Key Insights

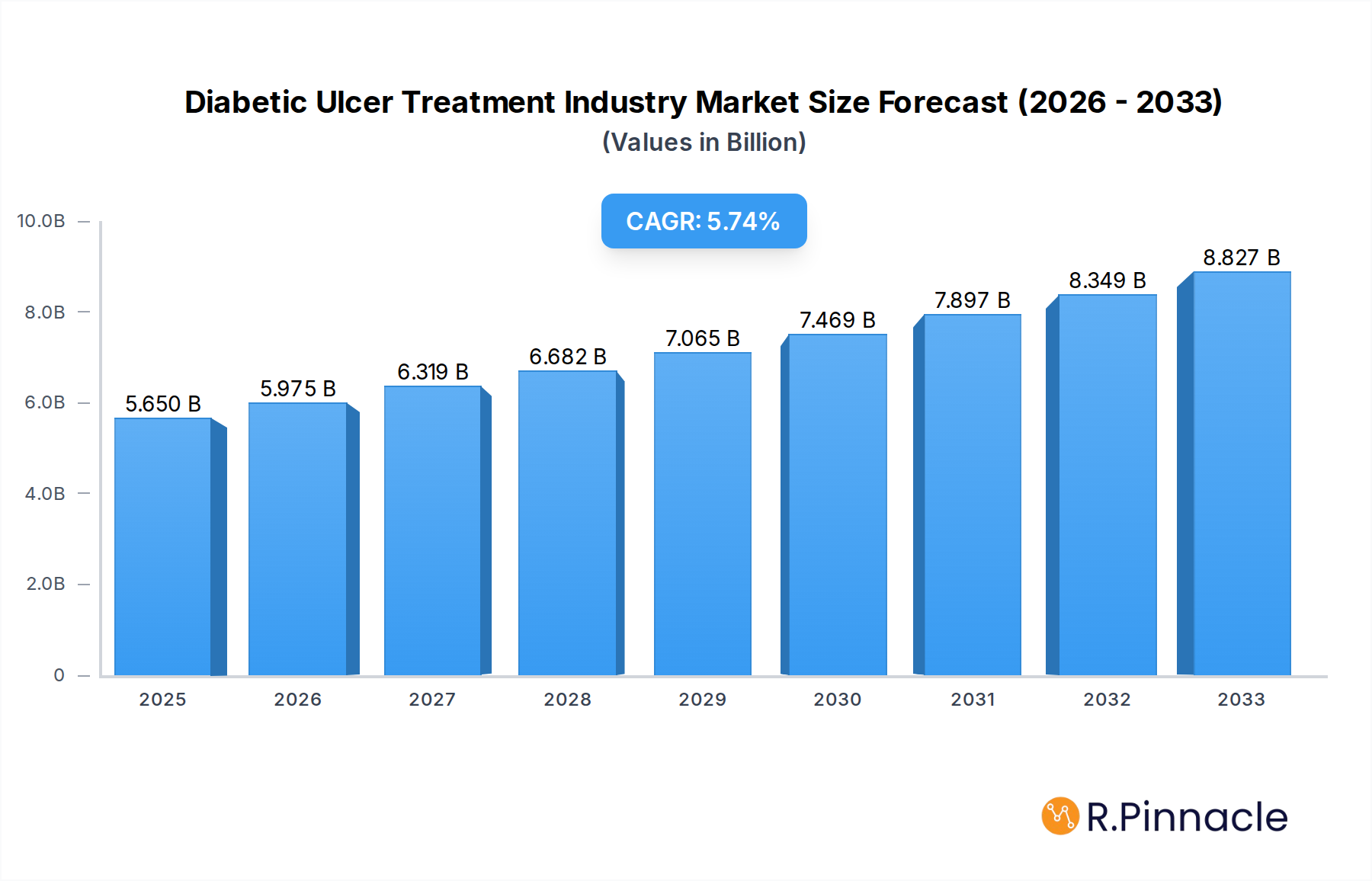

The Diabetic Ulcer Treatment market is poised for significant expansion, with a current estimated market size of $5.65 billion and a projected Compound Annual Growth Rate (CAGR) of 5.75% during the forecast period of 2025-2033. This robust growth is primarily fueled by the escalating prevalence of diabetes worldwide, a condition that directly contributes to the development of chronic and difficult-to-heal diabetic ulcers. Advancements in wound care technologies, including innovative dressings and sophisticated therapeutic devices, are further stimulating market demand. The increasing focus on early intervention and comprehensive management of diabetic foot ulcers, coupled with growing healthcare expenditure and a rising awareness among patients and healthcare providers regarding effective treatment options, are key drivers propelling the market forward. The availability of advanced treatments such as skin substitutes and growth factors, alongside the adoption of negative pressure wound therapy (NPWT) and hyperbaric oxygen therapy, are crucial in improving patient outcomes and driving market growth.

Diabetic Ulcer Treatment Industry Market Size (In Billion)

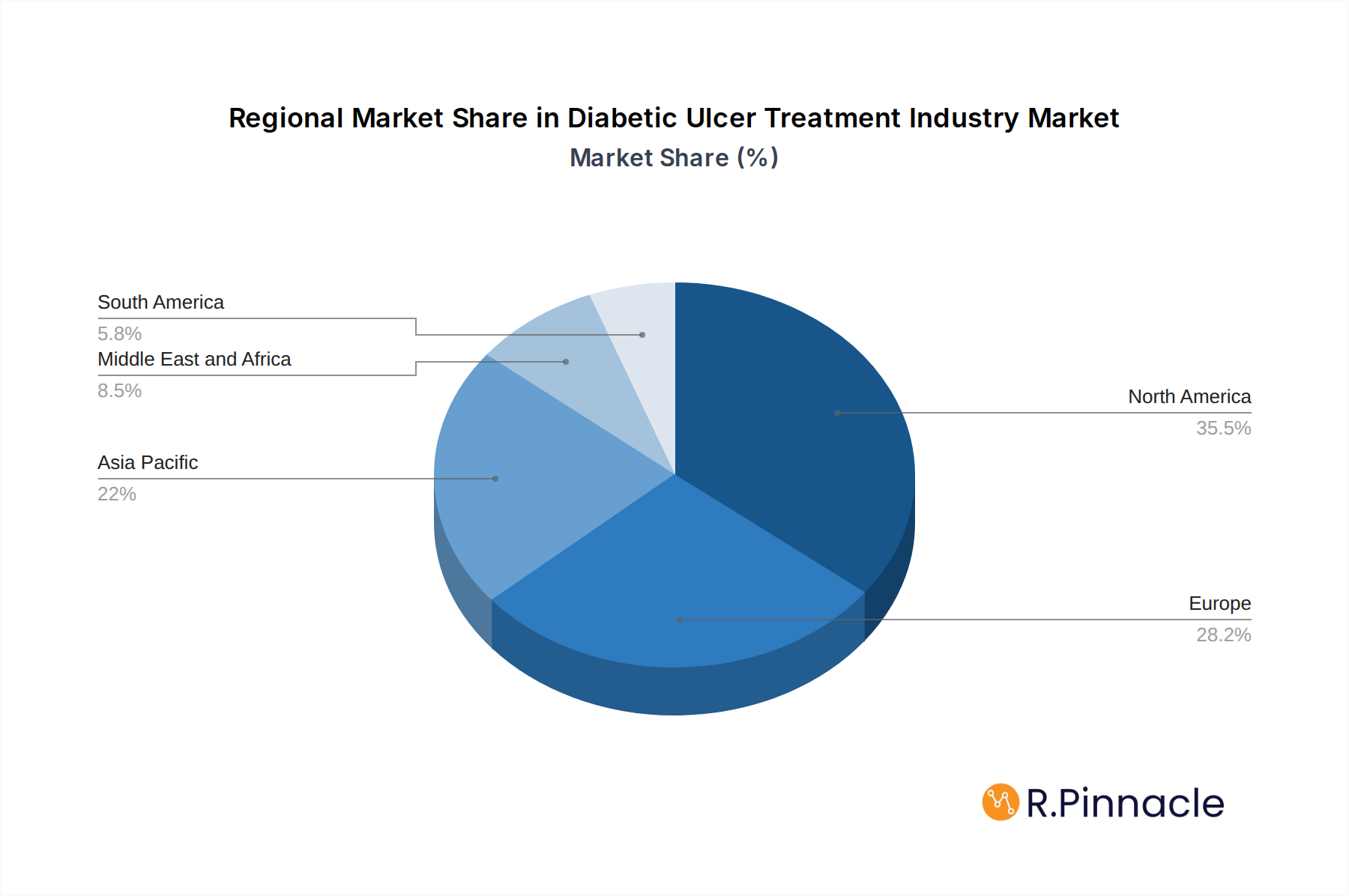

The market is segmented into Product Type, Active Wound Care Therapies, and Wound Care Devices. Within Product Type, wound care dressings, encompassing film, foam, hydrogel, and collagen dressings, represent a substantial segment due to their critical role in managing wound environments. Active Wound Care Therapies, particularly skin substitutes, are gaining traction for their regenerative potential in complex cases. The Wound Care Devices segment, led by Negative Pressure Wound Therapy (NPWT) and pressure-relieving devices, is witnessing increased adoption for its efficacy in accelerating healing and preventing complications. Geographically, North America currently leads the market, driven by high diabetes rates and advanced healthcare infrastructure. However, the Asia Pacific region is expected to exhibit the fastest growth, owing to its large and growing diabetic population, increasing healthcare investments, and rising adoption of advanced wound care solutions. Key industry players are actively engaged in research and development, strategic collaborations, and product launches to capture a larger market share and address the unmet needs in diabetic ulcer management.

Diabetic Ulcer Treatment Industry Company Market Share

Diabetic Ulcer Treatment Industry Market Structure & Innovation Trends

The global diabetic ulcer treatment market exhibits a moderately concentrated structure, with key players like Baxter International Inc (Hill-Rom Holdings Inc), Smith & Nephew PLC, and Integra LifeSciences Holding Corporation holding significant market shares. Innovation is a primary driver, fueled by advancements in material science for wound dressings, sophisticated active wound care therapies, and increasingly integrated wound care devices. Regulatory frameworks, particularly stringent FDA and EMA approvals, shape market entry and product development. The threat of product substitutes is managed through continuous innovation and evidence-based efficacy. End-user demographics are expanding with the rising global prevalence of diabetes. Mergers and acquisitions (M&A) remain a strategic tool for market consolidation and technology acquisition, with deal values in the high hundreds of billions. For instance, acquisitions in the wound care segment can reach values of over $1 Billion, indicating intense strategic activity.

- Market Concentration: Dominated by a few key multinational corporations, but with room for specialized innovators.

- Innovation Drivers: Focus on biomaterials, regenerative medicine, and smart wound monitoring technologies.

- Regulatory Landscape: Strict adherence to global healthcare regulations for product safety and efficacy.

- Product Substitutes: Managed through superior product performance, cost-effectiveness, and patient outcomes.

- End-User Demographics: Growing patient pool due to increasing diabetes rates and aging populations.

- M&A Activities: Strategic consolidations and acquisitions of innovative technologies are prevalent, with potential deal values exceeding $1 Billion.

Diabetic Ulcer Treatment Industry Market Dynamics & Trends

The diabetic ulcer treatment industry is poised for substantial growth, driven by a confluence of escalating global diabetes prevalence and an aging population, both contributing to an expanding patient base susceptible to chronic wound development. The estimated market size for diabetic ulcer treatments is projected to reach over $20 Billion by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033. Technological disruptions are at the forefront of market dynamics, with the continuous development of advanced wound care dressings offering enhanced moisture management, antimicrobial properties, and accelerated healing. Innovations in active wound care therapies, such as sophisticated skin substitutes and novel growth factor delivery systems, are revolutionizing treatment protocols by promoting tissue regeneration. Furthermore, the integration of wound care devices, including negative pressure wound therapy (NPWT) systems and advanced hyperbaric oxygen equipment, is becoming increasingly sophisticated, offering more effective and less invasive solutions. Consumer preferences are shifting towards treatments that offer faster healing times, reduced pain, improved patient comfort, and better aesthetic outcomes, influencing product development and marketing strategies. Competitive dynamics are characterized by intense R&D investment, strategic partnerships, and a focus on demonstrating clinical efficacy and cost-effectiveness to healthcare providers and payers. The market penetration of advanced treatment modalities is steadily increasing as awareness grows and reimbursement policies evolve to cover innovative solutions. The base year of 2025 is a critical juncture, with market trends firmly established and poised for significant acceleration in the coming years. Market players are investing heavily in addressing the unmet needs of patients with difficult-to-heal diabetic foot ulcers, a condition that significantly impacts quality of life and incurs substantial healthcare costs. The drive for novel solutions is amplified by the economic burden associated with managing diabetic ulcers, including prolonged hospital stays, frequent dressing changes, and the risk of infection and amputation. This economic imperative, coupled with a strong clinical need, creates a fertile ground for innovation and market expansion.

Dominant Regions & Segments in Diabetic Ulcer Treatment Industry

North America currently dominates the diabetic ulcer treatment market, with the United States leading regional consumption and investment in advanced wound care solutions. This dominance is attributed to several key factors including a high prevalence of diabetes, a well-established healthcare infrastructure, significant R&D investments, and favorable reimbursement policies for innovative treatments. The region’s robust market penetration for advanced wound care dressings and active wound care therapies, particularly in wound care devices like NPWT, solidifies its leading position.

Product Type Dominance:

Wound Care Dressings: This segment is foundational, with particular strength in advanced materials.

- Foam Dressings: Widely adopted for their absorbency and cushioning properties, foam dressings are a staple in managing exuding diabetic ulcers. Their ability to maintain a moist wound environment while managing exudate makes them highly effective.

- Hydrogel Dressings: Crucial for rehydrating dry wounds and promoting autolytic debridement, hydrogel dressings play a vital role in wound bed preparation. Their gel matrix provides a soothing effect and supports healing.

- Collagen Dressings: Increasingly important for chronic wounds that fail to progress, collagen dressings provide a scaffold for new tissue growth and support cellular activity.

- Film Dressings: Primarily used for superficial wounds or as secondary dressings, film dressings offer transparency for wound monitoring and a barrier against external contaminants.

Active Wound Care Therapies: This segment is witnessing rapid innovation and growth.

- Skin Substitutes: These bioengineered or biological materials, including allografts, xenografts, and synthetic scaffolds, are pivotal in promoting wound closure and regeneration, especially for severe ulcers. Their market share is growing significantly due to improved clinical outcomes.

Wound Care Devices: These are critical for managing complex cases and accelerating healing.

- Negative Pressure Wound Therapy (NPWT): This technology is a cornerstone in treating large, complex, or infected diabetic ulcers, significantly reducing healing times and complications. Its adoption continues to rise due to its efficacy and ability to manage exudate effectively.

- Hyperbaric Oxygen Equipment: While more specialized, hyperbaric oxygen therapy offers substantial benefits for select diabetic ulcer patients by increasing oxygen delivery to tissues, promoting angiogenesis, and combating infection.

The continuous innovation within these segments, coupled with a growing understanding of their clinical and economic benefits, fuels their dominance in the global diabetic ulcer treatment market. Economic policies supporting healthcare access, coupled with robust infrastructure for advanced medical devices and therapies, further solidify the leading position of regions like North America and, increasingly, Europe and Asia-Pacific.

Diabetic Ulcer Treatment Industry Product Innovations

Product innovations in the diabetic ulcer treatment industry are primarily focused on enhancing healing efficiency and patient comfort. Advanced wound dressings now incorporate antimicrobial agents, growth factors, and novel bio-materials that promote tissue regeneration and reduce inflammation. Skin substitutes are becoming more sophisticated, mimicking the natural extracellular matrix to support cellular proliferation and differentiation. Wound care devices are seeing advancements in miniaturization, user-friendliness, and integrated monitoring capabilities, allowing for more personalized and effective therapy delivery. These innovations aim to reduce treatment duration, minimize pain, and prevent complications like infection and amputation, offering a significant competitive advantage to companies at the forefront of R&D.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global diabetic ulcer treatment market, segmented comprehensively to provide actionable insights. The Product Type segmentation includes Wound Care Dressings, encompassing Film Dressings, Foams Dressings, Hydrogel Dressings, Collagen Dressings, and Other Wound Care Dressings. The Active Wound Care Therapies segment covers Skin Substitutes and Growth Factors. Finally, the Wound Care Devices segment includes Negative Pressure Wound Therapy, Hyperbaric Oxygen Equipment, Pressure Relieving Devices, and Other Devices. Each segment's market size, growth projections, and competitive dynamics are detailed, with specific attention to their contribution to the overall market growth and their respective market shares.

Key Drivers of Diabetic Ulcer Treatment Industry Growth

The diabetic ulcer treatment industry's growth is propelled by several key factors:

- Rising Global Diabetes Prevalence: The escalating number of individuals diagnosed with diabetes worldwide directly increases the pool of patients at risk for developing diabetic ulcers.

- Aging Population: Older adults are more susceptible to chronic conditions like diabetes and have a higher incidence of slow-healing wounds, contributing to sustained market demand.

- Technological Advancements: Continuous innovation in wound dressings, active therapies (like skin substitutes and growth factors), and devices (such as NPWT) offers more effective and efficient treatment options.

- Increased Healthcare Spending & Awareness: Growing investment in healthcare infrastructure and heightened awareness among patients and healthcare providers regarding advanced wound care solutions are driving market adoption.

Challenges in the Diabetic Ulcer Treatment Industry Sector

Despite robust growth, the diabetic ulcer treatment sector faces significant challenges:

- High Cost of Advanced Treatments: Innovative therapies and devices can be expensive, posing barriers to accessibility, particularly in resource-limited regions.

- Reimbursement Policies: Inconsistent or restrictive reimbursement policies for advanced wound care can hinder market penetration and adoption by healthcare providers.

- Regulatory Hurdles: Stringent approval processes for new medical devices and therapies can lead to lengthy development timelines and significant R&D costs.

- Lack of Skilled Healthcare Professionals: A shortage of trained wound care specialists can limit the effective application of complex treatment modalities.

Emerging Opportunities in Diabetic Ulcer Treatment Industry

The diabetic ulcer treatment industry is ripe with emerging opportunities:

- Development of Novel Biomaterials: Innovations in biodegradable and bio-integrative materials for wound dressings and scaffolds offer enhanced healing properties and patient comfort.

- Telehealth and Remote Patient Monitoring: The integration of telehealth platforms for wound assessment and monitoring can improve patient access to care, especially in rural areas.

- Personalized Medicine Approaches: Tailoring treatments based on individual patient profiles, including genetic predispositions and wound characteristics, presents a significant opportunity for improved outcomes.

- Growth in Emerging Markets: Rapidly developing economies with increasing diabetes rates and improving healthcare infrastructure represent substantial untapped market potential.

Leading Players in the Diabetic Ulcer Treatment Industry Market

- Baxter International Inc (Hill-Rom Holdings Inc)

- Smith & Nephew PLC

- Integra LifeSciences Holding Corporation

- Essity Aktiebolag

- ConvaTec Group PLC

- Molnlycke Health Care AB

- 3M Company

- Cardinal Health

- B Braun Melsungen AG

- Coloplast Group

Key Developments in Diabetic Ulcer Treatment Industry Industry

- March 2021: Smith+Nephew announced the results of a real-world study from Spain demonstrating how a switch to ALLEVYN LIFE Foam Dressings significantly reduced dressing change frequency and weekly dressing costs while improving treatment satisfaction for clinicians and patients in a community setting.

- February 2021: Axis Biosolutions received European CE mark approval for the advanced wound care product, MAxiCel, which is used in several chronic wounds, including pressure ulcers.

Future Outlook for Diabetic Ulcer Treatment Industry Market

The future outlook for the diabetic ulcer treatment industry is exceptionally bright, driven by persistent global diabetes prevalence and continuous technological advancements. The market is expected to witness accelerated growth propelled by the increasing adoption of advanced wound care dressings, regenerative medicine-based therapies like skin substitutes, and sophisticated wound care devices such as NPWT. Future growth accelerators will include a greater emphasis on evidence-based medicine, demonstrating cost-effectiveness alongside clinical efficacy, and the integration of digital health solutions for improved patient management and outcomes. Strategic partnerships, targeted R&D investments in novel materials and biologics, and expansion into emerging markets will be critical for sustained success. The industry is poised to evolve towards more personalized and minimally invasive treatment approaches, ultimately aiming to significantly reduce the burden of diabetic ulcers on patients and healthcare systems worldwide.

Diabetic Ulcer Treatment Industry Segmentation

-

1. Product Type

-

1.1. Wound Care Dressings

- 1.1.1. Film Dressings

- 1.1.2. Foams Dressings

- 1.1.3. Hydrogel Dressings

- 1.1.4. Collagen Dressings

- 1.1.5. Other Wound Care Dressings

-

1.2. Active Wound Care Therapies

- 1.2.1. Skin Substitutes

- 1.2.2. Growth Factors

-

1.3. Wound Care Devices

- 1.3.1. Negative Pressure Wound Therapy

- 1.3.2. Hyperbaric Oxygen Equipment

- 1.3.3. Pressure Relieving Devices

- 1.3.4. Other Devices

-

1.1. Wound Care Dressings

Diabetic Ulcer Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Diabetic Ulcer Treatment Industry Regional Market Share

Geographic Coverage of Diabetic Ulcer Treatment Industry

Diabetic Ulcer Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Wound Care Dressings

- 5.1.1.1. Film Dressings

- 5.1.1.2. Foams Dressings

- 5.1.1.3. Hydrogel Dressings

- 5.1.1.4. Collagen Dressings

- 5.1.1.5. Other Wound Care Dressings

- 5.1.2. Active Wound Care Therapies

- 5.1.2.1. Skin Substitutes

- 5.1.2.2. Growth Factors

- 5.1.3. Wound Care Devices

- 5.1.3.1. Negative Pressure Wound Therapy

- 5.1.3.2. Hyperbaric Oxygen Equipment

- 5.1.3.3. Pressure Relieving Devices

- 5.1.3.4. Other Devices

- 5.1.1. Wound Care Dressings

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Wound Care Dressings

- 6.1.1.1. Film Dressings

- 6.1.1.2. Foams Dressings

- 6.1.1.3. Hydrogel Dressings

- 6.1.1.4. Collagen Dressings

- 6.1.1.5. Other Wound Care Dressings

- 6.1.2. Active Wound Care Therapies

- 6.1.2.1. Skin Substitutes

- 6.1.2.2. Growth Factors

- 6.1.3. Wound Care Devices

- 6.1.3.1. Negative Pressure Wound Therapy

- 6.1.3.2. Hyperbaric Oxygen Equipment

- 6.1.3.3. Pressure Relieving Devices

- 6.1.3.4. Other Devices

- 6.1.1. Wound Care Dressings

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Wound Care Dressings

- 7.1.1.1. Film Dressings

- 7.1.1.2. Foams Dressings

- 7.1.1.3. Hydrogel Dressings

- 7.1.1.4. Collagen Dressings

- 7.1.1.5. Other Wound Care Dressings

- 7.1.2. Active Wound Care Therapies

- 7.1.2.1. Skin Substitutes

- 7.1.2.2. Growth Factors

- 7.1.3. Wound Care Devices

- 7.1.3.1. Negative Pressure Wound Therapy

- 7.1.3.2. Hyperbaric Oxygen Equipment

- 7.1.3.3. Pressure Relieving Devices

- 7.1.3.4. Other Devices

- 7.1.1. Wound Care Dressings

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Wound Care Dressings

- 8.1.1.1. Film Dressings

- 8.1.1.2. Foams Dressings

- 8.1.1.3. Hydrogel Dressings

- 8.1.1.4. Collagen Dressings

- 8.1.1.5. Other Wound Care Dressings

- 8.1.2. Active Wound Care Therapies

- 8.1.2.1. Skin Substitutes

- 8.1.2.2. Growth Factors

- 8.1.3. Wound Care Devices

- 8.1.3.1. Negative Pressure Wound Therapy

- 8.1.3.2. Hyperbaric Oxygen Equipment

- 8.1.3.3. Pressure Relieving Devices

- 8.1.3.4. Other Devices

- 8.1.1. Wound Care Dressings

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Wound Care Dressings

- 9.1.1.1. Film Dressings

- 9.1.1.2. Foams Dressings

- 9.1.1.3. Hydrogel Dressings

- 9.1.1.4. Collagen Dressings

- 9.1.1.5. Other Wound Care Dressings

- 9.1.2. Active Wound Care Therapies

- 9.1.2.1. Skin Substitutes

- 9.1.2.2. Growth Factors

- 9.1.3. Wound Care Devices

- 9.1.3.1. Negative Pressure Wound Therapy

- 9.1.3.2. Hyperbaric Oxygen Equipment

- 9.1.3.3. Pressure Relieving Devices

- 9.1.3.4. Other Devices

- 9.1.1. Wound Care Dressings

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Wound Care Dressings

- 10.1.1.1. Film Dressings

- 10.1.1.2. Foams Dressings

- 10.1.1.3. Hydrogel Dressings

- 10.1.1.4. Collagen Dressings

- 10.1.1.5. Other Wound Care Dressings

- 10.1.2. Active Wound Care Therapies

- 10.1.2.1. Skin Substitutes

- 10.1.2.2. Growth Factors

- 10.1.3. Wound Care Devices

- 10.1.3.1. Negative Pressure Wound Therapy

- 10.1.3.2. Hyperbaric Oxygen Equipment

- 10.1.3.3. Pressure Relieving Devices

- 10.1.3.4. Other Devices

- 10.1.1. Wound Care Dressings

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Diabetic Ulcer Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Wound Care Dressings

- 11.1.1.1. Film Dressings

- 11.1.1.2. Foams Dressings

- 11.1.1.3. Hydrogel Dressings

- 11.1.1.4. Collagen Dressings

- 11.1.1.5. Other Wound Care Dressings

- 11.1.2. Active Wound Care Therapies

- 11.1.2.1. Skin Substitutes

- 11.1.2.2. Growth Factors

- 11.1.3. Wound Care Devices

- 11.1.3.1. Negative Pressure Wound Therapy

- 11.1.3.2. Hyperbaric Oxygen Equipment

- 11.1.3.3. Pressure Relieving Devices

- 11.1.3.4. Other Devices

- 11.1.1. Wound Care Dressings

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Baxter International Inc (Hill-Rom Holdings Inc )

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Smith & Nephew PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Integra LifeSciences Holding Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Essity Aktiebolag

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ConvaTec Group PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Molnlycke Health Care AB

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 3M Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cardinal Health

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 B Braun Melsungen AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Coloplast Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Baxter International Inc (Hill-Rom Holdings Inc )

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Diabetic Ulcer Treatment Industry Revenue Breakdown (Billion, %) by Region 2025 & 2033

- Figure 2: North America Diabetic Ulcer Treatment Industry Revenue (Billion), by Product Type 2025 & 2033

- Figure 3: North America Diabetic Ulcer Treatment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Diabetic Ulcer Treatment Industry Revenue (Billion), by Country 2025 & 2033

- Figure 5: North America Diabetic Ulcer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Diabetic Ulcer Treatment Industry Revenue (Billion), by Product Type 2025 & 2033

- Figure 7: Europe Diabetic Ulcer Treatment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: Europe Diabetic Ulcer Treatment Industry Revenue (Billion), by Country 2025 & 2033

- Figure 9: Europe Diabetic Ulcer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Diabetic Ulcer Treatment Industry Revenue (Billion), by Product Type 2025 & 2033

- Figure 11: Asia Pacific Diabetic Ulcer Treatment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Asia Pacific Diabetic Ulcer Treatment Industry Revenue (Billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Diabetic Ulcer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East and Africa Diabetic Ulcer Treatment Industry Revenue (Billion), by Product Type 2025 & 2033

- Figure 15: Middle East and Africa Diabetic Ulcer Treatment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Middle East and Africa Diabetic Ulcer Treatment Industry Revenue (Billion), by Country 2025 & 2033

- Figure 17: Middle East and Africa Diabetic Ulcer Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: South America Diabetic Ulcer Treatment Industry Revenue (Billion), by Product Type 2025 & 2033

- Figure 19: South America Diabetic Ulcer Treatment Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: South America Diabetic Ulcer Treatment Industry Revenue (Billion), by Country 2025 & 2033

- Figure 21: South America Diabetic Ulcer Treatment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Region 2020 & 2033

- Table 3: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 4: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 5: United States Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 8: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 9: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 10: Germany Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 11: United Kingdom Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 12: France Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 13: Italy Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 14: Spain Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 16: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 17: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 18: China Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 19: Japan Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 20: India Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 21: Australia Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 22: South Korea Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Asia Pacific Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 24: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 25: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 26: GCC Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 27: South Africa Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 28: Rest of Middle East and Africa Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 29: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Product Type 2020 & 2033

- Table 30: Global Diabetic Ulcer Treatment Industry Revenue Billion Forecast, by Country 2020 & 2033

- Table 31: Brazil Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 32: Argentina Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of South America Diabetic Ulcer Treatment Industry Revenue (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetic Ulcer Treatment Industry?

The projected CAGR is approximately 5.75%.

2. Which companies are prominent players in the Diabetic Ulcer Treatment Industry?

Key companies in the market include Baxter International Inc (Hill-Rom Holdings Inc ), Smith & Nephew PLC, Integra LifeSciences Holding Corporation, Essity Aktiebolag, ConvaTec Group PLC, Molnlycke Health Care AB, 3M Company, Cardinal Health, B Braun Melsungen AG, Coloplast Group.

3. What are the main segments of the Diabetic Ulcer Treatment Industry?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.65 Billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Geriatric Population and Increasing Prevalence of Chronic Diseases; Growing Demand for Faster Recovery of Wounds.

6. What are the notable trends driving market growth?

Foam Dressing is Expected to Hold a Major Market Share in the Pressure Ulcers Treatment Market.

7. Are there any restraints impacting market growth?

High Cost of Advanced Wound Care Products.

8. Can you provide examples of recent developments in the market?

In March 2021, Smith+Nephew announced the results of a real-world study from Spain that showed how a switch to ALLEVYN LIFE Foam Dressings helped significantly reduce dressing change frequency and weekly dressing costs while improving treatment satisfaction for clinicians and patients in a community setting.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetic Ulcer Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetic Ulcer Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetic Ulcer Treatment Industry?

To stay informed about further developments, trends, and reports in the Diabetic Ulcer Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence