Key Insights

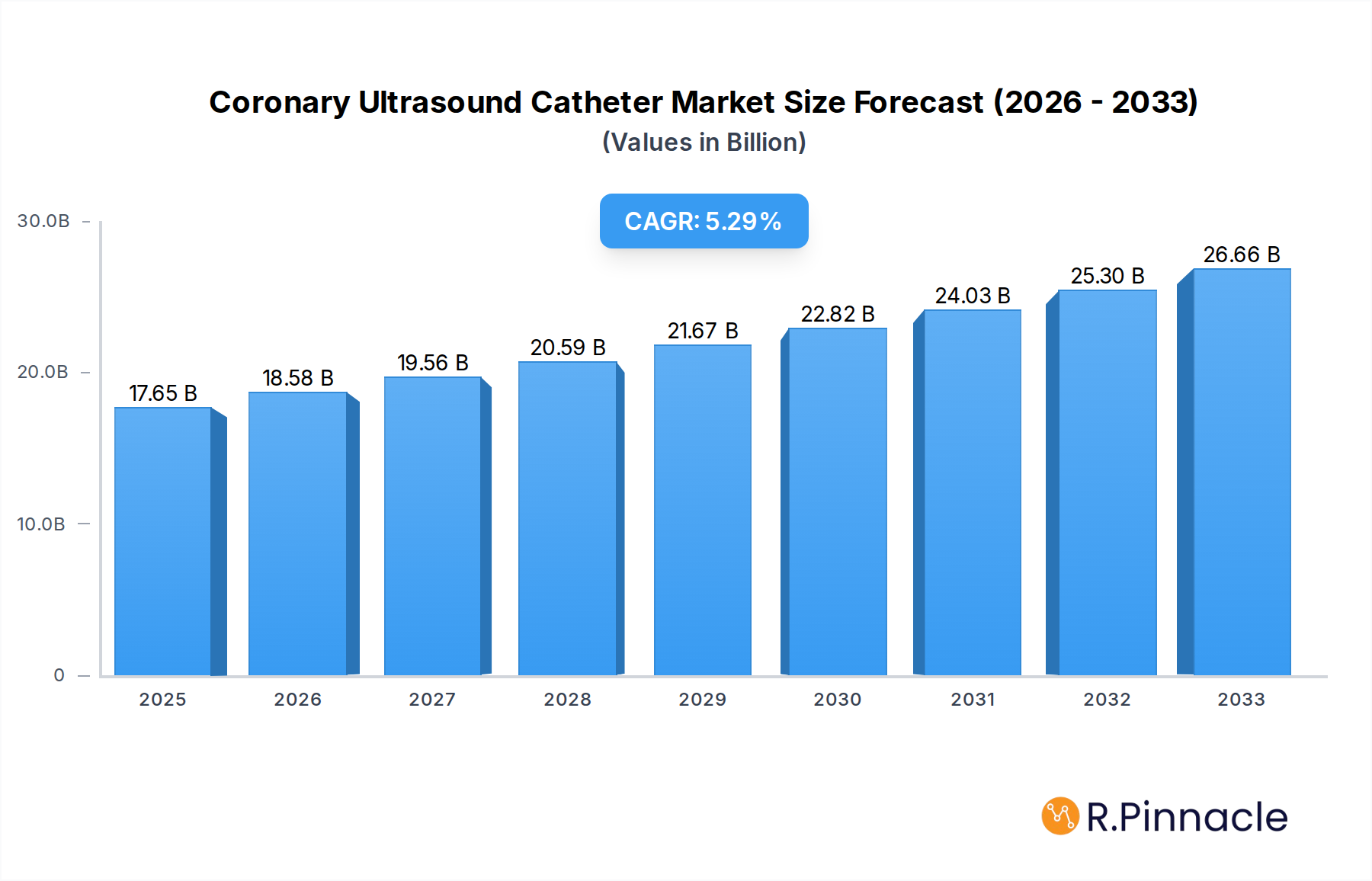

The Coronary Ultrasound Catheter market is poised for significant expansion, projected to reach $17.65 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 5.37% during the forecast period of 2025-2033. This growth is primarily fueled by the increasing prevalence of cardiovascular diseases, particularly coronary artery disease and heart valve disease. Advancements in intravascular ultrasound (IVUS) and intracardiac echocardiography (ICE) technologies are enhancing diagnostic accuracy and treatment planning, driving adoption among healthcare providers. The rising global burden of lifestyle-related illnesses, coupled with an aging population, further underpins the sustained demand for these sophisticated diagnostic tools. Furthermore, increased healthcare expenditure and a growing focus on minimally invasive procedures are contributing to market dynamism. The integration of artificial intelligence and machine learning into ultrasound imaging is also expected to revolutionize diagnostic capabilities, offering personalized patient care and improved outcomes, thus stimulating market growth.

Coronary Ultrasound Catheter Market Size (In Billion)

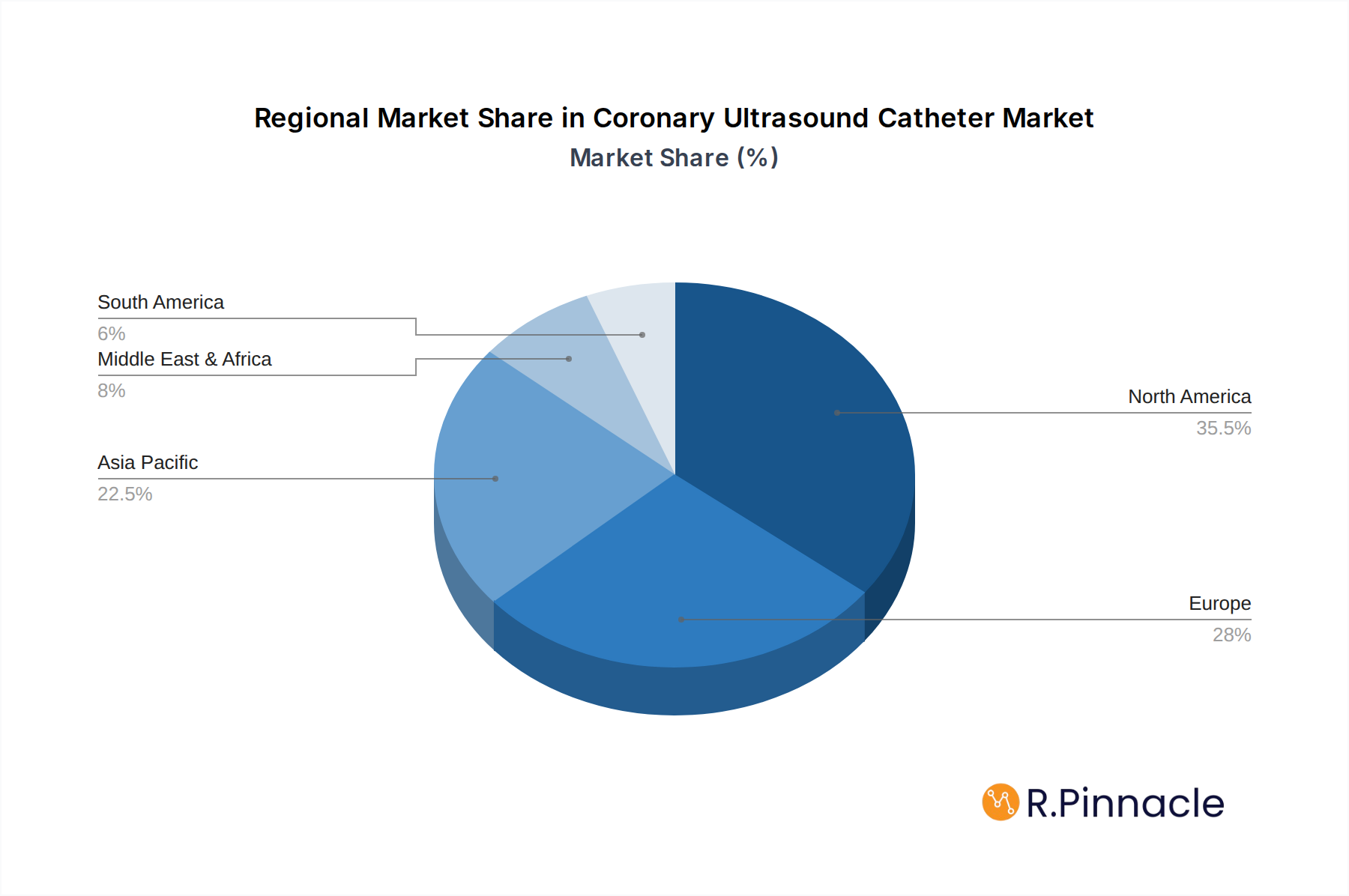

The market's upward trajectory is also being propelled by the expanding applications in arrhythmia management, where precise imaging is crucial for effective intervention. Key players like Philips Healthcare, Abbott Laboratories, and Siemens Healthineers are investing heavily in research and development to introduce innovative catheter designs and enhanced imaging software, catering to evolving clinical needs. The geographical landscape indicates a strong presence in North America and Europe, driven by advanced healthcare infrastructure and high patient awareness. However, the Asia Pacific region is anticipated to witness the fastest growth, attributed to a rapidly expanding healthcare sector, increasing disposable incomes, and a growing need for advanced cardiac diagnostics. While the market enjoys strong growth drivers, challenges such as high initial investment costs for advanced equipment and the need for specialized training for healthcare professionals may present some restraints, though these are expected to be offset by technological advancements and increasing market penetration.

Coronary Ultrasound Catheter Company Market Share

Coronary Ultrasound Catheter Market Report: Comprehensive Analysis and Future Projections (2019-2033)

This in-depth report provides a comprehensive analysis of the global Coronary Ultrasound Catheter market, encompassing historical trends, current dynamics, and future projections. Leveraging advanced analytical methodologies and extensive industry insights, this report offers critical information for stakeholders seeking to understand and capitalize on this rapidly evolving sector. The study period spans from 2019 to 2033, with a base year of 2025, and an estimated year also of 2025, followed by a forecast period from 2025 to 2033. Historical data covers the period from 2019 to 2024.

Coronary Ultrasound Catheter Market Structure & Innovation Trends

The Coronary Ultrasound Catheter market is characterized by a moderate to high level of concentration, with key players like Philips Healthcare, Abbott Laboratories, and Siemens Healthineers holding significant market share, estimated to be in the billions. Innovation remains a primary driver, fueled by advancements in imaging technology, miniaturization, and the integration of artificial intelligence for enhanced diagnostic accuracy. Regulatory frameworks, including stringent FDA and EMA approvals, play a crucial role in shaping product development and market entry strategies. Product substitutes, such as advanced MRI and CT angiography, pose a competitive challenge, necessitating continuous innovation in performance and cost-effectiveness. End-user demographics primarily include interventional cardiologists, cardiovascular surgeons, and diagnostic imaging specialists, with a growing demand from expanding healthcare infrastructures in emerging economies. Mergers and acquisition (M&A) activities are expected to be a significant trend, with estimated deal values in the billions, aimed at consolidating market presence, acquiring novel technologies, and expanding product portfolios.

Coronary Ultrasound Catheter Market Dynamics & Trends

The Coronary Ultrasound Catheter market is poised for robust growth, driven by an increasing prevalence of cardiovascular diseases (CVDs) globally. The estimated Compound Annual Growth Rate (CAGR) is projected to be robust, reaching billions by the end of the forecast period. Technological disruptions are at the forefront, with advancements in high-frequency ultrasound transducers and real-time 3D imaging significantly enhancing diagnostic capabilities. The development of integrated intravascular ultrasound (IVUS) and intracardiac echocardiography (ICE) catheters allows for simultaneous visualization and intervention, improving procedural outcomes and reducing complications. Consumer preferences are shifting towards less invasive diagnostic and therapeutic procedures, making ultrasound-guided interventions a preferred choice for cardiologists. Market penetration is steadily increasing as awareness of the benefits of these advanced imaging techniques grows among healthcare providers and patients. The competitive landscape is dynamic, with companies investing heavily in research and development to introduce next-generation catheters with superior resolution, smaller profiles, and enhanced ease of use. The integration of AI-powered image analysis and interpretation is emerging as a key differentiator, promising to optimize workflow and improve diagnostic precision. Furthermore, the growing adoption of these technologies in emerging markets, coupled with favorable reimbursement policies in developed economies, is expected to further accelerate market expansion. The increasing demand for personalized medicine and image-guided therapies will also contribute to sustained market growth, as these catheters provide invaluable anatomical and physiological information essential for tailored treatment plans. The market penetration is projected to reach billions, reflecting the widespread adoption across various healthcare settings.

Dominant Regions & Segments in Coronary Ultrasound Catheter

North America currently holds a dominant position in the Coronary Ultrasound Catheter market, driven by advanced healthcare infrastructure, high disposable incomes, and the early adoption of innovative medical technologies. The United States, in particular, is a key contributor, with a substantial number of interventional cardiology procedures performed annually. Economic policies that favor investment in cutting-edge medical devices and robust reimbursement frameworks for cardiovascular interventions further bolster this dominance. The application segment of Coronary Artery Disease (CAD) represents the largest share, owing to the high global burden of this condition and the established efficacy of ultrasound catheters in guiding interventions like percutaneous coronary intervention (PCI). Within the types, Intravascular Ultrasound (IVUS) is the most widely used, offering detailed imaging of vessel walls for plaque characterization and stent sizing, with a market size estimated in the billions.

Key drivers for regional dominance include:

- Advanced Healthcare Infrastructure: State-of-the-art hospitals and specialized cardiac centers equipped with the latest diagnostic and interventional tools.

- High Prevalence of Cardiovascular Diseases: A significant patient population with conditions like CAD and heart valve disease.

- Strong Research & Development Ecosystem: Prolific academic research and industry collaboration fostering innovation.

- Favorable Reimbursement Policies: Comprehensive insurance coverage for advanced cardiac procedures.

While North America leads, the Asia Pacific region is emerging as a high-growth market, fueled by a rapidly expanding healthcare sector, increasing awareness of cardiovascular health, and a growing middle-class population with improved access to healthcare. Countries like China and India are witnessing significant investments in cardiac care infrastructure and a surge in the demand for minimally invasive procedures. The application segment of Heart Valve Disease is also gaining traction due to an aging population and advancements in valve repair and replacement techniques, with a projected market growth in the billions. Intracardiac Echocardiography (ICE) is also witnessing increased adoption for complex structural heart interventions, contributing to its market expansion in the billions.

Coronary Ultrasound Catheter Product Innovations

Recent product innovations in the Coronary Ultrasound Catheter market focus on enhanced image resolution, miniaturization for improved deliverability in tortuous anatomy, and integrated functionalities. Companies are developing catheters with higher frequencies for finer plaque detail and advanced Doppler capabilities for precise flow assessment, providing a significant competitive advantage. Innovations also include steerable catheters with enhanced maneuverability and biocompatible materials to minimize patient trauma. The integration of AI-driven image analysis is a significant trend, enabling automated lesion characterization and measurement, thereby streamlining workflows and improving diagnostic accuracy. These advancements are crucial for addressing the growing complexity of cardiovascular interventions and improving patient outcomes, solidifying their market fit.

Report Scope & Segmentation Analysis

This report segments the Coronary Ultrasound Catheter market based on key applications and types.

Application Segments:

- Coronary Artery Disease (CAD): This segment, estimated to be in the billions, represents the largest application due to the high prevalence of atherosclerosis. Ultrasound catheters are crucial for visualizing plaque burden, guiding stent placement, and optimizing revascularization strategies. Growth is driven by increasing CVD rates and the demand for precise diagnostic tools.

- Heart Valve Disease: A significant and growing segment in the billions, driven by an aging global population and the need for accurate assessment of valve function, regurgitation, and stenosis. ICE catheters are increasingly used for guiding transcatheter valve interventions.

- Arrhythmias: This segment, with a projected market size in the billions, focuses on the use of ultrasound catheters to visualize cardiac structures involved in complex arrhythmias, aiding in ablation guidance and mapping.

Type Segments:

- Intravascular Ultrasound (IVUS): The dominant segment in the billions, IVUS catheters provide high-resolution cross-sectional imaging of coronary arteries, enabling detailed plaque analysis and measurement of lumen dimensions.

- Intracardiac Echocardiography (ICE): A rapidly growing segment in the billions, ICE catheters are inserted directly into the heart chambers, offering real-time, multi-planar imaging crucial for structural heart interventions and electrophysiology procedures.

Key Drivers of Coronary Ultrasound Catheter Growth

Several key factors are driving the growth of the Coronary Ultrasound Catheter market. Firstly, the escalating global burden of cardiovascular diseases, including coronary artery disease and heart valve disorders, necessitates advanced diagnostic and interventional tools. Secondly, continuous technological advancements in ultrasound imaging, such as miniaturization, higher resolution transducers, and AI integration, are enhancing catheter performance and utility. Thirdly, the increasing preference for minimally invasive procedures over traditional open-heart surgeries fuels the demand for less invasive diagnostic and therapeutic guidance. Fourthly, favorable reimbursement policies in developed nations and improving healthcare access in emerging economies are expanding market reach. Finally, robust investment in research and development by leading companies is fostering innovation and product differentiation, with R&D expenditure in the billions.

Challenges in the Coronary Ultrasound Catheter Sector

Despite robust growth, the Coronary Ultrasound Catheter sector faces several challenges. Stringent regulatory approval processes for new devices can lead to lengthy market entry timelines and significant development costs, impacting the speed of innovation. The high cost of these advanced catheters can be a barrier to adoption, particularly in resource-limited healthcare settings, leading to limited market penetration. Supply chain disruptions, as experienced globally, can affect the availability of critical components and finished products, impacting market stability. Furthermore, the presence of competing imaging modalities, such as CT angiography and MRI, requires continuous differentiation through superior performance and cost-effectiveness. The need for specialized training for healthcare professionals to effectively utilize these complex devices also presents an ongoing challenge, requiring substantial investment in education and skill development, potentially in the billions.

Emerging Opportunities in Coronary Ultrasound Catheter

Emerging opportunities in the Coronary Ultrasound Catheter market are abundant. The development of AI-powered diagnostic software that can automate image analysis and provide predictive insights for patient outcomes presents a significant avenue for growth. The expansion of these technologies into emerging markets, particularly in Asia Pacific and Latin America, offers vast untapped potential due to the growing prevalence of CVDs and improving healthcare infrastructure. Novel applications in areas like peripheral vascular interventions and the guidance of complex structural heart disease procedures, such as transcatheter mitral valve repair, are creating new market segments with substantial growth prospects. Furthermore, the integration of real-time imaging with therapeutic delivery systems is paving the way for more precise and effective interventions, further enhancing the value proposition of coronary ultrasound catheters, with future market potential in the billions.

Leading Players in the Coronary Ultrasound Catheter Market

- Philips Healthcare

- Avinger

- Terumo

- Abbott Laboratories

- Siemens Healthineers

- GE Healthcare

- BK Ultrasound

- Hitachi Healthcare

- Infraredx

- Boston Scientific

Key Developments in Coronary Ultrasound Catheter Industry

- 2024: Philips Healthcare launches its next-generation EPIQ CVm system with advanced IVUS capabilities, improving image quality and workflow efficiency.

- 2023: Avinger receives FDA clearance for its Lumivascular Intravascular Imaging Catheter, offering real-time plaque visualization.

- 2023: Abbott Laboratories introduces the next-generation Ultra High-Definition (UHD) IVUS catheter, enhancing resolution for better lesion assessment.

- 2022: Siemens Healthineers expands its portfolio with innovative ICE catheters designed for complex structural heart interventions.

- 2021: Terumo announces strategic partnerships to accelerate the development of AI-integrated ultrasound imaging solutions.

Future Outlook for Coronary Ultrasound Catheter Market

The future outlook for the Coronary Ultrasound Catheter market is exceptionally promising, driven by sustained innovation and increasing demand. The integration of artificial intelligence for enhanced diagnostic accuracy, predictive analytics, and streamlined procedural workflows will be a major growth accelerator. Continued miniaturization and improved maneuverability of catheters will enable their use in increasingly complex anatomical scenarios and less invasive procedures. The expansion of applications beyond traditional coronary interventions, particularly in structural heart disease and peripheral vascular imaging, will unlock new market segments. Furthermore, the growing emphasis on personalized medicine and image-guided therapies will solidify the indispensable role of coronary ultrasound catheters in modern cardiovascular care, with the global market projected to reach unprecedented valuations in the billions.

Coronary Ultrasound Catheter Segmentation

-

1. Application

- 1.1. Coronary Artery Disease

- 1.2. Heart Valve Disease

- 1.3. Arrhythmias

-

2. Types

- 2.1. Intravascular Ultrasound

- 2.2. Intracardiac Echocardiography

Coronary Ultrasound Catheter Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Coronary Ultrasound Catheter Regional Market Share

Geographic Coverage of Coronary Ultrasound Catheter

Coronary Ultrasound Catheter REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Coronary Artery Disease

- 5.1.2. Heart Valve Disease

- 5.1.3. Arrhythmias

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Intravascular Ultrasound

- 5.2.2. Intracardiac Echocardiography

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Coronary Artery Disease

- 6.1.2. Heart Valve Disease

- 6.1.3. Arrhythmias

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Intravascular Ultrasound

- 6.2.2. Intracardiac Echocardiography

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Coronary Artery Disease

- 7.1.2. Heart Valve Disease

- 7.1.3. Arrhythmias

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Intravascular Ultrasound

- 7.2.2. Intracardiac Echocardiography

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Coronary Artery Disease

- 8.1.2. Heart Valve Disease

- 8.1.3. Arrhythmias

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Intravascular Ultrasound

- 8.2.2. Intracardiac Echocardiography

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Coronary Artery Disease

- 9.1.2. Heart Valve Disease

- 9.1.3. Arrhythmias

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Intravascular Ultrasound

- 9.2.2. Intracardiac Echocardiography

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Coronary Artery Disease

- 10.1.2. Heart Valve Disease

- 10.1.3. Arrhythmias

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Intravascular Ultrasound

- 10.2.2. Intracardiac Echocardiography

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Coronary Ultrasound Catheter Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Coronary Artery Disease

- 11.1.2. Heart Valve Disease

- 11.1.3. Arrhythmias

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Intravascular Ultrasound

- 11.2.2. Intracardiac Echocardiography

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Philips Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Avinger

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Terumo

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Abbott Laboratories

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Siemens Healthineers

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GE Healthcare

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BK Ultrasound

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hitachi Healthcare

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Infraredx

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Boston Scientific

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Philips Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Coronary Ultrasound Catheter Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Coronary Ultrasound Catheter Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Coronary Ultrasound Catheter Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Coronary Ultrasound Catheter Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Coronary Ultrasound Catheter Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Coronary Ultrasound Catheter Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Coronary Ultrasound Catheter Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Coronary Ultrasound Catheter Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Coronary Ultrasound Catheter Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Coronary Ultrasound Catheter Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Coronary Ultrasound Catheter Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Coronary Ultrasound Catheter Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Coronary Ultrasound Catheter Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Coronary Ultrasound Catheter Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Coronary Ultrasound Catheter Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Coronary Ultrasound Catheter Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Coronary Ultrasound Catheter Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Coronary Ultrasound Catheter Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Coronary Ultrasound Catheter Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Coronary Ultrasound Catheter Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Coronary Ultrasound Catheter Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Coronary Ultrasound Catheter Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Coronary Ultrasound Catheter Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Coronary Ultrasound Catheter Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Coronary Ultrasound Catheter Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Coronary Ultrasound Catheter Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Coronary Ultrasound Catheter Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Coronary Ultrasound Catheter Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Coronary Ultrasound Catheter Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Coronary Ultrasound Catheter Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Coronary Ultrasound Catheter Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Coronary Ultrasound Catheter Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Coronary Ultrasound Catheter Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Coronary Ultrasound Catheter?

The projected CAGR is approximately 5.37%.

2. Which companies are prominent players in the Coronary Ultrasound Catheter?

Key companies in the market include Philips Healthcare, Avinger, Terumo, Abbott Laboratories, Siemens Healthineers, GE Healthcare, BK Ultrasound, Hitachi Healthcare, Infraredx, Boston Scientific.

3. What are the main segments of the Coronary Ultrasound Catheter?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Coronary Ultrasound Catheter," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Coronary Ultrasound Catheter report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Coronary Ultrasound Catheter?

To stay informed about further developments, trends, and reports in the Coronary Ultrasound Catheter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence