Key Insights

The global Healthcare Data market is projected to experience significant growth, reaching $3.1 billion by 2024, with a Compound Annual Growth Rate (CAGR) of 13.36% from 2024 to 2033. This expansion is driven by the increasing demand for advanced analytics to extract actionable insights from growing healthcare data volumes. Key growth factors include the adoption of digital health technologies, the pursuit of improved patient outcomes, and the rise of personalized medicine. Enhanced data privacy and security regulations, alongside government initiatives promoting data interoperability, further fuel market development. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into healthcare analytics platforms is revolutionizing the sector, enabling predictive modeling, early disease detection, and optimized resource allocation. The transition to value-based care models also necessitates sophisticated data analysis for demonstrating efficacy and managing costs.

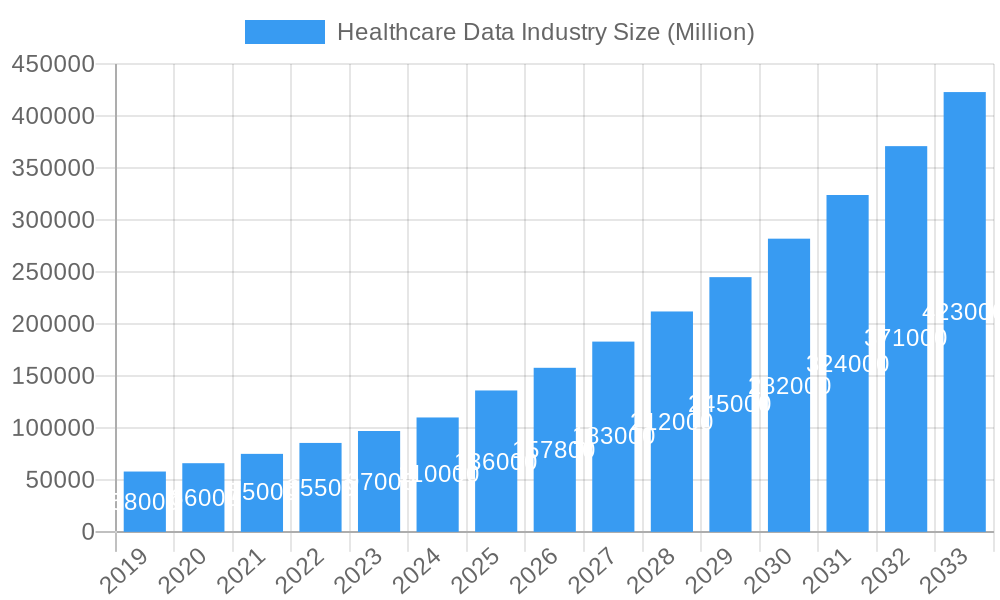

Healthcare Data Industry Market Size (In Billion)

Market segmentation highlights the dominance of Software and Services, underscoring the need for both robust platforms and expert implementation. Cloud deployment is increasingly preferred over on-premise solutions due to its scalability, flexibility, and cost-effectiveness. Key application segments like Financial Analytics, Clinical Data Analytics, Operational Analytics, and Population Health Analytics are all experiencing substantial growth. Geographically, North America is expected to lead, driven by early adoption of advanced healthcare technologies and substantial investments in data analytics infrastructure. The Asia Pacific region is projected to exhibit the fastest growth, fueled by rising healthcare expenditure, a growing patient population, and government support for digital transformation. Challenges such as data privacy concerns, high implementation costs, and a shortage of skilled professionals exist. However, continuous technological advancements and strategic collaborations are expected to overcome these restraints, ensuring sustained market development.

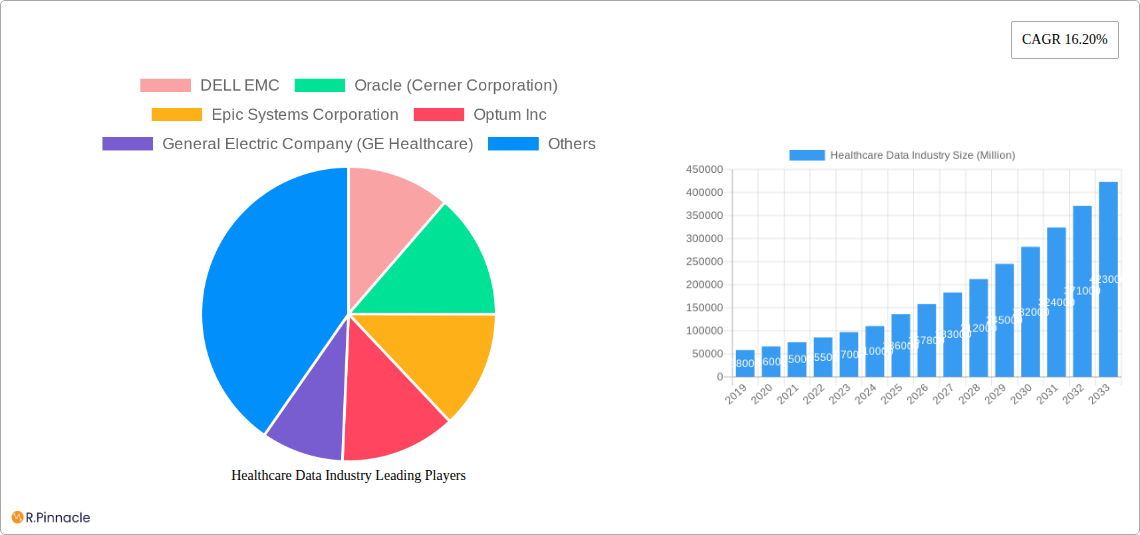

Healthcare Data Industry Company Market Share

Healthcare Data Industry Market Report Description

This comprehensive report provides an in-depth analysis of the global Healthcare Data Industry, offering critical insights for stakeholders navigating this rapidly evolving sector. With a study period spanning from 2019 to 2033, this report leverages a base year of 2025 to deliver precise market estimations and forecasts for the period 2025–2033. The historical period of 2019–2024 has been meticulously reviewed to establish a robust foundation for future projections. This analysis is essential for understanding the current landscape, identifying growth opportunities, and mitigating potential risks in the healthcare data analytics market, clinical data management solutions, and healthcare big data adoption.

Healthcare Data Industry Market Structure & Innovation Trends

The Healthcare Data Industry exhibits a dynamic market structure characterized by a mix of large, established players and agile innovators. Market concentration is influenced by significant investments in data infrastructure and analytics platforms. Innovation is primarily driven by advancements in AI, machine learning, and cloud computing, enabling sophisticated predictive analytics in healthcare and real-time patient data processing. Regulatory frameworks, such as HIPAA and GDPR, continue to shape data privacy and security protocols, impacting product development and market entry. Product substitutes include traditional data warehousing solutions and manual data analysis methods, though their effectiveness is diminishing against advanced digital solutions. End-user demographics are increasingly focused on providers, payers, and pharmaceutical companies seeking to optimize patient outcomes, reduce costs, and enhance operational efficiency. Mergers and acquisitions (M&A) are a significant trend, with deal values reaching over $15 Billion in the past year, as companies consolidate capabilities and expand market reach. Key M&A activities often involve acquisitions of specialized analytics firms by larger technology providers to enhance their healthcare AI solutions and data interoperability platforms. For instance, the acquisition of a leading population health management software provider by a major EHR vendor significantly altered the competitive landscape, integrating advanced analytics directly into clinical workflows. The market share of leading players in specific segments, like clinical data analytics software, is estimated to be around 35% collectively for the top five vendors.

Healthcare Data Industry Market Dynamics & Trends

The Healthcare Data Industry is poised for substantial growth, driven by an increasing volume of health-related data generated from electronic health records (EHRs), wearable devices, and genomic sequencing. This surge in data necessitates advanced healthcare data analytics platforms for meaningful interpretation and actionable insights. Technological disruptions, including the widespread adoption of cloud-based solutions and the integration of artificial intelligence (AI) and machine learning (ML), are fundamentally transforming how healthcare data is collected, stored, and analyzed. AI-powered tools are increasingly being used for disease prediction, personalized treatment plans, and drug discovery, significantly enhancing clinical decision support systems. Consumer preferences are shifting towards personalized healthcare experiences, demanding greater access to and control over their health information, which fuels the need for robust patient data management systems. The competitive dynamics are intensifying, with companies focusing on developing integrated solutions that offer comprehensive healthcare data intelligence. Market penetration of advanced analytics is projected to reach over 60% by 2028, up from approximately 30% in 2023. The compound annual growth rate (CAGR) for the healthcare big data market is estimated at a strong 15% over the forecast period, fueled by both technological innovation and the growing imperative for value-based care. Payers are leveraging healthcare data analytics to identify fraud, waste, and abuse, leading to cost savings estimated at over $50 Billion annually. Providers are utilizing these insights to improve patient outcomes and operational efficiency, with studies showing a 10% reduction in readmission rates through effective population health management analytics. The ongoing digital transformation within the healthcare ecosystem, coupled with increasing patient engagement, will continue to propel the market forward, making healthcare data analytics tools indispensable.

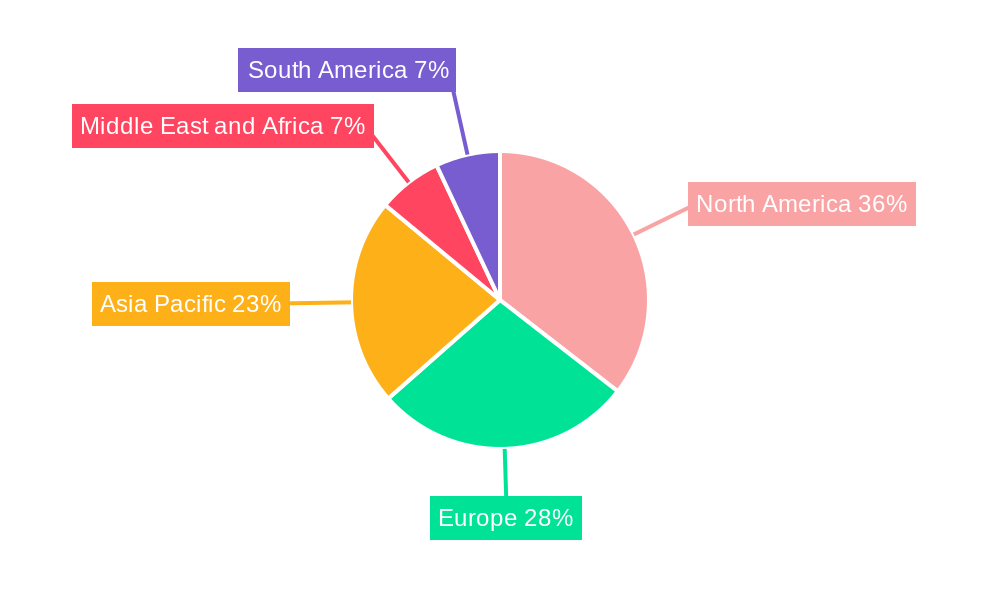

Dominant Regions & Segments in Healthcare Data Industry

The North America region, particularly the United States, currently dominates the Healthcare Data Industry, accounting for an estimated 65% of the global market share. This dominance is driven by a mature healthcare infrastructure, significant investments in digital health technologies, and a strong regulatory environment that encourages data utilization for improved patient care. Economic policies supporting innovation and substantial government initiatives to digitize healthcare records have further solidified its leading position.

Key Drivers of Regional Dominance in North America:

- Robust Healthcare Expenditure: High spending on healthcare translates to greater adoption of advanced data solutions.

- Technological Advancements: Early and widespread adoption of EHRs and telehealth platforms.

- Government Initiatives: Programs aimed at interoperability and data exchange.

- Presence of Key Market Players: Home to many leading technology and healthcare companies.

Within the Component segment, Software is the dominant category, holding an estimated 55% of the market share. This includes EHR systems, data analytics platforms, and specialized healthcare AI applications.

Component Segment Dominance:

- Software: Essential for data collection, processing, analysis, and visualization. Includes clinical data analytics software, financial analytics software, and operational analytics software.

- Services: Encompasses consulting, implementation, data integration, and ongoing support. While crucial, its market share is currently around 45%, complementing the software solutions.

In terms of Deployment, Cloud deployment is rapidly gaining traction and is projected to surpass on-premise solutions in the coming years, currently holding over 50% of the market.

Deployment Dominance:

- Cloud: Offers scalability, flexibility, and cost-effectiveness, making it ideal for handling vast amounts of healthcare data. This includes cloud-based EHR systems and SaaS analytics platforms.

- On-premise: Traditionally dominant, but its market share is declining due to the complexities and costs associated with managing large data centers.

Analyzing Application, Clinical Data Analytics is the most prominent segment, accounting for an estimated 40% of the market. This is followed closely by Population Health Analytics, which is crucial for managing patient populations and improving public health outcomes.

Application Segment Dominance:

- Clinical Data Analytics: Focuses on analyzing patient data to improve diagnoses, treatment efficacy, and patient safety.

- Population Health Analytics: Utilizes data to understand health trends across specific populations, enabling proactive interventions and disease prevention.

- Financial Analytics: Crucial for revenue cycle management, cost optimization, and fraud detection, holding approximately 20% of the market.

- Operational Analytics: Aims to improve the efficiency of healthcare operations, streamline workflows, and optimize resource allocation, with a market share of around 15%.

Healthcare Data Industry Product Innovations

The Healthcare Data Industry is witnessing a wave of product innovations centered around enhancing data utilization for improved patient care and operational efficiency. Key developments include the proliferation of AI-powered diagnostic tools, advanced predictive analytics platforms for identifying at-risk patients, and enhanced data interoperability solutions to facilitate seamless information exchange across disparate systems. Companies are also focusing on developing user-friendly interfaces for clinical data analytics and intuitive dashboards for population health management. These innovations provide a significant competitive advantage by enabling healthcare organizations to derive deeper insights, personalize treatments, and streamline workflows, ultimately leading to better patient outcomes and reduced healthcare costs. The market fit for these products is exceptionally strong, driven by the increasing demand for data-driven decision-making in all aspects of healthcare.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Healthcare Data Industry across several key segmentations, providing detailed market size, growth projections, and competitive dynamics.

Component: The Software segment, valued at over $30 Billion, is projected to grow at a CAGR of 16%, driven by demand for advanced analytics and AI solutions. The Services segment, valued at approximately $25 Billion, is expected to grow at a CAGR of 14%, supporting the implementation and optimization of software solutions.

Deployment: The Cloud deployment segment, currently valued at over $30 Billion, is anticipated to exhibit a strong CAGR of 18% due to its scalability and cost-effectiveness. The On-premise deployment segment, valued at approximately $25 Billion, is expected to see a modest CAGR of 8% as organizations migrate to cloud-based infrastructure.

Application: Clinical Data Analytics, the largest segment, is valued at over $22 Billion and is projected to grow at a CAGR of 17%. Population Health Analytics, valued at approximately $18 Billion, is expected to grow at a CAGR of 16%, driven by value-based care initiatives. Financial Analytics, valued at over $10 Billion, is projected to grow at a CAGR of 15%, while Operational Analytics, valued at approximately $8 Billion, is expected to grow at a CAGR of 14%.

Key Drivers of Healthcare Data Industry Growth

The Healthcare Data Industry is propelled by a confluence of powerful drivers. Technological advancements, particularly in AI and machine learning, are enabling more sophisticated healthcare data analytics and predictive modeling. The increasing volume of healthcare data generated from EHRs, wearables, and genomic sequencing necessitates advanced solutions for storage, management, and analysis. Economic factors, such as the push for value-based care and the need for cost containment within healthcare systems, are significant catalysts. Government initiatives and regulatory mandates aimed at improving data interoperability, patient safety, and health outcomes also play a crucial role. For example, the adoption of population health management software is directly linked to reimbursement models that incentivize better patient outcomes. The growing emphasis on personalized medicine and precision healthcare further fuels the demand for granular patient data analysis.

Challenges in the Healthcare Data Industry Sector

Despite its immense growth potential, the Healthcare Data Industry faces significant challenges. Regulatory hurdles, including stringent data privacy laws like HIPAA and GDPR, can complicate data sharing and analysis, requiring substantial investment in compliance and security. Interoperability issues between different healthcare systems and data silos remain a persistent barrier to seamless data integration. The high cost of implementing and maintaining advanced data analytics infrastructure and the scarcity of skilled data scientists and analytics professionals also present significant challenges. Cybersecurity threats and the risk of data breaches are constant concerns, necessitating robust security measures that can add to operational costs. Furthermore, resistance to change within established healthcare organizations can slow down the adoption of new data-driven technologies. The overall impact of these challenges can lead to delayed project timelines and increased implementation costs, estimated to affect up to 20% of large-scale data projects.

Emerging Opportunities in Healthcare Data Industry

The Healthcare Data Industry is ripe with emerging opportunities. The growing adoption of the Internet of Things (IoT) in healthcare, with an increasing number of connected medical devices, presents a massive influx of real-time patient data, creating demand for advanced monitoring and analytics. The expansion of telehealth and remote patient monitoring services further amplifies the need for robust data management and analytics capabilities. The burgeoning field of personalized medicine, driven by advancements in genomics and AI, offers significant opportunities for tailored treatment plans and drug development. Emerging markets, particularly in Asia-Pacific and Latin America, are witnessing rapid digital transformation in healthcare, creating new avenues for growth. The development of federated learning models, which allow data analysis without centralizing sensitive patient information, addresses privacy concerns and opens up new collaborative possibilities. The application of blockchain technology for secure data sharing and integrity is another promising area.

Leading Players in the Healthcare Data Industry Market

- DELL EMC

- Oracle (Cerner Corporation)

- Epic Systems Corporation

- Optum Inc

- General Electric Company (GE Healthcare)

- International Business Machines Corporation (IBM)

- ExlService Holdings Inc

- Health Fidelity Inc

- Allscripts Healthcare Solutions Inc

- Flatiron Health

- Apixio

- SAS INSTITUTE INC

- Innovaccer Inc

Key Developments in Healthcare Data Industry Industry

- March 2022: Microsoft launched Azure Health Data Services in the United States, a platform as a service (PAAS) offering designed exclusively to support protected health information (PHI) in the cloud, enhancing cloud-based healthcare data solutions.

- March 2022: The government of Thailand launched a big data portal for healthcare facilities. The National Reforms Committee on Public Health joined hands with 12 government agencies to improve the quality of healthcare services by implementing digital technologies, signaling a significant push for national healthcare data initiatives.

Future Outlook for Healthcare Data Industry Market

The future outlook for the Healthcare Data Industry is exceptionally bright, driven by an accelerating digital transformation and an increasing reliance on data-driven insights. The continued integration of AI and machine learning will unlock unprecedented capabilities in predictive diagnostics, personalized treatment, and drug discovery, leading to a paradigm shift in patient care. The growing adoption of cloud-based solutions will provide the scalability and flexibility necessary to manage the ever-expanding volume of healthcare data. Furthermore, the increasing focus on preventative care and population health management will further fuel the demand for sophisticated analytics platforms. Emerging technologies like the IoT and blockchain are poised to create new avenues for innovation and enhanced data security. Strategic collaborations and mergers between technology providers and healthcare organizations will continue to shape the market landscape, fostering an environment of rapid advancement and market expansion, with projected market growth reaching over $150 Billion by 2033.

Healthcare Data Industry Segmentation

-

1. Component

- 1.1. Software

- 1.2. Services

-

2. Deployment

- 2.1. On-premise

- 2.2. Cloud

-

3. Application

- 3.1. Financial Analytics

- 3.2. Clinical Data Analytics

- 3.3. Operational Analytics

- 3.4. Population Health Analytics

Healthcare Data Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Healthcare Data Industry Regional Market Share

Geographic Coverage of Healthcare Data Industry

Healthcare Data Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.36% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Software

- 5.1.2. Services

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. On-premise

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Financial Analytics

- 5.3.2. Clinical Data Analytics

- 5.3.3. Operational Analytics

- 5.3.4. Population Health Analytics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Healthcare Data Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Software

- 6.1.2. Services

- 6.2. Market Analysis, Insights and Forecast - by Deployment

- 6.2.1. On-premise

- 6.2.2. Cloud

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Financial Analytics

- 6.3.2. Clinical Data Analytics

- 6.3.3. Operational Analytics

- 6.3.4. Population Health Analytics

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Software

- 7.1.2. Services

- 7.2. Market Analysis, Insights and Forecast - by Deployment

- 7.2.1. On-premise

- 7.2.2. Cloud

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Financial Analytics

- 7.3.2. Clinical Data Analytics

- 7.3.3. Operational Analytics

- 7.3.4. Population Health Analytics

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Software

- 8.1.2. Services

- 8.2. Market Analysis, Insights and Forecast - by Deployment

- 8.2.1. On-premise

- 8.2.2. Cloud

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Financial Analytics

- 8.3.2. Clinical Data Analytics

- 8.3.3. Operational Analytics

- 8.3.4. Population Health Analytics

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Software

- 9.1.2. Services

- 9.2. Market Analysis, Insights and Forecast - by Deployment

- 9.2.1. On-premise

- 9.2.2. Cloud

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Financial Analytics

- 9.3.2. Clinical Data Analytics

- 9.3.3. Operational Analytics

- 9.3.4. Population Health Analytics

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Middle East and Africa Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Software

- 10.1.2. Services

- 10.2. Market Analysis, Insights and Forecast - by Deployment

- 10.2.1. On-premise

- 10.2.2. Cloud

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Financial Analytics

- 10.3.2. Clinical Data Analytics

- 10.3.3. Operational Analytics

- 10.3.4. Population Health Analytics

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. South America Healthcare Data Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Software

- 11.1.2. Services

- 11.2. Market Analysis, Insights and Forecast - by Deployment

- 11.2.1. On-premise

- 11.2.2. Cloud

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Financial Analytics

- 11.3.2. Clinical Data Analytics

- 11.3.3. Operational Analytics

- 11.3.4. Population Health Analytics

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 DELL EMC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Oracle (Cerner Corporation)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Epic Systems Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Optum Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 General Electric Company (GE Healthcare)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 International Business Machines Corporation (IBM)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ExlService Holdings Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Health Fidelity Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Allscripts Healthcare Solutions Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Flatiron Health

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Apixio

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SAS INSTITUTE INC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Innovaccer Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 DELL EMC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Healthcare Data Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Healthcare Data Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 4: North America Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 5: North America Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 8: North America Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 9: North America Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 10: North America Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 11: North America Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 12: North America Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 13: North America Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 20: Europe Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 21: Europe Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 22: Europe Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 23: Europe Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 24: Europe Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 25: Europe Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 26: Europe Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 27: Europe Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 29: Europe Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Europe Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 36: Asia Pacific Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 37: Asia Pacific Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 38: Asia Pacific Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 39: Asia Pacific Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 40: Asia Pacific Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 41: Asia Pacific Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 42: Asia Pacific Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 43: Asia Pacific Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 44: Asia Pacific Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Asia Pacific Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Asia Pacific Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Asia Pacific Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Asia Pacific Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 52: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 53: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 54: Middle East and Africa Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 55: Middle East and Africa Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 56: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 57: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 58: Middle East and Africa Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 59: Middle East and Africa Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 60: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 61: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Middle East and Africa Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 63: Middle East and Africa Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Middle East and Africa Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Healthcare Data Industry Revenue (billion), by Component 2025 & 2033

- Figure 68: South America Healthcare Data Industry Volume (K Unit), by Component 2025 & 2033

- Figure 69: South America Healthcare Data Industry Revenue Share (%), by Component 2025 & 2033

- Figure 70: South America Healthcare Data Industry Volume Share (%), by Component 2025 & 2033

- Figure 71: South America Healthcare Data Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 72: South America Healthcare Data Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 73: South America Healthcare Data Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 74: South America Healthcare Data Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 75: South America Healthcare Data Industry Revenue (billion), by Application 2025 & 2033

- Figure 76: South America Healthcare Data Industry Volume (K Unit), by Application 2025 & 2033

- Figure 77: South America Healthcare Data Industry Revenue Share (%), by Application 2025 & 2033

- Figure 78: South America Healthcare Data Industry Volume Share (%), by Application 2025 & 2033

- Figure 79: South America Healthcare Data Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: South America Healthcare Data Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Healthcare Data Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Healthcare Data Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 4: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 5: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Global Healthcare Data Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Healthcare Data Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 10: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 11: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 12: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 13: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United States Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Canada Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 24: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 25: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 26: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 27: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: France Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Spain Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 44: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 45: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 46: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 47: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 48: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: China Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: India Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Australia Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Korea Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 64: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 65: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 66: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 67: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 68: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 70: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: GCC Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Healthcare Data Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 78: Global Healthcare Data Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 79: Global Healthcare Data Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 80: Global Healthcare Data Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 81: Global Healthcare Data Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 82: Global Healthcare Data Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Global Healthcare Data Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 84: Global Healthcare Data Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: Brazil Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: Argentina Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Healthcare Data Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Healthcare Data Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Healthcare Data Industry?

The projected CAGR is approximately 13.36%.

2. Which companies are prominent players in the Healthcare Data Industry?

Key companies in the market include DELL EMC, Oracle (Cerner Corporation), Epic Systems Corporation, Optum Inc, General Electric Company (GE Healthcare), International Business Machines Corporation (IBM), ExlService Holdings Inc, Health Fidelity Inc, Allscripts Healthcare Solutions Inc, Flatiron Health, Apixio, SAS INSTITUTE INC, Innovaccer Inc.

3. What are the main segments of the Healthcare Data Industry?

The market segments include Component, Deployment, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Demand for Analytics Solutions for Population Health Management; Rise in Need for Business Intelligence to Optimize Health Administration and Strategy; Surge in Adoption of Big Data in the Healthcare Industry.

6. What are the notable trends driving market growth?

Cloud Segment is Expected to Register a High Growth Rate Over the Forecast Period.

7. Are there any restraints impacting market growth?

Security Concerns Related to Sensitive Patients Medical Data; High Cost of Implementation and Deployment.

8. Can you provide examples of recent developments in the market?

March 2022: Microsoft launched Azure Health Data Services in the United States. It is a platform as a service (PAAS) offering designed exclusively to support protected health information (PHI) in the cloud.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Healthcare Data Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Healthcare Data Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Healthcare Data Industry?

To stay informed about further developments, trends, and reports in the Healthcare Data Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence