Key Insights

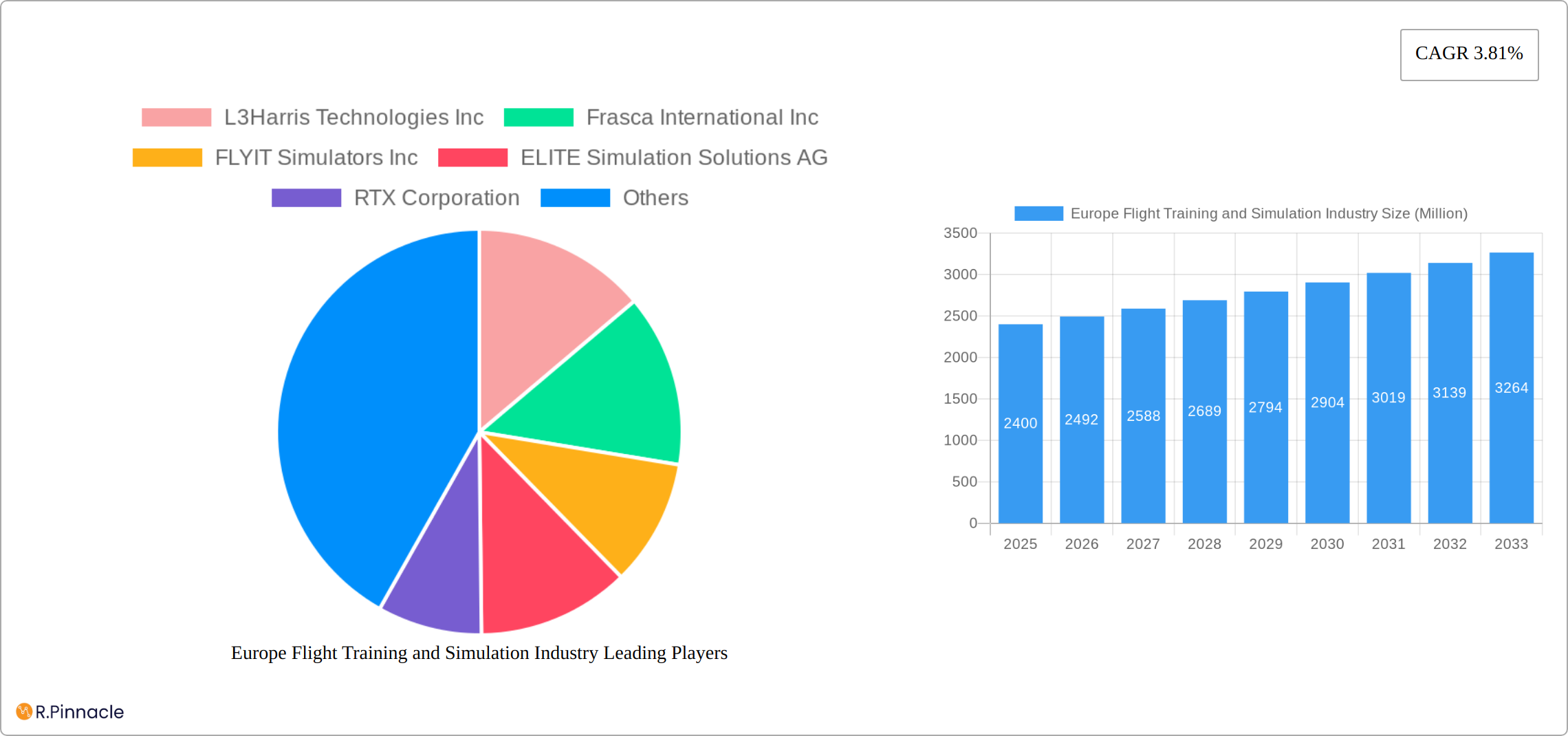

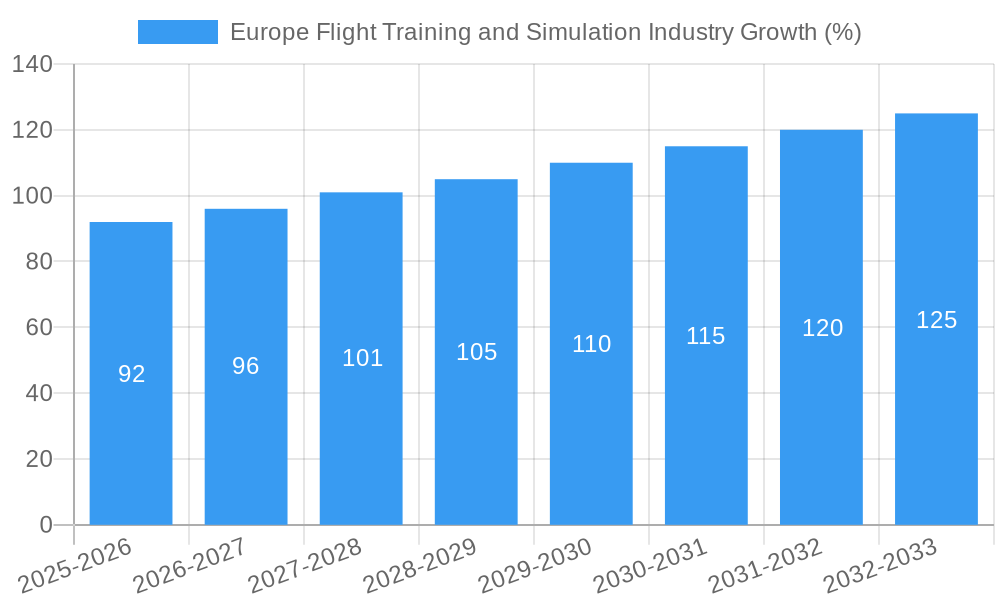

The European flight training and simulation market, valued at €2.4 billion in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 3.81% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, the increasing demand for skilled pilots across commercial and military aviation sectors necessitates enhanced training programs. Secondly, technological advancements in flight simulation, particularly the development of sophisticated Full Flight Simulators (FFS) and Flight Training Devices (FTDs), are improving training efficiency and reducing costs. The integration of advanced technologies such as virtual reality and artificial intelligence further enhances training realism and effectiveness. Finally, stringent safety regulations imposed by aviation authorities are driving the adoption of advanced simulation technologies to meet the required training standards. This is particularly pronounced in regions with significant air traffic, such as Germany, France, and the United Kingdom, which are key contributors to the European market's growth.

The market segmentation reveals a strong preference for Full Flight Simulators (FFS) due to their superior fidelity in replicating real-world flight conditions. However, Flight Training Devices (FTDs) are also gaining traction due to their cost-effectiveness and suitability for basic training. The rotorcraft segment is experiencing growth parallel to the fixed-wing segment driven by the increasing use of helicopters in diverse sectors, including emergency medical services and offshore operations. Key players, including L3Harris Technologies Inc, CAE Inc, and Frasca International Inc, are actively engaged in research and development, introducing innovative products and services to maintain a competitive edge. Competitive dynamics are characterized by strategic partnerships, mergers, and acquisitions, contributing to market consolidation. The market is expected to see continued expansion throughout the forecast period, particularly fueled by investments in next-generation simulation technologies and increased adoption across various training establishments.

Europe Flight Training and Simulation Industry: Market Analysis Report (2019-2033)

This comprehensive report provides an in-depth analysis of the European flight training and simulation industry, covering the period from 2019 to 2033. It offers actionable insights for industry professionals, investors, and stakeholders seeking to understand market dynamics, growth opportunities, and competitive landscapes within this crucial sector. The report leverages extensive market research and data analysis to deliver a detailed forecast, revealing a market projected to reach €XX Million by 2033.

Europe Flight Training and Simulation Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory factors shaping the European flight training and simulation market. The market exhibits a moderately concentrated structure, with key players such as CAE Inc, L3Harris Technologies Inc, and FlightSafety International Inc holding significant market share. However, smaller specialized firms like FLYIT Simulators Inc and ELITE Simulation Solutions AG contribute significantly to innovation.

- Market Concentration: The top 5 players account for approximately XX% of the market share in 2025, indicating a competitive yet consolidated structure.

- Innovation Drivers: Demand for advanced training technologies, stringent safety regulations, and the need for cost-effective training solutions are key drivers for innovation.

- Regulatory Framework: EASA (European Union Aviation Safety Agency) regulations significantly influence the industry standards and technological advancements.

- Product Substitutes: While the core function of flight simulators remains unparalleled, there is increasing use of augmented reality (AR) and virtual reality (VR) technologies as supplementary training aids.

- End-User Demographics: The primary end-users are airlines, flight schools, and military organizations, with growth increasingly driven by low-cost carriers and expanding training needs in emerging economies within Europe.

- M&A Activities: The past five years have seen several significant mergers and acquisitions, with deal values totaling €XX Million. These activities reflect a strategic move towards consolidation and expansion of technological capabilities within the industry.

Europe Flight Training and Simulation Industry Market Dynamics & Trends

The European flight training and simulation market is projected to experience robust growth over the forecast period (2025-2033), driven by a number of factors. The compound annual growth rate (CAGR) is estimated at XX% during this period.

Market growth is fueled by the increasing demand for air travel, a growing number of pilots required to meet this demand, and advancements in training technology leading to increased training efficiency and affordability. The rising adoption of Full Flight Simulators (FFS) and Flight Training Devices (FTD) contributes significantly to market expansion. Technological disruptions such as the integration of AI and the development of more sophisticated simulation software are reshaping the competitive landscape, while increasing focus on sustainable aviation solutions is also shaping the industry. Market penetration of advanced training technologies continues to grow with FFS market penetration predicted to reach XX% by 2033.

Dominant Regions & Segments in Europe Flight Training and Simulation Industry

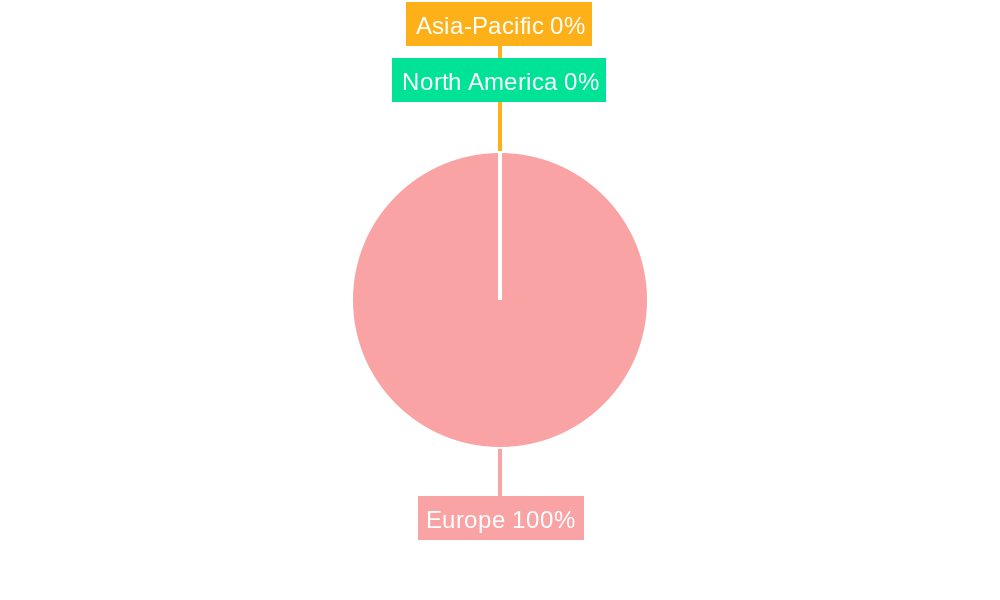

Western Europe, particularly the UK, Germany, and France, holds a commanding position in the European flight training and simulation market. This dominance stems from several key factors: a well-established aviation infrastructure, robust regulatory frameworks fostering innovation, and a high concentration of flight schools and airlines. This mature ecosystem provides a fertile ground for growth and development within the sector.

- Leading Region: Western Europe, driven by its established aviation infrastructure and robust regulatory environment.

- Key Drivers for Western Europe Dominance:

- Extensive aviation infrastructure and a deeply established flight training ecosystem.

- Strong regulatory frameworks from bodies like EASA, encouraging technological innovation and ensuring high safety standards.

- High density of airlines and flight schools, creating a large pool of training needs.

- Significant government funding and investment in aviation training programs, supporting infrastructure development and technological advancements.

Segment Analysis:

- Training Capability: While both fixed-wing and rotorcraft segments are significant, fixed-wing simulators currently command a larger market share due to the proportionally higher number of fixed-wing aircraft operations across Europe. However, growth opportunities exist in the rotorcraft sector.

- Simulator Type: Full Flight Simulators (FFS) currently hold the largest market share, driven by the demand for highly realistic and comprehensive training experiences. Flight Training Devices (FTDs) are experiencing steady growth due to their cost-effectiveness and suitability for certain training phases.

Europe Flight Training and Simulation Industry Product Innovations

Recent innovations include the development of more realistic and immersive simulation environments, enhanced software capabilities that simulate a wider range of operational scenarios, and integration of advanced technologies such as AI and VR for improved training effectiveness and efficiency. This shift is creating a more competitive market, with companies focusing on offering tailored solutions that meet the diverse training needs of their clients. The market is seeing the emergence of more modular and flexible simulator designs, facilitating cost-effective upgrades and adaptations to evolving training requirements.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the European flight training and simulation market, segmented by training capability (rotorcraft and fixed-wing), simulator type (FFS and FTD), and region (Western and Eastern Europe). The report offers detailed insights into market size, growth projections, and the competitive landscape within each segment. Specific focus is given to understanding the dynamics and future trajectories of each market segment.

- Training Capability: The fixed-wing segment is projected to maintain higher growth rates compared to the rotorcraft segment, reflecting the current trends in air travel and aircraft operation numbers.

- Simulator Type: While FFS will continue to dominate the market due to its realistic capabilities, the FTD segment is poised for significant growth, driven by factors such as cost efficiency and technological advancements.

- Regional Segmentation: Western Europe will retain its leading position, but Eastern Europe presents a significant area of emerging opportunity and growth potential, driven by increasing investment in aviation infrastructure and expansion of the airline sector.

Key Drivers of Europe Flight Training and Simulation Industry Growth

The growth trajectory of the European flight training and simulation market is propelled by several key factors:

- Increasing Air Traffic: The continuous rise in air passenger numbers necessitates a substantial increase in the number of qualified pilots, fueling the demand for effective and efficient training solutions.

- Technological Advancements: The integration of cutting-edge technologies such as AI, VR, and AR is revolutionizing training methodologies, enhancing efficacy, and improving cost-effectiveness.

- Stringent Safety Regulations: The European Union Aviation Safety Agency (EASA)'s stringent safety regulations are driving the adoption of advanced training technologies, ensuring the highest standards of pilot proficiency.

- Economic Growth: A healthy European economy fuels investment in aviation infrastructure and training programs, stimulating market expansion.

Challenges in the Europe Flight Training and Simulation Industry Sector

Despite the positive growth outlook, the industry faces several significant challenges:

- High Initial Investment Costs: The acquisition and ongoing maintenance of advanced simulators represent substantial financial commitments for training organizations.

- Regulatory Compliance: Meeting and maintaining compliance with stringent EASA regulations necessitates significant investment in resources and expertise.

- Intense Competition: The market is characterized by intense competition among both established and emerging players, demanding continuous innovation and adaptation.

- Supply Chain Disruptions: Global supply chain vulnerabilities can lead to delays in the procurement of crucial simulator components and software, impacting project timelines and operational efficiency.

These challenges disproportionately affect smaller companies, highlighting the importance of strategic planning and resource management within the sector.

Emerging Opportunities in Europe Flight Training and Simulation Industry

The European flight training and simulation industry is experiencing a wave of emerging opportunities:

- Growth in Low-Cost Carrier Training: The continued expansion of low-cost airlines presents a substantial and growing market segment requiring training solutions.

- Increasing Demand for Specialized Training: The demand for specialized training programs tailored to advanced aircraft types and operational complexities is on the rise.

- Adoption of New Technologies: The integration of AI, VR, and AR offers innovative solutions for improving training effectiveness and efficiency, creating a competitive advantage.

- Focus on Sustainability: A growing emphasis on sustainable aviation practices is driving demand for training solutions that incorporate environmental considerations.

Leading Players in the Europe Flight Training and Simulation Industry Market

- L3Harris Technologies Inc

- Frasca International Inc

- FLYIT Simulators Inc

- ELITE Simulation Solutions AG

- RTX Corporation

- ALSIM EMEA

- CAE Inc

- Multi Pilot Simulations BV

- Thales

- TRU Simulation + Training Inc

- FlightSafety International Inc

- The Boeing Company

Key Developments in Europe Flight Training and Simulation Industry Industry

- 2022 Q4: CAE Inc announced a significant investment in a new training center in France.

- 2023 Q1: L3Harris Technologies Inc launched a new generation of FFS with enhanced VR capabilities.

- 2023 Q2: A merger between two smaller simulation companies created a larger player in the market. (Further details regarding the merger are not available, and therefore xx is used for the value of the merger.) The merger resulted in a combined revenue of €XX Million.

Future Outlook for Europe Flight Training and Simulation Industry Market

The European flight training and simulation market is poised for continued growth, driven by increasing air traffic, technological advancements, and a focus on enhanced safety standards. Strategic opportunities exist for companies that can effectively adapt to emerging technologies and cater to the evolving training needs of airlines and flight schools. The market will witness increasing consolidation and a stronger emphasis on delivering integrated training solutions.

Europe Flight Training and Simulation Industry Segmentation

-

1. Simulator Type

- 1.1. Full Flight Simulator (FFS)

- 1.2. Flight Training Devices (FTD)

-

2. Training Capability

- 2.1. Rotorcraft

- 2.2. Fixed-Wing

Europe Flight Training and Simulation Industry Segmentation By Geography

- 1. United Kingdom

- 2. France

- 3. Germany

- 4. Poland

- 5. Spain

- 6. Italy

- 7. Rest of Europe

Europe Flight Training and Simulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.81% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions

- 3.3. Market Restrains

- 3.3.1. Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data

- 3.4. Market Trends

- 3.4.1. Fixed-wing to Dominate Market Share during the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Simulator Type

- 5.1.1. Full Flight Simulator (FFS)

- 5.1.2. Flight Training Devices (FTD)

- 5.2. Market Analysis, Insights and Forecast - by Training Capability

- 5.2.1. Rotorcraft

- 5.2.2. Fixed-Wing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. France

- 5.3.3. Germany

- 5.3.4. Poland

- 5.3.5. Spain

- 5.3.6. Italy

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Simulator Type

- 6. United Kingdom Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Simulator Type

- 6.1.1. Full Flight Simulator (FFS)

- 6.1.2. Flight Training Devices (FTD)

- 6.2. Market Analysis, Insights and Forecast - by Training Capability

- 6.2.1. Rotorcraft

- 6.2.2. Fixed-Wing

- 6.1. Market Analysis, Insights and Forecast - by Simulator Type

- 7. France Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Simulator Type

- 7.1.1. Full Flight Simulator (FFS)

- 7.1.2. Flight Training Devices (FTD)

- 7.2. Market Analysis, Insights and Forecast - by Training Capability

- 7.2.1. Rotorcraft

- 7.2.2. Fixed-Wing

- 7.1. Market Analysis, Insights and Forecast - by Simulator Type

- 8. Germany Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Simulator Type

- 8.1.1. Full Flight Simulator (FFS)

- 8.1.2. Flight Training Devices (FTD)

- 8.2. Market Analysis, Insights and Forecast - by Training Capability

- 8.2.1. Rotorcraft

- 8.2.2. Fixed-Wing

- 8.1. Market Analysis, Insights and Forecast - by Simulator Type

- 9. Poland Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Simulator Type

- 9.1.1. Full Flight Simulator (FFS)

- 9.1.2. Flight Training Devices (FTD)

- 9.2. Market Analysis, Insights and Forecast - by Training Capability

- 9.2.1. Rotorcraft

- 9.2.2. Fixed-Wing

- 9.1. Market Analysis, Insights and Forecast - by Simulator Type

- 10. Spain Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Simulator Type

- 10.1.1. Full Flight Simulator (FFS)

- 10.1.2. Flight Training Devices (FTD)

- 10.2. Market Analysis, Insights and Forecast - by Training Capability

- 10.2.1. Rotorcraft

- 10.2.2. Fixed-Wing

- 10.1. Market Analysis, Insights and Forecast - by Simulator Type

- 11. Italy Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Simulator Type

- 11.1.1. Full Flight Simulator (FFS)

- 11.1.2. Flight Training Devices (FTD)

- 11.2. Market Analysis, Insights and Forecast - by Training Capability

- 11.2.1. Rotorcraft

- 11.2.2. Fixed-Wing

- 11.1. Market Analysis, Insights and Forecast - by Simulator Type

- 12. Rest of Europe Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - by Simulator Type

- 12.1.1. Full Flight Simulator (FFS)

- 12.1.2. Flight Training Devices (FTD)

- 12.2. Market Analysis, Insights and Forecast - by Training Capability

- 12.2.1. Rotorcraft

- 12.2.2. Fixed-Wing

- 12.1. Market Analysis, Insights and Forecast - by Simulator Type

- 13. Germany Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 14. France Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 15. Italy Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 16. United Kingdom Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 17. Netherlands Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 18. Sweden Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 19. Rest of Europe Europe Flight Training and Simulation Industry Analysis, Insights and Forecast, 2019-2031

- 20. Competitive Analysis

- 20.1. Market Share Analysis 2024

- 20.2. Company Profiles

- 20.2.1 L3Harris Technologies Inc

- 20.2.1.1. Overview

- 20.2.1.2. Products

- 20.2.1.3. SWOT Analysis

- 20.2.1.4. Recent Developments

- 20.2.1.5. Financials (Based on Availability)

- 20.2.2 Frasca International Inc

- 20.2.2.1. Overview

- 20.2.2.2. Products

- 20.2.2.3. SWOT Analysis

- 20.2.2.4. Recent Developments

- 20.2.2.5. Financials (Based on Availability)

- 20.2.3 FLYIT Simulators Inc

- 20.2.3.1. Overview

- 20.2.3.2. Products

- 20.2.3.3. SWOT Analysis

- 20.2.3.4. Recent Developments

- 20.2.3.5. Financials (Based on Availability)

- 20.2.4 ELITE Simulation Solutions AG

- 20.2.4.1. Overview

- 20.2.4.2. Products

- 20.2.4.3. SWOT Analysis

- 20.2.4.4. Recent Developments

- 20.2.4.5. Financials (Based on Availability)

- 20.2.5 RTX Corporation

- 20.2.5.1. Overview

- 20.2.5.2. Products

- 20.2.5.3. SWOT Analysis

- 20.2.5.4. Recent Developments

- 20.2.5.5. Financials (Based on Availability)

- 20.2.6 ALSIM EMEA

- 20.2.6.1. Overview

- 20.2.6.2. Products

- 20.2.6.3. SWOT Analysis

- 20.2.6.4. Recent Developments

- 20.2.6.5. Financials (Based on Availability)

- 20.2.7 CAE Inc

- 20.2.7.1. Overview

- 20.2.7.2. Products

- 20.2.7.3. SWOT Analysis

- 20.2.7.4. Recent Developments

- 20.2.7.5. Financials (Based on Availability)

- 20.2.8 Multi Pilot Simulations BV

- 20.2.8.1. Overview

- 20.2.8.2. Products

- 20.2.8.3. SWOT Analysis

- 20.2.8.4. Recent Developments

- 20.2.8.5. Financials (Based on Availability)

- 20.2.9 Thale

- 20.2.9.1. Overview

- 20.2.9.2. Products

- 20.2.9.3. SWOT Analysis

- 20.2.9.4. Recent Developments

- 20.2.9.5. Financials (Based on Availability)

- 20.2.10 TRU Simulation + Training Inc

- 20.2.10.1. Overview

- 20.2.10.2. Products

- 20.2.10.3. SWOT Analysis

- 20.2.10.4. Recent Developments

- 20.2.10.5. Financials (Based on Availability)

- 20.2.11 FlightSafety International Inc

- 20.2.11.1. Overview

- 20.2.11.2. Products

- 20.2.11.3. SWOT Analysis

- 20.2.11.4. Recent Developments

- 20.2.11.5. Financials (Based on Availability)

- 20.2.12 The Boeing Company

- 20.2.12.1. Overview

- 20.2.12.2. Products

- 20.2.12.3. SWOT Analysis

- 20.2.12.4. Recent Developments

- 20.2.12.5. Financials (Based on Availability)

- 20.2.1 L3Harris Technologies Inc

List of Figures

- Figure 1: Europe Flight Training and Simulation Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Flight Training and Simulation Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 3: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 4: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Flight Training and Simulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 14: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 15: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 17: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 18: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 20: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 21: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 23: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 24: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 26: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 27: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 29: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 30: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 31: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Simulator Type 2019 & 2032

- Table 32: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Training Capability 2019 & 2032

- Table 33: Europe Flight Training and Simulation Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Flight Training and Simulation Industry?

The projected CAGR is approximately 3.81%.

2. Which companies are prominent players in the Europe Flight Training and Simulation Industry?

Key companies in the market include L3Harris Technologies Inc, Frasca International Inc, FLYIT Simulators Inc, ELITE Simulation Solutions AG, RTX Corporation, ALSIM EMEA, CAE Inc, Multi Pilot Simulations BV, Thale, TRU Simulation + Training Inc, FlightSafety International Inc, The Boeing Company.

3. What are the main segments of the Europe Flight Training and Simulation Industry?

The market segments include Simulator Type, Training Capability.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.40 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions.

6. What are the notable trends driving market growth?

Fixed-wing to Dominate Market Share during the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Flight Training and Simulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Flight Training and Simulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Flight Training and Simulation Industry?

To stay informed about further developments, trends, and reports in the Europe Flight Training and Simulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence