drivers include the growing understanding of tumor biology, the development of personalized medicine approaches, and significant investments in oncology drug discovery by leading pharmaceutical and biotechnology companies. The rising prevalence of lifestyle-related diseases and an aging population further contribute to the increasing demand for advanced cancer treatments. The market is characterized by a strong pipeline of innovative therapies and a growing adoption of immunotherapy and target therapy, which are demonstrating remarkable efficacy in treating complex cancers.

Cancer Biological Therapy Industry in Europe Market Size (In Million)

The competitive landscape of the European Cancer Biological Therapy Market is dynamic, with major global players such as Bayer AG, Novartis AG, Amgen Inc., Merck & Co Inc., and F Hoffmann-La Roche Ltd. actively investing in research, development, and strategic collaborations. The market segmentation reveals a strong focus on the treatment of blood, breast, and lung cancers, with chemotherapy, target therapy, and immunotherapy being the dominant treatment modalities. Hospitals and specialized cancer centers are the primary end-users, reflecting the sophisticated nature of biological therapy administration and patient management. Restraints, such as the high cost of advanced therapies and stringent regulatory approvals, are being mitigated by favorable reimbursement policies in several European countries and a continuous push for cost-effectiveness through innovative manufacturing processes and biosimilars. Emerging trends include the increasing use of companion diagnostics to identify patient populations most likely to benefit from specific biological therapies and the growing exploration of combination therapies to enhance treatment efficacy against resistant cancers.

Cancer Biological Therapy Industry in Europe Company Market Share

Cancer Biological Therapy Industry in Europe Market Structure & Innovation Trends

The European cancer biological therapy market exhibits a dynamic structure characterized by significant innovation and a degree of market concentration. Key players like Bayer AG, Novartis AG, and F Hoffmann-La Roche Ltd hold substantial market shares, driven by robust R&D pipelines and strategic acquisitions. The market is intensely competitive, with Amgen Inc, Merck & Co Inc, and AstraZeneca PLC also vying for dominance. Innovation is primarily fueled by advancements in immunotherapy and targeted therapy, with a growing emphasis on personalized medicine and novel drug delivery systems. Regulatory frameworks, while stringent, are evolving to accommodate groundbreaking therapies. Potential substitutes exist in traditional chemotherapy, but biological therapies offer improved efficacy and reduced side effects for many indications. End-user demographics show a rising demand from an aging population and increased cancer incidence. M&A activities are a significant feature, with substantial deal values indicating consolidation and strategic expansion. For example, Pfizer Inc and Johnson & Johnson are actively involved in strategic partnerships and acquisitions to bolster their oncology portfolios. The overall market concentration is moderate to high, with a few dominant players influencing market trends and innovation trajectories.

Cancer Biological Therapy Industry in Europe Market Dynamics & Trends

The European cancer biological therapy market is poised for substantial growth, driven by a confluence of technological advancements, increasing cancer prevalence, and a growing emphasis on personalized medicine. The CAGR for this sector is projected to be robust throughout the forecast period of 2025-2033. This expansion is significantly influenced by escalating R&D investments by major pharmaceutical companies such as Bristol-Myers Squibb Company, GlaxoSmithKline PLC, and Bayer AG. These investments are translating into the development of more effective and less toxic therapeutic options compared to conventional treatments.

Technological disruptions are a primary growth catalyst. The advent of sophisticated gene sequencing and bioinformatics has enabled a deeper understanding of cancer at a molecular level, paving the way for highly targeted therapies and innovative immunotherapies. These advancements are crucial for the successful development and deployment of novel treatments for complex cancers.

Consumer preferences are also shifting. Patients and healthcare providers are increasingly favoring biological therapies due to their potential for higher remission rates, improved quality of life, and reduced side effects. This growing demand is a significant market penetration driver, encouraging further investment and innovation.

Competitive dynamics within the industry are intense. Companies are actively engaged in strategic collaborations, licensing agreements, and mergers and acquisitions to secure their market positions and expand their product portfolios. The landscape includes established giants like Novartis AG, Amgen Inc, and F Hoffmann-La Roche Ltd, alongside agile biotech firms, all competing to bring groundbreaking therapies to market. The market penetration of biological therapies is expected to continue its upward trajectory as more effective treatments become available and reimbursement policies adapt to recognize their value. The ongoing research into novel drug targets and delivery mechanisms will further shape the market's evolution, making it a dynamic and rapidly advancing sector within the broader European healthcare industry.

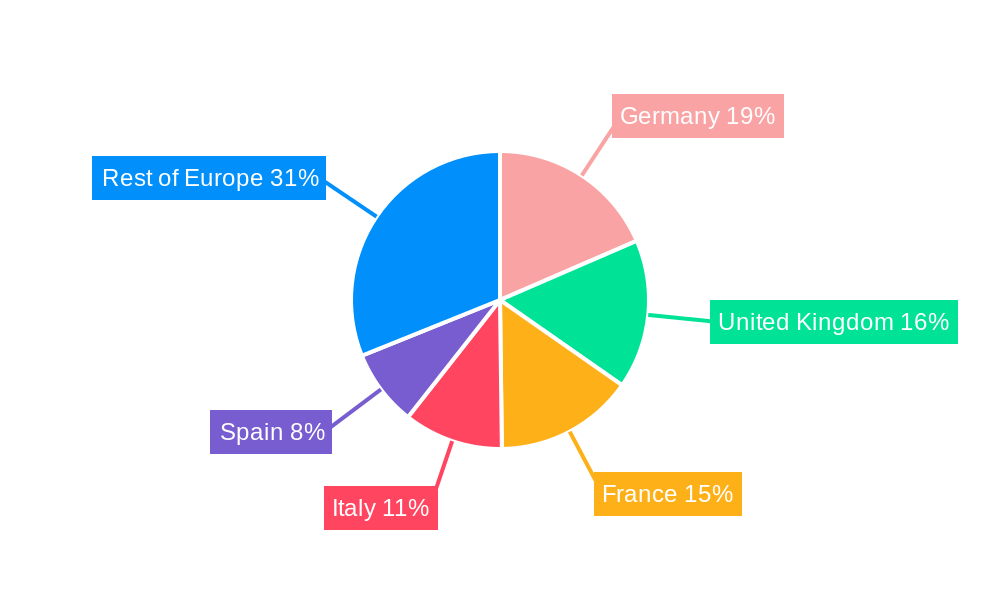

Dominant Regions & Segments in Cancer Biological Therapy Industry in Europe

Western European countries, particularly Germany, the United Kingdom, France, and Switzerland, currently dominate the cancer biological therapy industry in Europe. This dominance is attributed to several key drivers, including robust healthcare infrastructure, high disposable incomes, a higher prevalence of targeted cancer research institutions, and favorable reimbursement policies for advanced therapies. Economic policies in these nations often prioritize healthcare innovation and patient access to cutting-edge treatments, fostering a fertile ground for biological therapy market growth.

Within the treatment segment, Immunotherapy (Biologic Therapy) is experiencing the most significant growth and dominance. This surge is propelled by breakthroughs in checkpoint inhibitors, CAR T-cell therapies, and monoclonal antibodies, offering unprecedented efficacy in various cancer types. Target Therapy also holds a substantial market share, driven by the increasing availability of personalized treatments tailored to specific genetic mutations within cancer cells. While Chemotherapy remains a foundational treatment, its market share is gradually being influenced by the superior outcomes and reduced toxicity profile of biological options for many indications. Hormonal Therapy continues to be crucial for hormone-sensitive cancers like breast and prostate cancer.

In terms of cancer types, Breast Cancer and Prostate Cancer are leading segments for biological therapy applications due to well-established targeted and hormonal treatment protocols. Blood Cancer also represents a significant and growing market, particularly with the advancements in CAR T-cell therapies. Gastrointestinal Cancer and Respiratory/Lung Cancer are also witnessing increased adoption of biological therapies as research yields more effective treatment options.

The end-user segment is primarily dominated by Hospitals, which possess the infrastructure and specialized medical expertise to administer complex biological therapies. Specialty Clinics focusing on oncology are also significant contributors, offering focused care and advanced treatment options. While Cancer and Radiation Therapy Centers are vital for comprehensive cancer care, their direct involvement in biological therapy administration might be more specialized compared to general hospitals. The economic policies supporting research and development of novel biological agents, coupled with the infrastructure readiness to adopt these advanced treatments, underpin the dominance of these regions and segments.

Cancer Biological Therapy Industry in Europe Product Innovations

Product innovation in the European cancer biological therapy market is rapidly evolving, focusing on enhancing therapeutic efficacy, reducing side effects, and expanding treatment accessibility. Key trends include the development of bispecific antibodies that can engage multiple cancer targets simultaneously, and next-generation CAR T-cell therapies with improved persistence and safety profiles. Advances in mRNA technology are also leading to novel cancer vaccines and personalized immunotherapies. These innovations aim to overcome treatment resistance and address unmet needs in challenging cancer types, providing a competitive advantage by offering more precise and potent treatment modalities that align with the growing demand for personalized oncology solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Cancer Biological Therapy Industry in Europe, encompassing its market structure, dynamics, and future outlook. The market is segmented by Treatment Type, including Chemotherapy, Target Therapy, Immunotherapy (Biologic Therapy), Hormonal Therapy, and Other Treatment Types. Each segment's market size, growth projections, and competitive dynamics are thoroughly examined. Further segmentation by Cancer Type includes Blood Cancer, Breast Cancer, Prostate Cancer, Gastrointestinal Cancer, Gynecologic Cancer, Respiratory/Lung Cancer, and Other Cancer Types. The End User segmentation covers Hospitals, Specialty Clinics, and Cancer and Radiation Therapy Centers. Each segment's market penetration and key growth drivers are detailed, offering granular insights into the European landscape.

Key Drivers of Cancer Biological Therapy Industry in Europe Growth

Several key factors are propelling the growth of the Cancer Biological Therapy Industry in Europe. Technological advancements in genomics and proteomics are enabling the development of highly targeted therapies with improved efficacy. Increased R&D investments by pharmaceutical giants and biotech firms, driven by the lucrative oncology market, are accelerating drug discovery and development. A rising cancer incidence across Europe, coupled with an aging population, is creating a sustained demand for advanced treatment options. Favorable regulatory pathways for innovative therapies and evolving reimbursement policies that recognize the value of biological treatments are also crucial growth accelerators. Furthermore, a growing awareness among patients and healthcare professionals regarding the benefits of biological therapies over conventional treatments is significantly impacting market penetration.

Challenges in the Cancer Biological Therapy Industry in Europe Sector

Despite robust growth, the Cancer Biological Therapy Industry in Europe faces several significant challenges. The high cost of developing and manufacturing these complex biological agents leads to expensive treatments, posing affordability and accessibility issues for some patient populations and healthcare systems. Stringent and lengthy regulatory approval processes, while ensuring safety and efficacy, can delay market entry for innovative therapies. Furthermore, complex supply chain management for biologics, requiring specialized storage and handling, presents logistical hurdles. Competitive pressures from both established players and emerging biotech companies necessitate continuous innovation and strategic market positioning. The emergence of treatment resistance in certain cancers also demands ongoing research into novel therapeutic strategies and combination approaches.

Emerging Opportunities in Cancer Biological Therapy Industry in Europe

The European cancer biological therapy sector presents numerous emerging opportunities. The continued advancement in personalized medicine, utilizing biomarker-driven patient stratification, offers a significant avenue for niche market development. The expansion of CAR T-cell therapy beyond hematological malignancies into solid tumors represents a substantial growth frontier. Growing investments in early-stage research for novel immunotherapy targets, such as oncolytic viruses and T-cell engagers, hold immense promise for future pipeline development. The increasing adoption of digital health technologies, including AI-powered diagnostics and treatment planning, can optimize patient selection and treatment outcomes. Furthermore, strategic collaborations between pharmaceutical companies and academic research institutions can accelerate the translation of cutting-edge scientific discoveries into clinical applications.

Leading Players in the Cancer Biological Therapy Industry in Europe Market

- Bayer AG

- Novartis AG

- Amgen Inc

- Merck & Co Inc

- F Hoffmann-La Roche Ltd

- AstraZeneca PLC

- Pfizer Inc

- Johnson & Johnson

- Bristol-Myers Squibb Company

- GlaxoSmithKline PLC

Key Developments in Cancer Biological Therapy Industry in Europe Industry

- May 2022: Boehringer Ingelheim acquired Northern Biologics, a wholly owned subsidiary of Northern LP. This acquisition has assisted the company to add two complementary assets to its existing cancer immunology portfolio including cancer vaccines, oncolytic viruses, T-cell engagers, and myeloid cell modulators.

- June 2021: Genetech collaborated with Nykode (Vaccibody) to develop novel DNA-based cancer vaccines. This global, oncology collaboration between Nykode and Genentech is to develop individualized neoantigen cancer vaccines across multiple tumor types.

Future Outlook for Cancer Biological Therapy Industry in Europe Market

The future outlook for the Cancer Biological Therapy Industry in Europe is exceptionally promising, characterized by sustained growth and transformative innovation. The market is expected to be driven by ongoing breakthroughs in immunotherapy, targeted therapies, and the increasing application of precision medicine. The focus on developing combination therapies to overcome treatment resistance and improve patient outcomes will be a significant growth accelerator. Furthermore, the exploration of novel drug delivery systems and the integration of advanced digital health technologies will enhance treatment efficacy and patient management. Strategic partnerships and M&A activities will continue to shape the competitive landscape, fostering consolidation and the expansion of product portfolios. The increasing understanding of the tumor microenvironment and the development of next-generation biologics are expected to address a wider spectrum of cancers, further solidifying the market's growth trajectory.

Cancer Biological Therapy Industry in Europe Segmentation

-

1. Treatment

- 1.1. Chemotherapy

- 1.2. Target Therapy

- 1.3. Immunotherapy (Biologic Therapy)

- 1.4. Hormonal Therapy

- 1.5. Other Treatment Types

-

2. Cancer Type

- 2.1. Blood Cancer

- 2.2. Breast Cancer

- 2.3. Prostate Cancer

- 2.4. Gastrointestinal Cancer

- 2.5. Gynecologic Cancer

- 2.6. Respiratory/Lung Cancer

- 2.7. Other Cancer Types

-

3. End User

- 3.1. Hospitals

- 3.2. Specilty Clinics

- 3.3. Cancer and Radiation Therapy Centers

Cancer Biological Therapy Industry in Europe Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Cancer Biological Therapy Industry in Europe Regional Market Share

Geographic Coverage of Cancer Biological Therapy Industry in Europe

Cancer Biological Therapy Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 5.1.1. Chemotherapy

- 5.1.2. Target Therapy

- 5.1.3. Immunotherapy (Biologic Therapy)

- 5.1.4. Hormonal Therapy

- 5.1.5. Other Treatment Types

- 5.2. Market Analysis, Insights and Forecast - by Cancer Type

- 5.2.1. Blood Cancer

- 5.2.2. Breast Cancer

- 5.2.3. Prostate Cancer

- 5.2.4. Gastrointestinal Cancer

- 5.2.5. Gynecologic Cancer

- 5.2.6. Respiratory/Lung Cancer

- 5.2.7. Other Cancer Types

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Specilty Clinics

- 5.3.3. Cancer and Radiation Therapy Centers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 6. Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 6.1.1. Chemotherapy

- 6.1.2. Target Therapy

- 6.1.3. Immunotherapy (Biologic Therapy)

- 6.1.4. Hormonal Therapy

- 6.1.5. Other Treatment Types

- 6.2. Market Analysis, Insights and Forecast - by Cancer Type

- 6.2.1. Blood Cancer

- 6.2.2. Breast Cancer

- 6.2.3. Prostate Cancer

- 6.2.4. Gastrointestinal Cancer

- 6.2.5. Gynecologic Cancer

- 6.2.6. Respiratory/Lung Cancer

- 6.2.7. Other Cancer Types

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Specilty Clinics

- 6.3.3. Cancer and Radiation Therapy Centers

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 7. Germany Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 7.1.1. Chemotherapy

- 7.1.2. Target Therapy

- 7.1.3. Immunotherapy (Biologic Therapy)

- 7.1.4. Hormonal Therapy

- 7.1.5. Other Treatment Types

- 7.2. Market Analysis, Insights and Forecast - by Cancer Type

- 7.2.1. Blood Cancer

- 7.2.2. Breast Cancer

- 7.2.3. Prostate Cancer

- 7.2.4. Gastrointestinal Cancer

- 7.2.5. Gynecologic Cancer

- 7.2.6. Respiratory/Lung Cancer

- 7.2.7. Other Cancer Types

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Specilty Clinics

- 7.3.3. Cancer and Radiation Therapy Centers

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 8. United Kingdom Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 8.1.1. Chemotherapy

- 8.1.2. Target Therapy

- 8.1.3. Immunotherapy (Biologic Therapy)

- 8.1.4. Hormonal Therapy

- 8.1.5. Other Treatment Types

- 8.2. Market Analysis, Insights and Forecast - by Cancer Type

- 8.2.1. Blood Cancer

- 8.2.2. Breast Cancer

- 8.2.3. Prostate Cancer

- 8.2.4. Gastrointestinal Cancer

- 8.2.5. Gynecologic Cancer

- 8.2.6. Respiratory/Lung Cancer

- 8.2.7. Other Cancer Types

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Specilty Clinics

- 8.3.3. Cancer and Radiation Therapy Centers

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 9. France Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 9.1.1. Chemotherapy

- 9.1.2. Target Therapy

- 9.1.3. Immunotherapy (Biologic Therapy)

- 9.1.4. Hormonal Therapy

- 9.1.5. Other Treatment Types

- 9.2. Market Analysis, Insights and Forecast - by Cancer Type

- 9.2.1. Blood Cancer

- 9.2.2. Breast Cancer

- 9.2.3. Prostate Cancer

- 9.2.4. Gastrointestinal Cancer

- 9.2.5. Gynecologic Cancer

- 9.2.6. Respiratory/Lung Cancer

- 9.2.7. Other Cancer Types

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Specilty Clinics

- 9.3.3. Cancer and Radiation Therapy Centers

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 10. Italy Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 10.1.1. Chemotherapy

- 10.1.2. Target Therapy

- 10.1.3. Immunotherapy (Biologic Therapy)

- 10.1.4. Hormonal Therapy

- 10.1.5. Other Treatment Types

- 10.2. Market Analysis, Insights and Forecast - by Cancer Type

- 10.2.1. Blood Cancer

- 10.2.2. Breast Cancer

- 10.2.3. Prostate Cancer

- 10.2.4. Gastrointestinal Cancer

- 10.2.5. Gynecologic Cancer

- 10.2.6. Respiratory/Lung Cancer

- 10.2.7. Other Cancer Types

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Specilty Clinics

- 10.3.3. Cancer and Radiation Therapy Centers

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 11. Spain Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Treatment

- 11.1.1. Chemotherapy

- 11.1.2. Target Therapy

- 11.1.3. Immunotherapy (Biologic Therapy)

- 11.1.4. Hormonal Therapy

- 11.1.5. Other Treatment Types

- 11.2. Market Analysis, Insights and Forecast - by Cancer Type

- 11.2.1. Blood Cancer

- 11.2.2. Breast Cancer

- 11.2.3. Prostate Cancer

- 11.2.4. Gastrointestinal Cancer

- 11.2.5. Gynecologic Cancer

- 11.2.6. Respiratory/Lung Cancer

- 11.2.7. Other Cancer Types

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Specilty Clinics

- 11.3.3. Cancer and Radiation Therapy Centers

- 11.1. Market Analysis, Insights and Forecast - by Treatment

- 12. Rest of Europe Cancer Biological Therapy Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Treatment

- 12.1.1. Chemotherapy

- 12.1.2. Target Therapy

- 12.1.3. Immunotherapy (Biologic Therapy)

- 12.1.4. Hormonal Therapy

- 12.1.5. Other Treatment Types

- 12.2. Market Analysis, Insights and Forecast - by Cancer Type

- 12.2.1. Blood Cancer

- 12.2.2. Breast Cancer

- 12.2.3. Prostate Cancer

- 12.2.4. Gastrointestinal Cancer

- 12.2.5. Gynecologic Cancer

- 12.2.6. Respiratory/Lung Cancer

- 12.2.7. Other Cancer Types

- 12.3. Market Analysis, Insights and Forecast - by End User

- 12.3.1. Hospitals

- 12.3.2. Specilty Clinics

- 12.3.3. Cancer and Radiation Therapy Centers

- 12.1. Market Analysis, Insights and Forecast - by Treatment

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Bayer AG

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Novartis AG

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Amgen Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Merck & Co Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 F Hoffmann-La Roche Ltd

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 AstraZeneca PLC

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Pfizer Inc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Johnson & Johnson

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Bristol-Myers Squibb Company

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 GlaxoSmithKline PLC

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Bayer AG

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Cancer Biological Therapy Industry in Europe Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Cancer Biological Therapy Industry in Europe Share (%) by Company 2025

List of Tables

- Table 1: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 2: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 3: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 4: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 5: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 10: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 11: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 12: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 13: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 14: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 15: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 18: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 19: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 20: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 21: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 22: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 23: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 26: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 27: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 28: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 29: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 31: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

- Table 33: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 34: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 35: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 36: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 37: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 38: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 39: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 42: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 43: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 44: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 45: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 46: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 47: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

- Table 49: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Treatment 2020 & 2033

- Table 50: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 51: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Cancer Type 2020 & 2033

- Table 52: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Cancer Type 2020 & 2033

- Table 53: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 54: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by End User 2020 & 2033

- Table 55: Cancer Biological Therapy Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Cancer Biological Therapy Industry in Europe Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cancer Biological Therapy Industry in Europe?

The projected CAGR is approximately 5.38%.

2. Which companies are prominent players in the Cancer Biological Therapy Industry in Europe?

Key companies in the market include Bayer AG, Novartis AG, Amgen Inc, Merck & Co Inc, F Hoffmann-La Roche Ltd, AstraZeneca PLC, Pfizer Inc , Johnson & Johnson, Bristol-Myers Squibb Company, GlaxoSmithKline PLC.

3. What are the main segments of the Cancer Biological Therapy Industry in Europe?

The market segments include Treatment, Cancer Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 58.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Cancer in Europe; Strong R&D Initiatives from Key Players.

6. What are the notable trends driving market growth?

Target Therapy is Expected to Witness Significant Growth over the Forecast Period (2022-2027).

7. Are there any restraints impacting market growth?

Inequality in Access of Cancer Therapy across Europe; High Cost of Cancer Therapies.

8. Can you provide examples of recent developments in the market?

In May 2022 Boehringer Ingelheim acquired Northern Biologics, a wholly owned subsidiary of Northern LP. This acquisition has assisted the company to add two complementary assets to its existing cancer immunology portfolio including cancer vaccines, oncolytic viruses, T-cell engagers, and myeloid cell modulators.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cancer Biological Therapy Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cancer Biological Therapy Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cancer Biological Therapy Industry in Europe?

To stay informed about further developments, trends, and reports in the Cancer Biological Therapy Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence