Key Insights

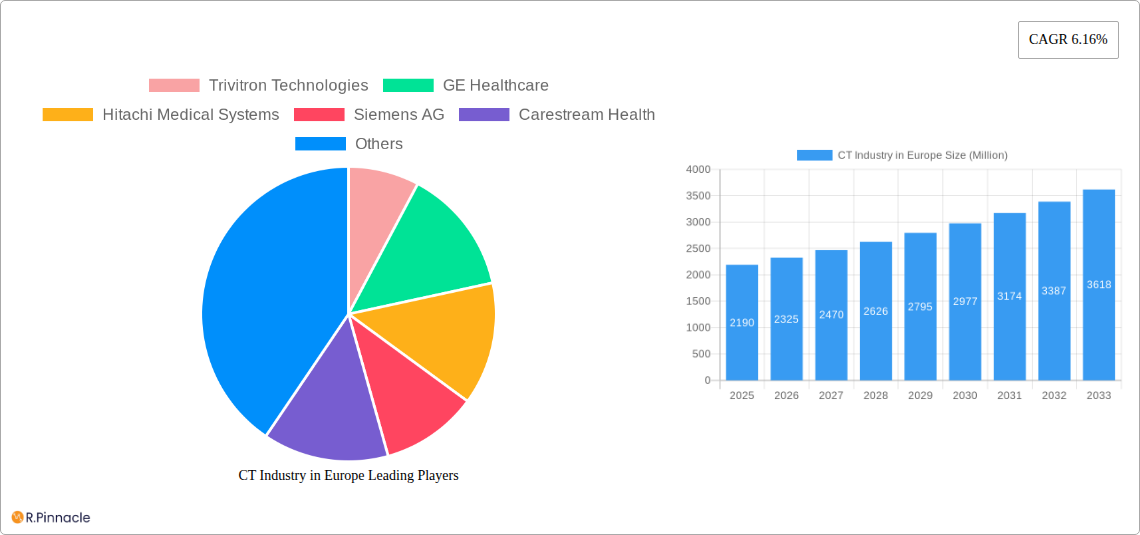

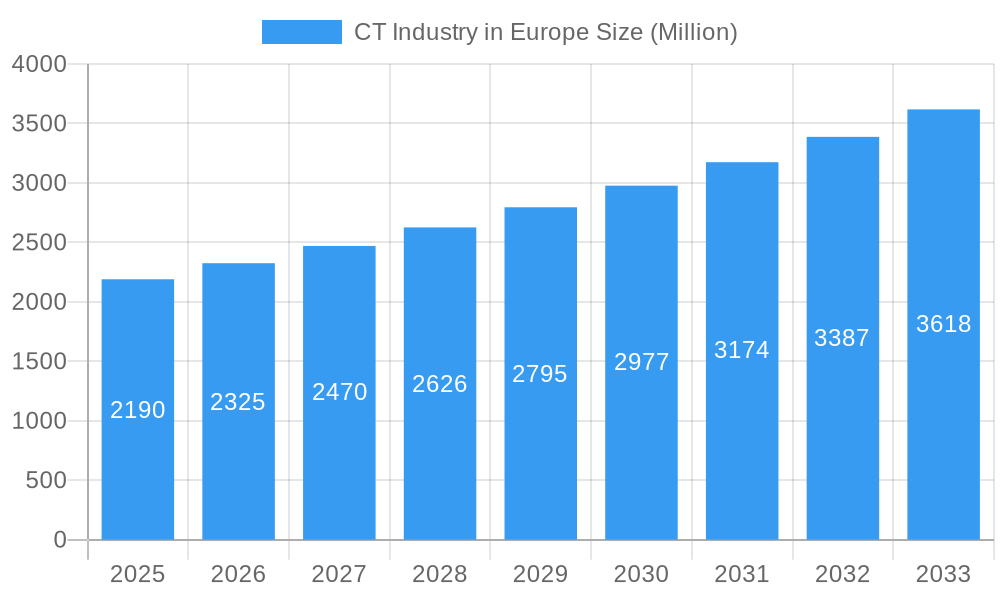

The European CT (Computed Tomography) industry is poised for substantial growth, with a **market size of *2.19* million** in the base year 2025, projected to expand at a robust Compound Annual Growth Rate (CAGR) of 6.16% through 2033. This upward trajectory is driven by several key factors, including the increasing prevalence of chronic diseases such as oncology, cardiovascular conditions, and neurological disorders, which necessitate advanced diagnostic imaging. Furthermore, technological advancements in CT scanners, such as enhanced resolution, faster scan times, and improved radiation dose reduction techniques, are stimulating demand. The growing adoption of AI-powered diagnostic solutions and the expansion of healthcare infrastructure, particularly in developing European nations, are also significant growth catalysts. The market is segmented by slice count, with medium and high-slice CT scanners likely to see increased adoption due to their superior diagnostic capabilities for complex pathologies.

CT Industry in Europe Market Size (In Billion)

The European CT market is experiencing a dynamic shift with a growing emphasis on improving diagnostic accuracy and patient outcomes. While advancements in technology and the rising disease burden are key drivers, the market also faces certain restraints, including the high capital expenditure required for advanced CT systems and concerns regarding radiation exposure. However, innovative solutions focusing on dose optimization and the increasing availability of refurbished CT scanners are helping to mitigate these challenges. Hospitals and diagnostic centers are the primary end-users, with a growing demand for integrated imaging solutions that offer seamless workflow and data management. Geographically, Western European countries like Germany and the United Kingdom are expected to maintain their leadership positions due to established healthcare systems and early adoption of new technologies, while other European regions are rapidly catching up, presenting significant growth opportunities.

CT Industry in Europe Company Market Share

This in-depth report provides a critical analysis of the CT Industry in Europe, meticulously examining its current landscape and forecasting its trajectory through 2033. Leveraging advanced analytics and extensive primary and secondary research, this report delivers actionable insights for stakeholders navigating this dynamic sector. We dissect market segmentation, explore technological innovations, and identify key growth drivers and challenges, offering a definitive resource for strategic decision-making.

CT Industry in Europe Market Structure & Innovation Trends

The CT industry in Europe exhibits a moderately concentrated market structure, dominated by a few multinational players like Siemens AG, GE Healthcare, and Koninklijke Philips NV, who collectively hold an estimated XX Million market share. Innovation is the primary catalyst, driven by advancements in detector technology, AI-powered image reconstruction, and the development of lower radiation dose protocols, all crucial for enhancing diagnostic accuracy and patient safety. Regulatory frameworks, such as those governed by the European Union Medical Device Regulation (MDR), play a significant role in shaping product development and market access, demanding rigorous adherence to quality and safety standards. While direct product substitutes are limited, alternative imaging modalities like MRI and Ultrasound continue to exert competitive pressure, particularly in specific diagnostic niches. End-user demographics are increasingly sophisticated, with hospitals and specialized diagnostic centers demanding higher throughput and more precise imaging capabilities. Mergers and acquisitions (M&A) remain a strategic tool for consolidation and market expansion, with recent deal values estimated in the range of hundreds of Million, enabling companies to acquire new technologies and broaden their product portfolios.

CT Industry in Europe Market Dynamics & Trends

The CT Industry in Europe is poised for substantial growth, driven by a confluence of factors including an aging population, increasing prevalence of chronic diseases, and a growing demand for minimally invasive diagnostic procedures. The market penetration of advanced CT technologies continues to rise, fueled by heightened awareness of early disease detection and the imperative for more accurate diagnoses. Technological disruptions are at the forefront of market evolution, with the integration of artificial intelligence (AI) revolutionizing image acquisition and analysis. AI algorithms are enhancing image clarity, reducing scan times, and enabling automated detection of abnormalities, thereby improving diagnostic efficiency and patient outcomes.

Consumer preferences are shifting towards more patient-centric solutions, emphasizing reduced radiation exposure, enhanced comfort during scans, and faster turnaround times for results. This is driving the demand for innovative CT scanner designs and advanced imaging techniques that minimize patient discomfort and potential health risks. Competitive dynamics are intensifying, with established players continuously investing in R&D to maintain their market leadership and emerging companies seeking to carve out niche segments with specialized offerings. The Compound Annual Growth Rate (CAGR) for the CT industry in Europe is estimated to be a robust XX% during the forecast period. This growth is underpinned by significant investments in healthcare infrastructure across European nations, coupled with a progressive reimbursement landscape for advanced diagnostic imaging procedures.

The increasing adoption of multi-slice CT scanners, particularly high-slice systems, is a significant trend. These advanced systems offer superior spatial resolution and faster scan times, making them indispensable for complex diagnostic scenarios in fields like oncology and cardiology. Furthermore, the growing emphasis on preventative healthcare and early disease detection strategies across European countries is directly contributing to the increased demand for CT imaging services. This proactive approach to healthcare ensures that diagnostic imaging remains a critical component of patient care pathways. The ongoing evolution of CT technology, including the development of photon-counting detectors and dual-energy CT, promises even more precise and informative imaging, further propelling market expansion. These advancements are not only improving diagnostic capabilities but also opening up new avenues for therapeutic guidance and monitoring.

Dominant Regions & Segments in CT Industry in Europe

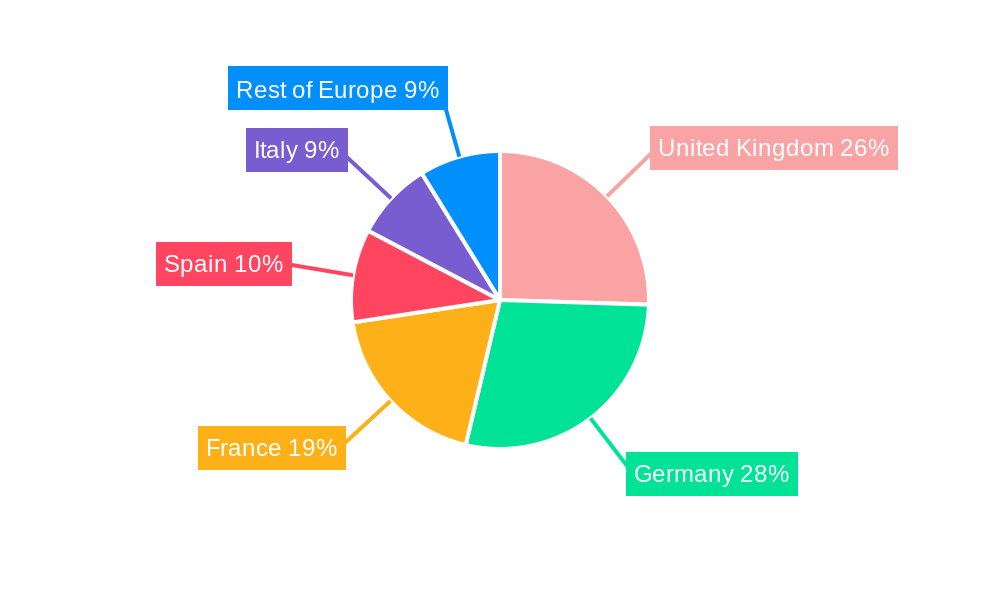

Germany stands out as the dominant region within the European CT industry, driven by its robust healthcare infrastructure, significant government investments in medical technology, and a highly skilled workforce. The country's economic policies, which prioritize healthcare innovation and accessibility, coupled with its advanced research and development capabilities, have cemented its leadership position.

- Type: The High Slice segment is experiencing the most significant growth, driven by its superior image resolution and faster scan times, crucial for complex diagnostic applications. This segment is projected to capture a substantial XX Million market share by 2033.

- Key Drivers: Advancements in detector technology, increased demand for detailed anatomical imaging in oncology and neurology, and the development of AI-powered reconstruction algorithms.

- Application: Oncology remains the largest and fastest-growing application segment. The increasing incidence of cancer across Europe and the critical role of CT in diagnosis, staging, and treatment monitoring are major contributors.

- Key Drivers: Growing cancer prevalence, demand for precise tumor localization and characterization, and the integration of CT with radiotherapy planning.

- End User: Hospitals are the primary end-users, accounting for the largest market share due to their comprehensive diagnostic capabilities and the volume of patient throughput.

- Key Drivers: High patient volumes, comprehensive diagnostic needs, and ongoing investments in advanced medical imaging equipment.

The dominance of these segments is further amplified by substantial investments in healthcare modernization across key European markets. Economic policies that encourage the adoption of cutting-edge medical technologies and a strong emphasis on public health initiatives contribute to the sustained demand for advanced CT solutions. The collaborative efforts between CT manufacturers, healthcare providers, and research institutions in Europe foster an environment of continuous innovation, ensuring that the industry remains at the forefront of diagnostic imaging advancements. This intricate interplay of economic, technological, and regulatory factors underscores the dynamism and resilience of the European CT market.

CT Industry in Europe Product Innovations

Product innovations in the European CT industry are characterized by a relentless pursuit of enhanced image quality, reduced radiation exposure, and improved workflow efficiency. Key developments include the integration of Artificial Intelligence (AI) for advanced image reconstruction and anomaly detection, significantly improving diagnostic accuracy and speed. Companies are focusing on developing multi-slice CT scanners with higher slice counts for greater detail and faster scanning times, particularly beneficial for cardiovascular and neurology applications. The introduction of low-dose CT protocols and iterative reconstruction techniques is a major stride towards patient safety. Furthermore, advancements in portable and compact CT systems are expanding accessibility in various clinical settings, including emergency rooms and remote areas, offering competitive advantages through increased versatility and cost-effectiveness.

Report Scope & Segmentation Analysis

The CT Industry in Europe is comprehensively segmented to provide granular insights into market dynamics. This report analyzes the market across three key Type segments: Low Slice, Medium Slice, and High Slice CT scanners, detailing their respective market sizes and growth trajectories. The Application segmentation includes Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications, each with distinct market drivers and future projections. The End User segmentation focuses on Hospitals, Diagnostic Centers, and Other End-Users, highlighting their unique purchasing behaviors and demands. Growth projections for each segment are meticulously calculated based on historical data and anticipated market trends, with an estimated XX Million for the total market size in 2025 and projected growth to XX Million by 2033.

Key Drivers of CT Industry in Europe Growth

The growth of the CT industry in Europe is propelled by several pivotal factors. An aging population across the continent leads to a higher incidence of age-related diseases, necessitating advanced diagnostic imaging. The increasing prevalence of chronic diseases, particularly cancer and cardiovascular conditions, directly drives the demand for CT scans for diagnosis, staging, and monitoring. Technological advancements, such as AI integration and improved detector technology, are enhancing diagnostic accuracy and efficiency, making CT imaging a preferred choice. Furthermore, favorable reimbursement policies and increasing healthcare expenditure in many European countries ensure greater accessibility to these advanced technologies. Investments in upgrading existing healthcare infrastructure and the development of specialized diagnostic centers also contribute significantly to market expansion.

Challenges in the CT Industry in Europe Sector

Despite its robust growth, the CT industry in Europe faces several challenges. Stringent regulatory frameworks, while ensuring patient safety, can also lead to lengthy approval processes and increased compliance costs for manufacturers. High initial investment costs for advanced CT systems can be a barrier for smaller healthcare providers and facilities in less developed regions. Supply chain disruptions and the scarcity of critical components can impact production and delivery timelines. Moreover, intense competition among established players and emerging technologies necessitates continuous innovation and cost management to maintain market share. The need for highly skilled personnel to operate and interpret complex CT scans also presents a workforce challenge.

Emerging Opportunities in CT Industry in Europe

Emerging opportunities in the European CT industry lie in several key areas. The increasing adoption of AI-powered diagnostic solutions presents a significant avenue for growth, promising enhanced accuracy and efficiency. The development and deployment of low-dose and ultra-low-dose CT technologies cater to the growing demand for radiation safety, particularly in pediatric and frequent screening scenarios. The expansion of mobile CT units and point-of-care diagnostic solutions can address healthcare disparities and provide imaging access in underserved areas. Furthermore, the growing focus on personalized medicine is driving demand for CT scanners capable of providing more detailed and precise anatomical and functional information for targeted therapies. Partnerships between technology providers and healthcare institutions to develop integrated diagnostic workflows also represent a significant opportunity.

Leading Players in the CT Industry in Europe Market

- Trivitron Technologies

- GE Healthcare

- Hitachi Medical Systems

- Siemens AG

- Carestream Health

- Koninklijke Philips NV

- Canon Medical Systems

- Samsung Medison

- Planmeca Group (Planmed OY)

- Koning Corporation

- Shimadzu Corporation

- Fujifilm Holdings Corporation

Key Developments in CT Industry in Europe Industry

- October 2022: GE Healthcare introduced the Omni Legend positron emission tomography/ computed tomography platform at the 36th Annual congress of the European Association of Nuclear Medicine in Barcelona, Spain, enhancing diagnostic capabilities in nuclear medicine.

- June 2022: Siemens Healthineers launched innovations in SPECT/CT imaging at the European Congress of Radiology in Germany. The company demonstrated the Symbia Prospecta, SPECT/CT system with CE mark clearance that has advanced in imaging technologies, offering improved diagnostic performance.

Future Outlook for CT Industry in Europe Market

The future outlook for the CT Industry in Europe is exceptionally promising, driven by sustained demand for advanced diagnostic imaging and continuous technological innovation. The increasing integration of AI is expected to revolutionize image analysis and workflow efficiency, leading to faster and more accurate diagnoses. The development of next-generation CT scanners with even lower radiation doses and higher resolution will cater to the growing emphasis on patient safety and precision medicine. Expansion into emerging markets within Europe and the adoption of more cost-effective solutions will broaden market access. Strategic collaborations and partnerships will remain crucial for driving innovation and addressing complex healthcare challenges. The market is projected to witness significant growth, fueled by an aging population, rising chronic disease rates, and ongoing investments in healthcare infrastructure, creating substantial opportunities for stakeholders in the coming years.

CT Industry in Europe Segmentation

-

1. Type

- 1.1. Low Slice

- 1.2. Medium Slice

- 1.3. High Slice

-

2. Application

- 2.1. Oncology

- 2.2. Neurology

- 2.3. Cardiovascular

- 2.4. Musculoskeletal

- 2.5. Other Applications

-

3. End User

- 3.1. Hospitals

- 3.2. Diagnostic Centers

- 3.3. Other End-Users

CT Industry in Europe Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. France

- 4. Spain

- 5. Italy

- 6. Rest of Europe

CT Industry in Europe Regional Market Share

Geographic Coverage of CT Industry in Europe

CT Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Incidence of Cancer & Chronic Diseases; Advancement in Technology

- 3.3. Market Restrains

- 3.3.1. Expensive Procedures and Instruments; Stringent Regulatory Framework

- 3.4. Market Trends

- 3.4.1. Oncology Segment is Expected to Hold the Largest Market Share in the European CT Market Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Low Slice

- 5.1.2. Medium Slice

- 5.1.3. High Slice

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Oncology

- 5.2.2. Neurology

- 5.2.3. Cardiovascular

- 5.2.4. Musculoskeletal

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Diagnostic Centers

- 5.3.3. Other End-Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Kingdom

- 5.4.2. Germany

- 5.4.3. France

- 5.4.4. Spain

- 5.4.5. Italy

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United Kingdom CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Low Slice

- 6.1.2. Medium Slice

- 6.1.3. High Slice

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Oncology

- 6.2.2. Neurology

- 6.2.3. Cardiovascular

- 6.2.4. Musculoskeletal

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Diagnostic Centers

- 6.3.3. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Germany CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Low Slice

- 7.1.2. Medium Slice

- 7.1.3. High Slice

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Oncology

- 7.2.2. Neurology

- 7.2.3. Cardiovascular

- 7.2.4. Musculoskeletal

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Diagnostic Centers

- 7.3.3. Other End-Users

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Low Slice

- 8.1.2. Medium Slice

- 8.1.3. High Slice

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Oncology

- 8.2.2. Neurology

- 8.2.3. Cardiovascular

- 8.2.4. Musculoskeletal

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Diagnostic Centers

- 8.3.3. Other End-Users

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Spain CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Low Slice

- 9.1.2. Medium Slice

- 9.1.3. High Slice

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Oncology

- 9.2.2. Neurology

- 9.2.3. Cardiovascular

- 9.2.4. Musculoskeletal

- 9.2.5. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Diagnostic Centers

- 9.3.3. Other End-Users

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Italy CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Low Slice

- 10.1.2. Medium Slice

- 10.1.3. High Slice

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Oncology

- 10.2.2. Neurology

- 10.2.3. Cardiovascular

- 10.2.4. Musculoskeletal

- 10.2.5. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Diagnostic Centers

- 10.3.3. Other End-Users

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Europe CT Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Low Slice

- 11.1.2. Medium Slice

- 11.1.3. High Slice

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Oncology

- 11.2.2. Neurology

- 11.2.3. Cardiovascular

- 11.2.4. Musculoskeletal

- 11.2.5. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Diagnostic Centers

- 11.3.3. Other End-Users

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2025

- 12.2. Company Profiles

- 12.2.1 Trivitron Technologies

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 GE Healthcare

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Hitachi Medical Systems

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Siemens AG

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Carestream Health

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Koninklijke Philips NV

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Canon Medical Systems

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Samsung Medison

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Planmeca Group (Planmed OY)

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Koning Corporation

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.11 Shimadzu Corporation

- 12.2.11.1. Overview

- 12.2.11.2. Products

- 12.2.11.3. SWOT Analysis

- 12.2.11.4. Recent Developments

- 12.2.11.5. Financials (Based on Availability)

- 12.2.12 Fujifilm Holdings Corporation

- 12.2.12.1. Overview

- 12.2.12.2. Products

- 12.2.12.3. SWOT Analysis

- 12.2.12.4. Recent Developments

- 12.2.12.5. Financials (Based on Availability)

- 12.2.1 Trivitron Technologies

List of Figures

- Figure 1: CT Industry in Europe Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: CT Industry in Europe Share (%) by Company 2025

List of Tables

- Table 1: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 2: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 3: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 4: CT Industry in Europe Revenue Million Forecast, by Region 2020 & 2033

- Table 5: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 6: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 7: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 8: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 9: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 10: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 11: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 12: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 13: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 14: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 15: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 16: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 17: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 18: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 19: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 20: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 21: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 22: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 23: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 24: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 25: CT Industry in Europe Revenue Million Forecast, by Type 2020 & 2033

- Table 26: CT Industry in Europe Revenue Million Forecast, by Application 2020 & 2033

- Table 27: CT Industry in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 28: CT Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the CT Industry in Europe?

The projected CAGR is approximately 6.16%.

2. Which companies are prominent players in the CT Industry in Europe?

Key companies in the market include Trivitron Technologies, GE Healthcare, Hitachi Medical Systems, Siemens AG, Carestream Health, Koninklijke Philips NV, Canon Medical Systems, Samsung Medison, Planmeca Group (Planmed OY), Koning Corporation, Shimadzu Corporation, Fujifilm Holdings Corporation.

3. What are the main segments of the CT Industry in Europe?

The market segments include Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.19 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidence of Cancer & Chronic Diseases; Advancement in Technology.

6. What are the notable trends driving market growth?

Oncology Segment is Expected to Hold the Largest Market Share in the European CT Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Expensive Procedures and Instruments; Stringent Regulatory Framework.

8. Can you provide examples of recent developments in the market?

October 2022: GE Healthcare introduced Omni Legend positron emission tomography/ computed tomography platform at the 36th Annual congress of the European Association of Nuclear Medicine in Barcelona, Spain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "CT Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the CT Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the CT Industry in Europe?

To stay informed about further developments, trends, and reports in the CT Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence