Key Insights

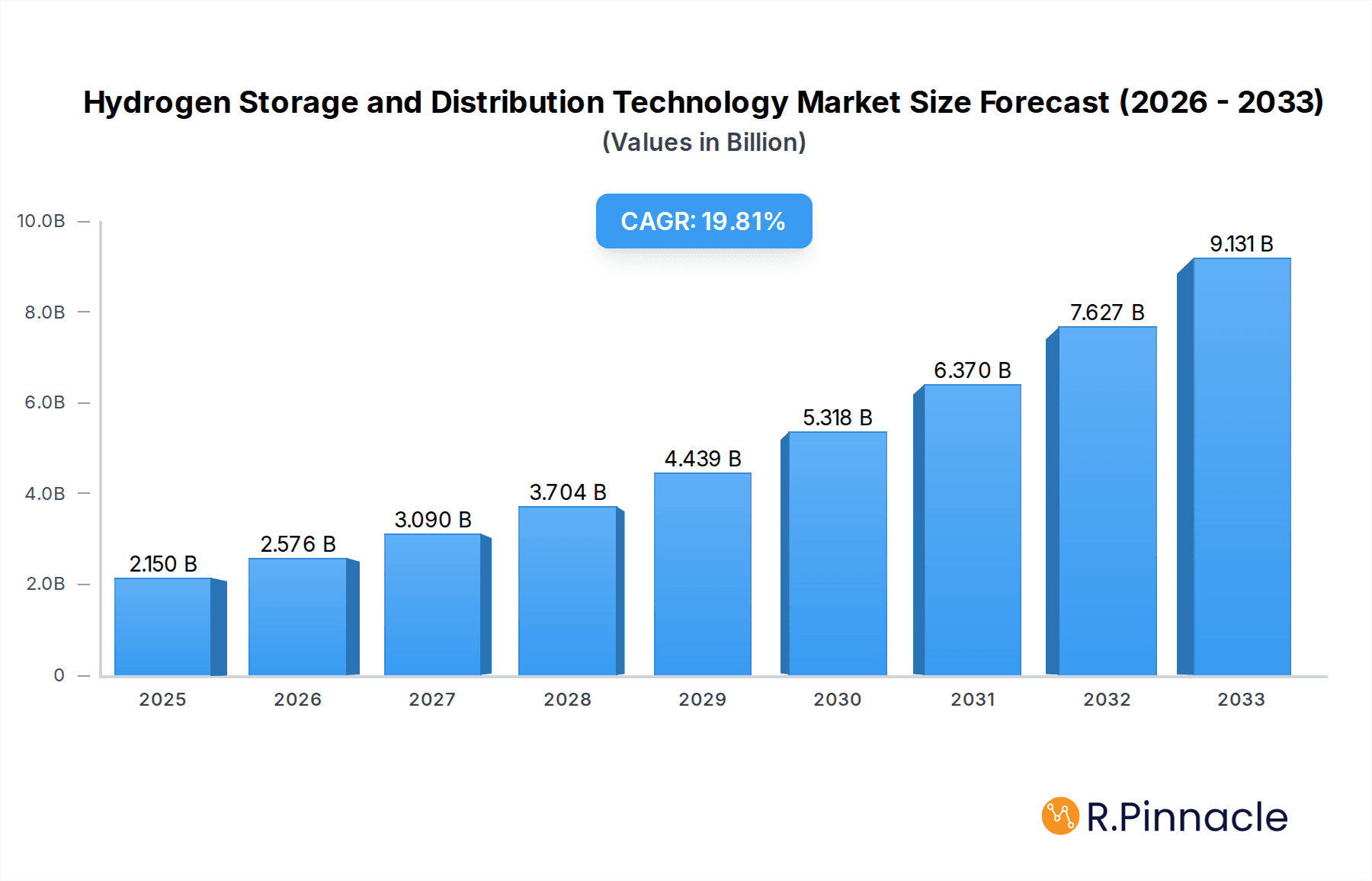

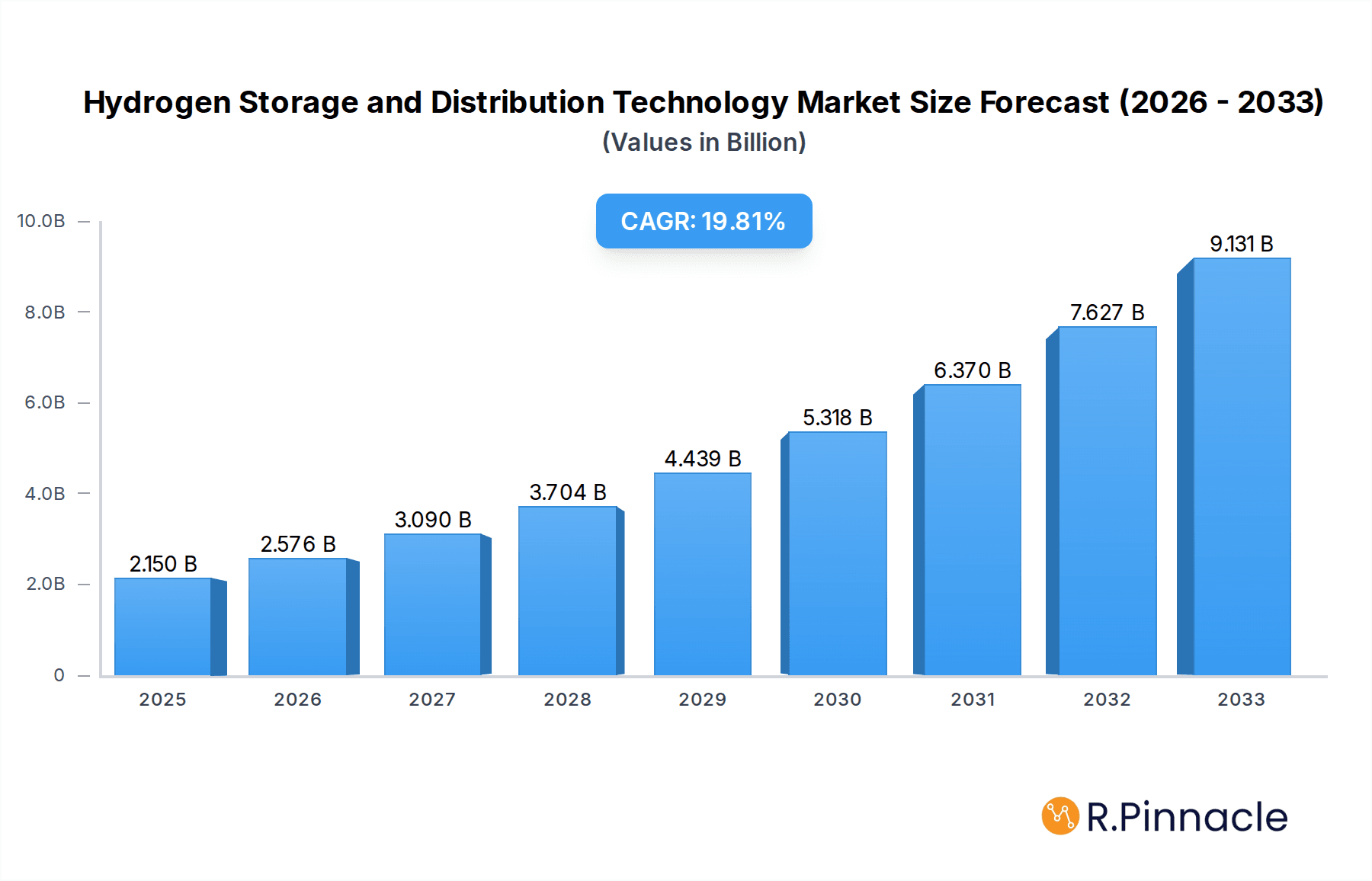

The global Hydrogen Storage and Distribution Technology market is poised for substantial expansion, projected to reach an estimated $2.15 billion by 2025. This robust growth is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 19.49% throughout the forecast period of 2025-2033. The burgeoning demand for clean energy solutions, driven by stringent environmental regulations and the urgent need to decarbonize various sectors, stands as the primary catalyst for this market's ascent. Key applications such as new energy vehicles, particularly fuel cell electric vehicles (FCEVs), are witnessing an accelerated adoption rate, necessitating advanced and efficient hydrogen storage and distribution infrastructure. The aerospace industry's increasing interest in hydrogen as a sustainable fuel further bolsters market prospects. Furthermore, the chemical sector's ongoing efforts to integrate hydrogen into its processes, alongside a growing demand for other specialized applications, contribute significantly to the market's upward trajectory. Innovations in storage technologies, including advancements in compressed gas systems, cold liquid hydrogen storage, and solid-state hydrogen storage solutions, are crucial in overcoming current limitations and enabling wider hydrogen utilization.

Hydrogen Storage and Distribution Technology Market Size (In Billion)

The market's expansion is further propelled by significant investments in hydrogen infrastructure development and supportive government policies aimed at fostering a hydrogen-based economy. Leading companies are actively engaged in research and development to enhance storage capacity, improve safety, and reduce the cost of hydrogen handling. While opportunities abound, the market also faces certain challenges, including the high capital expenditure required for establishing a comprehensive hydrogen supply chain and the need for standardization in safety protocols across different regions. Nonetheless, the inherent advantages of hydrogen as a clean and versatile energy carrier, coupled with ongoing technological breakthroughs and a global commitment to sustainability, paint a very promising picture for the Hydrogen Storage and Distribution Technology market in the coming years. The diversification of storage types, from compressed gas and cold liquid to organic liquid and solid compound solutions, caters to a wider array of application needs and operational demands, indicating a dynamic and evolving market landscape.

Hydrogen Storage and Distribution Technology Company Market Share

Hydrogen Storage and Distribution Technology Market Report: Unlocking a Billion-Dollar Future

Study Period: 2019–2033 | Base Year: 2025 | Estimated Year: 2025 | Forecast Period: 2025–2033 | Historical Period: 2019–2024

This comprehensive report provides an in-depth analysis of the global Hydrogen Storage and Distribution Technology market, projecting a billion-dollar valuation and unprecedented growth. It delves into the intricate market structure, dynamic forces, and emerging opportunities shaping this pivotal sector. Covering a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period extending from 2025 to 2033, this report offers strategic insights for stakeholders navigating the evolving hydrogen economy.

Hydrogen Storage and Distribution Technology Market Structure & Innovation Trends

The Hydrogen Storage and Distribution Technology market is characterized by a dynamic and evolving structure, with a moderate level of concentration. Key innovators and established players are actively investing in research and development to overcome storage density and safety challenges. Regulatory frameworks are rapidly being established and harmonized globally to support the safe and efficient deployment of hydrogen infrastructure, driving significant market expansion. The emergence of advanced materials and novel storage methods is mitigating the impact of product substitutes, while end-user demographics are increasingly favoring sustainable energy solutions. Mergers and acquisitions (M&A) are a significant trend, with deal values reaching into the billion range as companies seek to consolidate market positions and acquire cutting-edge technologies. For instance, recent M&A activities have seen significant capital infusion, demonstrating robust investor confidence. The market share of leading innovators is steadily increasing as proprietary technologies gain traction.

Hydrogen Storage and Distribution Technology Market Dynamics & Trends

The Hydrogen Storage and Distribution Technology market is poised for exponential growth, driven by a confluence of powerful forces. A primary growth driver is the global imperative for decarbonization and the transition to a clean energy future. Governments worldwide are implementing supportive policies and offering substantial incentives, fostering the development of hydrogen production, storage, and distribution networks. Technological disruptions are at the forefront, with continuous advancements in storage materials, compression techniques, and liquefaction processes. These innovations are enhancing efficiency, reducing costs, and improving the safety profile of hydrogen handling, thereby increasing market penetration. Consumer preferences are shifting towards sustainable transportation and industrial processes, creating a strong demand for hydrogen-based solutions. The competitive dynamics are intensifying, with both established energy giants and agile startups vying for market share. The compound annual growth rate (CAGR) is projected to be robust, fueled by these accelerating trends. The increasing adoption of fuel cell vehicles and the expansion of industrial hydrogen applications are directly contributing to the market's upward trajectory. Furthermore, the development of decentralized hydrogen production and distribution hubs is creating new avenues for market expansion and reducing logistical complexities. The integration of renewable energy sources for green hydrogen production further amplifies the market's sustainable appeal, attracting significant investment and driving innovation in storage and distribution technologies to match the intermittent nature of renewable generation.

Dominant Regions & Segments in Hydrogen Storage and Distribution Technology

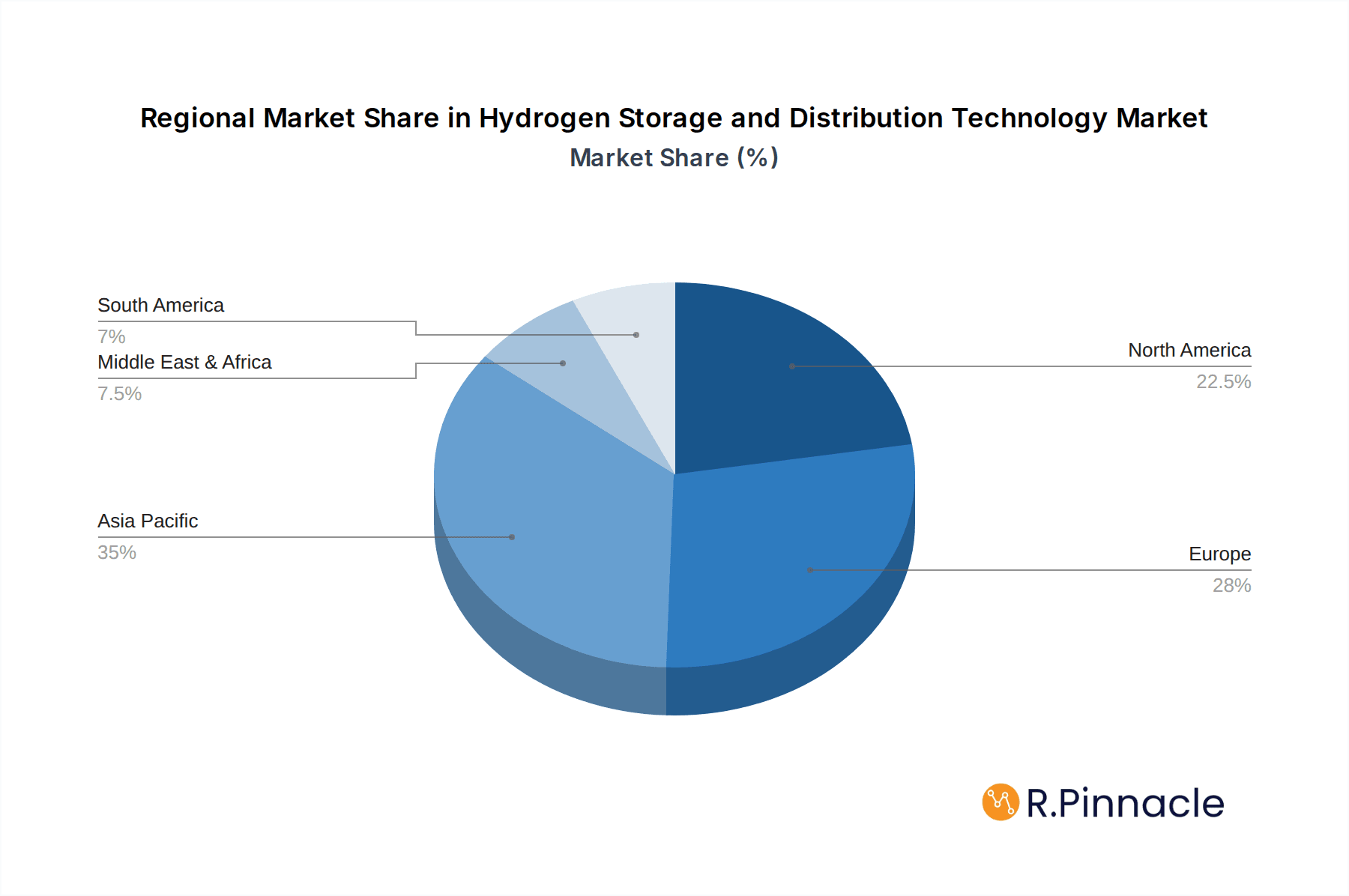

The Asia Pacific region, particularly China, is emerging as a dominant force in the Hydrogen Storage and Distribution Technology market. This leadership is underpinned by aggressive government initiatives, substantial investments in hydrogen infrastructure, and a rapidly expanding industrial and automotive sector.

- Key Drivers in Asia Pacific:

- Economic Policies & Incentives: Strong government support through subsidies, tax breaks, and national hydrogen strategies, aiming to achieve carbon neutrality targets.

- Infrastructure Development: Extensive investment in building hydrogen refueling stations and pipelines to support growing demand.

- Industrial Demand: High demand from the chemical and manufacturing sectors for hydrogen as a feedstock and energy source.

- New Energy Automobile Growth: Rapid adoption of fuel cell electric vehicles (FCEVs) driven by policy and consumer demand.

In terms of Application, New Energy Automobile represents the most significant segment, driven by the global push for zero-emission transportation. The development of advanced hydrogen storage tanks for vehicles is a critical area of innovation and investment.

- Dominance of New Energy Automobile:

- Technological Advancements: Continuous improvements in the weight, capacity, and safety of Type IV and Type V composite hydrogen storage tanks by companies like Iljin Hysolus and Hexagon Composites.

- Government Mandates & Targets: Stringent emission regulations and ambitious targets for FCEV deployment in key markets.

- Infrastructure Build-out: The rapid expansion of hydrogen refueling station networks to support FCEV adoption, with significant contributions from companies like Iwatani and Toyota.

Analyzing the Types of Hydrogen Storage and Distribution technologies, Compressed Gas storage remains dominant due to its established infrastructure and cost-effectiveness, especially for stationary applications and early-stage FCEV deployment. However, Cold Compressed Liquid Hydrogen is gaining significant traction for long-haul transportation and large-scale storage due to its higher energy density.

Compressed Gas Dominance:

- Proven Technology: Well-established safety protocols and manufacturing processes.

- Cost-Effectiveness: Lower capital investment compared to liquefaction or solid-state storage for certain applications.

- Wide Applicability: Suitable for a broad range of industrial uses and early-stage mobility.

Emerging Strength of Cold Compressed Liquid Hydrogen:

- Higher Energy Density: Crucial for applications requiring longer range and reduced storage volume.

- Infrastructure Specialization: Development of specialized cryogenic tanks by companies like Chart Industries and Gardner Cryogenics.

- Logistical Efficiency: Enabling larger-scale transportation of hydrogen over longer distances.

The Chemical industry also represents a substantial segment, utilizing hydrogen as a key feedstock. The report predicts substantial growth in this sector as industries seek cleaner alternatives.

Hydrogen Storage and Distribution Technology Product Innovations

The Hydrogen Storage and Distribution Technology market is witnessing a surge in product innovations aimed at enhancing safety, efficiency, and cost-effectiveness. Key developments include the commercialization of advanced composite materials for lighter and stronger high-pressure tanks, such as Type IV and Type V tanks, by companies like Hexagon Composites and Faurecia. Innovations in cryogenic storage are leading to more efficient liquefaction and insulation technologies, enabling the cost-effective transport of liquid hydrogen by players like Chart Industries and Faber Industrie. Furthermore, breakthroughs in solid-state hydrogen storage materials and organic liquid hydrogen (OLH2) systems by companies like Hydrogenious Technologies and Jiangsu Guofu Hydrogen Energy Equipment are paving the way for higher storage densities and improved safety profiles, offering significant competitive advantages in niche and emerging applications.

Report Scope & Segmentation Analysis

This report meticulously segments the Hydrogen Storage and Distribution Technology market across various critical dimensions.

Application:

- New Energy Automobile: This segment is projected to experience the highest growth, driven by the burgeoning demand for FCEVs. Market size is expected to reach hundreds of billions by 2033, fueled by government mandates and ongoing technological advancements in storage solutions from companies like Toyota and Faurecia.

- Aerospace: While a nascent market, aerospace applications are expected to see steady growth as hydrogen fuel gains traction for sustainable aviation. Market size is estimated to be in the tens of billions, with a focus on lightweight and high-capacity storage solutions.

- Chemical: This segment currently represents a significant portion of the market and is anticipated to grow substantially as industries transition to cleaner feedstocks. Market size is projected to be in the hundreds of billions, with established players like The Japan Steel Works and Kawasaki playing a key role.

- Others: This broad category encompasses diverse applications such as industrial backup power, material handling equipment, and stationary fuel cells. It is expected to grow steadily, contributing tens of billions to the overall market value.

Types:

- Compressed Gas: This remains a dominant segment, particularly for medium-duty vehicles and stationary storage, with projected market growth in the hundreds of billions.

- Cold Compressed Liquid Hydrogen: This segment is poised for rapid expansion due to its high energy density, especially for long-haul transportation and large-scale industrial use, with an estimated market value in the hundreds of billions.

- Solid Compound Hydrogen Storage and Distribution: While still in developmental stages for many applications, this segment holds significant promise for enhanced safety and storage density, with future market potential in the tens of billions.

- Organic Liquid Hydrogen Storage and Distribution: This emerging technology offers a promising alternative for safe and efficient hydrogen transport and storage, with projected market growth in the tens of billions.

Key Drivers of Hydrogen Storage and Distribution Technology Growth

The exponential growth of the Hydrogen Storage and Distribution Technology market is propelled by several key drivers. The global push for decarbonization and stringent environmental regulations are creating an unprecedented demand for clean energy solutions, making hydrogen storage and distribution a critical enabler. Technological advancements, including improvements in storage density, material science, and safety features, are continuously making hydrogen more viable and cost-effective. Government incentives, subsidies, and supportive policies worldwide are accelerating the adoption of hydrogen infrastructure. The increasing commercialization and declining costs of fuel cell technology, particularly in the automotive sector, are driving demand for efficient storage and distribution. Furthermore, the development of a robust hydrogen supply chain, from production to end-use, is vital for market expansion.

Challenges in the Hydrogen Storage and Distribution Technology Sector

Despite its immense potential, the Hydrogen Storage and Distribution Technology sector faces several significant challenges. High upfront capital costs associated with building large-scale storage facilities and distribution networks remain a considerable barrier. Safety concerns, though continuously addressed through technological advancements, persist and require stringent regulatory oversight and public education. The lack of standardized infrastructure and interoperability across different regions and applications can hinder widespread adoption. Supply chain complexities, particularly for specialized materials and components, can lead to bottlenecks and increased costs. Furthermore, the energy-intensive nature of hydrogen liquefaction and compression processes needs to be addressed to ensure the overall sustainability of the hydrogen economy, with potential energy losses impacting overall efficiency by tens of percent.

Emerging Opportunities in Hydrogen Storage and Distribution Technology

The Hydrogen Storage and Distribution Technology market is ripe with emerging opportunities. The expansion of green hydrogen production, powered by renewable energy, is creating a significant demand for large-scale storage solutions. The development of innovative onboard storage systems for heavy-duty trucks, buses, and maritime vessels presents a massive growth avenue. Opportunities also lie in the integration of hydrogen storage with renewable energy grids for enhanced grid stability and energy arbitrage. The development of modular and decentralized hydrogen storage and distribution systems offers potential for localized energy solutions and remote applications. Furthermore, advancements in solid-state storage materials and organic liquid hydrogen technologies are opening doors for novel applications in consumer electronics and portable energy devices, potentially creating new market segments worth billions.

Leading Players in the Hydrogen Storage and Distribution Technology Market

- Iljin Hysolus

- Iwatani

- The Japan Steel Works

- Chart Industries

- Toyota

- Gardner Cryogenics

- Faurecia

- Hexagon Composites

- CLD

- Faber Industrie

- Jiangsu Guofu Hydrogen Energy Equipment

- Kawasaki

- PRAGMA INDUSTRIES

- Whole Win (Beijing) Materials Sci. & Tech

- Hydrogenious Technologies

- Chiyoda Corporation

- Hynertech Co Ltd

Key Developments in Hydrogen Storage and Distribution Technology Industry

- 2023/05: Hexagon Composites announces significant investment in expanding its composite cylinder production capacity to meet growing demand for hydrogen storage solutions.

- 2023/03: Chart Industries secures a major contract for cryogenic fuel systems for a new fleet of hydrogen-powered trucks, highlighting the growth of liquid hydrogen distribution.

- 2022/11: Hydrogenious Technologies demonstrates successful large-scale transport of hydrogen using its LOHC technology, signaling a breakthrough in safe and efficient liquid organic hydrogen carriers.

- 2022/09: Toyota showcases advancements in its hydrogen storage tank technology for its Mirai fuel cell vehicle, improving efficiency and storage capacity.

- 2022/07: Faurecia partners with other industry leaders to develop next-generation hydrogen storage systems for commercial vehicles, aiming for enhanced safety and cost-effectiveness.

- 2022/04: Iwatani accelerates the development of hydrogen refueling stations across Japan, supporting the expansion of FCEV adoption.

- 2021/12: Iljin Hysolus expands its manufacturing facilities to increase the production of high-pressure hydrogen tanks for various applications.

- 2021/09: The Japan Steel Works invests in new technologies for high-pressure hydrogen storage vessels, catering to industrial and transportation needs.

- 2020/06: Faber Industrie introduces innovative cryogenic tanks designed for enhanced efficiency in liquid hydrogen storage and distribution.

Future Outlook for Hydrogen Storage and Distribution Technology Market

The future outlook for the Hydrogen Storage and Distribution Technology market is exceptionally promising, with growth accelerators firmly in place. The sustained global commitment to decarbonization, coupled with increasingly stringent environmental regulations, will continue to fuel demand for hydrogen solutions. Technological advancements will unlock new levels of efficiency, safety, and cost-competitiveness in storage and distribution. Strategic opportunities abound in emerging markets and applications, such as green hydrogen for industrial processes, heavy-duty transport, and aviation. The continued investment in hydrogen infrastructure, driven by both public and private sectors, will create a robust ecosystem for hydrogen deployment. The market is anticipated to witness substantial growth, reaching trillions of dollars in value by the end of the forecast period, presenting significant strategic opportunities for innovation, expansion, and leadership in the global clean energy transition.

Hydrogen Storage and Distribution Technology Segmentation

-

1. Application

- 1.1. New Energy Automobile

- 1.2. Aerospace

- 1.3. Chemical

- 1.4. Others

-

2. Types

- 2.1. Compressed Gas

- 2.2. Cold Compressed Liquid Hydrogen

- 2.3. Solid Compound Hydrogen Storage and Distribution

- 2.4. Organic Liquid Hydrogen Storage and Distribution

Hydrogen Storage and Distribution Technology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hydrogen Storage and Distribution Technology Regional Market Share

Geographic Coverage of Hydrogen Storage and Distribution Technology

Hydrogen Storage and Distribution Technology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. New Energy Automobile

- 5.1.2. Aerospace

- 5.1.3. Chemical

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Compressed Gas

- 5.2.2. Cold Compressed Liquid Hydrogen

- 5.2.3. Solid Compound Hydrogen Storage and Distribution

- 5.2.4. Organic Liquid Hydrogen Storage and Distribution

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. New Energy Automobile

- 6.1.2. Aerospace

- 6.1.3. Chemical

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Compressed Gas

- 6.2.2. Cold Compressed Liquid Hydrogen

- 6.2.3. Solid Compound Hydrogen Storage and Distribution

- 6.2.4. Organic Liquid Hydrogen Storage and Distribution

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. New Energy Automobile

- 7.1.2. Aerospace

- 7.1.3. Chemical

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Compressed Gas

- 7.2.2. Cold Compressed Liquid Hydrogen

- 7.2.3. Solid Compound Hydrogen Storage and Distribution

- 7.2.4. Organic Liquid Hydrogen Storage and Distribution

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. New Energy Automobile

- 8.1.2. Aerospace

- 8.1.3. Chemical

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Compressed Gas

- 8.2.2. Cold Compressed Liquid Hydrogen

- 8.2.3. Solid Compound Hydrogen Storage and Distribution

- 8.2.4. Organic Liquid Hydrogen Storage and Distribution

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. New Energy Automobile

- 9.1.2. Aerospace

- 9.1.3. Chemical

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Compressed Gas

- 9.2.2. Cold Compressed Liquid Hydrogen

- 9.2.3. Solid Compound Hydrogen Storage and Distribution

- 9.2.4. Organic Liquid Hydrogen Storage and Distribution

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Hydrogen Storage and Distribution Technology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. New Energy Automobile

- 10.1.2. Aerospace

- 10.1.3. Chemical

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Compressed Gas

- 10.2.2. Cold Compressed Liquid Hydrogen

- 10.2.3. Solid Compound Hydrogen Storage and Distribution

- 10.2.4. Organic Liquid Hydrogen Storage and Distribution

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Iljin Hysolus

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Iwatani

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 The Japan Steel Works

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Chart Industries

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Toyota

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Gardner Cryogenics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Faurecia

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hexagon Composites

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CLD

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Faber Industrie

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jiangsu Guofu Hydrogen Energy Equipment

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Kawasaki

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 PRAGMA INDUSTRIES

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Whole Win (Beijing) Materials Sci. & Tech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Hydrogenious Technologies

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Chiyoda Corporation

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Hynertech Co Ltd

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Iljin Hysolus

List of Figures

- Figure 1: Global Hydrogen Storage and Distribution Technology Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Hydrogen Storage and Distribution Technology Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Hydrogen Storage and Distribution Technology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hydrogen Storage and Distribution Technology Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Hydrogen Storage and Distribution Technology Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Hydrogen Storage and Distribution Technology Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Hydrogen Storage and Distribution Technology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hydrogen Storage and Distribution Technology Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Hydrogen Storage and Distribution Technology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hydrogen Storage and Distribution Technology Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Hydrogen Storage and Distribution Technology Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Hydrogen Storage and Distribution Technology Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Hydrogen Storage and Distribution Technology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hydrogen Storage and Distribution Technology Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Hydrogen Storage and Distribution Technology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hydrogen Storage and Distribution Technology Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Hydrogen Storage and Distribution Technology Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Hydrogen Storage and Distribution Technology Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Hydrogen Storage and Distribution Technology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hydrogen Storage and Distribution Technology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hydrogen Storage and Distribution Technology Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Hydrogen Storage and Distribution Technology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hydrogen Storage and Distribution Technology Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Hydrogen Storage and Distribution Technology Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Hydrogen Storage and Distribution Technology Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Hydrogen Storage and Distribution Technology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Hydrogen Storage and Distribution Technology Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hydrogen Storage and Distribution Technology Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hydrogen Storage and Distribution Technology?

The projected CAGR is approximately 19.49%.

2. Which companies are prominent players in the Hydrogen Storage and Distribution Technology?

Key companies in the market include Iljin Hysolus, Iwatani, The Japan Steel Works, Chart Industries, Toyota, Gardner Cryogenics, Faurecia, Hexagon Composites, CLD, Faber Industrie, Jiangsu Guofu Hydrogen Energy Equipment, Kawasaki, PRAGMA INDUSTRIES, Whole Win (Beijing) Materials Sci. & Tech, Hydrogenious Technologies, Chiyoda Corporation, Hynertech Co Ltd.

3. What are the main segments of the Hydrogen Storage and Distribution Technology?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hydrogen Storage and Distribution Technology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hydrogen Storage and Distribution Technology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hydrogen Storage and Distribution Technology?

To stay informed about further developments, trends, and reports in the Hydrogen Storage and Distribution Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence