Key Insights

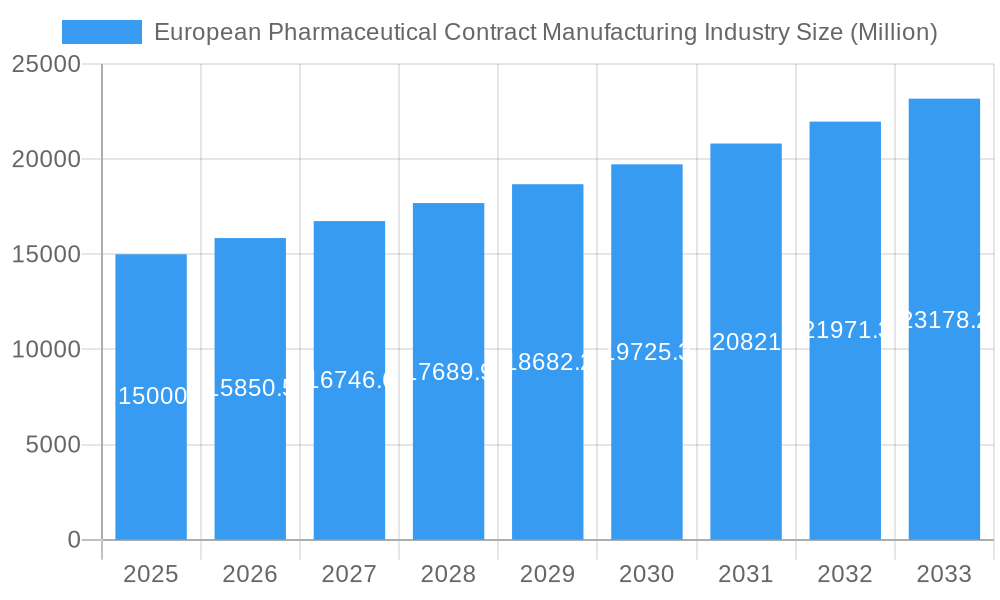

The European pharmaceutical contract manufacturing market, valued at approximately €15 billion in 2025, is projected to experience robust growth, driven by several key factors. The increasing complexity of drug development, coupled with escalating R&D costs, is pushing pharmaceutical companies to outsource manufacturing processes to specialized contract manufacturers (CMOs). This trend is further amplified by the growing demand for innovative therapies, such as biologics and advanced drug delivery systems, which require specialized manufacturing expertise and infrastructure. The market's growth is also fueled by a rise in outsourcing among smaller pharmaceutical firms seeking to streamline operations and reduce capital expenditure, particularly given the substantial investments required for advanced manufacturing technologies. Regulatory changes and increasing focus on quality control and compliance further contribute to the demand for experienced CMOs, driving market expansion. Germany, the UK, and France represent the largest national markets, benefitting from established pharmaceutical ecosystems and a strong presence of major CMOs.

European Pharmaceutical Contract Manufacturing Industry Market Size (In Billion)

Significant growth segments include Active Pharmaceutical Ingredient (API) manufacturing and finished dosage formulation (FDF) development and manufacturing, reflecting the diverse range of services offered by European CMOs. However, the market faces some constraints. These include potential supply chain disruptions, fluctuating raw material costs, and the need for continuous investment in advanced technologies to meet evolving regulatory requirements and maintain a competitive edge. While these challenges exist, the overall outlook for the European pharmaceutical contract manufacturing market remains positive, with a projected Compound Annual Growth Rate (CAGR) of 5.71% from 2025 to 2033, promising substantial growth opportunities for both established players and emerging CMOs within the region. This expansion signifies a strategic shift towards collaborative partnerships in the pharmaceutical industry, fostering innovation and efficiency across the value chain.

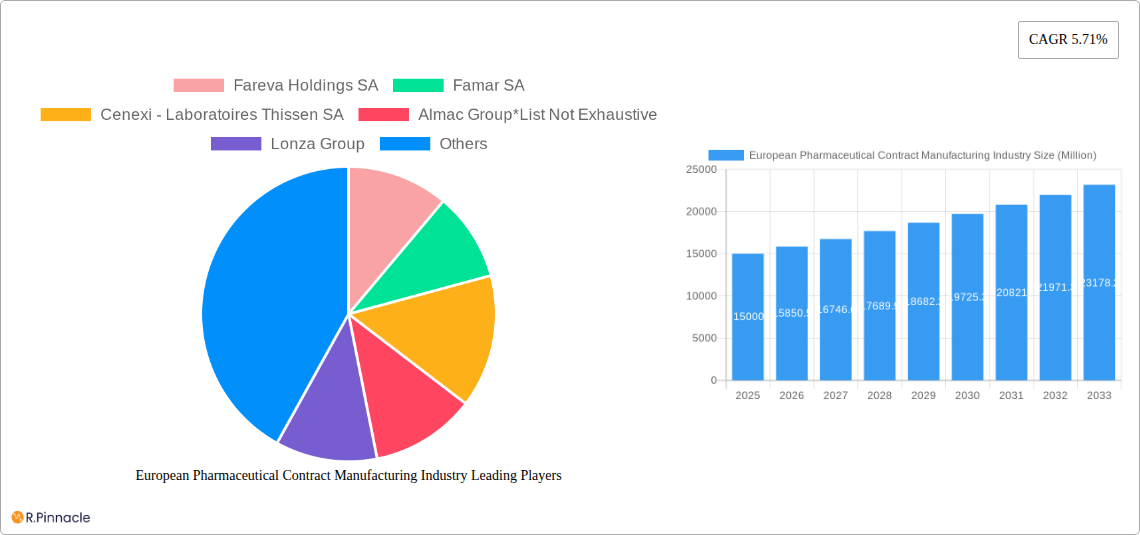

European Pharmaceutical Contract Manufacturing Industry Company Market Share

This comprehensive report provides a detailed analysis of the European Pharmaceutical Contract Manufacturing (PCM) industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a focus on 2025, this report unveils market dynamics, growth drivers, challenges, and future opportunities within this rapidly evolving sector.

European Pharmaceutical Contract Manufacturing Industry Market Structure & Innovation Trends

The European Pharmaceutical Contract Manufacturing (PCM) market is characterized by a moderately concentrated structure, with established leaders like Fareva Holdings SA, Famar SA, Cenexi - Laboratoires Thissen SA, Almac Group, Lonza Group, Aenova Group, Boehringer Ingelheim Group, and Recipharm AB holding substantial market shares. Alongside these giants, a vibrant ecosystem of smaller, highly specialized contract manufacturers fuels a dynamic and competitive landscape. Market analysis for 2024 indicates that the top 5 companies collectively represent approximately [Insert xx% here] of the market, presenting fertile ground for both strategic consolidation and niche player expansion. Innovation is a key differentiator, primarily driven by the escalating demand for advanced drug delivery systems, the burgeoning field of personalized medicine, and the sophisticated manufacturing requirements for biologics. Navigating this complex environment is heavily influenced by stringent regulatory frameworks, notably those established by the EMA (European Medicines Agency), which dictate industry practices and quality standards. While in-house manufacturing capabilities within larger pharmaceutical firms can be considered a form of product substitute, the trend leans towards strategic outsourcing. Merger and acquisition (M&A) activity has been notably robust, with cumulative deal values exceeding €[Insert xx Million here] over the past five years, underscoring a pronounced industry-wide consolidation trajectory. The primary end-user demographic consists of large and mid-sized pharmaceutical companies across the European continent.

European Pharmaceutical Contract Manufacturing Industry Market Dynamics & Trends

The European PCM market exhibits robust growth, driven by increasing outsourcing trends among pharmaceutical companies seeking to optimize costs and focus on core competencies. Technological advancements, particularly in automation and digitalization, are significantly enhancing efficiency and productivity within PCM facilities. Consumer preferences for innovative and personalized medicines fuel the demand for complex drug formulations and sophisticated manufacturing processes. Competitive dynamics are intense, characterized by price competition, service differentiation, and a continuous race for technological superiority. The market is expected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), with market penetration increasing by xx% by 2033. This growth will be particularly driven by the increasing demand for complex formulations and the growing biologics manufacturing segment.

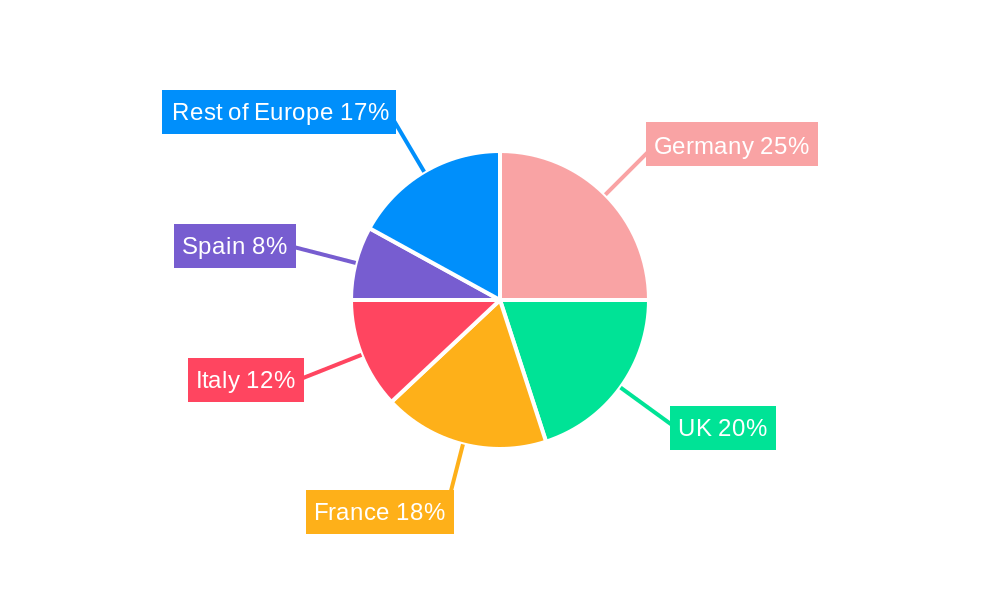

Dominant Regions & Segments in European Pharmaceutical Contract Manufacturing Industry

Dominant Region: Germany consistently leads the European PCM market, driven by a strong pharmaceutical industry presence, advanced infrastructure, and favorable regulatory environments. The UK and France follow as prominent players.

Dominant Segments:

By Service Type: Finished Dosage Formulation (FDF) Development and Manufacturing dominates the market due to higher value-added services and growing demand for complex formulations. API manufacturing, though crucial, represents a relatively smaller segment due to the complexities and investment requirements. Injectable dose formulation and secondary packaging are growing rapidly due to rising demand for injectables, particularly in biologics and biosimilars.

By Country: Germany's dominance stems from a strong concentration of pharmaceutical companies, robust R&D infrastructure, and a skilled workforce. The UK benefits from its established life sciences ecosystem, while France leverages its long history in pharmaceutical manufacturing. Italy and Spain represent significant but smaller markets. The “Rest of Europe” collectively contributes a noteworthy segment to the overall market.

Key Drivers:

- Germany: Strong domestic pharmaceutical industry, highly skilled workforce, robust R&D infrastructure, favorable government policies supporting the life sciences sector.

- UK: Established life sciences ecosystem, strong regulatory environment, access to skilled labor, substantial investments in pharmaceutical research.

- France: Established pharmaceutical manufacturing history, supportive government policies, significant investments in life sciences infrastructure.

European Pharmaceutical Contract Manufacturing Industry Product Innovations

The European Pharmaceutical Contract Manufacturing (PCM) sector is a hotbed of product innovation, propelled by rapid technological advancements. Key developments include the widespread adoption of continuous manufacturing processes, offering enhanced efficiency and real-time quality control. The integration of advanced analytics is revolutionizing process optimization, enabling predictive maintenance and yield improvements. Furthermore, the increasing reliance on single-use technologies is a significant trend, offering paramount benefits in terms of sterility assurance, reduced cross-contamination risks, and significantly shortened cleaning validation timelines. These innovations collectively empower pharmaceutical manufacturers with greater flexibility, heightened operational efficiency, and improved cost-effectiveness. Beyond traditional modalities, the PCM industry is actively developing specialized manufacturing processes to cater to the unique requirements of novel drug modalities, such as cell and gene therapies, opening up significant avenues for growth and strategic differentiation.

Report Scope & Segmentation Analysis

This comprehensive report provides an in-depth analysis of the European Pharmaceutical Contract Manufacturing (PCM) industry. The market is meticulously segmented by service type, encompassing Active Pharmaceutical Ingredient (API) Manufacturing, Finished Dosage Formulation (FDF) Development and Manufacturing, Injectable Dose Formulation, and Secondary Packaging. Additionally, a granular country-level segmentation is provided, including the United Kingdom, Germany, France, Italy, Spain, and the Rest of Europe. For each identified segment, the report offers detailed projections on growth, market size estimations, and a thorough analysis of competitive dynamics. Specific growth rates are projected for each segment over the forecast period of 2025-2033. The report delivers a holistic overview of the current market landscape and provides actionable insights for future growth across all analyzed segments.

Key Drivers of European Pharmaceutical Contract Manufacturing Industry Growth

The European PCM industry's growth is primarily driven by increased outsourcing by pharmaceutical companies, seeking cost optimization and focus on core competencies. Stringent regulations necessitate specialized facilities and expertise, fostering outsourcing. Technological advancements, such as automation and digitalization, boost productivity. Furthermore, the growing demand for complex drug formulations and novel modalities, like biologics and cell therapies, fuel the need for specialized contract manufacturing services.

Challenges in the European Pharmaceutical Contract Manufacturing Industry Sector

The European Pharmaceutical Contract Manufacturing (PCM) sector is navigating a complex landscape of challenges. Paramount among these are the stringent and ever-evolving regulatory compliance requirements, which necessitate significant investment in infrastructure, quality systems, and specialized expertise, thereby increasing operational costs and complexity. Supply chain disruptions, exacerbated by geopolitical volatilities and global economic uncertainties, pose a significant threat to the consistent availability of critical raw materials and can lead to unpredictable production timelines. Furthermore, the industry grapples with intense competition and persistent price pressures from both domestic and international players, compelling a relentless pursuit of innovation and operational efficiency to sustain profitability. These combined pressures collectively impact profitability margins, with an estimated average of [Insert xx% here] for the sector in 2024.

Emerging Opportunities in European Pharmaceutical Contract Manufacturing Industry

Emerging opportunities arise from increasing demand for complex formulations, personalized medicine, and advanced drug delivery systems. The rise of novel drug modalities, like cell and gene therapies, creates specialized manufacturing needs. Expansion into emerging markets within Europe offers further growth potential. Technological advancements, such as continuous manufacturing and AI-driven process optimization, unlock efficiency gains and new service offerings.

Leading Players in the European Pharmaceutical Contract Manufacturing Industry Market

- Fareva Holdings SA

- Famar SA

- Cenexi - Laboratoires Thissen SA

- Almac Group

- Lonza Group

- Aenova Group

- Boehringer Ingelheim Group

- Recipharm AB

Key Developments in European Pharmaceutical Contract Manufacturing Industry Industry

- February 2022: Merck (Germany) restructured its business to strengthen its CDMO business, consolidating services into Life Science Services (LSS).

- March 2022: MorphoSys (Germany) consolidated its R&D operations, incurring a USD 254 Million charge, reflecting industry consolidation trends.

Future Outlook for European Pharmaceutical Contract Manufacturing Industry Market

The European Pharmaceutical Contract Manufacturing (PCM) market is poised for substantial and sustained growth, underpinned by enduring outsourcing trends, continuous technological innovation, and the escalating global demand for increasingly complex pharmaceuticals. Key strategic opportunities for players in this market lie in proactively expanding manufacturing capacities for novel therapeutic modalities, making strategic investments in cutting-edge technologies such as artificial intelligence and advanced automation, and cultivating distinct service offerings to maintain a competitive edge. The market is also anticipated to witness further consolidation, driven by the strategic objectives of larger entities seeking to broaden their market reach and enhance their comprehensive service portfolios.

European Pharmaceutical Contract Manufacturing Industry Segmentation

-

1. Service Type

- 1.1. Active P

-

1.2. Finished

- 1.2.1. Solid Dose Formulation

- 1.2.2. Liquid Dose Formulation

- 1.2.3. Injectable Dose Formulation

- 1.3. Secondary Packaging

European Pharmaceutical Contract Manufacturing Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Pharmaceutical Contract Manufacturing Industry Regional Market Share

Geographic Coverage of European Pharmaceutical Contract Manufacturing Industry

European Pharmaceutical Contract Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Active P

- 5.1.2. Finished

- 5.1.2.1. Solid Dose Formulation

- 5.1.2.2. Liquid Dose Formulation

- 5.1.2.3. Injectable Dose Formulation

- 5.1.3. Secondary Packaging

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. European Pharmaceutical Contract Manufacturing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Active P

- 6.1.2. Finished

- 6.1.2.1. Solid Dose Formulation

- 6.1.2.2. Liquid Dose Formulation

- 6.1.2.3. Injectable Dose Formulation

- 6.1.3. Secondary Packaging

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Fareva Holdings SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Famar SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cenexi - Laboratoires Thissen SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Almac Group*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lonza Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Aenova Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Boehringer Ingelheim Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Recipharm AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Fareva Holdings SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: European Pharmaceutical Contract Manufacturing Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Pharmaceutical Contract Manufacturing Industry Share (%) by Company 2025

List of Tables

- Table 1: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 4: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Pharmaceutical Contract Manufacturing Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the European Pharmaceutical Contract Manufacturing Industry?

Key companies in the market include Fareva Holdings SA, Famar SA, Cenexi - Laboratoires Thissen SA, Almac Group*List Not Exhaustive, Lonza Group, Aenova Group, Boehringer Ingelheim Group, Recipharm AB.

3. What are the main segments of the European Pharmaceutical Contract Manufacturing Industry?

The market segments include Service Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 209.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Outsourcing Volume by Pharmaceutical Companies; Increasing Investment in R&D.

6. What are the notable trends driving market growth?

Rising Investment in R&D will Drive The Market Growth.

7. Are there any restraints impacting market growth?

Increasing Lead Time and Logistics Costs; Stringent Regulatory Requirements; Capacity Utilization Issues Affecting the Profitability of CMOs.

8. Can you provide examples of recent developments in the market?

March 2022: MorphoSys sacked US R&D to consolidate work in Germany, taking USD 254 million in charges. MorphoSys axed its early pipeline and U.S. R&D work that came with the USD 1.7 billion purchase of Constellation Pharmaceuticals, meaning a more than USD 250 million impairment charge as the German pharma shifted the focus home.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Pharmaceutical Contract Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Pharmaceutical Contract Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Pharmaceutical Contract Manufacturing Industry?

To stay informed about further developments, trends, and reports in the European Pharmaceutical Contract Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence