Key Insights

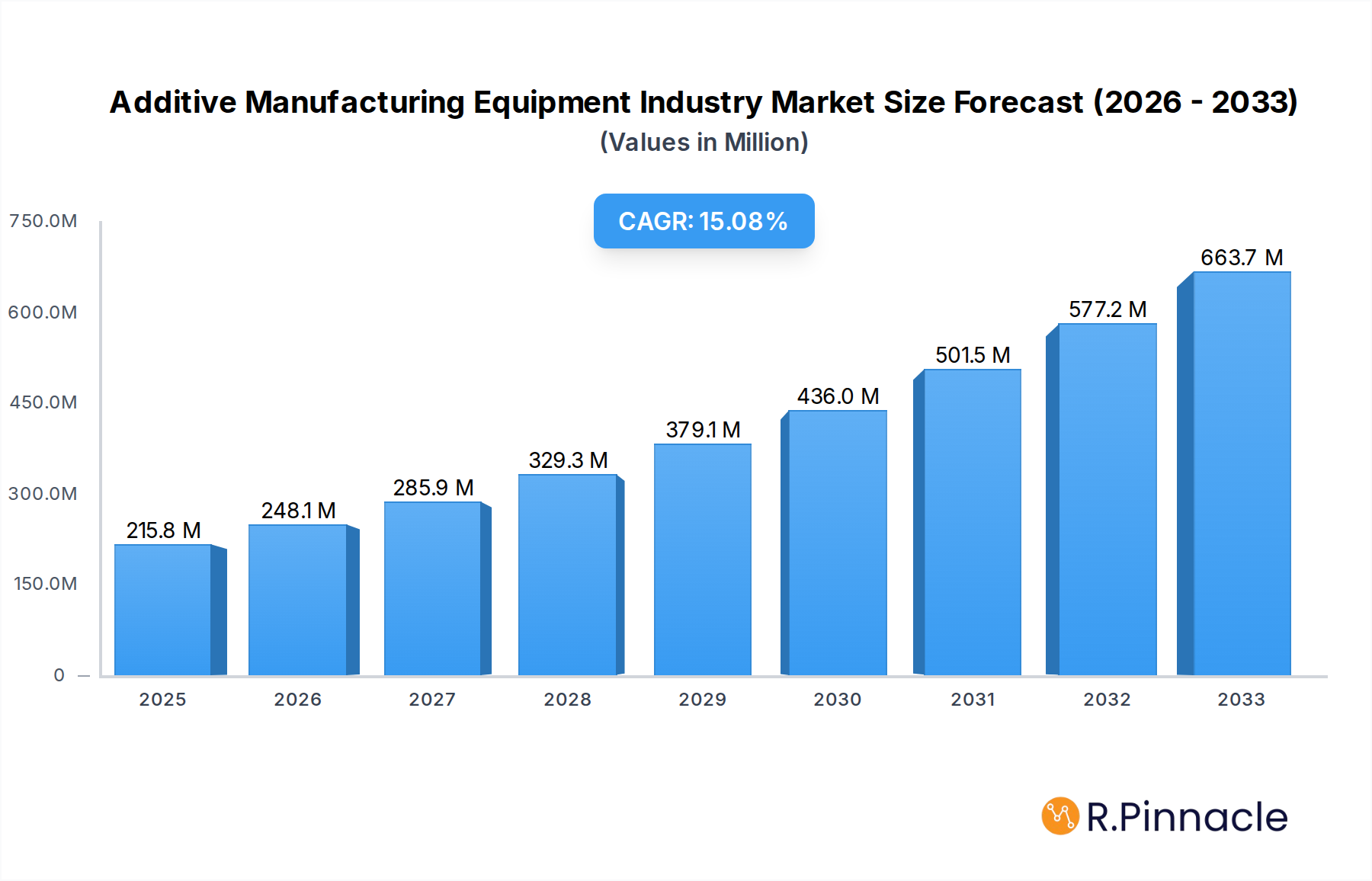

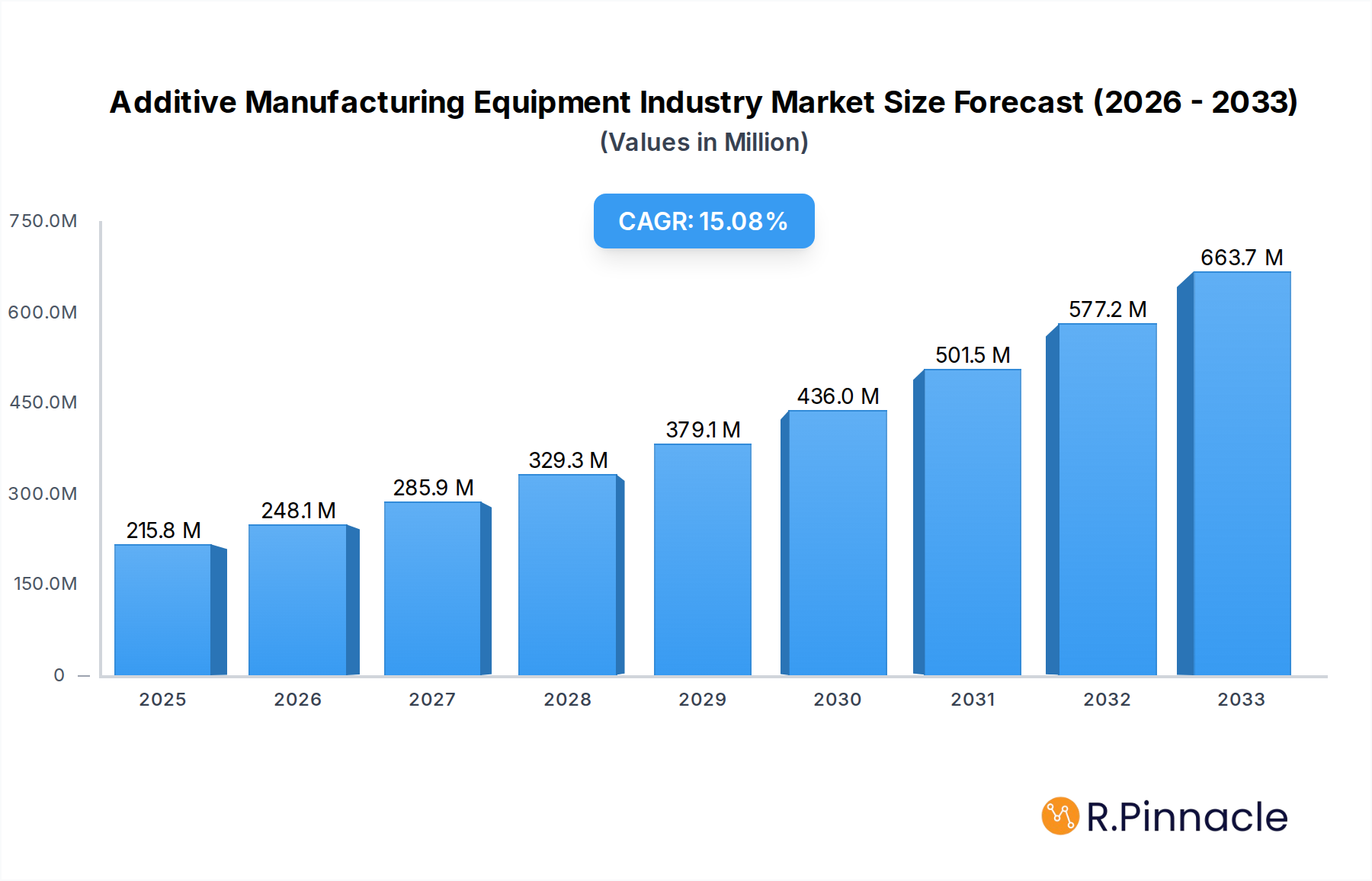

The global Additive Manufacturing Equipment market is poised for substantial expansion, projected to reach $215.78 million by 2025, driven by a remarkable Compound Annual Growth Rate (CAGR) of 15.17%. This robust growth trajectory is primarily fueled by the increasing adoption of advanced manufacturing technologies across diverse industries. Key drivers include the soaring demand for customized and complex components, particularly within the aerospace and defense sector, where lightweight and high-performance parts are critical. The energy and power industry is also a significant contributor, leveraging additive manufacturing for rapid prototyping and the production of specialized tools and components. Furthermore, the burgeoning medical sector's reliance on patient-specific implants and prosthetics, alongside the automotive industry's pursuit of innovative designs and reduced production costs, are powerful accelerators for this market. The Electronics industry's need for intricate, high-density circuitry and components further bolsters demand. Emerging trends such as the integration of AI and machine learning for process optimization, the development of novel materials, and the proliferation of distributed manufacturing models are set to redefine the landscape.

Additive Manufacturing Equipment Industry Market Size (In Million)

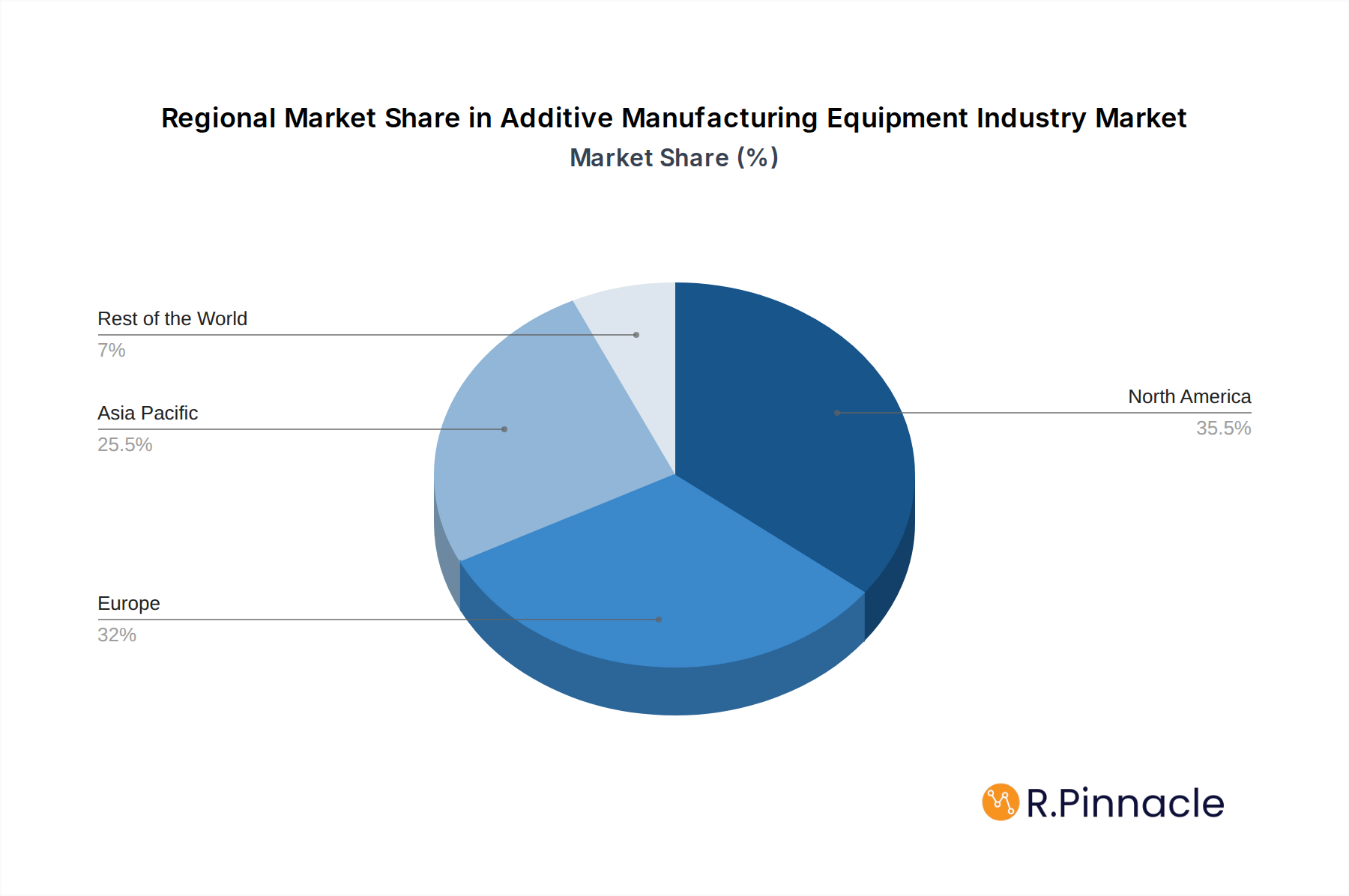

While the market exhibits strong growth, certain restraints could influence the pace of adoption. High initial investment costs for advanced additive manufacturing systems remain a hurdle for smaller enterprises. Additionally, the need for skilled labor capable of operating and maintaining these sophisticated machines, along with evolving regulatory frameworks, present challenges. However, these are being actively addressed through technological advancements and industry-led training initiatives. The market is segmented by end-user industries, with Aerospace & Defense, Energy & Power, Electronics, Medical, and Automotive anticipated to dominate. Companies like Optomec Inc., Mazak Corporation, and DMG MORI are at the forefront of innovation, introducing cutting-edge equipment and solutions. Geographically, North America and Europe are expected to lead in market share due to established industrial bases and significant R&D investments, followed closely by the Asia Pacific region, which is rapidly expanding its manufacturing capabilities. The "Rest of the World" segment, while smaller, presents significant untapped potential for future growth as developing economies increasingly embrace advanced manufacturing.

Additive Manufacturing Equipment Industry Company Market Share

Report Description: Additive Manufacturing Equipment Industry: Market Analysis, Trends, and Forecasts (2019–2033)

Gain a comprehensive understanding of the Additive Manufacturing Equipment Industry with this in-depth market report. Spanning from 2019 to 2033, with a base year of 2025, this report offers critical insights into market structure, dynamics, innovations, and future outlook. Leveraging high-ranking keywords such as 3D printing equipment, industrial additive manufacturing, metal 3D printing, polymer 3D printing, and advanced manufacturing technology, this analysis is designed to boost search visibility and engage industry professionals, decision-makers, and investors. Discover actionable intelligence on key players, emerging trends, and growth drivers shaping this rapidly evolving sector.

Additive Manufacturing Equipment Industry Market Structure & Innovation Trends

The additive manufacturing equipment market is characterized by a moderate concentration, with a few dominant players holding significant market share, estimated at approximately 60% of the total market value in 2025. Innovation is a primary driver, fueled by continuous research and development in materials science, software, and hardware, leading to advancements in printing speed, accuracy, and material capabilities. Regulatory frameworks, while still evolving, are increasingly focused on standardization and safety, impacting product development and adoption rates. Product substitutes, such as traditional subtractive manufacturing methods, are becoming less of a threat as additive manufacturing demonstrates superior capabilities for complex geometries, customization, and rapid prototyping. End-user demographics are diversifying, with strong growth in aerospace, medical, automotive, and electronics sectors, each demanding tailored solutions. Mergers and acquisitions (M&A) activities are strategic, with deal values ranging from tens to hundreds of millions of dollars, aimed at expanding product portfolios, market reach, and technological expertise. Key M&A activities are expected to contribute to further market consolidation and innovation synergy.

Additive Manufacturing Equipment Industry Market Dynamics & Trends

The additive manufacturing equipment market is experiencing robust growth, driven by an increasing demand for customized and complex parts, significant advancements in printing technologies, and the rising adoption of Industry 4.0 principles. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is estimated at 18.5%, indicating a significant expansion trajectory. Market penetration is deepening across various end-user industries as the benefits of additive manufacturing, such as reduced lead times, lower material waste, and enhanced design freedom, become more apparent. Technological disruptions, including the development of new printing materials (e.g., high-performance polymers, advanced metal alloys) and innovative printing processes (e.g., binder jetting, multi-material printing), are continuously reshaping the competitive landscape. Consumer preferences are shifting towards greater product personalization and on-demand manufacturing, directly benefiting additive manufacturing solutions. Competitive dynamics are intensifying, with established machinery manufacturers expanding their additive offerings and new specialized players emerging. The integration of AI and machine learning in design and production workflows is also a significant trend, optimizing processes and improving product quality. The increasing focus on sustainability, with additive manufacturing enabling lighter-weight designs and reduced material consumption, further fuels market expansion. The global market size is projected to reach approximately $25,000 million by 2025.

Dominant Regions & Segments in Additive Manufacturing Equipment Industry

North America currently dominates the additive manufacturing equipment market, driven by a strong ecosystem of innovation, significant government investment in advanced manufacturing, and the presence of leading end-user industries like aerospace and defense. The United States, in particular, leads in research and development, adoption rates, and market size, with an estimated market share of 35% in 2025. Key drivers for this dominance include robust economic policies supporting technological advancement, advanced infrastructure for industrial adoption, and a high concentration of R&D centers.

End-user Industry Dominance:

- Aerospace & Defense: This segment remains a primary driver, accounting for approximately 30% of the market share in 2025. The demand for lightweight, high-strength components, complex geometries, and rapid prototyping for aircraft and defense systems fuels significant investment in additive manufacturing equipment.

- Automotive: The automotive industry is rapidly adopting additive manufacturing for prototyping, tooling, and eventually, end-use parts production, representing around 20% of the market share. The pursuit of lighter vehicles for fuel efficiency and the need for mass customization are key growth factors.

- Medical: The medical sector, with its stringent requirements for biocompatibility, precision, and customization, is a high-value segment. This includes implants, prosthetics, and surgical instruments, contributing approximately 18% to the market share.

- Electronics: While a smaller segment currently at around 12%, the electronics industry is seeing increasing adoption for specialized components and rapid prototyping of circuit boards and intricate parts.

- Energy & Power: This segment, representing about 10% of the market share, benefits from additive manufacturing for producing complex turbine blades, specialized tools, and spare parts for exploration and production equipment.

- Other End-user Industries: This segment, making up the remaining 5%, includes sectors like consumer goods, industrial machinery, and education, which are increasingly exploring and adopting additive manufacturing solutions.

Additive Manufacturing Equipment Industry Product Innovations

Product innovations in the additive manufacturing equipment sector are focused on enhancing speed, precision, material compatibility, and user-friendliness. Developments include multi-material printing capabilities, enabling the creation of complex, functional parts with varying properties. Advanced software integration offers greater design freedom and process optimization, while new metal alloy printing technologies unlock applications requiring exceptional strength and durability. The competitive advantage lies in offering robust, scalable solutions that meet the demanding requirements of industries like aerospace and medical.

Report Scope & Segmentation Analysis

This report analyzes the additive manufacturing equipment industry across several key segments. The Aerospace & Defense sector is characterized by high growth projections and significant market size due to its demand for complex, lightweight components. The Energy & Power sector presents growing opportunities for specialized equipment used in turbine manufacturing and exploration. Electronics applications are expanding with the need for miniaturized and intricate components. The Medical segment is a high-value area, driven by demand for patient-specific implants and prosthetics, with strong growth projections. The Automotive industry is rapidly increasing its adoption for prototyping, tooling, and end-use parts. Other End-user Industries encompass a broad range of applications, each contributing to overall market expansion with unique growth dynamics.

Key Drivers of Additive Manufacturing Equipment Industry Growth

The growth of the additive manufacturing equipment industry is propelled by several interconnected factors. Technological advancements, such as enhanced material science, faster printing speeds, and increased precision, are fundamental drivers. The widespread adoption of Industry 4.0 principles and the increasing need for customized, on-demand manufacturing solutions are creating significant market opportunities. Government initiatives and investments supporting advanced manufacturing technologies, particularly in defense and aerospace sectors, also play a crucial role. Furthermore, the economic benefits of additive manufacturing, including reduced lead times, lower production costs for low-volume runs, and minimized material waste, are compelling businesses to invest in this technology.

Challenges in the Additive Manufacturing Equipment Industry Sector

Despite its rapid growth, the additive manufacturing equipment industry faces several challenges. High initial investment costs for industrial-grade equipment remain a barrier for some potential adopters. Regulatory hurdles and standardization efforts are still evolving, leading to uncertainty in certain applications. Supply chain complexities for specialized materials and spare parts can impact production continuity. Scalability for mass production is an ongoing area of development, with limitations in speed and throughput compared to traditional methods for very high volumes. Workforce skills gap, requiring specialized training for operation and maintenance, also presents a challenge.

Emerging Opportunities in Additive Manufacturing Equipment Industry

Emerging opportunities in the additive manufacturing equipment industry are abundant, driven by continuous innovation and expanding applications. The development of new advanced materials, including ceramics and composites, is opening up novel use cases. The growth of distributed manufacturing and on-demand production creates opportunities for smaller, more agile additive manufacturing solutions. The integration of AI and machine learning for process optimization, quality control, and predictive maintenance is a significant trend. Furthermore, the increasing focus on sustainability and circular economy principles, where additive manufacturing can play a key role in reducing waste and extending product lifecycles, presents a major opportunity for growth and market differentiation.

Leading Players in the Additive Manufacturing Equipment Industry Market

- Optomec Inc

- Mazak Corporation

- DMG MORI

- Matsuura Machinery Ltd

- Hybrid Manufacturing Technologies

- ELB-SCHLIFF Werkzeugmaschinen GmbH

- Mitsui Seiki Inc

- Okuma America Corporation

- Diversified Machine Systems

- Fabrisonic

Key Developments in Additive Manufacturing Equipment Industry Industry

- October 2023: Alphacam GmbH and Evolve Additive Solutions established a strategic alliance, enabling Alphacam to provide European customers with parts produced via the Selective Thermoplastic Electrophotographic Process (STEP).

- October 2023: Siemens integrated DMG MORI's digital twin for machine tool processing onto its Xcelerator marketplace, strengthening their collaboration in the Industry 4.0 space.

- July 2023: Mazak India, a division of Yamazaki Mazak Corporation, inaugurated a new, state-of-the-art production facility in Pune, signaling a commitment to innovation and expansion within the Indian manufacturing sector.

Future Outlook for Additive Manufacturing Equipment Industry Market

The future outlook for the additive manufacturing equipment industry is exceptionally bright, driven by sustained technological advancements and expanding market adoption. Continued investment in R&D will lead to more sophisticated equipment capable of handling a wider range of materials and complex geometries with enhanced speed and precision. The ongoing digital transformation of manufacturing, including the integration of IoT, AI, and cloud computing, will further streamline additive manufacturing processes. We anticipate a significant surge in adoption across existing sectors and the emergence of new applications in fields like sustainable energy solutions and personalized consumer goods. Strategic partnerships and collaborations will continue to shape the market, fostering innovation and expanding global reach, positioning additive manufacturing as a cornerstone of future industrial production.

Additive Manufacturing Equipment Industry Segmentation

-

1. End-user Industry

- 1.1. Aerospace & Defense

- 1.2. Energy & Power

- 1.3. Electronics

- 1.4. Medical

- 1.5. Automotive

- 1.6. Other End-user Industries

Additive Manufacturing Equipment Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Additive Manufacturing Equipment Industry Regional Market Share

Geographic Coverage of Additive Manufacturing Equipment Industry

Additive Manufacturing Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 5.1.1. Aerospace & Defense

- 5.1.2. Energy & Power

- 5.1.3. Electronics

- 5.1.4. Medical

- 5.1.5. Automotive

- 5.1.6. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6. Global Additive Manufacturing Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6.1.1. Aerospace & Defense

- 6.1.2. Energy & Power

- 6.1.3. Electronics

- 6.1.4. Medical

- 6.1.5. Automotive

- 6.1.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7. North America Additive Manufacturing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7.1.1. Aerospace & Defense

- 7.1.2. Energy & Power

- 7.1.3. Electronics

- 7.1.4. Medical

- 7.1.5. Automotive

- 7.1.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8. Europe Additive Manufacturing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8.1.1. Aerospace & Defense

- 8.1.2. Energy & Power

- 8.1.3. Electronics

- 8.1.4. Medical

- 8.1.5. Automotive

- 8.1.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9. Asia Pacific Additive Manufacturing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9.1.1. Aerospace & Defense

- 9.1.2. Energy & Power

- 9.1.3. Electronics

- 9.1.4. Medical

- 9.1.5. Automotive

- 9.1.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10. Rest of the World Additive Manufacturing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10.1.1. Aerospace & Defense

- 10.1.2. Energy & Power

- 10.1.3. Electronics

- 10.1.4. Medical

- 10.1.5. Automotive

- 10.1.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Optomec Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Mazak Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 DMG MORI

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Matsuura Machinery Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Hybrid Manufacturing technologies

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 ELB-SCHLIFF Werkzeugmaschinen GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Mitsui Seiki Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Okuma America Corporation

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Diversified Machine Systems

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Fabrisonic**List Not Exhaustive

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Optomec Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Additive Manufacturing Equipment Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Additive Manufacturing Equipment Industry Volume Breakdown (Billion, %) by Region 2025 & 2033

- Figure 3: North America Additive Manufacturing Equipment Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 4: North America Additive Manufacturing Equipment Industry Volume (Billion), by End-user Industry 2025 & 2033

- Figure 5: North America Additive Manufacturing Equipment Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Additive Manufacturing Equipment Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 7: North America Additive Manufacturing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 8: North America Additive Manufacturing Equipment Industry Volume (Billion), by Country 2025 & 2033

- Figure 9: North America Additive Manufacturing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Additive Manufacturing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Additive Manufacturing Equipment Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 12: Europe Additive Manufacturing Equipment Industry Volume (Billion), by End-user Industry 2025 & 2033

- Figure 13: Europe Additive Manufacturing Equipment Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: Europe Additive Manufacturing Equipment Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: Europe Additive Manufacturing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: Europe Additive Manufacturing Equipment Industry Volume (Billion), by Country 2025 & 2033

- Figure 17: Europe Additive Manufacturing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Additive Manufacturing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Additive Manufacturing Equipment Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 20: Asia Pacific Additive Manufacturing Equipment Industry Volume (Billion), by End-user Industry 2025 & 2033

- Figure 21: Asia Pacific Additive Manufacturing Equipment Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: Asia Pacific Additive Manufacturing Equipment Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific Additive Manufacturing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Asia Pacific Additive Manufacturing Equipment Industry Volume (Billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Additive Manufacturing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Additive Manufacturing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Rest of the World Additive Manufacturing Equipment Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 28: Rest of the World Additive Manufacturing Equipment Industry Volume (Billion), by End-user Industry 2025 & 2033

- Figure 29: Rest of the World Additive Manufacturing Equipment Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Rest of the World Additive Manufacturing Equipment Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: Rest of the World Additive Manufacturing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Rest of the World Additive Manufacturing Equipment Industry Volume (Billion), by Country 2025 & 2033

- Figure 33: Rest of the World Additive Manufacturing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Rest of the World Additive Manufacturing Equipment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 2: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 5: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 9: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 13: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 17: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 19: Global Additive Manufacturing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Global Additive Manufacturing Equipment Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Additive Manufacturing Equipment Industry?

The projected CAGR is approximately 15.17%.

2. Which companies are prominent players in the Additive Manufacturing Equipment Industry?

Key companies in the market include Optomec Inc, Mazak Corporation, DMG MORI, Matsuura Machinery Ltd, Hybrid Manufacturing technologies, ELB-SCHLIFF Werkzeugmaschinen GmbH, Mitsui Seiki Inc, Okuma America Corporation, Diversified Machine Systems, Fabrisonic**List Not Exhaustive.

3. What are the main segments of the Additive Manufacturing Equipment Industry?

The market segments include End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 215.78 Million as of 2022.

5. What are some drivers contributing to market growth?

Industry 4.0 Integration; In industries like healthcare and automotive. there is a growing demand for customized and patient-specific parts..

6. What are the notable trends driving market growth?

Medical Sector Expected to Hold a Significant Share.

7. Are there any restraints impacting market growth?

Industry 4.0 Integration; In industries like healthcare and automotive. there is a growing demand for customized and patient-specific parts..

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Additive Manufacturing Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Additive Manufacturing Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Additive Manufacturing Equipment Industry?

To stay informed about further developments, trends, and reports in the Additive Manufacturing Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence