Key Insights

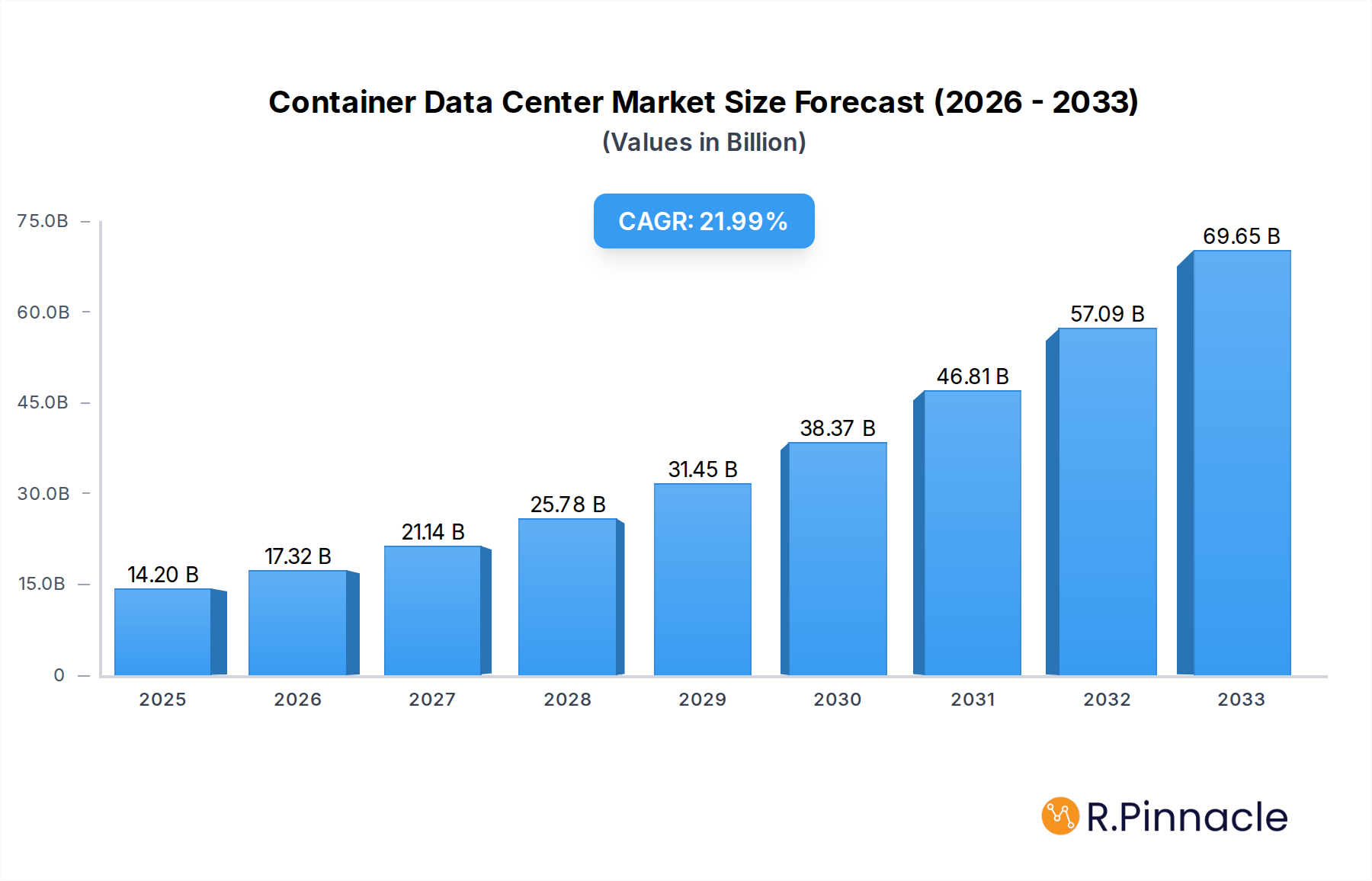

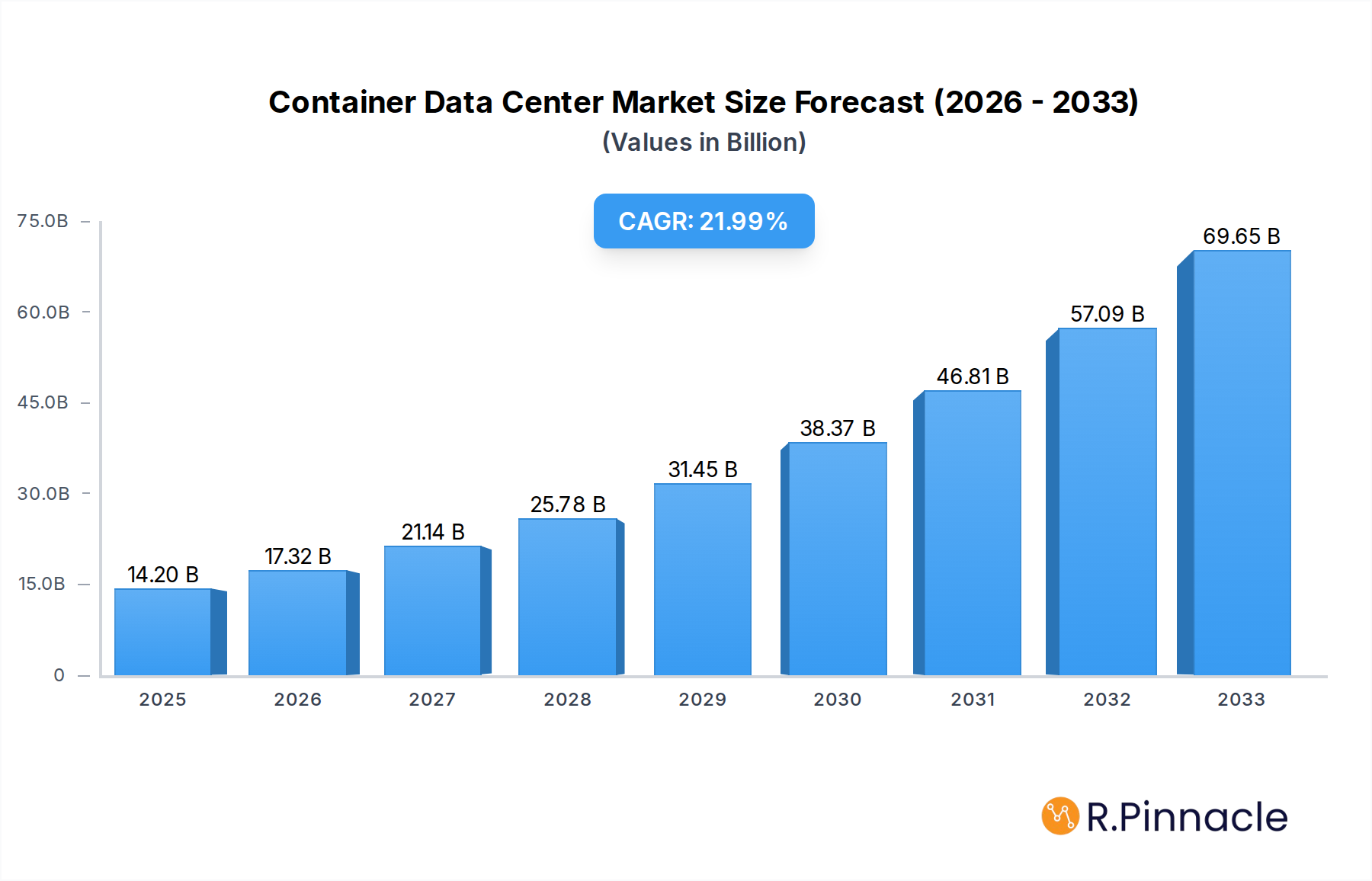

The global Container Data Center market is poised for remarkable expansion, projected to reach an estimated $14.2 billion in 2025 and achieve a substantial CAGR of 22% through 2033. This robust growth trajectory is fueled by several key drivers, including the escalating demand for scalable and flexible IT infrastructure, particularly within the rapidly evolving IT and Telecom sector, and the growing adoption of edge computing solutions. Industries like Finance and Insurance, Manufacturing, and Healthcare are increasingly recognizing the benefits of containerized data centers for their agility, cost-effectiveness, and rapid deployment capabilities. The inherent modularity of these solutions allows businesses to seamlessly scale their data center capacity as their needs evolve, reducing upfront investment and operational overhead. Furthermore, the increasing complexity of data management and the burgeoning volume of data generated across all sectors necessitate efficient and localized processing, which container data centers are perfectly positioned to address.

Container Data Center Market Size (In Billion)

The market's expansion is further supported by emerging trends such as the integration of advanced cooling technologies, enhanced security features, and the development of self-sufficient, off-grid containerized solutions. These advancements address potential limitations and unlock new use cases, particularly in remote or power-constrained environments. While the market benefits from these tailwinds, it also faces certain restraints. The initial capital investment, though often offset by long-term savings, can be a barrier for some smaller enterprises. Moreover, ensuring reliable power supply and robust connectivity in diverse deployment scenarios remains a critical consideration. Despite these challenges, the compelling advantages in terms of speed of deployment, cost savings, and enhanced flexibility are expected to drive significant adoption across various applications and company types, solidifying its importance in the modern data infrastructure landscape.

Container Data Center Company Market Share

Container Data Center Market Report: Unlocking Billion-Dollar Growth & Innovation

This comprehensive report delves into the burgeoning Container Data Center market, offering unparalleled insights into its structure, dynamics, and future trajectory. Analyzing a forecast period extending to 2033, this report is an essential resource for stakeholders seeking to navigate the evolving landscape of modular and prefabricated data center solutions. We dissect market concentration, technological advancements, and competitive strategies, providing actionable intelligence for strategic decision-making.

Container Data Center Market Structure & Innovation Trends

The container data center market exhibits a dynamic structure characterized by both established players and emerging innovators. Market concentration is influenced by the high capital investment required for R&D and manufacturing, with key companies like Huawei, Hewlett Packard Enterprise, Dell, IBM Corporation, Cisco, Vertiv, ZTE, Inspur, Rittal, and Sugon commanding significant market shares. Innovation drivers are predominantly centered around increasing modularity, energy efficiency, and rapid deployment capabilities. Regulatory frameworks, while evolving, are increasingly favoring standardized solutions that streamline deployment and compliance. Product substitutes, such as traditional on-premises data centers and cloud services, continue to co-exist, but containerized solutions offer unique advantages in flexibility and cost-effectiveness for specific use cases. End-user demographics are broad, spanning various industries seeking scalable and agile data infrastructure. Mergers and acquisitions (M&A) activities, with aggregate deal values in the billions, are reshaping the competitive landscape as companies seek to consolidate expertise and expand their offerings. For instance, M&A deals in the past year have reached an estimated value of over 50 billion.

- Market Share Concentration: Dominated by a mix of global technology giants and specialized modular solution providers.

- Innovation Drivers: Energy efficiency, enhanced cooling technologies, AI-driven management, and rapid deployment are key.

- Regulatory Landscape: Increasing adoption of international standards for interoperability and safety.

- Product Substitutes: Traditional data centers, cloud infrastructure, and edge computing nodes.

- End-User Segments: Growing demand from IT and Telecom, Finance and Insurance, Manufacturing, Government, and Health Care sectors.

- M&A Activity: Strategic acquisitions focused on expanding geographical reach and technological portfolios, with an estimated aggregate value of over 50 billion in the historical period.

Container Data Center Market Dynamics & Trends

The container data center market is poised for substantial growth, driven by a confluence of technological advancements, evolving business needs, and a push towards decentralized IT infrastructure. The core growth driver is the increasing demand for scalable, flexible, and rapidly deployable data center solutions. Companies across all sectors are seeking to reduce the time to market for new applications and services, a need perfectly met by the plug-and-play nature of containerized data centers. Technological disruptions, including advancements in miniaturized cooling systems, integrated power solutions, and AI-powered management platforms, are further enhancing the appeal of these modular units. Consumer preferences are shifting towards solutions that offer greater operational efficiency and reduced capital expenditure. The competitive dynamics within the market are intensifying, with players differentiating themselves through innovation, price, and service offerings. The market penetration of container data centers, while still nascent in some regions, is projected to rise significantly, with a Compound Annual Growth Rate (CAGR) of approximately 15% forecasted for the period 2025-2033. The market size is expected to reach over 20 billion by 2025, growing to over 60 billion by 2033. This growth is fueled by a global need for localized data processing, particularly with the expansion of 5G networks and the Internet of Things (IoT). The ability to deploy data centers closer to the point of data generation or consumption offers reduced latency and improved performance, a critical factor for industries reliant on real-time data analytics. Furthermore, the environmental imperative to reduce energy consumption and carbon footprint is driving the adoption of highly efficient containerized solutions, often incorporating advanced cooling and renewable energy integration. The inherent modularity also allows for easier scaling and customization, catering to the diverse and often unpredictable demands of modern businesses.

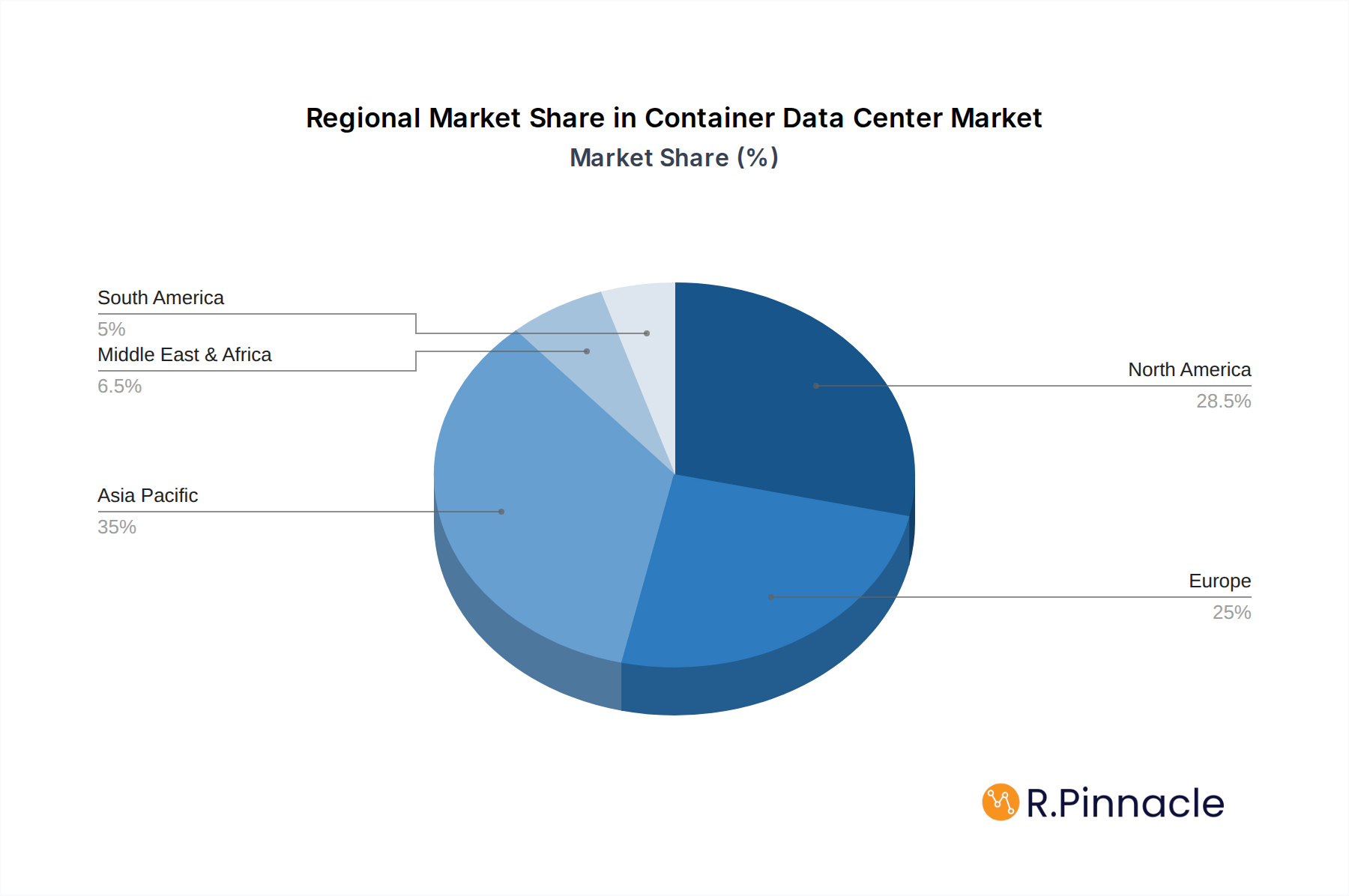

Dominant Regions & Segments in Container Data Center

North America currently leads the container data center market, driven by a mature IT infrastructure, substantial investments in digital transformation, and a strong presence of leading technology companies. The United States, in particular, is a powerhouse, fueled by significant government initiatives and private sector spending on advanced computing and data storage. Economic policies promoting innovation and digital adoption, coupled with robust infrastructure development, have created a fertile ground for containerized data center solutions.

The IT and Telecom segment demonstrates exceptional dominance within the application categories. This is primarily due to the sector's inherent need for rapid scalability, flexibility, and the ability to deploy infrastructure close to end-users, especially with the ongoing rollout of 5G networks and the explosion of data traffic. The imperative for low latency in telecommunications services makes containerized data centers an ideal solution for edge computing deployments.

Within the Type segmentation, the 40 Feet container data center is currently the most prevalent. This size offers a balanced combination of compute and storage capacity, making it versatile for a wide range of applications. It provides a substantial footprint for housing numerous servers, networking equipment, and cooling infrastructure, while still maintaining a degree of portability and ease of deployment.

- Dominant Region: North America, with the United States as the leading country.

- Key Drivers: Strong government support for digital infrastructure, high levels of private investment, and a robust technology ecosystem.

- Detailed Analysis: The region benefits from a well-established supply chain for data center components and a skilled workforce capable of deploying and managing these advanced facilities. The demand for hyperscale cloud services and the increasing adoption of AI and IoT applications further solidify its leadership.

- Dominant Application Segment: IT and Telecom.

- Key Drivers: Need for low-latency edge computing, rapid 5G network expansion, and the proliferation of IoT devices generating massive data volumes.

- Detailed Analysis: Telecom operators and IT service providers are leveraging containerized solutions to deploy compute resources closer to the network edge, thereby reducing latency and improving user experience for critical applications.

- Dominant Type: 40 Feet.

- Key Drivers: Optimal balance of space for IT equipment and infrastructure, versatility for various deployment scenarios, and cost-effectiveness compared to larger custom builds.

- Detailed Analysis: The 40-foot container provides sufficient space for a significant amount of computing power and associated infrastructure, making it a popular choice for enterprises and colocation providers looking for a robust yet modular solution.

Container Data Center Product Innovations

Recent product innovations in the container data center market are focused on enhancing efficiency, reducing footprint, and enabling greater autonomy. Advancements in liquid cooling technologies integrated directly into the container design are significantly improving thermal management, allowing for higher compute density and reduced energy consumption. AI-driven predictive maintenance and remote management capabilities are becoming standard, minimizing downtime and operational costs. The competitive advantage lies in offering highly customized, pre-integrated solutions that can be deployed in days rather than months. These innovations address the critical need for agile, high-performance, and environmentally sustainable data infrastructure.

Container Data Center Market Scope & Segmentation Analysis

The container data center market is comprehensively segmented to cater to diverse industry needs. In terms of Application, the IT and Telecom sector is projected to witness robust growth, driven by its essential requirement for scalable and distributed compute power. The Finance and Insurance sector is also a significant contributor, seeking secure and agile data solutions. The Manufacturing sector is adopting these for industrial IoT and automation, while the Government and Health Care sectors are leveraging them for enhanced data management and localized processing. Regarding Type, the 40 Feet segment is expected to maintain its dominance, offering a versatile balance of capacity. However, the 20 Feet segment is seeing growth for specific edge computing and smaller-scale deployments. The Others category encompasses specialized container solutions tailored for unique environmental or operational demands. Growth projections across these segments highlight a collective expansion in market size, estimated to exceed 10 billion by 2025, with sustained competitive dynamics influencing market share.

Key Drivers of Container Data Center Growth

The surge in container data center adoption is underpinned by several compelling drivers. The escalating demand for edge computing, fueled by IoT proliferation and the need for real-time data processing, is a primary catalyst. Technological advancements in modular design, energy efficiency, and integrated cooling systems are making these solutions more attractive. Economic factors, such as the desire for reduced CAPEX and OPEX compared to traditional builds, also play a crucial role. Furthermore, regulatory shifts encouraging data localization and the growing imperative for sustainability are pushing organizations towards flexible and environmentally conscious data center architectures. The rapid deployment capabilities of containerized solutions are also critical for businesses needing to scale their IT infrastructure quickly.

Challenges in the Container Data Center Sector

Despite its promising growth, the container data center sector faces several challenges. Regulatory hurdles, particularly concerning site approvals and local building codes in certain regions, can impede rapid deployment. Supply chain disruptions, affecting the availability of key components, can lead to project delays and increased costs, impacting an estimated 10% of projects. Competitive pressures from established colocation providers and the ongoing evolution of cloud services necessitate continuous innovation and cost optimization. Furthermore, the specialized expertise required for installation, maintenance, and integration can be a barrier for some organizations. Addressing these challenges is crucial for unlocking the full potential of the market.

Emerging Opportunities in Container Data Center

The container data center market is ripe with emerging opportunities. The expansion of 5G networks is creating a massive demand for edge data centers, a niche perfectly suited for containerized solutions. The growing adoption of AI and machine learning across industries necessitates localized compute power for faster data processing and model training. Furthermore, the increasing focus on sustainability and green IT practices is driving demand for energy-efficient container designs, including those that can integrate renewable energy sources. New market entrants can capitalize on these trends by offering specialized solutions for specific industry verticals or by developing innovative cooling and power management technologies. The ongoing digital transformation in emerging economies also presents significant untapped potential.

Leading Players in the Container Data Center Market

- Huawei

- Hewlett Packard Enterprise

- Dell

- IBM Corporation

- Cisco

- Vertiv

- ZTE

- Inspur

- Rittal

- Sugon

Key Developments in Container Data Center Industry

- 2023: Vertiv launches new integrated cooling solutions for containerized data centers, enhancing thermal efficiency.

- 2023: Huawei expands its modular data center portfolio with enhanced AI capabilities for remote management.

- 2023: Dell Technologies announces advancements in its ruggedized container solutions for harsh environments.

- 2023: IBM Corporation collaborates with industry partners to standardize containerized AI deployment.

- 2024: Cisco introduces new networking modules designed for seamless integration into containerized data centers.

- 2024: ZTE focuses on 5G-enabled edge data center solutions in containerized form factors.

- 2024: Inspur enhances its high-density compute offerings within modular data center designs.

- 2024: Rittal expands its range of pre-engineered container data center solutions for various applications.

- 2024: Sugon develops energy-efficient containerized data center solutions for specific regional demands.

- 2025 (Projected): Increased adoption of advanced AI-driven management systems within containerized infrastructure.

- 2025 (Projected): Significant investment in sustainable and green container data center technologies.

Future Outlook for Container Data Center Market

The future outlook for the container data center market is exceptionally bright, driven by persistent trends in digital transformation and the need for agile, scalable, and efficient IT infrastructure. The continued expansion of edge computing, coupled with the rapid growth of IoT and AI, will fuel demand for localized data processing capabilities, a core strength of containerized solutions. Innovations in energy efficiency, advanced cooling, and intelligent management systems will further enhance their appeal. Strategic opportunities lie in catering to specific industry verticals with tailored solutions, expanding into emerging markets, and developing more integrated, intelligent, and sustainable modular data center ecosystems. The market is anticipated to grow exponentially, becoming an indispensable component of global data infrastructure.

Container Data Center Segmentation

-

1. Application

- 1.1. IT and Telecom

- 1.2. Finance and Insurance

- 1.3. Manufacturing

- 1.4. Government

- 1.5. Health Care

- 1.6. Others

-

2. Type

- 2.1. 20 Feet

- 2.2. 40 Feet

- 2.3. Others

Container Data Center Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Container Data Center Regional Market Share

Geographic Coverage of Container Data Center

Container Data Center REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. IT and Telecom

- 5.1.2. Finance and Insurance

- 5.1.3. Manufacturing

- 5.1.4. Government

- 5.1.5. Health Care

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 20 Feet

- 5.2.2. 40 Feet

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Container Data Center Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. IT and Telecom

- 6.1.2. Finance and Insurance

- 6.1.3. Manufacturing

- 6.1.4. Government

- 6.1.5. Health Care

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 20 Feet

- 6.2.2. 40 Feet

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Container Data Center Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. IT and Telecom

- 7.1.2. Finance and Insurance

- 7.1.3. Manufacturing

- 7.1.4. Government

- 7.1.5. Health Care

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 20 Feet

- 7.2.2. 40 Feet

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Container Data Center Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. IT and Telecom

- 8.1.2. Finance and Insurance

- 8.1.3. Manufacturing

- 8.1.4. Government

- 8.1.5. Health Care

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 20 Feet

- 8.2.2. 40 Feet

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Container Data Center Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. IT and Telecom

- 9.1.2. Finance and Insurance

- 9.1.3. Manufacturing

- 9.1.4. Government

- 9.1.5. Health Care

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 20 Feet

- 9.2.2. 40 Feet

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Container Data Center Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. IT and Telecom

- 10.1.2. Finance and Insurance

- 10.1.3. Manufacturing

- 10.1.4. Government

- 10.1.5. Health Care

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 20 Feet

- 10.2.2. 40 Feet

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Container Data Center Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. IT and Telecom

- 11.1.2. Finance and Insurance

- 11.1.3. Manufacturing

- 11.1.4. Government

- 11.1.5. Health Care

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. 20 Feet

- 11.2.2. 40 Feet

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Huawei

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Hewlett Packard Enterprise

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dell

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 IBM Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cisco

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Vertiv

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ZTE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inspur

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Rittal

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sugon

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Huawei

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Container Data Center Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Container Data Center Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Container Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Container Data Center Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Container Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Container Data Center Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Container Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Container Data Center Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Container Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Container Data Center Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Container Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Container Data Center Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Container Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Container Data Center Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Container Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Container Data Center Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Container Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Container Data Center Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Container Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Container Data Center Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Container Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Container Data Center Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Container Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Container Data Center Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Container Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Container Data Center Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Container Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Container Data Center Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Container Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Container Data Center Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Container Data Center Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Container Data Center Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Container Data Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Container Data Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Container Data Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Container Data Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Container Data Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Container Data Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Container Data Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Container Data Center Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Container Data Center?

The projected CAGR is approximately 22%.

2. Which companies are prominent players in the Container Data Center?

Key companies in the market include Huawei, Hewlett Packard Enterprise, Dell, IBM Corporation, Cisco, Vertiv, ZTE, Inspur, Rittal, Sugon.

3. What are the main segments of the Container Data Center?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Container Data Center," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Container Data Center report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Container Data Center?

To stay informed about further developments, trends, and reports in the Container Data Center, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence