Key Insights

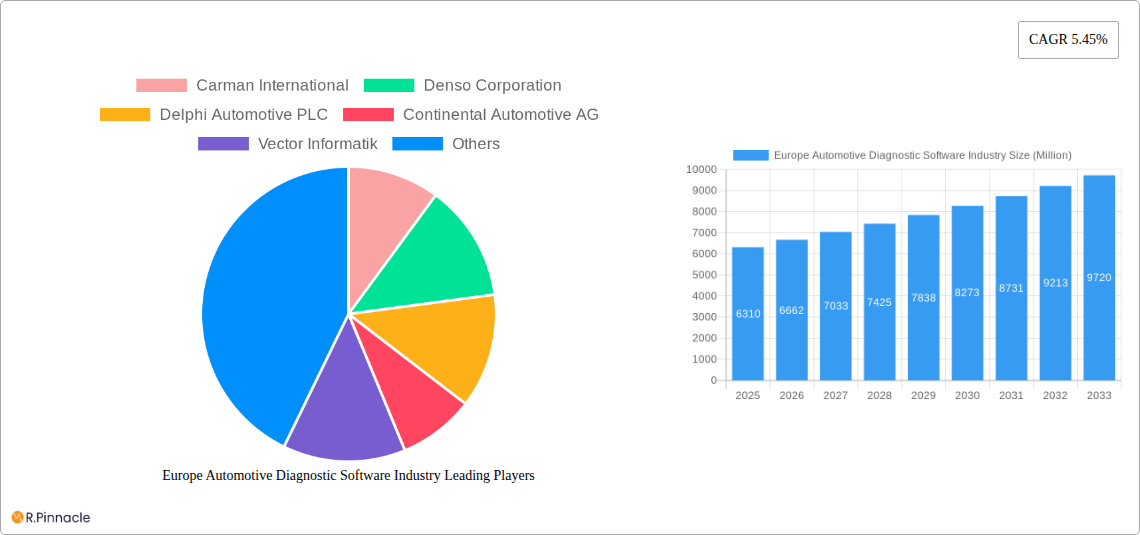

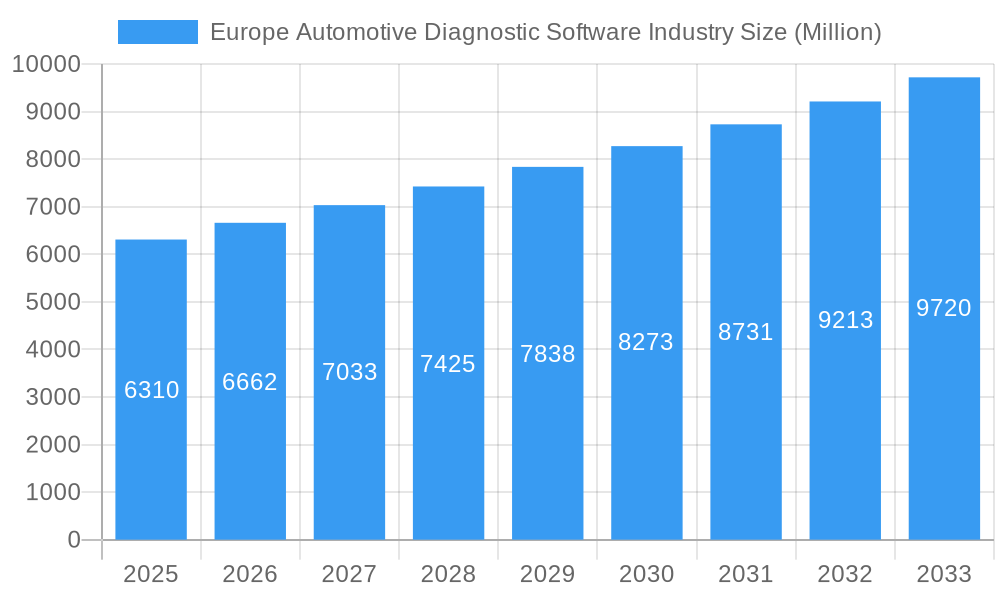

The European automotive diagnostic software market, valued at €6.31 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.45% from 2025 to 2033. This expansion is driven by several key factors. The increasing complexity of modern vehicles, incorporating advanced driver-assistance systems (ADAS) and electric powertrains, necessitates sophisticated diagnostic tools. Furthermore, stringent emission regulations and the growing demand for efficient vehicle maintenance are fueling the adoption of advanced diagnostic software solutions. The market is segmented by software type (OBD, Electric System Analyzer, Scan Tool) and vehicle type (Passenger Cars, Commercial Vehicles). Passenger cars currently dominate the market share, although the commercial vehicle segment is expected to experience faster growth due to increasing fleet management needs and the rising importance of preventative maintenance in optimizing operational efficiency. Key players like Bosch, Denso, and Continental are actively investing in research and development, leading to continuous innovation in diagnostic software capabilities. The dominance of established players, however, suggests a competitive landscape with high barriers to entry for new entrants. Growth is also geographically concentrated, with Germany, the UK, and France leading the market due to a higher concentration of automotive manufacturers and a well-established automotive aftermarket.

Europe Automotive Diagnostic Software Industry Market Size (In Billion)

The forecast period (2025-2033) anticipates continued market expansion, fueled by increasing vehicle connectivity and the rise of connected car technologies. Data analytics embedded within diagnostic software will play a crucial role, providing valuable insights into vehicle performance and enabling predictive maintenance. This will translate to improved operational efficiency, reduced downtime, and enhanced customer satisfaction. However, challenges remain. Data security concerns related to connected vehicles and the high cost of developing and implementing advanced diagnostic systems could potentially hinder market growth. Nevertheless, the long-term outlook for the European automotive diagnostic software market remains positive, driven by technological advancements and increasing regulatory pressures. The market's trajectory suggests a steady increase in value and market share over the next decade, indicating significant opportunities for industry players.

Europe Automotive Diagnostic Software Industry Company Market Share

Europe Automotive Diagnostic Software Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe Automotive Diagnostic Software Industry, offering valuable insights for industry professionals, investors, and strategists. Covering the period from 2019 to 2033, with a focus on 2025, this report leverages rigorous data analysis and expert insights to present a clear picture of the market's current state and future trajectory. The market is expected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

Europe Automotive Diagnostic Software Industry Market Structure & Innovation Trends

The European automotive diagnostic software market is characterized by a moderately concentrated structure, with major industry stalwarts such as Robert Bosch GmbH, Continental Automotive AG, and Delphi Automotive PLC commanding substantial market share. Nevertheless, the market presents a vibrant and evolving competitive arena where established giants and agile technology innovators actively contend for leadership. A primary catalyst for innovation is the escalating complexity of modern vehicles, especially the rapid integration of electric vehicles (EVs), which necessitates increasingly sophisticated and efficient diagnostic and repair solutions. Furthermore, the stringent emission regulations and rigorous safety standards mandated by the European Union play a pivotal role in shaping innovation trajectories and accelerating the adoption of advanced diagnostic tools.

- Market Concentration: The market is moderately concentrated, with the top 5 players estimated to hold approximately 60-70% of the market share in 2025.

- Innovation Drivers: Key drivers include the accelerated adoption of Electric Vehicles (EVs), the tightening of emission regulations, the escalating demand for streamlined and cost-effective repair solutions, and continuous advancements in software technology, including AI and IoT integration.

- Regulatory Frameworks: EU directives concerning vehicle emissions, safety standards (e.g., Euro 7, GSR2), and data access for repairers significantly influence market dynamics, compelling the development and adoption of compliant and interoperable diagnostic software.

- Product Substitutes: While direct substitutes are limited, the emergence and increasing sophistication of cloud-based diagnostic platforms and integrated vehicle systems are presenting competitive alternatives to traditional standalone diagnostic tools.

- End-User Demographics: The primary customer base encompasses a broad spectrum of automotive service providers, including franchised dealerships, independent repair workshops, specialized EV service centers, fleet management organizations, and vehicle manufacturers' authorized service networks.

- M&A Activities: The past five years have witnessed a notable surge in strategic acquisitions and partnerships, with an estimated total M&A deal value of approximately €1.5 - €2.5 Billion. These strategic moves are aimed at consolidating market positions, acquiring cutting-edge technological capabilities, broadening product portfolios, and gaining access to new and expanding customer segments.

Europe Automotive Diagnostic Software Industry Market Dynamics & Trends

The European automotive diagnostic software market is currently experiencing a period of robust and sustained growth. This upward trajectory is significantly influenced by several compelling factors. The widespread implementation of Advanced Driver-Assistance Systems (ADAS) and the pervasive proliferation of connected vehicle technologies are directly fueling an increased demand for more advanced and comprehensive diagnostic tools. The burgeoning electric vehicle (EV) market serves as another potent catalyst, necessitating specialized diagnostic software for the intricate management of battery systems and electric powertrains. Consumer expectations are also evolving, with a discernible shift towards enhanced vehicle diagnostics and more efficient, predictive repair services. This dynamic environment fosters an intensely competitive landscape, driving companies to continuously innovate and refine their product and service offerings to achieve differentiation.

A prominent trend shaping the market is the transition from conventional on-site diagnostic solutions towards sophisticated cloud-based platforms. These platforms offer enhanced data analytics capabilities, enabling remote diagnostics, predictive maintenance, and over-the-air (OTA) updates, thereby improving operational efficiency for service providers. Technological advancements, particularly the integration of Artificial Intelligence (AI) and Machine Learning (ML), are revolutionizing diagnostic software, leading to improvements in diagnostic accuracy, speed, and the identification of complex issues. The market penetration of these advanced diagnostic solutions is on a steady ascent, currently estimated at approximately 45-55% in 2025 and projected to reach an impressive 75-85% by 2033.

Dominant Regions & Segments in Europe Automotive Diagnostic Software Industry

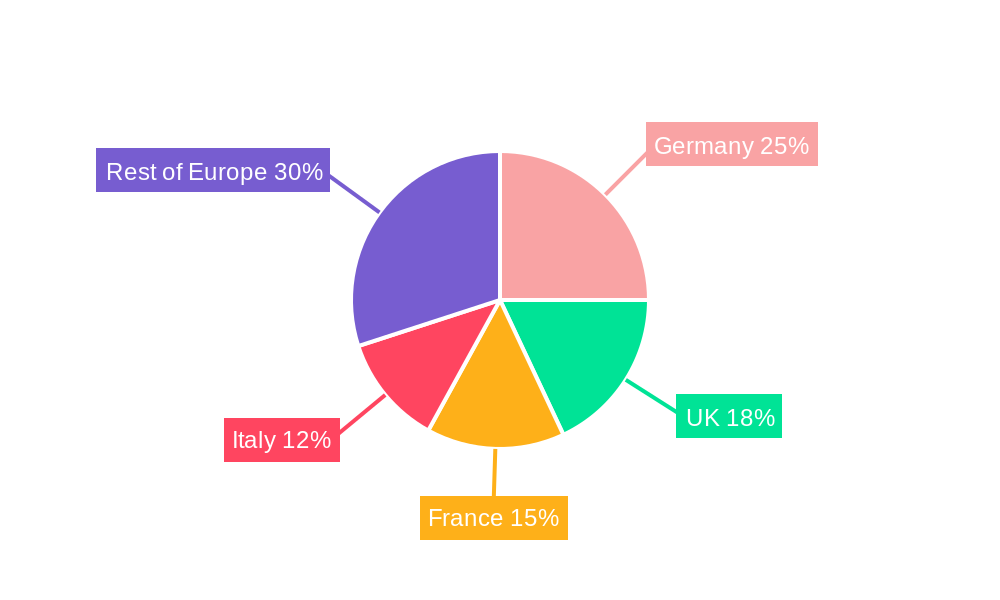

Germany and the United Kingdom are currently the leading markets within Europe, driven by strong automotive manufacturing sectors and a high concentration of repair shops and dealerships. The passenger car segment holds the largest market share, owing to the significantly higher volume compared to commercial vehicles. However, the commercial vehicle segment is projected to experience higher growth, fueled by increasing fleet sizes and stricter regulatory standards.

Key Drivers:

- Germany: Strong automotive manufacturing base, well-developed infrastructure, and high adoption of advanced technologies.

- United Kingdom: Large automotive repair network, robust aftermarket, and significant focus on EV infrastructure development.

- Passenger Cars: High volume, established service infrastructure, and diverse customer base.

- Commercial Vehicles: Stringent emission regulations, increasing fleet sizes, and growing demand for efficient fleet management solutions.

The OBD segment dominates the market by type due to its widespread adoption in modern vehicles. However, the Electric System Analyzer and Scan Tool segments are witnessing rapid growth, particularly due to the rise of EVs and hybrid vehicles.

Europe Automotive Diagnostic Software Industry Product Innovations

Recent product innovations include the integration of AI and ML algorithms to enhance diagnostic accuracy and speed, cloud-based diagnostic platforms for remote monitoring and analysis, and specialized software for EV battery management systems. These innovations cater to the growing demand for efficient, accurate, and cost-effective diagnostic solutions, while enhancing customer satisfaction and reducing downtime. The market is witnessing a trend towards modular and scalable software platforms to accommodate the increasing complexity of modern vehicles.

Report Scope & Segmentation Analysis

This report segments the European automotive diagnostic software market by type (OBD, Electric System Analyzer, Scan Tool) and vehicle type (Passenger Cars, Commercial Vehicles).

By Type:

- OBD: The largest segment, with a projected market size of xx Million in 2025, driven by its widespread adoption in modern vehicles. The segment is expected to maintain a stable growth rate throughout the forecast period.

- Electric System Analyzer: Experiencing rapid growth due to the increasing popularity of EVs and hybrid vehicles. The market size is projected to reach xx Million by 2025.

- Scan Tool: A crucial component of automotive diagnostics, the scan tool segment maintains a significant market share, projected at xx Million in 2025, demonstrating sustained growth.

By Vehicle Type:

- Passenger Cars: Currently the largest segment, with a market size of xx Million in 2025, reflecting the higher overall sales volume.

- Commercial Vehicles: Demonstrates promising growth potential, driven by increasing fleet sizes and stricter regulatory requirements. The market size is anticipated to reach xx Million by 2025.

Key Drivers of Europe Automotive Diagnostic Software Industry Growth

The expansion of the European automotive diagnostic software industry is primarily propelled by a confluence of critical factors. The ever-increasing complexity of automotive systems, particularly with the rapid rise of Electric Vehicles (EVs) and Advanced Driver-Assistance Systems (ADAS), mandates sophisticated diagnostic capabilities. Stringent government regulations aimed at enhancing vehicle safety and controlling emissions (such as Euro 7 standards) are significant drivers, compelling the adoption of advanced diagnostic tools. The burgeoning connected car market generates vast amounts of data that require specialized software for analysis and diagnostics. Furthermore, the growing demand from end-users for more efficient, cost-effective, and predictive vehicle maintenance and repair services is a key propellant. The increasing adoption and proven benefits of cloud-based diagnostic solutions, offering superior data analytics and remote diagnostic capabilities, also significantly contribute to market expansion.

Challenges in the Europe Automotive Diagnostic Software Industry Sector

The Europe automotive diagnostic software industry grapples with several significant challenges. The substantial initial investment required for acquiring advanced diagnostic hardware and sophisticated software licenses can be a barrier, especially for smaller independent garages. The relentless pace of automotive technology evolution necessitates continuous and often costly software updates to ensure compatibility with new vehicle models and electronic control units (ECUs). The inherent complexity of integrating diverse diagnostic systems across a wide array of vehicle brands, models, and software architectures presents a persistent integration challenge. The market is also characterized by intense competition from both deeply entrenched established players and agile, innovative emerging companies, which can pressure profit margins. Moreover, growing concerns surrounding the cybersecurity of connected diagnostic systems and the secure handling of sensitive vehicle data are becoming increasingly critical.

Emerging Opportunities in Europe Automotive Diagnostic Software Industry

Significant opportunities lie in the development of specialized diagnostic software for EVs and hybrid vehicles; the integration of AI and ML algorithms to improve diagnostic accuracy; the expansion of cloud-based diagnostic platforms to provide remote diagnostics and predictive maintenance capabilities; and the development of standardized diagnostic interfaces across different vehicle brands and models. The increasing adoption of autonomous driving technology also presents a substantial opportunity for the development of specialized diagnostic tools.

Leading Players in the Europe Automotive Diagnostic Software Industry Market

- Carman International

- Denso Corporation

- Delphi Automotive PLC

- Continental Automotive AG

- Vector Informatik

- Snap-On Inc

- Actia Group

- General Technology Group

- Robert Bosch GmbH

- KPIT Technologies Ltd

- Hella KGaA Hueck & Co

- Softing AG

Key Developments in Europe Automotive Diagnostic Software Industry

- September 2022: Saietta Group PLC showcased Saietta Electric Drive Diagnostics (SEDD), a comprehensive diagnostic and calibration system for electric vehicles at IAA Transportation.

- December 2022: Otonomo Technologies Ltd. partnered with Groupe Renault to provide fleet customers with enhanced vehicle data insights.

- May 2023: MAHLE GmbH and Midtronics Inc. collaborated to develop service devices for EV Li-ion battery diagnostics and maintenance.

Future Outlook for Europe Automotive Diagnostic Software Industry Market

The future of the European automotive diagnostic software market appears bright, driven by the continued growth of the EV market, advancements in autonomous driving technology, and the increasing demand for connected car services. Strategic opportunities exist for companies that can develop innovative diagnostic solutions tailored to these emerging trends, focusing on cloud-based platforms, AI-powered diagnostics, and seamless integration with vehicle ecosystems. The market is poised for significant expansion, presenting compelling opportunities for growth and innovation.

Europe Automotive Diagnostic Software Industry Segmentation

-

1. Offering

- 1.1. Diagnostic Equipment/Hardware

- 1.2. Diagnostic Software

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

-

3. Workshop Equipment

- 3.1. Exhaust Gas Analyzer

- 3.2. Wheel Alignment Equipment

- 3.3. Paint Scan Equipment

- 3.4. Dynamometer

- 3.5. Headlight Tester

- 3.6. Fuel Injection Diagnostic

- 3.7. Pressure Leak Detection

- 3.8. Engine Analyzer

-

4. End User

- 4.1. Automotive Repair and Maintenance Shops

- 4.2. OEM Dealerships

- 4.3. Fleet Management Companies

- 4.4. Other End Users

Europe Automotive Diagnostic Software Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Spain

- 5. Italy

- 6. Netherlands

- 7. Rest of Europe

Europe Automotive Diagnostic Software Industry Regional Market Share

Geographic Coverage of Europe Automotive Diagnostic Software Industry

Europe Automotive Diagnostic Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Diagnostic Equipment/Hardware

- 5.1.2. Diagnostic Software

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 5.3.1. Exhaust Gas Analyzer

- 5.3.2. Wheel Alignment Equipment

- 5.3.3. Paint Scan Equipment

- 5.3.4. Dynamometer

- 5.3.5. Headlight Tester

- 5.3.6. Fuel Injection Diagnostic

- 5.3.7. Pressure Leak Detection

- 5.3.8. Engine Analyzer

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Automotive Repair and Maintenance Shops

- 5.4.2. OEM Dealerships

- 5.4.3. Fleet Management Companies

- 5.4.4. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Germany

- 5.5.2. United Kingdom

- 5.5.3. France

- 5.5.4. Spain

- 5.5.5. Italy

- 5.5.6. Netherlands

- 5.5.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Diagnostic Equipment/Hardware

- 6.1.2. Diagnostic Software

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 6.3.1. Exhaust Gas Analyzer

- 6.3.2. Wheel Alignment Equipment

- 6.3.3. Paint Scan Equipment

- 6.3.4. Dynamometer

- 6.3.5. Headlight Tester

- 6.3.6. Fuel Injection Diagnostic

- 6.3.7. Pressure Leak Detection

- 6.3.8. Engine Analyzer

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Automotive Repair and Maintenance Shops

- 6.4.2. OEM Dealerships

- 6.4.3. Fleet Management Companies

- 6.4.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. Germany Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 7.1.1. Diagnostic Equipment/Hardware

- 7.1.2. Diagnostic Software

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 7.3.1. Exhaust Gas Analyzer

- 7.3.2. Wheel Alignment Equipment

- 7.3.3. Paint Scan Equipment

- 7.3.4. Dynamometer

- 7.3.5. Headlight Tester

- 7.3.6. Fuel Injection Diagnostic

- 7.3.7. Pressure Leak Detection

- 7.3.8. Engine Analyzer

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Automotive Repair and Maintenance Shops

- 7.4.2. OEM Dealerships

- 7.4.3. Fleet Management Companies

- 7.4.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 8. United Kingdom Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 8.1.1. Diagnostic Equipment/Hardware

- 8.1.2. Diagnostic Software

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 8.3.1. Exhaust Gas Analyzer

- 8.3.2. Wheel Alignment Equipment

- 8.3.3. Paint Scan Equipment

- 8.3.4. Dynamometer

- 8.3.5. Headlight Tester

- 8.3.6. Fuel Injection Diagnostic

- 8.3.7. Pressure Leak Detection

- 8.3.8. Engine Analyzer

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Automotive Repair and Maintenance Shops

- 8.4.2. OEM Dealerships

- 8.4.3. Fleet Management Companies

- 8.4.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 9. France Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 9.1.1. Diagnostic Equipment/Hardware

- 9.1.2. Diagnostic Software

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 9.3.1. Exhaust Gas Analyzer

- 9.3.2. Wheel Alignment Equipment

- 9.3.3. Paint Scan Equipment

- 9.3.4. Dynamometer

- 9.3.5. Headlight Tester

- 9.3.6. Fuel Injection Diagnostic

- 9.3.7. Pressure Leak Detection

- 9.3.8. Engine Analyzer

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Automotive Repair and Maintenance Shops

- 9.4.2. OEM Dealerships

- 9.4.3. Fleet Management Companies

- 9.4.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 10. Spain Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 10.1.1. Diagnostic Equipment/Hardware

- 10.1.2. Diagnostic Software

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 10.3.1. Exhaust Gas Analyzer

- 10.3.2. Wheel Alignment Equipment

- 10.3.3. Paint Scan Equipment

- 10.3.4. Dynamometer

- 10.3.5. Headlight Tester

- 10.3.6. Fuel Injection Diagnostic

- 10.3.7. Pressure Leak Detection

- 10.3.8. Engine Analyzer

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Automotive Repair and Maintenance Shops

- 10.4.2. OEM Dealerships

- 10.4.3. Fleet Management Companies

- 10.4.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 11. Italy Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 11.1.1. Diagnostic Equipment/Hardware

- 11.1.2. Diagnostic Software

- 11.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.2.1. Passenger Cars

- 11.2.2. Commercial Vehicles

- 11.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 11.3.1. Exhaust Gas Analyzer

- 11.3.2. Wheel Alignment Equipment

- 11.3.3. Paint Scan Equipment

- 11.3.4. Dynamometer

- 11.3.5. Headlight Tester

- 11.3.6. Fuel Injection Diagnostic

- 11.3.7. Pressure Leak Detection

- 11.3.8. Engine Analyzer

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Automotive Repair and Maintenance Shops

- 11.4.2. OEM Dealerships

- 11.4.3. Fleet Management Companies

- 11.4.4. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 12. Netherlands Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Offering

- 12.1.1. Diagnostic Equipment/Hardware

- 12.1.2. Diagnostic Software

- 12.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 12.2.1. Passenger Cars

- 12.2.2. Commercial Vehicles

- 12.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 12.3.1. Exhaust Gas Analyzer

- 12.3.2. Wheel Alignment Equipment

- 12.3.3. Paint Scan Equipment

- 12.3.4. Dynamometer

- 12.3.5. Headlight Tester

- 12.3.6. Fuel Injection Diagnostic

- 12.3.7. Pressure Leak Detection

- 12.3.8. Engine Analyzer

- 12.4. Market Analysis, Insights and Forecast - by End User

- 12.4.1. Automotive Repair and Maintenance Shops

- 12.4.2. OEM Dealerships

- 12.4.3. Fleet Management Companies

- 12.4.4. Other End Users

- 12.1. Market Analysis, Insights and Forecast - by Offering

- 13. Rest of Europe Europe Automotive Diagnostic Software Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Offering

- 13.1.1. Diagnostic Equipment/Hardware

- 13.1.2. Diagnostic Software

- 13.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 13.2.1. Passenger Cars

- 13.2.2. Commercial Vehicles

- 13.3. Market Analysis, Insights and Forecast - by Workshop Equipment

- 13.3.1. Exhaust Gas Analyzer

- 13.3.2. Wheel Alignment Equipment

- 13.3.3. Paint Scan Equipment

- 13.3.4. Dynamometer

- 13.3.5. Headlight Tester

- 13.3.6. Fuel Injection Diagnostic

- 13.3.7. Pressure Leak Detection

- 13.3.8. Engine Analyzer

- 13.4. Market Analysis, Insights and Forecast - by End User

- 13.4.1. Automotive Repair and Maintenance Shops

- 13.4.2. OEM Dealerships

- 13.4.3. Fleet Management Companies

- 13.4.4. Other End Users

- 13.1. Market Analysis, Insights and Forecast - by Offering

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Carman International

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Denso Corporation

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Delphi Automotive PLC

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Continental Automotive AG

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Vector Informatik

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Snap-On Inc

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Actia Group

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 General Technology Group

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Robert Bosch GmbH

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 KPIT Technologies Lt

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Hella KGaA Hueck & Co

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 Softing AG

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.1 Carman International

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Automotive Diagnostic Software Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Diagnostic Software Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 2: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 4: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 7: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 9: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 12: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 13: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 14: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 17: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 18: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 19: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 20: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 22: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 23: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 24: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 25: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 27: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 28: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 29: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 32: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 33: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 34: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 35: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 37: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 38: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Workshop Equipment 2020 & 2033

- Table 39: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 40: Europe Automotive Diagnostic Software Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Diagnostic Software Industry?

The projected CAGR is approximately 5.45%.

2. Which companies are prominent players in the Europe Automotive Diagnostic Software Industry?

Key companies in the market include Carman International, Denso Corporation, Delphi Automotive PLC, Continental Automotive AG, Vector Informatik, Snap-On Inc, Actia Group, General Technology Group, Robert Bosch GmbH, KPIT Technologies Lt, Hella KGaA Hueck & Co, Softing AG.

3. What are the main segments of the Europe Automotive Diagnostic Software Industry?

The market segments include Offering, Vehicle Type, Workshop Equipment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.31 Million as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements In Vehicles Driving Demand; Others.

6. What are the notable trends driving market growth?

Increasing Adoption in Passenger and Commercial Vehicles.

7. Are there any restraints impacting market growth?

High Scan Tool Costs to Limit Growth; Others.

8. Can you provide examples of recent developments in the market?

May 2023: MAHLE GmbH and Midtronics Inc. jointly developed service devices for EVs from all manufacturers. The partnership aimed to offer safe, simple, and effective service for Li-ion battery diagnostics and maintenance, regardless of brand, over the entire life cycle of the batteries and vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Diagnostic Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Diagnostic Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Diagnostic Software Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Diagnostic Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence