Key Insights

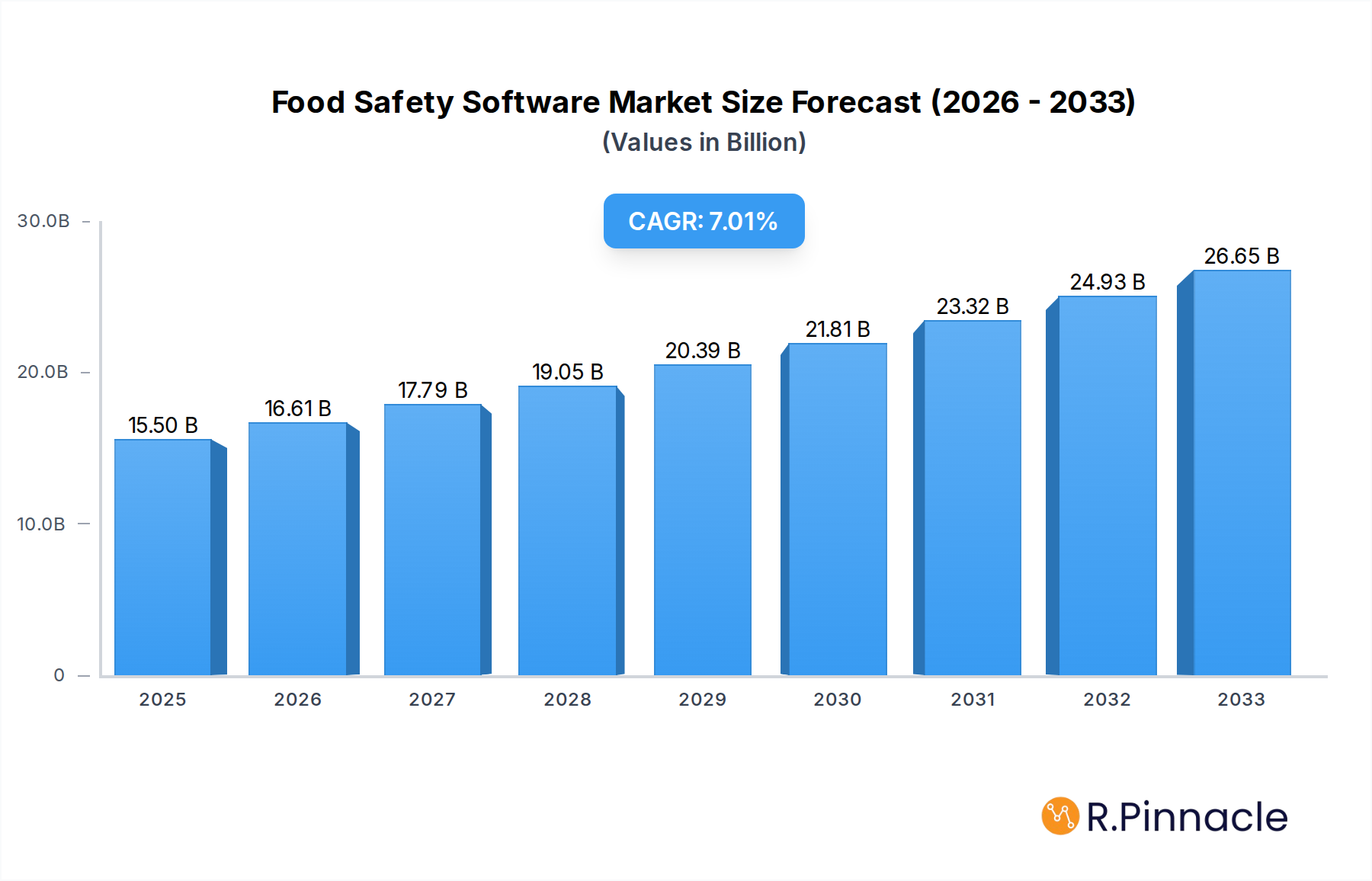

The global Food Safety Software market is poised for robust expansion, projecting a substantial market size of $15.5 billion in 2025. This growth is propelled by a compelling CAGR of 7.11% over the forecast period, indicating a dynamic and expanding industry. The increasing global demand for safe and high-quality food products, coupled with stringent regulatory frameworks across nations, forms the bedrock of this market's expansion. Businesses are increasingly recognizing the critical role of sophisticated software solutions in managing complex supply chains, ensuring compliance, and mitigating the risks associated with foodborne illnesses. The rising awareness among consumers about food safety standards further incentivizes food manufacturers, distributors, and retailers to invest in advanced software to maintain traceability, manage quality control, and streamline recall processes effectively. Emerging markets, with their rapidly growing populations and evolving food industries, represent significant untapped potential for further market penetration and growth.

Food Safety Software Market Size (In Billion)

Key drivers fueling this market's ascent include the growing need for enhanced traceability throughout the food supply chain, from farm to fork, and the imperative to comply with an ever-increasing number of global and regional food safety regulations. The adoption of cloud-based solutions is accelerating, offering scalability, accessibility, and cost-effectiveness, particularly for Small and Medium-sized Enterprises (SMEs) seeking to modernize their food safety protocols without significant upfront infrastructure investment. Conversely, challenges such as the high initial implementation costs for some complex systems and the need for extensive employee training can act as minor restraints. However, the overwhelming benefits of improved operational efficiency, reduced compliance risks, and enhanced brand reputation are expected to outweigh these hurdles. The market is characterized by a diverse range of solutions, catering to both Large Enterprises and SMEs, with specialized applications designed for various stages of the food production and distribution lifecycle.

Food Safety Software Company Market Share

Comprehensive Food Safety Software Market Report: Navigate the Evolving Landscape

This in-depth report provides a definitive analysis of the global Food Safety Software market, offering actionable insights and strategic guidance for stakeholders. Covering the period from 2019 to 2033, with a base year of 2025, this report leverages extensive data to forecast market trajectories and identify key growth opportunities.

Food Safety Software Market Structure & Innovation Trends

The food safety software market is characterized by a dynamic structure driven by increasing regulatory scrutiny and the growing imperative for proactive risk management within the food and beverage industry. Market concentration varies by segment, with established players like MasterControl and Odoo holding significant market share in enterprise solutions, while niche providers cater to SMEs. Innovation is primarily fueled by advancements in Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT), enabling predictive analytics, real-time monitoring, and enhanced traceability. Regulatory frameworks, such as HACCP, FSMA, and GFSI standards, are robust and continuously evolving, pushing companies to adopt sophisticated compliance solutions. Product substitutes, while present in manual or less integrated systems, are increasingly being outpaced by the comprehensive capabilities offered by dedicated software. End-user demographics span the entire food value chain, from primary producers to retailers, with a significant focus on large enterprises seeking scalable and integrated solutions, alongside a growing demand from SMEs requiring cost-effective and user-friendly platforms. Mergers and acquisitions (M&A) activities are on the rise, with reported deal values in the range of hundreds of billions of dollars, as larger companies seek to acquire innovative technologies and expand their market reach.

- Market Concentration: Moderate to High in enterprise segments, evolving in SME segments.

- Innovation Drivers: AI, ML, IoT, Blockchain, cloud computing.

- Regulatory Impact: Significant driver for software adoption and feature development.

- M&A Activity: Increasing, with deal values in the hundreds of billions.

Food Safety Software Market Dynamics & Trends

The food safety software market is poised for substantial growth, driven by a confluence of factors that are reshaping industry practices. A key growth driver is the escalating consumer demand for transparent and ethically sourced food products, compelling businesses to invest in technologies that ensure end-to-end traceability and verifiable safety standards. Technological disruptions are a constant, with cloud-based solutions gaining widespread adoption due to their scalability, accessibility, and cost-effectiveness. On-premises solutions, while still relevant for highly regulated environments or specific IT infrastructures, are seeing a slower growth trajectory. Consumer preferences are increasingly shifting towards brands that can demonstrably prove their commitment to food safety, leading to a premium placed on robust software systems. The competitive landscape is intensifying, with companies differentiating themselves through advanced feature sets, industry-specific customization, and exceptional customer support. The CAGR for the food safety software market is projected to be in the high teens, indicating a robust expansion. Market penetration is still relatively low in certain emerging economies, presenting significant untapped potential. The focus on preventative measures, driven by data analytics and risk assessment capabilities inherent in modern software, is a significant trend, moving away from reactive recall management towards proactive safety assurance. Furthermore, the integration of food safety software with broader enterprise resource planning (ERP) systems is becoming a standard expectation, facilitating seamless data flow and operational efficiency across the entire organization. The evolving nature of foodborne illnesses and recalls, coupled with stringent global food regulations, continually pushes the boundaries of what food safety software needs to achieve, emphasizing real-time data capture, immediate alert systems, and comprehensive audit trails.

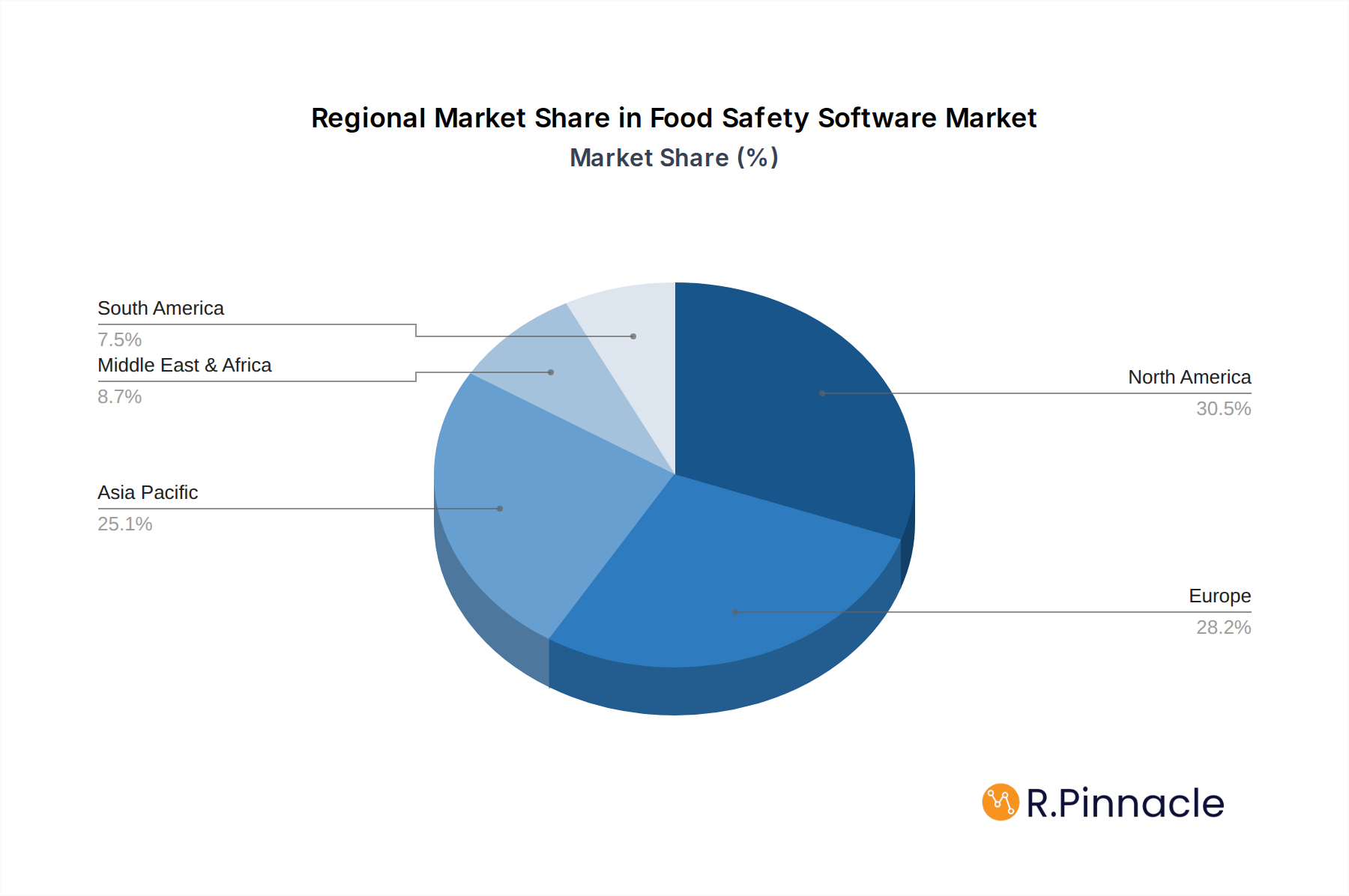

Dominant Regions & Segments in Food Safety Software

North America currently holds a dominant position in the global food safety software market, driven by its advanced regulatory landscape, high consumer awareness regarding food safety, and a mature food and beverage industry with substantial investment capacity. Within North America, the United States spearheads this dominance due to stringent federal regulations like the Food Safety Modernization Act (FSMA), which mandates proactive prevention strategies and sophisticated record-keeping. Economically, the region boasts robust infrastructure and a strong emphasis on technological adoption across all business sizes.

In terms of application, Large Enterprises represent the largest and most influential segment. These organizations, often multinational corporations, face complex supply chains, extensive product portfolios, and rigorous compliance demands. Their need for comprehensive, integrated, and scalable solutions to manage global food safety operations makes them primary adopters of advanced food safety software. The market share of this segment is substantial, exceeding seventy billion dollars in market valuation.

The Cloud-based deployment type is experiencing the most rapid growth and is quickly becoming the preferred choice across all enterprise sizes. This dominance is fueled by the inherent advantages of cloud solutions: lower upfront costs, enhanced accessibility from any location, automatic updates and maintenance, and superior scalability to accommodate fluctuating business needs. The flexibility and cost-effectiveness of cloud platforms enable even SMEs to access sophisticated food safety management tools.

- Leading Region: North America, particularly the United States.

- Key Drivers: Stringent regulations (FSMA), high consumer awareness, advanced industry infrastructure, significant R&D investment.

- Dominant Application Segment: Large Enterprises.

- Key Drivers: Complex supply chains, global operations, high compliance requirements, need for integrated enterprise-wide solutions, substantial IT budgets.

- Market Size: Estimated market valuation of over seventy billion dollars.

- Dominant Deployment Type: Cloud-based.

- Key Drivers: Scalability, accessibility, cost-effectiveness, reduced IT overhead, automatic updates, ease of integration.

Food Safety Software Product Innovations

Food safety software is undergoing a significant evolution, with product innovations focusing on AI-driven risk assessment, real-time IoT sensor integration for environmental monitoring, and blockchain for enhanced supply chain traceability. These advancements are creating a competitive advantage by enabling predictive capabilities for potential hazards, automating compliance checks, and providing immutable records of product journeys. Applications now extend beyond basic compliance to encompass proactive quality control, waste reduction, and consumer engagement.

Report Scope & Segmentation Analysis

This report meticulously segments the global Food Safety Software market to provide granular insights into its diverse landscape. The analysis covers key segmentation criteria, including application and deployment type, offering a comprehensive view of market dynamics and growth projections. Each segment is analyzed with respect to its current market size and projected future growth, alongside the competitive strategies employed by key players within that specific niche.

- Application: Large Enterprises: This segment is characterized by substantial market size and a high demand for integrated, scalable solutions. Projections indicate continued strong growth as these enterprises invest in advanced compliance and risk management technologies. Competitive dynamics are driven by feature richness and integration capabilities.

- Application: SMEs: While historically a smaller segment, SMEs are increasingly adopting food safety software due to rising regulatory pressures and the availability of more affordable, user-friendly cloud-based solutions. Growth is expected to be robust as awareness and accessibility increase.

- Type: Cloud-based: This segment is the fastest-growing, driven by its inherent advantages in scalability, cost-effectiveness, and accessibility. Market size is rapidly expanding, with significant growth projections. Competitive dynamics focus on ease of use, integration, and subscription models.

- Type: On-premises: This segment, while more mature, continues to hold relevance for specific industries or organizations with strict data sovereignty requirements. Growth is expected to be moderate compared to cloud solutions, with competitive strategies focusing on security and customization for complex IT environments.

Key Drivers of Food Safety Software Growth

The global Food Safety Software market is experiencing robust expansion driven by several interconnected factors. Increasingly stringent global regulations, such as FSMA in the US and similar mandates in Europe and Asia, compel food businesses to implement sophisticated software for compliance and traceability. Consumer demand for safe, transparently sourced food products is a significant accelerator, pushing companies to invest in solutions that provide end-to-end visibility. Technological advancements, including AI, machine learning, and IoT, are enabling more predictive and proactive food safety management, moving beyond reactive recall processes. Economic factors, such as a growing global population and increased disposable income, translate to a larger food market and, consequently, a greater need for comprehensive safety solutions.

Challenges in the Food Safety Software Sector

Despite the strong growth trajectory, the Food Safety Software sector faces several hurdles. High initial implementation costs can be a barrier for smaller businesses, particularly those with limited IT budgets. The complexity of integrating new software with existing legacy systems often presents significant technical challenges and requires substantial investment in IT infrastructure and training. Cybersecurity concerns are paramount, as a data breach in food safety systems can have catastrophic consequences for brand reputation and consumer trust. Furthermore, a lack of standardized data formats across different software solutions and supply chain partners can hinder seamless data flow and interoperability, impacting overall effectiveness.

Emerging Opportunities in Food Safety Software

Significant opportunities exist within the Food Safety Software market, particularly in leveraging emerging technologies and expanding into underserved regions. The increasing adoption of blockchain technology offers a revolutionary approach to supply chain transparency and traceability, creating immutable records that build consumer confidence. The expansion of IoT sensors for real-time monitoring of temperature, humidity, and other critical parameters within storage and transit provides invaluable data for proactive risk mitigation. Furthermore, the growing markets in Asia-Pacific and Latin America present substantial untapped potential as these regions increasingly prioritize food safety and adopt advanced technological solutions. The development of specialized software modules catering to specific food categories, such as dairy, meat, or produce, also presents a lucrative avenue for growth.

Leading Players in the Food Safety Software Market

- Fishbowl

- Odoo

- 3DS

- ERPAG

- Quickbase

- iAuditor

- MasterControl

- Prodsmart

- Qualtrax

- PARSEC

- SQCpack

- Qooling

- DevonWay

- Intellect

- QT9 QMS

- Adaptive Compliance Engine (ACE)

- interfacing

Key Developments in Food Safety Software Industry

- 2023 Q4: Increased adoption of AI for predictive food spoilage detection by major food manufacturers.

- 2023 Q3: Launch of advanced blockchain-enabled traceability solutions by several key vendors.

- 2023 Q2: Significant M&A activity with acquisition of smaller, specialized compliance software firms by larger players, aiming to broaden product portfolios.

- 2023 Q1: Growing emphasis on cloud-native solutions for enhanced scalability and remote accessibility in response to evolving work environments.

- 2022 Q4: Integration of IoT sensor data into food safety dashboards for real-time environmental monitoring and alerts.

- 2022 Q3: Release of enhanced features for allergen management and recall execution by leading software providers.

- 2022 Q2: Increased demand for software supporting GFSI (Global Food Safety Initiative) standards across diverse global markets.

- 2022 Q1: Development of predictive analytics modules to forecast potential food safety risks based on historical data and external factors.

- 2021: Emergence of mobile-first solutions for on-the-go data capture and compliance checks in food production and distribution facilities.

- 2020: Accelerated adoption of digital record-keeping and cloud-based systems in response to the global pandemic's impact on supply chains and workforce management.

Future Outlook for Food Safety Software Market

The future outlook for the Food Safety Software market is exceptionally bright, projecting sustained double-digit growth over the forecast period. The increasing digitalization of the food industry, coupled with ever-evolving consumer expectations and regulatory mandates, will continue to fuel demand. Innovations in AI, IoT, and blockchain will become increasingly integral, enabling a more proactive, transparent, and efficient approach to food safety management. Strategic opportunities lie in catering to the burgeoning SME segment with tailored, cost-effective solutions and expanding market penetration in emerging economies. Companies that can offer integrated, data-driven platforms with robust cybersecurity will be best positioned to capitalize on the market's immense potential and secure a dominant position in the years to come.

Food Safety Software Segmentation

-

1. Application

- 1.1. Large Enterpries

- 1.2. SMEs

-

2. Type

- 2.1. Cloud-based

- 2.2. On-premises

Food Safety Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Safety Software Regional Market Share

Geographic Coverage of Food Safety Software

Food Safety Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Enterpries

- 5.1.2. SMEs

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud-based

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Enterpries

- 6.1.2. SMEs

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud-based

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Enterpries

- 7.1.2. SMEs

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud-based

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Enterpries

- 8.1.2. SMEs

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud-based

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Enterpries

- 9.1.2. SMEs

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud-based

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Food Safety Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Enterpries

- 10.1.2. SMEs

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud-based

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Fishbowl

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Odoo

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 3DS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ERPAG

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Quickbase

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 iAuditor

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 MasterControl

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Prodsmart

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Qualtrax

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 PARSEC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 SQCpack

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Qooling

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 DevonWay

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Intellect

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 QT9 QMS

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Adaptive Compliance Engine (ACE)

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 interfacing

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Fishbowl

List of Figures

- Figure 1: Global Food Safety Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Food Safety Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Food Safety Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Safety Software Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Food Safety Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Food Safety Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Food Safety Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Safety Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Food Safety Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Safety Software Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Food Safety Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Food Safety Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Food Safety Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Safety Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Food Safety Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Safety Software Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Food Safety Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Food Safety Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Food Safety Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Safety Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Safety Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Safety Software Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Food Safety Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Food Safety Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Safety Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Safety Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Safety Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Safety Software Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Food Safety Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Food Safety Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Safety Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Food Safety Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Food Safety Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Food Safety Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Food Safety Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Food Safety Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Food Safety Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Food Safety Software Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Food Safety Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Safety Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Safety Software?

The projected CAGR is approximately 7.11%.

2. Which companies are prominent players in the Food Safety Software?

Key companies in the market include Fishbowl, Odoo, 3DS, ERPAG, Quickbase, iAuditor, MasterControl, Prodsmart, Qualtrax, PARSEC, SQCpack, Qooling, DevonWay, Intellect, QT9 QMS, Adaptive Compliance Engine (ACE), interfacing.

3. What are the main segments of the Food Safety Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Safety Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Safety Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Safety Software?

To stay informed about further developments, trends, and reports in the Food Safety Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence