Key Insights

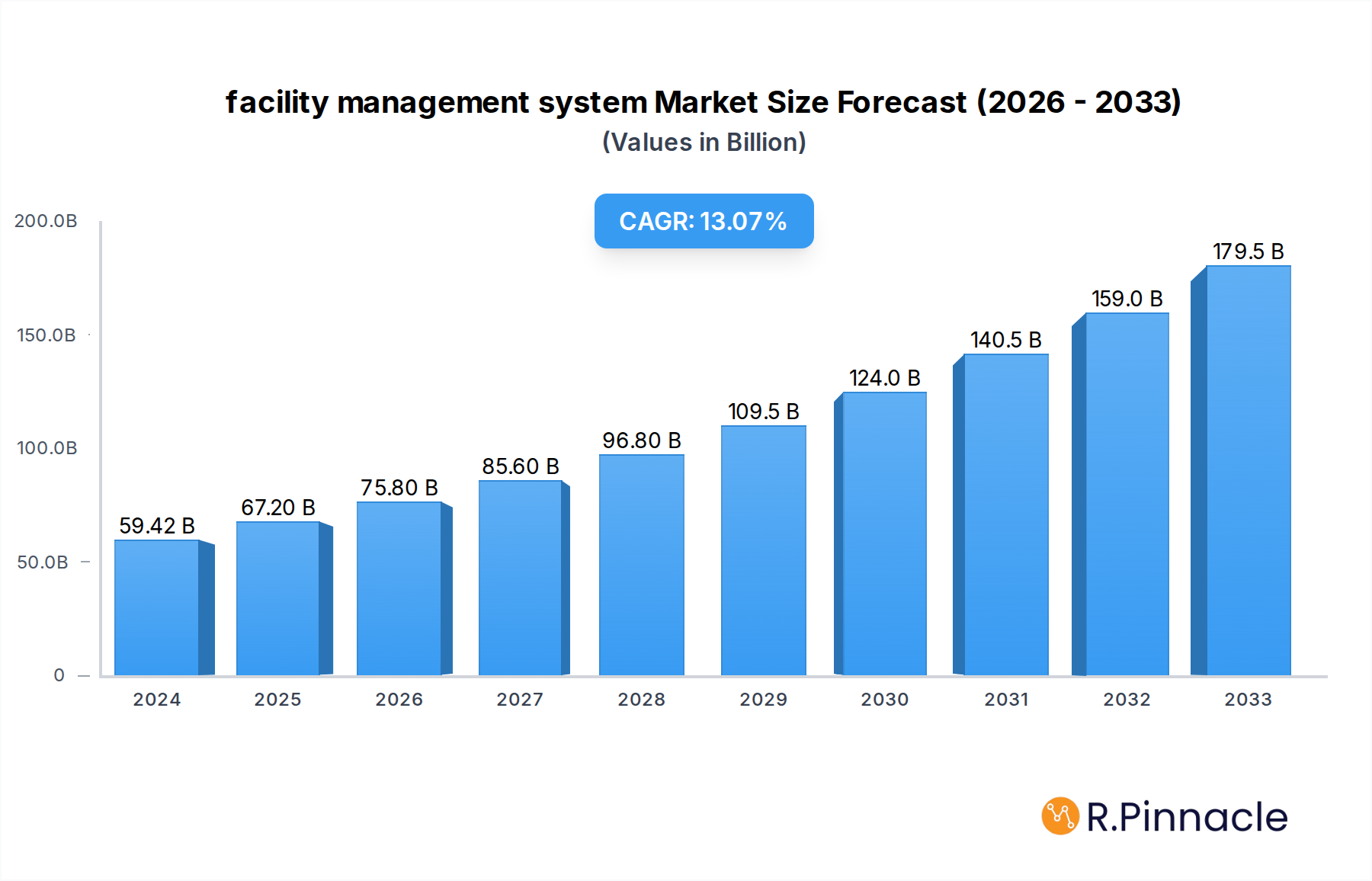

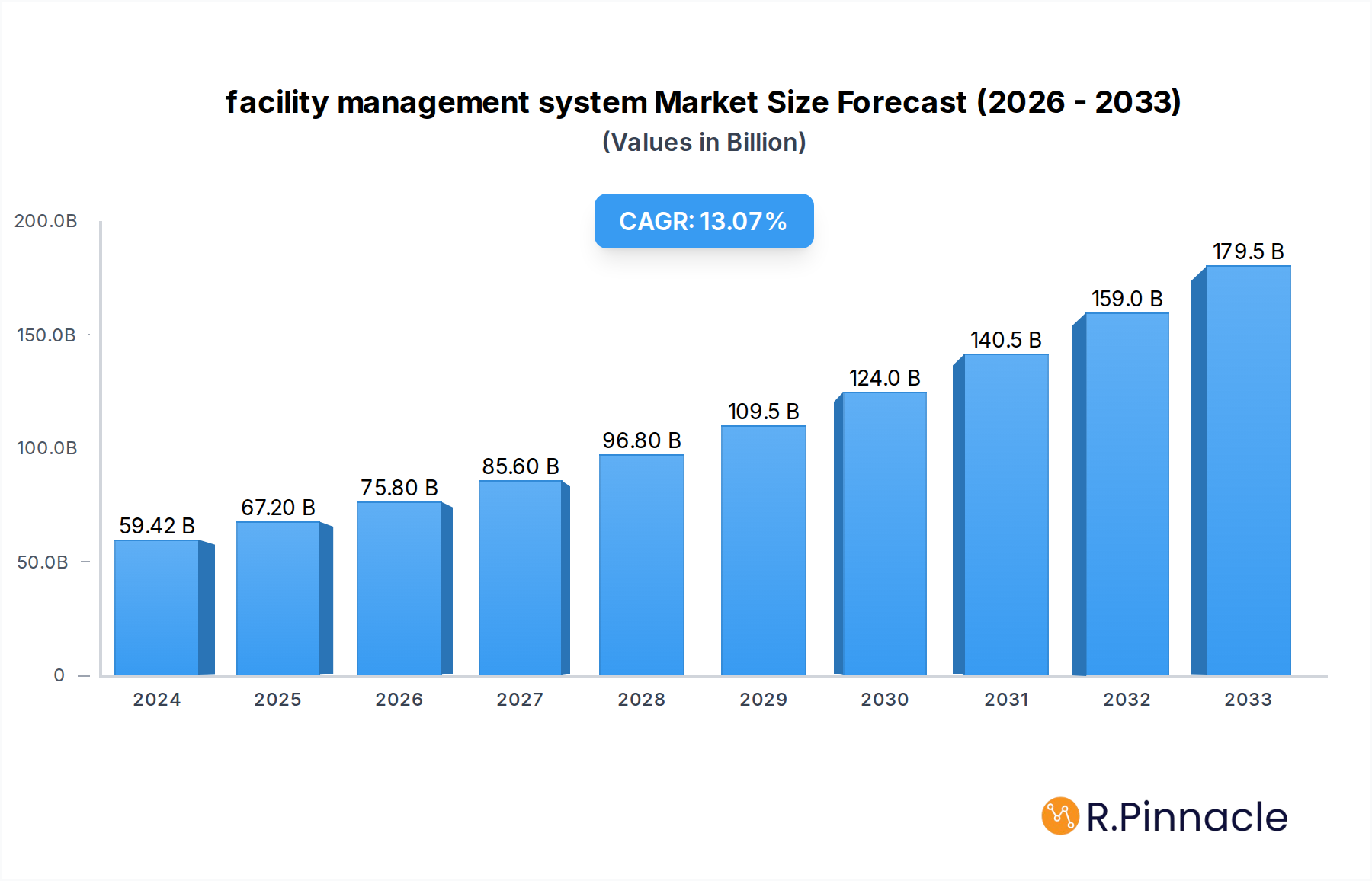

The global facility management system (FMS) market is poised for substantial expansion, projecting a market size of approximately USD 59.42 billion in 2024, with a robust Compound Annual Growth Rate (CAGR) of 12.8% anticipated throughout the forecast period of 2025-2033. This impressive growth trajectory is primarily fueled by the increasing adoption of integrated facility management solutions across diverse organizational structures, from Small and Medium-sized Enterprises (SMEs) to large enterprises. The escalating need for operational efficiency, cost optimization, and enhanced occupant experience are key drivers propelling the market forward. Furthermore, the growing emphasis on smart building technologies and the Internet of Things (IoT) integration within FMS platforms are creating new avenues for market penetration and innovation. Companies are increasingly investing in sophisticated FMS to streamline maintenance operations, manage space utilization effectively, and ensure regulatory compliance, all of which contribute to a more sustainable and productive work environment.

facility management system Market Size (In Billion)

The market is characterized by a strong shift towards cloud-based FMS solutions, offering greater scalability, accessibility, and real-time data analytics compared to traditional local deployment models. This trend is democratizing access to advanced facility management capabilities, particularly for SMEs. Emerging trends include the integration of AI and machine learning for predictive maintenance and energy management, the growing importance of occupant well-being features, and the consolidation of the market through strategic mergers and acquisitions. While the FMS market presents significant opportunities, challenges such as the initial cost of implementation and the need for skilled personnel to manage complex systems may present some headwinds. However, the undeniable benefits in terms of improved asset lifecycle management, reduced operational expenses, and enhanced decision-making capabilities are expected to outweigh these restraints, ensuring a dynamic and growing market landscape.

facility management system Company Market Share

This comprehensive report offers an in-depth analysis of the global Facility Management System (FMS) market, providing actionable insights for industry stakeholders. Covering the historical period from 2019–2024, the base year of 2025, and a forecast period extending to 2033, this report details market structure, dynamics, dominant regions, product innovations, and future outlook. Leveraging high-ranking keywords such as "facility management software," "CMMS," "IWMS," "building management systems," and "integrated workplace management systems," this report is optimized for maximum search visibility and engagement with facility management professionals, IT decision-makers, and business strategists.

facility management system Market Structure & Innovation Trends

The facility management system market exhibits a dynamic structure characterized by both fragmentation and consolidation. While a significant number of vendors cater to niche segments, leading players are actively pursuing M&A to expand their portfolios and market reach. Innovation is a critical driver, fueled by the increasing demand for integrated solutions that streamline operations, enhance sustainability, and improve employee experience. Key innovation trends include the adoption of AI and machine learning for predictive maintenance, IoT integration for real-time data collection, and the rise of mobile-first solutions for on-the-go facility management. Regulatory frameworks, such as data privacy laws and building codes, also shape market development, emphasizing security and compliance. Product substitutes, including manual processes and disparate software solutions, are gradually being replaced by comprehensive FMS platforms. End-user demographics are diverse, ranging from Small and Medium-sized Enterprises (SMEs) to Large Enterprises across various industries. M&A activities are on the rise, with deal values projected to reach billions as companies seek to acquire advanced technologies and expand their customer base. For instance, the market share of leading integrated platform providers is expected to grow by an estimated 30 billion in M&A deal values over the forecast period.

facility management system Market Dynamics & Trends

The global facility management system market is poised for substantial growth, driven by a confluence of technological advancements, evolving business needs, and a growing emphasis on operational efficiency. The market's compound annual growth rate (CAGR) is projected to reach xx% during the forecast period of 2025–2033, reflecting strong underlying demand. Technological disruptions are at the forefront, with the integration of the Internet of Things (IoT) enabling real-time data collection from sensors embedded in buildings and equipment. This influx of data empowers facility managers with predictive maintenance capabilities, significantly reducing downtime and operational costs. Artificial Intelligence (AI) and Machine Learning (ML) algorithms are further enhancing these capabilities by analyzing historical data to predict equipment failures, optimize energy consumption, and personalize occupant experiences. The shift towards cloud-based solutions is a dominant trend, offering scalability, accessibility, and reduced upfront investment for businesses of all sizes. This cloud adoption is projected to increase market penetration by an estimated 40 billion by 2033.

Consumer preferences are increasingly aligning with user-friendly interfaces, mobile accessibility, and integrated functionalities that cover the entire facility lifecycle, from space planning and asset management to maintenance scheduling and sustainability tracking. Businesses are recognizing FMS not just as a tool for operational efficiency but as a strategic asset for enhancing employee productivity, improving safety, and achieving corporate sustainability goals. The competitive landscape is characterized by intense innovation and strategic partnerships. Companies are investing heavily in R&D to develop advanced features such as augmented reality for maintenance tasks and sophisticated analytics for space utilization optimization. The penetration of FMS solutions in the SME segment is expected to witness a significant surge, driven by the availability of affordable, scalable cloud-based options and the growing need for professional facility management practices. The competitive dynamics are pushing vendors to offer comprehensive solutions that cater to the unique requirements of diverse industries, including healthcare, education, and manufacturing. The market is also seeing increased adoption in smart buildings initiatives, where FMS plays a pivotal role in managing the complex interplay of building systems and occupant needs, contributing an estimated 35 billion in market expansion.

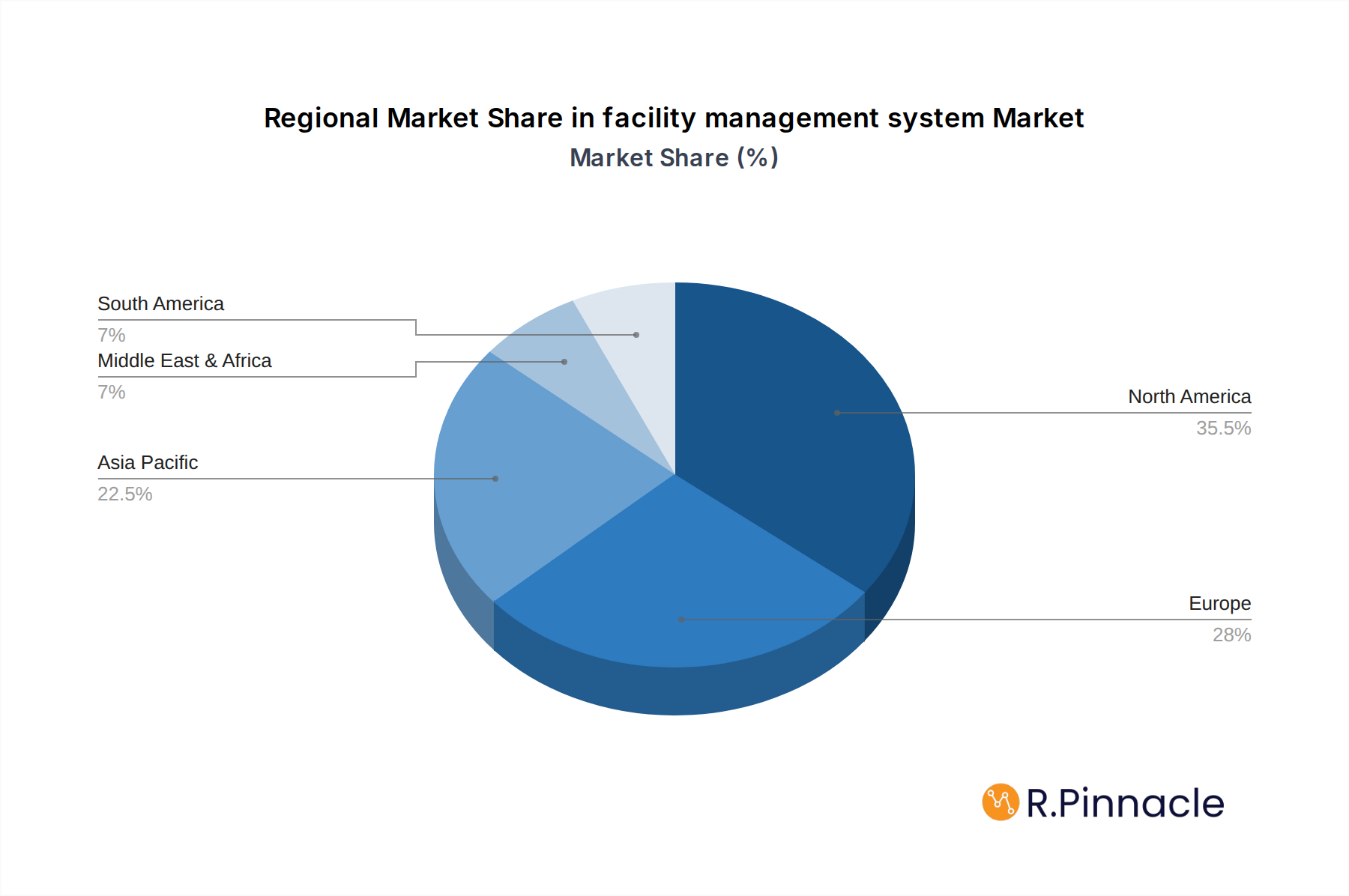

Dominant Regions & Segments in facility management system

The facility management system market exhibits significant regional variations and segment-specific dominance, driven by economic policies, infrastructure development, and industry adoption rates. North America is expected to maintain its leading position throughout the forecast period, bolstered by a mature market for advanced technologies, a strong emphasis on operational efficiency in large enterprises, and substantial investment in smart building initiatives. The United States and Canada are key contributors, with a high adoption rate of cloud-based solutions among both SMEs and Large Enterprises. Economic policies promoting digitalization and sustainability further fuel this dominance.

In terms of application segments, Large Enterprises currently represent the largest share of the market. These organizations typically manage complex portfolios of facilities, requiring robust and integrated solutions for comprehensive asset management, maintenance scheduling, and regulatory compliance. The substantial budgets allocated to facility management in large corporations allow for the widespread adoption of sophisticated FMS platforms. However, the SME segment is projected to witness the fastest growth. As cloud-based FMS becomes more accessible and affordable, SMEs are increasingly leveraging these solutions to professionalize their operations, improve efficiency, and gain a competitive edge. The ease of deployment and scalability of cloud-based FMS are particularly attractive to this segment, contributing an estimated 25 billion in market growth.

Analyzing the types of deployment, Cloud-Based solutions are clearly dominating the market and are expected to continue their upward trajectory. The inherent benefits of cloud deployment, including lower upfront costs, greater flexibility, easier scalability, and enhanced accessibility from any location, make them the preferred choice for businesses of all sizes. This trend is supported by ongoing advancements in cloud infrastructure and security protocols, further enhancing user confidence. Local Deployment, while still relevant for organizations with specific security or regulatory constraints, is experiencing slower growth compared to its cloud-based counterpart. The shift towards cloud adoption is a global phenomenon, with developing regions also witnessing accelerated uptake due to the cost-effectiveness and rapid implementation capabilities of cloud FMS. This widespread adoption of cloud-based solutions is projected to account for an additional xx billion in market expansion by 2033.

facility management system Product Innovations

Product innovation in the facility management system sector is predominantly focused on enhancing automation, intelligence, and user experience. Key developments include the integration of Artificial Intelligence (AI) for predictive maintenance, enabling systems to anticipate equipment failures and schedule repairs proactively, thus minimizing downtime. The proliferation of Internet of Things (IoT) devices is revolutionizing data collection, providing real-time insights into building performance, energy consumption, and occupancy levels. Mobile applications are becoming increasingly sophisticated, empowering facility managers and technicians with on-the-go access to work orders, asset data, and reporting tools. Furthermore, the trend towards integrated workplace management systems (IWMS) is gaining momentum, offering a holistic approach by combining FMS functionalities with space management, asset tracking, and sustainability reporting. These innovations provide significant competitive advantages by improving operational efficiency, reducing costs, and enhancing occupant satisfaction.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global facility management system market across various critical segments. The Application segmentation distinguishes between SMEs and Large Enterprises. SMEs, characterized by smaller operational footprints and budgets, are increasingly adopting scalable, cost-effective cloud-based solutions to streamline their facility operations. Growth projections for the SME segment are robust, driven by the accessibility of modern FMS technologies. Large Enterprises, managing extensive and complex facilities, continue to invest in comprehensive, integrated platforms to optimize their diverse operational needs, representing a significant market share.

The Types of deployment are segmented into Cloud Based and Local Deployment. Cloud-based FMS solutions are experiencing exponential growth due to their flexibility, scalability, and cost-efficiency, making them the preferred choice for a majority of organizations. Local deployment, while still a viable option for entities with strict data sovereignty requirements, exhibits a slower growth rate. The competitive dynamics within the cloud segment are intense, with vendors vying to offer feature-rich, secure, and user-friendly platforms. Market sizes and growth projections are detailed for each segment, providing a granular understanding of the FMS landscape.

Key Drivers of facility management system Growth

The facility management system market is propelled by several key drivers, primarily technological advancements and the increasing imperative for operational efficiency. The widespread adoption of the Internet of Things (IoT) enables real-time data collection from various building systems and assets, facilitating predictive maintenance and optimized resource allocation. Artificial Intelligence (AI) and Machine Learning (ML) are transforming FMS capabilities, allowing for intelligent automation of tasks, energy consumption optimization, and enhanced occupant comfort. Furthermore, the growing emphasis on sustainability and environmental regulations is pushing organizations to implement FMS solutions that can monitor and reduce energy usage, waste, and carbon footprints, contributing an estimated 20 billion in market value. The need to enhance employee productivity and workplace experience is also a significant driver, as effective facility management directly impacts the comfort, safety, and efficiency of the work environment.

Challenges in the facility management system Sector

Despite its strong growth trajectory, the facility management system sector faces several challenges. A significant restraint is the initial cost of implementation and integration, particularly for smaller organizations or those with legacy systems. The lack of skilled personnel to effectively deploy, manage, and leverage advanced FMS technologies can also hinder adoption. Data security and privacy concerns remain paramount, especially with the increasing reliance on cloud-based solutions, necessitating robust cybersecurity measures. Resistance to change and adoption inertia within organizations can slow down the transition from traditional methods to modern FMS. Furthermore, the complexity of integrating disparate systems from various vendors can present technical hurdles, impacting the seamless flow of information and operational efficiency. The estimated impact of these challenges could reduce market growth by approximately 15 billion if not adequately addressed.

Emerging Opportunities in facility management system

The facility management system market is ripe with emerging opportunities driven by technological innovation and evolving business needs. The rise of smart buildings and the Internet of Things (IoT) presents a significant avenue for growth, enabling integrated management of building systems, energy efficiency, and occupant comfort through real-time data analytics. The increasing focus on sustainability and ESG (Environmental, Social, and Governance) goals is creating demand for FMS solutions that can track and report on environmental impact, optimize energy consumption, and promote resource conservation. Artificial Intelligence (AI) and Machine Learning (ML) are opening new frontiers for predictive maintenance, personalized occupant experiences, and automated workflow optimization, offering significant value-added services. The growing demand for remote work enablement and flexible workspace management is also driving the need for agile FMS solutions that can support distributed workforces and optimize space utilization in hybrid work models, contributing an estimated 28 billion in new market potential.

Leading Players in the facility management system Market

- IBM

- Oracle

- SAP

- Broadcom

- Fortive

- Planon

- FM: Systems

- iOFFICE + SpaceIQ

- Nemetschek

- FMX

- eMaint by Fluke

- Apleona

- MRI Software(FSI)

- Indus Systems

- Autodesk

- Officespace

- FacilityONE

Key Developments in facility management system Industry

- 2023 Q4: Oracle announces significant enhancements to its cloud-based FMS suite, focusing on AI-driven predictive maintenance and sustainability reporting.

- 2023 Q3: SAP integrates advanced IoT capabilities into its FMS solutions, enabling real-time building performance monitoring and energy optimization.

- 2023 Q2: Broadcom expands its cybersecurity offerings within its FMS portfolio, addressing growing data security concerns.

- 2023 Q1: Fortive completes the acquisition of a leading FMS provider specializing in asset management, strengthening its market position.

- 2022 Q4: Planon launches a new mobile-first FMS platform designed for enhanced user experience and on-the-go facility management.

- 2022 Q3: FM: Systems partners with a major IoT hardware provider to offer end-to-end smart building solutions.

- 2022 Q2: iOFFICE + SpaceIQ enhances its space management functionalities, addressing the growing needs of hybrid work models.

- 2022 Q1: Nemetschek introduces AI-powered analytics for space utilization and workplace optimization within its FMS offerings.

- 2021 Q4: FMX rolls out advanced features for compliance management and risk assessment in its FMS platform.

- 2021 Q3: eMaint by Fluke introduces a new module for preventative maintenance scheduling, improving asset lifecycle management.

- 2021 Q2: Apleona strategically invests in a startup focused on sustainable facility management technologies.

- 2021 Q1: MRI Software (FSI) acquires a company specializing in real estate and facility management software for the healthcare sector.

- 2020 Q4: Indus Systems enhances its FMS with advanced reporting and dashboard capabilities for better decision-making.

- 2020 Q3: Autodesk integrates its FMS solutions with its BIM (Building Information Modeling) platforms for seamless data flow.

- 2020 Q2: Officespace launches new features for virtual office tours and hybrid work support.

- 2020 Q1: FacilityONE expands its service offerings to include comprehensive sustainability consulting for FMS users.

Future Outlook for facility management system Market

The future outlook for the facility management system market is exceptionally bright, characterized by continuous innovation and expanding applications. The increasing adoption of AI, IoT, and automation will further streamline operations, enabling truly intelligent buildings that adapt to occupant needs and environmental conditions. The growing emphasis on ESG compliance and sustainability will drive demand for FMS solutions that can monitor and reduce environmental impact, making them indispensable tools for corporate responsibility. The market will witness a further surge in cloud adoption, with enhanced security and scalability fostering greater trust. As hybrid work models become entrenched, FMS will play a crucial role in optimizing office space utilization, enhancing employee well-being, and ensuring seamless operational continuity. Strategic partnerships and M&A activities are expected to continue, leading to the consolidation of vendors and the emergence of more comprehensive, integrated platforms that offer end-to-end facility management solutions. The market is projected to unlock billions in new value by enabling greater operational efficiency, cost savings, and enhanced occupant experiences.

facility management system Segmentation

-

1. Application

- 1.1. SMEs

- 1.2. Large Enterprise

-

2. Types

- 2.1. Cloud Based

- 2.2. Local Deployment

facility management system Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

facility management system Regional Market Share

Geographic Coverage of facility management system

facility management system REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global facility management system Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SMEs

- 5.1.2. Large Enterprise

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud Based

- 5.2.2. Local Deployment

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America facility management system Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SMEs

- 6.1.2. Large Enterprise

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud Based

- 6.2.2. Local Deployment

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America facility management system Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SMEs

- 7.1.2. Large Enterprise

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud Based

- 7.2.2. Local Deployment

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe facility management system Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SMEs

- 8.1.2. Large Enterprise

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud Based

- 8.2.2. Local Deployment

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa facility management system Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SMEs

- 9.1.2. Large Enterprise

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud Based

- 9.2.2. Local Deployment

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific facility management system Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SMEs

- 10.1.2. Large Enterprise

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud Based

- 10.2.2. Local Deployment

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 IBM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Oracle

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SAP

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Broadcom

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fortive

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Planon

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 FM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 IBM

List of Figures

- Figure 1: Global facility management system Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America facility management system Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America facility management system Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America facility management system Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America facility management system Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America facility management system Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America facility management system Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America facility management system Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America facility management system Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America facility management system Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America facility management system Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America facility management system Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America facility management system Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe facility management system Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe facility management system Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe facility management system Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe facility management system Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe facility management system Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe facility management system Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa facility management system Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa facility management system Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa facility management system Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa facility management system Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa facility management system Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa facility management system Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific facility management system Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific facility management system Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific facility management system Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific facility management system Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific facility management system Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific facility management system Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global facility management system Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global facility management system Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global facility management system Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global facility management system Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global facility management system Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global facility management system Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global facility management system Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global facility management system Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific facility management system Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the facility management system?

The projected CAGR is approximately 12.8%.

2. Which companies are prominent players in the facility management system?

Key companies in the market include IBM, Oracle, SAP, Broadcom, Fortive, Planon, FM: Systems, iOFFICE + SpaceIQ, Nemetschek, FMX, eMaint by Fluke, Apleona, MRI Software(FSI), Indus Systems, Autodesk, Officespace, FacilityONE.

3. What are the main segments of the facility management system?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "facility management system," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the facility management system report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the facility management system?

To stay informed about further developments, trends, and reports in the facility management system, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence