Key Insights

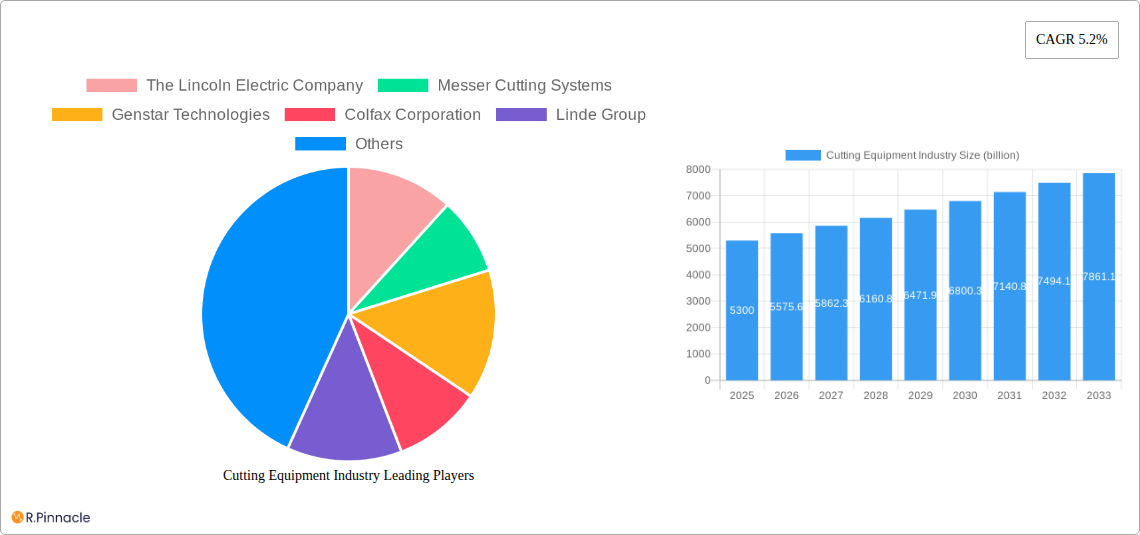

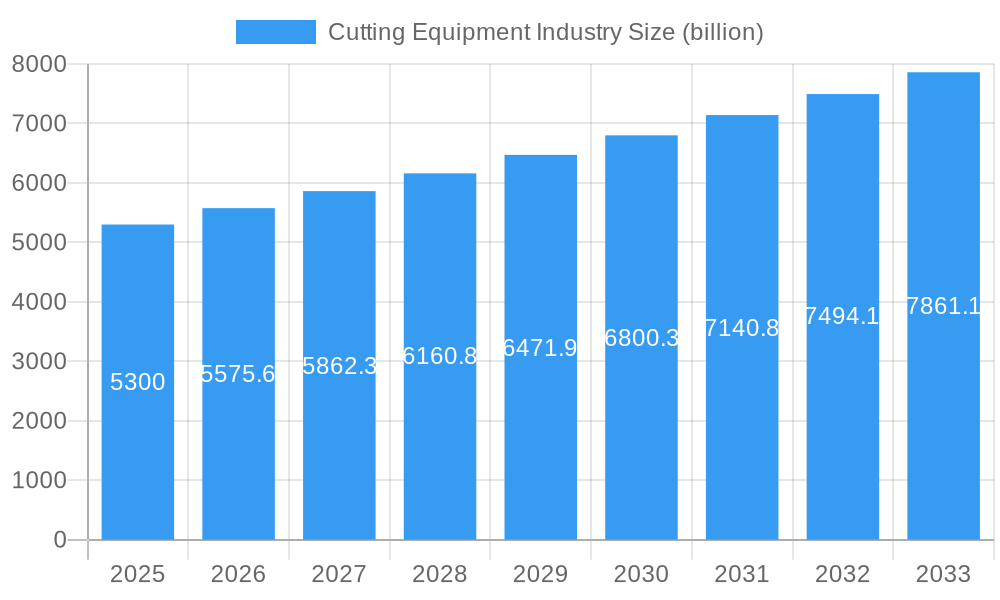

The global cutting equipment market is projected to reach an estimated $5.3 billion in 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 5.2% throughout the forecast period of 2025-2033. This significant growth is propelled by a confluence of factors, including the escalating demand for precision and efficiency across various industrial sectors. The automotive industry, driven by advancements in vehicle manufacturing and the increasing adoption of lightweight materials, is a primary consumer of sophisticated cutting solutions. Similarly, the aerospace and defense sector's continuous need for high-performance components fabricated with utmost accuracy fuels market expansion. Furthermore, the burgeoning electrical and electronics industry, characterized by miniaturization and complex designs, also contributes substantially to the demand for advanced cutting technologies. The construction sector, with its ongoing infrastructure development and renovation projects, further underpins this growth trajectory.

Cutting Equipment Industry Market Size (In Billion)

Technological innovation is a key driver, with advancements in laser, plasma, and waterjet cutting technologies offering superior speed, precision, and versatility compared to traditional methods like flame cutting. These technologies are enabling manufacturers to achieve intricate designs, reduce material waste, and enhance overall productivity. Emerging trends such as the integration of automation and artificial intelligence in cutting processes are also shaping the market landscape, promising further optimization and cost savings. While the market enjoys strong growth, potential restraints could emerge from the high initial investment costs associated with advanced cutting machinery and fluctuating raw material prices. Nevertheless, the persistent drive for enhanced manufacturing capabilities and the expanding application spectrum of cutting equipment across diverse industries suggest a dynamic and promising future for this market.

Cutting Equipment Industry Company Market Share

This in-depth report provides a definitive analysis of the global cutting equipment market, spanning a historical period of 2019–2024 and a forecast period of 2025–2033, with a base and estimated year of 2025. We delve into the intricacies of market structure, dynamics, dominant regions, and technological innovations, offering actionable insights for industry professionals. The report leverages high-ranking keywords to ensure maximum search visibility and targets key decision-makers within the cutting equipment, industrial machinery, metal fabrication, automation solutions, and advanced manufacturing sectors. We project the global market to reach billions in valuation by 2033, driven by increasing demand across various end-user industries.

Cutting Equipment Industry Market Structure & Innovation Trends

The cutting equipment industry exhibits a moderately concentrated market structure, with a few dominant players like TRUMPF GmbH + Co KG, Bystronic Laser AG, and Hypertherm holding significant market share in high-value segments such as laser and plasma cutting. The overall market valuation is estimated to be in the tens of billions, with M&A activities contributing billions in deal values as companies aim to expand their technological portfolios and geographic reach. Innovation is primarily driven by advancements in automation, digitalization, and the development of more precise and efficient cutting technologies like fiber laser cutting and high-definition plasma. Regulatory frameworks, particularly those related to environmental impact and safety standards, are increasingly influencing product development and market entry. Substitutes, such as manual cutting tools and older technologies, are steadily being replaced by automated solutions, especially in high-volume manufacturing environments. End-user demographics are shifting towards industries demanding higher precision, faster throughput, and greater flexibility, such as aerospace and defense and automotive. Key players are strategically investing in R&D and acquisitions to maintain a competitive edge and capture emerging market opportunities.

Cutting Equipment Industry Market Dynamics & Trends

The global cutting equipment market is experiencing robust growth, projected to witness a significant Compound Annual Growth Rate (CAGR) of approximately xx% from 2025 to 2033. This expansion is underpinned by a confluence of powerful market growth drivers, chief among them being the escalating adoption of advanced manufacturing technologies across diverse industries. The relentless pursuit of enhanced productivity, improved operational efficiency, and superior product quality by businesses worldwide fuels the demand for cutting-edge cutting solutions. Technological disruptions are at the forefront of this market evolution. The rise of Industry 4.0 principles, including the integration of AI, IoT, and robotics, is revolutionizing the capabilities of cutting equipment. Smart, connected machines offer real-time data analytics, predictive maintenance, and remote operational control, significantly boosting uptime and reducing costs. Furthermore, the miniaturization and increased power efficiency of technologies like fiber lasers are making them more accessible and versatile, penetrating even niche applications.

Consumer preferences are increasingly leaning towards solutions that offer greater precision, faster cutting speeds, and the ability to handle a wider range of materials. This demand surge is particularly evident in sectors like automotive, where complex designs and lightweight materials necessitate advanced cutting techniques, and aerospace and defense, where stringent quality and safety standards are paramount. The electrical and electronics sector also contributes significantly to market growth, driven by the need for intricate and precise cutting in the manufacturing of components.

The competitive landscape is characterized by intense innovation and strategic alliances. Established players are continually investing in R&D to develop next-generation cutting technologies, while new entrants are emerging with specialized solutions. Mergers and acquisitions are common as companies seek to consolidate market share, acquire proprietary technologies, and expand their global footprint. Market penetration for advanced cutting technologies is steadily increasing, displacing traditional methods and creating new avenues for growth. The ongoing drive towards automation and the need for cost-effective, high-volume production are key factors propelling the overall market forward. The trend towards customized and on-demand manufacturing also necessitates flexible and adaptable cutting solutions, further stimulating market dynamics.

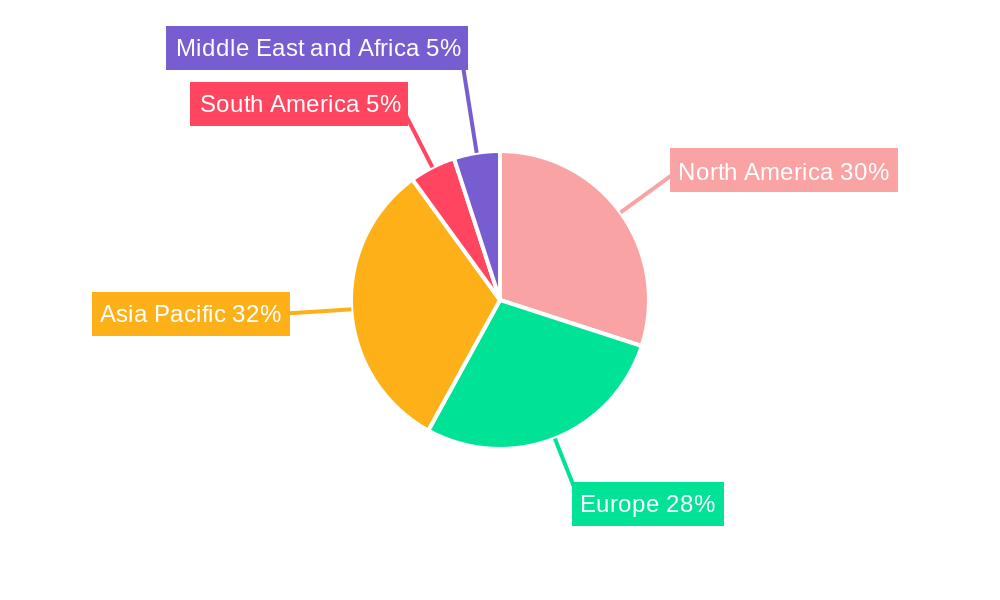

Dominant Regions & Segments in Cutting Equipment Industry

The Asia-Pacific region stands as the dominant force in the global cutting equipment market, driven by its robust manufacturing base, burgeoning industrialization, and significant investments in advanced technologies. Countries like China and India are experiencing rapid economic growth, leading to increased demand for cutting equipment across various sectors, including automotive, construction, and electrical and electronics. Favorable government policies supporting manufacturing and industrial development further bolster the region's dominance.

Within the technology segments, Laser cutting equipment is leading the market, owing to its unparalleled precision, speed, and versatility in cutting a wide array of materials, from thin sheets to thick plates. The continuous innovation in fiber laser technology, offering higher efficiency and lower operating costs, has significantly accelerated its adoption. The Automotive end-user segment is also a major contributor to market growth. The increasing complexity of vehicle designs, the demand for lightweight materials, and the trend towards electric vehicles all necessitate advanced cutting solutions for components like chassis, body panels, and battery casings.

Key drivers contributing to the dominance of these regions and segments include:

- Economic Policies: Government initiatives promoting industrial automation, manufacturing upgrades, and export-oriented growth strategies in regions like Asia-Pacific significantly boost demand for cutting equipment.

- Infrastructure Development: Large-scale infrastructure projects in emerging economies require substantial quantities of fabricated metal components, driving the demand for efficient cutting solutions.

- Technological Advancements: Continuous innovation in laser, plasma, and waterjet technologies, leading to increased precision, speed, and cost-effectiveness, is a primary growth accelerator.

- Demand from Key End-Users: The automotive sector's push for lighter, more fuel-efficient vehicles, the aerospace industry's need for high-strength, intricate parts, and the electronics sector's demand for miniaturization are powerful market drivers.

- Skilled Workforce Availability: In developed regions, a skilled workforce adept at operating and maintaining advanced cutting machinery facilitates the adoption of sophisticated technologies.

- Supply Chain Efficiencies: The presence of a well-established supply chain for raw materials and components, coupled with efficient logistics, supports the widespread availability and adoption of cutting equipment.

The Aerospace and Defense sector, while smaller in volume compared to automotive, represents a high-value segment due to the stringent requirements for precision, material integrity, and compliance with safety regulations. The Construction industry also presents substantial opportunities, particularly with the increasing use of pre-fabricated components and structural steel.

Cutting Equipment Industry Product Innovations

The cutting equipment industry is witnessing a wave of product innovations centered on enhancing efficiency, precision, and automation. Companies are heavily investing in AI-driven cutting path optimization, advanced sensor integration for real-time quality control, and the development of multi-process machines capable of performing welding, marking, and cutting functions. The advent of ultra-high-power fiber lasers is enabling faster cutting speeds and the ability to process thicker materials, expanding applications in heavy industries. Innovations in waterjet cutting are focusing on higher pressures and advanced nozzle designs for improved edge quality and reduced kerf width. Plasma cutting is evolving with improved gas control and arc stability for cleaner cuts and reduced post-processing. These technological advancements offer significant competitive advantages by improving throughput, reducing waste, and enabling the fabrication of more complex designs across diverse end-user industries.

Report Scope & Segmentation Analysis

This report meticulously segments the cutting equipment market by technology and end-user applications. The technology segmentation includes Laser cutting, Plasma cutting, Waterjet cutting, Flame cutting, and Other Technologies such as mechanical shearing and abrasive cutting. The end-user segmentation encompasses Automotive, Aerospace and Defense, Electrical and Electronics, Construction, and Other End-Users including general manufacturing, metal fabrication, and shipbuilding.

- Laser Cutting: This segment is projected to exhibit the highest growth rate, driven by advancements in fiber laser technology and its widespread adoption in high-precision applications. Market size is expected to reach billions by 2033.

- Plasma Cutting: This segment will continue to hold a substantial market share, fueled by its cost-effectiveness for medium-thickness materials and ongoing technological improvements.

- Waterjet Cutting: Characterized by its ability to cut virtually any material without thermal distortion, waterjet cutting is expected to see steady growth, particularly in specialized industries like aerospace and medical devices.

- Flame Cutting: While a mature technology, flame cutting will remain relevant for heavy fabrication and structural steel applications, albeit with slower growth projections compared to other segments.

- Automotive: This end-user segment will remain a key revenue driver, with increasing demand for advanced cutting solutions for new vehicle architectures and lightweighting initiatives.

- Aerospace and Defense: This segment, though smaller in volume, offers high-value opportunities due to the stringent precision and material integrity requirements.

- Electrical and Electronics: The miniaturization and increasing complexity of electronic components will drive demand for precise and efficient cutting technologies.

- Construction: Growth in infrastructure development and pre-fabricated construction will boost the demand for cutting equipment in this sector.

Key Drivers of Cutting Equipment Industry Growth

The cutting equipment industry's growth trajectory is propelled by several interconnected factors. The relentless pursuit of automation and efficiency across manufacturing sectors is a primary driver, as businesses seek to optimize production processes, reduce labor costs, and enhance throughput. Continuous technological advancements, particularly in laser, plasma, and waterjet technologies, are creating more precise, faster, and versatile cutting solutions, thereby expanding their application scope. The growing demand for high-precision components in industries like aerospace, automotive, and electronics necessitates sophisticated cutting equipment. Furthermore, increasing government investments in manufacturing infrastructure and supportive policies aimed at boosting industrial output in emerging economies are significantly fueling market expansion. The trend towards lightweighting in vehicles and aircraft also drives the adoption of advanced cutting techniques for specialized materials.

Challenges in the Cutting Equipment Industry Sector

Despite its robust growth, the cutting equipment industry faces several challenges. High initial investment costs for advanced cutting machinery can be a barrier for small and medium-sized enterprises (SMEs). The shortage of skilled labor capable of operating and maintaining these complex machines poses a significant restraint on adoption and operational efficiency. Supply chain disruptions and fluctuations in raw material prices can impact manufacturing costs and lead times. Intensifying competition from both established players and new entrants can lead to price pressures and necessitate continuous innovation to maintain market share. Furthermore, stringent environmental regulations regarding energy consumption and emissions require manufacturers to invest in more sustainable and energy-efficient technologies, which can add to development costs. The rapid pace of technological change also requires companies to constantly adapt and upgrade their offerings, posing a challenge to maintain a competitive edge.

Emerging Opportunities in Cutting Equipment Industry

The cutting equipment industry is ripe with emerging opportunities driven by evolving market demands and technological breakthroughs. The increasing adoption of Industry 4.0 and smart manufacturing principles presents significant opportunities for intelligent, connected cutting systems with advanced data analytics and predictive maintenance capabilities. The growing demand for additive manufacturing (3D printing) is creating complementary opportunities for advanced cutting technologies in post-processing and finishing. The expansion of renewable energy sectors, such as solar and wind power, requires specialized cutting solutions for large components and structural elements. The growing trend of customization and on-demand manufacturing favors flexible and agile cutting systems. Furthermore, the development of new materials and composites in industries like aerospace and automotive will drive the need for innovative cutting solutions capable of handling these advanced substances. The global push towards sustainability also opens avenues for energy-efficient and waste-reducing cutting technologies.

Leading Players in the Cutting Equipment Industry Market

- The Lincoln Electric Company

- Messer Cutting Systems

- Genstar Technologies

- Colfax Corporation

- Linde Group

- Struers

- Ador Welding Ltd

- GCE Group

- DAIHEN Corporation

- Hypertherm

- Amada Miyachi

- Koike Aronson Inc

- Kennametal

- TRUMPF GmbH + Co KG

- Bystronic Laser AG

Key Developments in Cutting Equipment Industry Industry

- July 2022: Lincoln Electric has introduced the POWER MIG 215 MPi multi-process welder, a lightweight dual-input voltage machine with a new ergonomic design. This development caters to the increasing demand for versatile and user-friendly welding and cutting solutions.

- February 2022: Messer Cutting Systems acquired the US-American manufacturer of products in the oxyfuel sector, Flame Technologies, Inc. (Flame Tech) through an affiliate company. With Flame Tech, Messer Cutting Systems strengthens its position as an international solution provider of Oxyfuel, Steel Mill, and pre-heating solutions. This strategic acquisition expands Messer's product portfolio and market reach in the oxyfuel segment.

Future Outlook for Cutting Equipment Industry Market

The future outlook for the cutting equipment industry is exceptionally promising, driven by sustained global industrial growth and accelerating technological innovation. The ongoing digital transformation within manufacturing, coupled with the imperative for enhanced efficiency and precision, will continue to fuel demand for advanced cutting solutions. Emerging markets are poised for significant growth as they adopt modern manufacturing practices. Opportunities abound in the development of smarter, more autonomous cutting systems integrated with AI and IoT capabilities. The increasing focus on sustainability and energy efficiency will drive the adoption of greener technologies. Strategic partnerships, R&D investments in novel materials and cutting methods, and a proactive approach to addressing the skills gap will be crucial for companies looking to capitalize on the expanding market potential and secure long-term competitive advantages in this dynamic industry.

Cutting Equipment Industry Segmentation

-

1. Technology

- 1.1. Laser

- 1.2. Plasma

- 1.3. Waterjet

- 1.4. Flame

- 1.5. Other Technologies

-

2. End-user

- 2.1. Automotive

- 2.2. Aerospace and Defense

- 2.3. Electrical and Electronics

- 2.4. Construction

- 2.5. Other End-Users

Cutting Equipment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. UAE

- 5.2. Saudi Arabia

- 5.3. Egypt

- 5.4. South Africa

- 5.5. Rest of Middle East and Africa

Cutting Equipment Industry Regional Market Share

Geographic Coverage of Cutting Equipment Industry

Cutting Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Laser

- 5.1.2. Plasma

- 5.1.3. Waterjet

- 5.1.4. Flame

- 5.1.5. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by End-user

- 5.2.1. Automotive

- 5.2.2. Aerospace and Defense

- 5.2.3. Electrical and Electronics

- 5.2.4. Construction

- 5.2.5. Other End-Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Cutting Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Laser

- 6.1.2. Plasma

- 6.1.3. Waterjet

- 6.1.4. Flame

- 6.1.5. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by End-user

- 6.2.1. Automotive

- 6.2.2. Aerospace and Defense

- 6.2.3. Electrical and Electronics

- 6.2.4. Construction

- 6.2.5. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Cutting Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Laser

- 7.1.2. Plasma

- 7.1.3. Waterjet

- 7.1.4. Flame

- 7.1.5. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by End-user

- 7.2.1. Automotive

- 7.2.2. Aerospace and Defense

- 7.2.3. Electrical and Electronics

- 7.2.4. Construction

- 7.2.5. Other End-Users

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Cutting Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Laser

- 8.1.2. Plasma

- 8.1.3. Waterjet

- 8.1.4. Flame

- 8.1.5. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by End-user

- 8.2.1. Automotive

- 8.2.2. Aerospace and Defense

- 8.2.3. Electrical and Electronics

- 8.2.4. Construction

- 8.2.5. Other End-Users

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Cutting Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Laser

- 9.1.2. Plasma

- 9.1.3. Waterjet

- 9.1.4. Flame

- 9.1.5. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by End-user

- 9.2.1. Automotive

- 9.2.2. Aerospace and Defense

- 9.2.3. Electrical and Electronics

- 9.2.4. Construction

- 9.2.5. Other End-Users

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. South America Cutting Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Laser

- 10.1.2. Plasma

- 10.1.3. Waterjet

- 10.1.4. Flame

- 10.1.5. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by End-user

- 10.2.1. Automotive

- 10.2.2. Aerospace and Defense

- 10.2.3. Electrical and Electronics

- 10.2.4. Construction

- 10.2.5. Other End-Users

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East and Africa Cutting Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Laser

- 11.1.2. Plasma

- 11.1.3. Waterjet

- 11.1.4. Flame

- 11.1.5. Other Technologies

- 11.2. Market Analysis, Insights and Forecast - by End-user

- 11.2.1. Automotive

- 11.2.2. Aerospace and Defense

- 11.2.3. Electrical and Electronics

- 11.2.4. Construction

- 11.2.5. Other End-Users

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 The Lincoln Electric Company

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Messer Cutting Systems

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Genstar Technologies

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Colfax Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Linde Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Struers

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ador Welding Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GCE Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DAIHEN Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hypertherm

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Amada Miyachi

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Koike Aronson Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Kennametal

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 TRUMPF GmbH + Co KG

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Bystronic Laser AG**List Not Exhaustive

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 The Lincoln Electric Company

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cutting Equipment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Cutting Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 3: North America Cutting Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Cutting Equipment Industry Revenue (billion), by End-user 2025 & 2033

- Figure 5: North America Cutting Equipment Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 6: North America Cutting Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Cutting Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Cutting Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 9: Europe Cutting Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Cutting Equipment Industry Revenue (billion), by End-user 2025 & 2033

- Figure 11: Europe Cutting Equipment Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 12: Europe Cutting Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Cutting Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Cutting Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 15: Asia Pacific Cutting Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Pacific Cutting Equipment Industry Revenue (billion), by End-user 2025 & 2033

- Figure 17: Asia Pacific Cutting Equipment Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 18: Asia Pacific Cutting Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Cutting Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Cutting Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 21: South America Cutting Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: South America Cutting Equipment Industry Revenue (billion), by End-user 2025 & 2033

- Figure 23: South America Cutting Equipment Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 24: South America Cutting Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Cutting Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Cutting Equipment Industry Revenue (billion), by Technology 2025 & 2033

- Figure 27: Middle East and Africa Cutting Equipment Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Middle East and Africa Cutting Equipment Industry Revenue (billion), by End-user 2025 & 2033

- Figure 29: Middle East and Africa Cutting Equipment Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 30: Middle East and Africa Cutting Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Cutting Equipment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 3: Global Cutting Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 5: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 6: Global Cutting Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 11: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 12: Global Cutting Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Russia Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 20: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 21: Global Cutting Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: India Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Japan Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: South Korea Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 28: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 29: Global Cutting Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Brazil Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Argentina Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Rest of South America Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Global Cutting Equipment Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 34: Global Cutting Equipment Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 35: Global Cutting Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: UAE Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Saudi Arabia Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Egypt Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: South Africa Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Middle East and Africa Cutting Equipment Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cutting Equipment Industry?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Cutting Equipment Industry?

Key companies in the market include The Lincoln Electric Company, Messer Cutting Systems, Genstar Technologies, Colfax Corporation, Linde Group, Struers, Ador Welding Ltd, GCE Group, DAIHEN Corporation, Hypertherm, Amada Miyachi, Koike Aronson Inc, Kennametal, TRUMPF GmbH + Co KG, Bystronic Laser AG**List Not Exhaustive.

3. What are the main segments of the Cutting Equipment Industry?

The market segments include Technology, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.3 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Positive Outlook for the Automotive Industry.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

July 2022 - Lincoln Electric has introduced the POWER MIG 215 MPi multi-process welder, a lightweight dual-input voltage machine with a new ergonomic design.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cutting Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cutting Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cutting Equipment Industry?

To stay informed about further developments, trends, and reports in the Cutting Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence