Key Insights

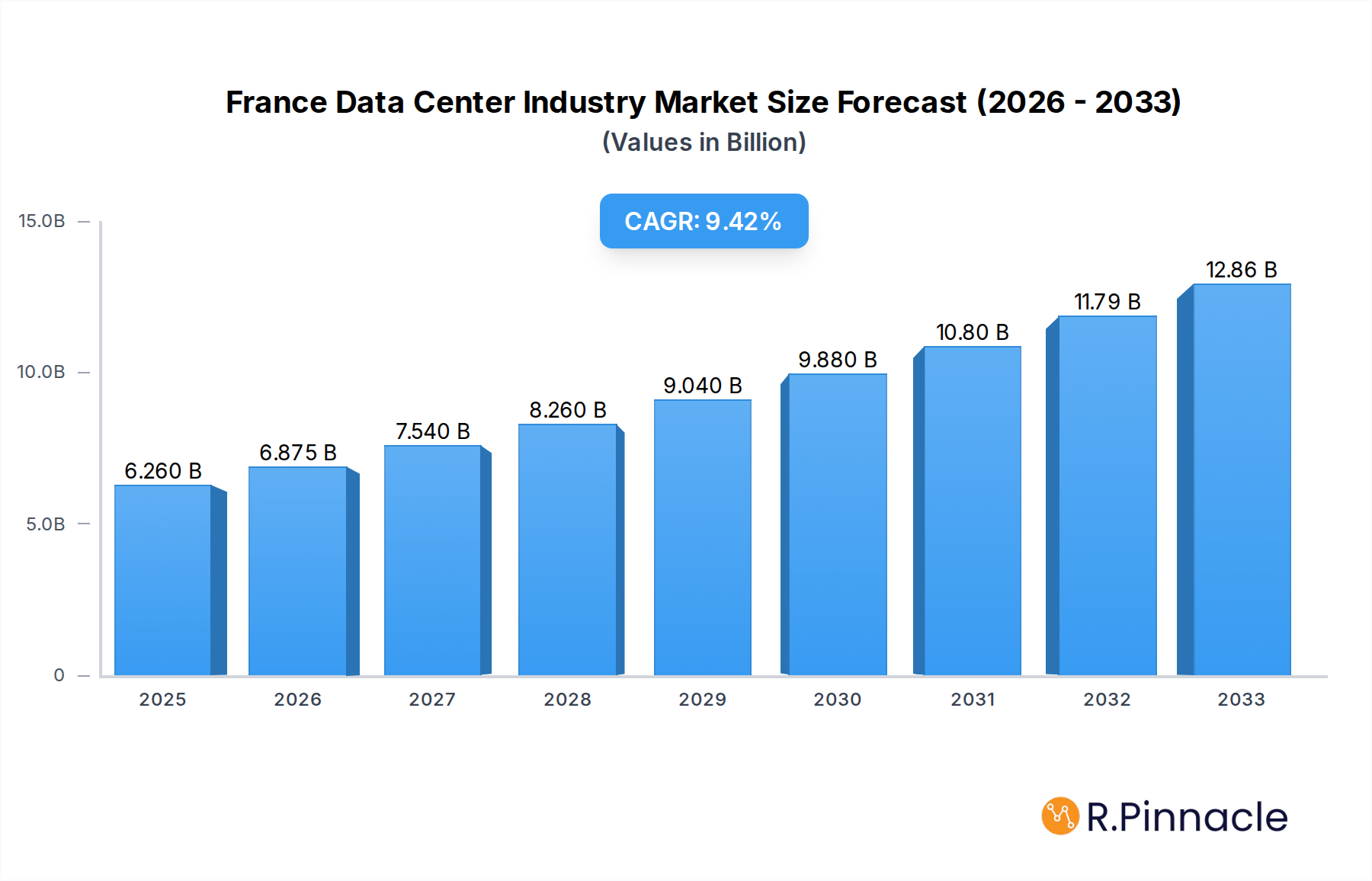

The French data center industry is poised for significant expansion, driven by an increasing demand for digital infrastructure and cloud services. The market is estimated to reach a substantial USD 6.26 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of 9.84% through 2033. This robust growth is fueled by escalating data generation from diverse end-user segments, including BFSI, cloud providers, e-commerce platforms, government agencies, and the burgeoning media & entertainment sector. The ongoing digital transformation across all industries, coupled with the continuous evolution of 5G technology and the Internet of Things (IoT), necessitates greater data processing and storage capabilities, directly impacting the demand for advanced data center solutions. Furthermore, the strategic importance of France as a continental hub, particularly with Paris and its surrounding Ile-De-France region leading the way, is a critical factor in this expansion. The increasing adoption of hyperscale and wholesale colocation models by major cloud providers is also a significant growth driver, indicating a shift towards larger, more centralized facilities.

France Data Center Industry Market Size (In Billion)

The market landscape is characterized by a dynamic interplay of trends and a clear segmentation across various parameters. The prevalence of large and massive data center sizes, along with a focus on Tier 3 and Tier 4 facilities, highlights the industry's commitment to reliability, security, and high availability for critical workloads. While the availability of non-utilized space offers immediate capacity for new entrants and expansions, the long-term growth trajectory points towards increasing absorption rates. Key players like Equinix, Interxion (Digital Reality Trust), and Scaleway SAS are actively investing in expanding their footprint and capabilities to meet the surging demand. Emerging trends such as edge computing, increasing power efficiency demands, and a focus on sustainability are also shaping the future of the French data center market, promising further innovation and investment in the coming years.

France Data Center Industry Company Market Share

This comprehensive report provides an in-depth analysis of the France Data Center Industry, offering critical insights for stakeholders navigating this rapidly evolving market. Covering the historical period from 2019 to 2024 and projecting growth through 2033, this study leverages current data and expert analysis to deliver actionable intelligence.

France Data Center Industry Market Structure & Innovation Trends

The France data center industry exhibits a moderately consolidated structure, with key players like Digital Reality Trust Inc. (Interxion), Equinix Inc., and Scaleway SAS (Iliad Group) holding significant market share. Innovation is primarily driven by the escalating demand for cloud computing, AI, and IoT, pushing for more efficient cooling systems, higher power densities, and advanced security protocols. Regulatory frameworks, particularly concerning data sovereignty and environmental sustainability (e.g., EU's GDPR and France's digital transition policies), significantly influence market development and operational standards. While direct product substitutes are limited, the rise of edge computing and distributed IT infrastructure presents an evolving competitive landscape. End-user demographics are increasingly skewed towards hyperscale cloud providers, BFSI, and e-commerce, driving the need for massive and mega-sized data centers. Mergers and acquisitions remain a strategic imperative for expansion and market consolidation. Notable M&A activities within the study period have seen significant investment in expanding existing footprints and acquiring new facilities, bolstering capacity and technological capabilities. The market share of the top three players is estimated to be over 60 billion EUR. M&A deal values are projected to exceed 15 billion EUR over the forecast period.

France Data Center Industry Market Dynamics & Trends

The France data center industry is experiencing robust growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 15% from 2025 to 2033. This expansion is fueled by a confluence of dynamic market drivers, including the accelerating digital transformation across all sectors, the relentless expansion of cloud services, and the burgeoning adoption of AI and machine learning technologies. The proliferation of 5G networks and the associated increase in data traffic further necessitate enhanced data processing and storage capabilities, directly benefiting the data center sector. Consumer preferences are shifting towards more responsive and accessible digital services, demanding lower latency and higher bandwidth, which are hallmarks of modern data center infrastructure. Technologically, the industry is witnessing disruptive innovations such as liquid cooling for high-density computing, advanced energy-efficient designs, and the integration of renewable energy sources to meet sustainability goals. The competitive dynamics are characterized by intense competition among colocation providers, hyperscalers, and enterprise data centers, each vying for market share through service differentiation, pricing strategies, and strategic partnerships. The increasing demand for sovereign cloud solutions within France and the EU also presents a significant growth avenue, encouraging investments in local data center capacity and security. The overall market penetration of advanced data center services is estimated to reach over 75% by 2033. Investments in R&D for next-generation cooling and power management solutions are projected to exceed 2 billion EUR annually.

Dominant Regions & Segments in France Data Center Industry

The Paris (Ile-de-France) region overwhelmingly dominates the France data center industry, serving as the primary hub for digital infrastructure and connectivity. Its dominance is driven by:

- Infrastructure and Connectivity: Paris boasts unparalleled fiber optic network density and access to major subsea cable landing stations, facilitating high-speed data transfer and international connectivity.

- Economic and Business Hub: As the financial and political capital, Paris attracts a large concentration of enterprises, cloud providers, and government agencies requiring significant data processing and storage capacity.

- Talent Pool: Access to a skilled workforce proficient in IT operations, cybersecurity, and engineering further cements its position.

Key Segment Dominance:

- Data Center Size: Mega and Massive sized data centers are leading the charge, catering to the immense demands of hyperscale cloud providers and large enterprises. The need for scalability and high capacity is paramount.

- Tier Type: Tier 3 and Tier 4 data centers are the most sought after, ensuring high availability, redundancy, and fault tolerance crucial for mission-critical applications.

- Colocation Type: Hyperscale colocation dominates due to the massive deployments by global cloud giants. Wholesale colocation is also a significant segment, serving large enterprises with dedicated space and power.

- End User: Cloud service providers are the largest consumers, followed closely by BFSI (Banking, Financial Services, and Insurance) and E-Commerce, which require robust, secure, and scalable data infrastructure. The Telecom sector also plays a crucial role in supporting network connectivity and data exchange.

The Rest of France is also seeing significant growth, particularly in areas with strategic connectivity options and government incentives for digital infrastructure development. Marseille, for instance, is emerging as a key hub due to its subsea cable connectivity.

France Data Center Industry Product Innovations

Product innovations in the France data center industry are focused on enhancing efficiency, sustainability, and performance. Key developments include advanced liquid cooling solutions for high-density server racks, enabling greater compute power in smaller footprints. Innovations in renewable energy integration, such as on-site solar generation and advanced battery storage, are reducing operational costs and environmental impact. Furthermore, enhanced cybersecurity features and AI-driven monitoring systems are being integrated to ensure data integrity and resilience. These innovations offer competitive advantages by reducing PUE (Power Usage Effectiveness) ratios, increasing operational uptime, and meeting stringent environmental regulations, making French data centers more attractive to global clients.

France Data Center Industry Report Scope & Segmentation Analysis

This report segments the France data center industry across several key dimensions. The Hotspot: Paris (Ile-de-France) is the most mature and largest market, driven by high demand from cloud providers and enterprises, with significant growth projections. The Rest of France segment, while smaller, presents substantial growth opportunities as new hubs emerge and connectivity improves. In terms of Data Center Size, Mega and Massive facilities are experiencing the highest growth rates due to hyperscale demand, while Medium and Large facilities cater to enterprise needs. Tier 3 and Tier 4 Tier Types are commanding premium pricing and market share due to their reliability. Absorption: Non-Utilized capacity is decreasing as demand outstrips supply. Colocation Types like Hyperscale and Wholesale are leading the market, with Retail colocation serving smaller businesses. Key End Users like Cloud, BFSI, and E-Commerce are driving significant investment and expansion, with sustained growth expected.

Key Drivers of France Data Center Industry Growth

The France data center industry's growth is propelled by several key factors. The ongoing digital transformation across all business sectors necessitates increased data storage and processing capabilities. The rapid expansion of cloud services, driven by the demand for scalability and flexibility, is a primary accelerator. The adoption of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) requires significant computational power and data infrastructure. Furthermore, increasing data privacy regulations and the push for data sovereignty within the EU encourage the development of localized data centers. Government initiatives supporting digital innovation and investment in high-speed connectivity also play a crucial role.

Challenges in the France Data Center Industry Sector

Despite its strong growth trajectory, the France data center industry faces several challenges. Obtaining permits and navigating complex regulatory frameworks, particularly concerning environmental impact and energy consumption, can be time-consuming and costly. Supply chain disruptions for critical hardware components and specialized equipment can lead to project delays and increased costs. The high demand for renewable energy to power these facilities poses a challenge in ensuring a consistent and sustainable supply. Furthermore, intense competition and the need for continuous investment in upgrading technology to meet evolving client demands require significant capital expenditure, placing pressure on profit margins. The skilled labor shortage in specialized IT and engineering roles also presents a growing concern.

Emerging Opportunities in France Data Center Industry

Emerging opportunities within the France data center industry are abundant. The increasing demand for edge computing solutions, driven by latency-sensitive applications like autonomous vehicles and real-time analytics, presents a significant growth area. The development of specialized data centers for AI and high-performance computing (HPC) is another key opportunity, catering to the growing need for massive computational power. The push for sustainability is driving opportunities in green data center technologies, including advanced cooling systems and renewable energy integration. Furthermore, the growing demand for sovereign cloud solutions within France and the EU offers substantial potential for domestic data center providers. Expansion into secondary cities and regions outside of Paris, supported by improved connectivity, also presents new growth frontiers.

Leading Players in the France Data Center Industry Market

- Interxion (Digital Reality Trust Inc.)

- Zenlayer Inc.

- Equinix Inc.

- Euclyde Data Centers

- Scaleway SAS (Iliad Group)

- Thésée DataCenter

- SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR

- Cogent Communications

- CyrusOne Inc.

- Telehouse (KDDI Corporation)

- Global Switch Holdings Limited

- Sungard Availability Services LP

Key Developments in France Data Center Industry Industry

- June 2022: SFR BUSINESS is strengthening its hosting offer for companies with 26 new datacenters in France via partnership with Equinix and Interxion.

- September 2021: Telehouse opened new data center facility known as THM1 in Marseille and this facility will give customers access to 160Tbps of capacity via the 14 subsea cables that connect the city with MEA and APAC.

- July 2021: Thésée DataCenters opened its first Tier IV data center in Aubergenville, in the Yvelines area of France.

Future Outlook for France Data Center Industry Market

The future outlook for the France data center industry remains exceptionally strong, driven by sustained demand for digital infrastructure. The continuous growth of cloud computing, AI, IoT, and 5G will necessitate significant expansion in data center capacity and capabilities. Strategic investments in sustainable technologies and renewable energy sources will be crucial for long-term growth and compliance with environmental regulations. The increasing focus on data sovereignty and security will further bolster domestic data center development. Opportunities abound in emerging technologies like edge computing and specialized HPC facilities. Collaborations and partnerships will continue to shape the market landscape, fostering innovation and expanding reach. The industry is poised for continued robust investment and technological advancement, solidifying France's position as a key European data center hub, with projected market growth exceeding 50 billion EUR by 2033.

France Data Center Industry Segmentation

-

1. Hotspot

- 1.1. Paris (Ile-De-France)

- 1.2. Rest of France

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. Colocation Type

- 5.1. Hyperscale

- 5.2. Retail

- 5.3. Wholesale

-

6. End User

- 6.1. BFSI

- 6.2. Cloud

- 6.3. E-Commerce

- 6.4. Government

- 6.5. Manufacturing

- 6.6. Media & Entertainment

- 6.7. Telecom

- 6.8. Other End User

France Data Center Industry Segmentation By Geography

- 1. France

France Data Center Industry Regional Market Share

Geographic Coverage of France Data Center Industry

France Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Paris (Ile-De-France)

- 5.1.2. Rest of France

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by Colocation Type

- 5.5.1. Hyperscale

- 5.5.2. Retail

- 5.5.3. Wholesale

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. BFSI

- 5.6.2. Cloud

- 5.6.3. E-Commerce

- 5.6.4. Government

- 5.6.5. Manufacturing

- 5.6.6. Media & Entertainment

- 5.6.7. Telecom

- 5.6.8. Other End User

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. France

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. France Data Center Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Hotspot

- 6.1.1. Paris (Ile-De-France)

- 6.1.2. Rest of France

- 6.2. Market Analysis, Insights and Forecast - by Data Center Size

- 6.2.1. Large

- 6.2.2. Massive

- 6.2.3. Medium

- 6.2.4. Mega

- 6.2.5. Small

- 6.3. Market Analysis, Insights and Forecast - by Tier Type

- 6.3.1. Tier 1 and 2

- 6.3.2. Tier 3

- 6.3.3. Tier 4

- 6.4. Market Analysis, Insights and Forecast - by Absorption

- 6.4.1. Non-Utilized

- 6.5. Market Analysis, Insights and Forecast - by Colocation Type

- 6.5.1. Hyperscale

- 6.5.2. Retail

- 6.5.3. Wholesale

- 6.6. Market Analysis, Insights and Forecast - by End User

- 6.6.1. BFSI

- 6.6.2. Cloud

- 6.6.3. E-Commerce

- 6.6.4. Government

- 6.6.5. Manufacturing

- 6.6.6. Media & Entertainment

- 6.6.7. Telecom

- 6.6.8. Other End User

- 6.1. Market Analysis, Insights and Forecast - by Hotspot

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Interxion (Digital Reality Trust Inc )

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Zenlayer Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Equinix Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Euclyde Data Centers

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Scaleway SAS (Illiad Group)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Thésée DataCenter

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cogent Communications

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 CyrusOne Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Telehouse (KDDI Corporation)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Global Switch Holdings Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Sungard Availability Services LP

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Interxion (Digital Reality Trust Inc )

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: France Data Center Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: France Data Center Industry Share (%) by Company 2025

List of Tables

- Table 1: France Data Center Industry Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 2: France Data Center Industry Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 3: France Data Center Industry Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 4: France Data Center Industry Revenue billion Forecast, by Absorption 2020 & 2033

- Table 5: France Data Center Industry Revenue billion Forecast, by Colocation Type 2020 & 2033

- Table 6: France Data Center Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 7: France Data Center Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: France Data Center Industry Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 9: France Data Center Industry Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 10: France Data Center Industry Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 11: France Data Center Industry Revenue billion Forecast, by Absorption 2020 & 2033

- Table 12: France Data Center Industry Revenue billion Forecast, by Colocation Type 2020 & 2033

- Table 13: France Data Center Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 14: France Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Data Center Industry?

The projected CAGR is approximately 9.84%.

2. Which companies are prominent players in the France Data Center Industry?

Key companies in the market include Interxion (Digital Reality Trust Inc ), Zenlayer Inc , Equinix Inc, Euclyde Data Centers, Scaleway SAS (Illiad Group), Thésée DataCenter, SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR, Cogent Communications, CyrusOne Inc, Telehouse (KDDI Corporation), Global Switch Holdings Limited, Sungard Availability Services LP.

3. What are the main segments of the France Data Center Industry?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, Colocation Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.26 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Securing Confidential Data and Protection Against Data Loss; Growing Demand for Improving Archived Content across Channels; Ongoing efforts to promote Digitization at Workplaces.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Transition from Legacy Systems Chips; Customization Challenges Leading to Implementation Issues.

8. Can you provide examples of recent developments in the market?

June 2022: SFR BUSINESS is strengthening its hosting offer for companies with 26 new datacenters in France via partnership with Equinix and Interxion.September 2021: Telehouse opened new data center facility known as THM1 in Marseille and this facility will give customers access to 160Tbps of capacity via the 14 subsea cables that connect the city with MEA and APAC.July 2021: Thésée DataCenters opened its first Tier IV data center in Aubergenville, in the Yvelines area of France.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Data Center Industry?

To stay informed about further developments, trends, and reports in the France Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence