Key Insights

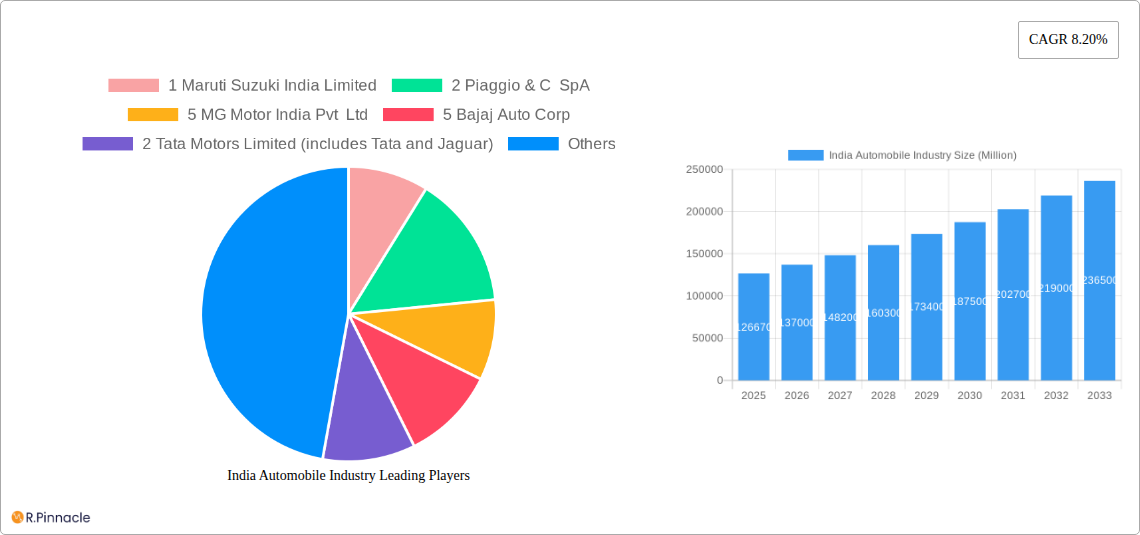

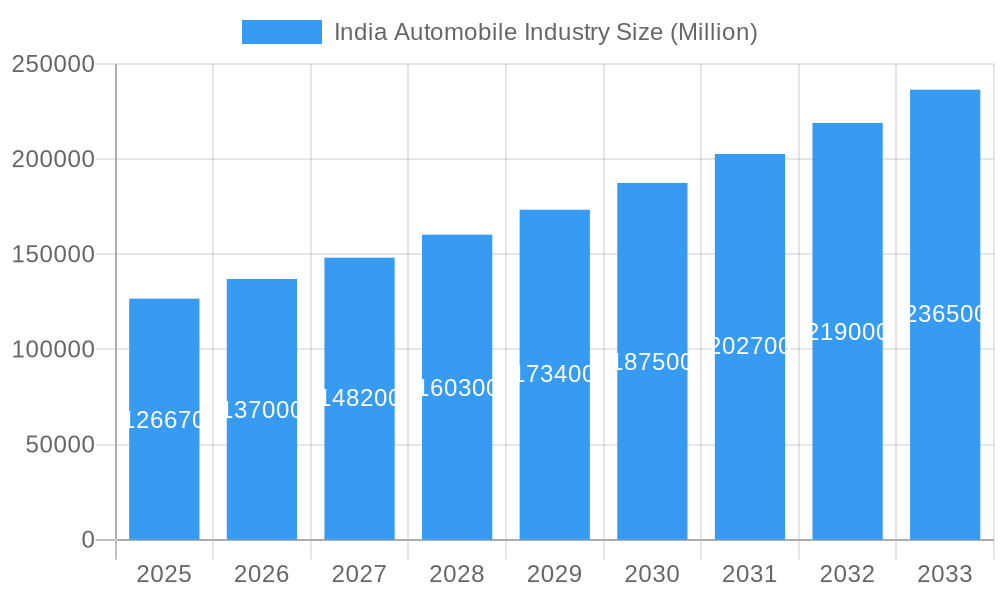

The Indian automobile industry, valued at $126.67 billion in 2025, is projected to experience robust growth, fueled by a compound annual growth rate (CAGR) of 8.20% from 2025 to 2033. This expansion is driven by several factors. Rising disposable incomes and a burgeoning middle class are stimulating demand for personal vehicles, particularly two-wheelers and passenger cars. Government initiatives promoting infrastructure development and electric vehicle (EV) adoption are further accelerating market growth. The increasing urbanization and the need for efficient last-mile connectivity are boosting the demand for three-wheelers and commercial vehicles. However, challenges remain. Fluctuations in fuel prices, stringent emission norms, and the ongoing semiconductor shortage pose potential restraints on the industry's growth trajectory. The market is segmented by vehicle type (two-wheelers, passenger cars, commercial vehicles, three-wheelers), fuel type (diesel, petrol/gasoline, CNG and LPG, electric, others), and region (North, South, East, and West India). The competitive landscape is dominated by a mix of established global and domestic players, each vying for market share through product innovation, strategic partnerships, and aggressive marketing campaigns. The electric vehicle segment is expected to witness significant growth in the coming years, driven by government incentives and increasing consumer awareness of environmental sustainability.

India Automobile Industry Market Size (In Billion)

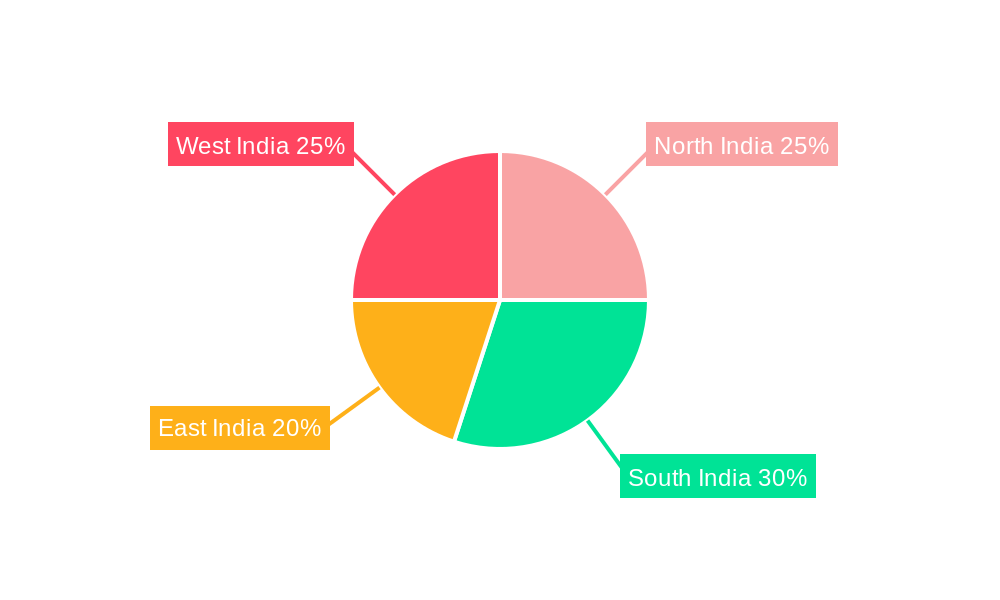

The regional distribution of market share reflects the varying levels of economic development and infrastructure across India. While the South and West regions currently hold larger shares due to higher per capita income and infrastructure development, the North and East regions are expected to witness considerable growth, fueled by rising incomes and improving infrastructure. The industry is characterized by intense competition, with key players constantly innovating to capture market share. The success of individual companies will depend on their ability to adapt to evolving consumer preferences, navigate regulatory changes, and manage supply chain disruptions effectively. The forecast period, 2025-2033, promises significant opportunities, particularly for companies focusing on technological advancements in electric vehicles and connected car technologies. The industry's sustained growth will significantly contribute to India's overall economic development.

India Automobile Industry Company Market Share

India Automobile Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Indian automobile industry, covering market dynamics, key players, emerging trends, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and strategists.

India Automobile Industry Market Structure & Innovation Trends

The Indian automobile market is a vibrant and complex ecosystem, characterized by a strong presence of both global automotive powerhouses and ambitious domestic manufacturers. Market concentration varies considerably across different vehicle segments, with the highly competitive two-wheeler sector standing in contrast to the more consolidated passenger car segment. Innovation is a powerful force, primarily propelled by the imperative of meeting stringent emission standards like BS-VI, a surging consumer appetite for cutting-edge safety technologies, and the undeniable momentum of electric vehicle (EV) adoption. The regulatory landscape, encompassing crucial elements such as import duties and localization policies, exerts a profound influence on market dynamics. Furthermore, the availability of product substitutes, including robust public transportation networks and the ubiquitous rise of ride-sharing services, especially in urban centers, significantly shapes consumer choices. The demographic profile of end-users, marked by a growing segment of young and aspirational individuals, plays a pivotal role in dictating demand patterns. The industry has also been a hotbed of consolidation, with substantial Mergers and Acquisitions (M&A) activity observed in recent years, with deal values reaching approximately **$X.XX Billion USD** in the past five years (placeholder for actual data).

- Market Share: Maruti Suzuki continues to command a substantial market share in the passenger car segment, while Hero MotoCorp remains the undisputed leader in the two-wheeler market.

- M&A Activity: Recent strategic alliances and acquisitions have primarily focused on accelerating technology integration, facilitating expansion into burgeoning new segments, and gaining access to untapped markets. For instance, the collaborative venture between TVS Motor Company and Mitsubishi Heavy Industries exemplifies strategic partnerships aimed at advancing electric vehicle technology and global market penetration.

India Automobile Industry Market Dynamics & Trends

The Indian automobile industry demonstrates robust growth, driven primarily by rising disposable incomes, increasing urbanization, and expanding infrastructure. Technological advancements, including the adoption of electric and hybrid vehicles, are reshaping the landscape. Consumer preferences are shifting toward safer, more fuel-efficient, and technologically advanced vehicles. Competitive dynamics are intense, with players constantly vying for market share through product innovation, aggressive pricing strategies, and strategic partnerships. The Compound Annual Growth Rate (CAGR) for the overall market is projected at xx% during the forecast period, with significant variations across segments. Market penetration of electric vehicles is steadily increasing, though from a relatively low base.

Dominant Regions & Segments in India Automobile Industry

- By Vehicle Type: The two-wheeler segment continues to reign supreme as the largest contributor to the market, driven by its inherent affordability and pervasive usage across a wide spectrum of demographic groups. Passenger cars represent the second-largest segment, followed closely by commercial vehicles and the agile three-wheeler segment.

- By Fuel Type: Petrol/Gasoline remains the predominant fuel type powering the majority of vehicles. However, the market share of electric vehicles is experiencing an impressive and sustained growth trajectory. Diesel fuel continues to maintain a significant presence, particularly within the commercial vehicle category. Compressed Natural Gas (CNG) and Liquefied Petroleum Gas (LPG) cater to specific niche markets.

- By Region: Currently, North and West India hold the largest market share, largely attributable to their higher population density and robust economic activity. Nonetheless, South and East India are emerging as dynamic growth corridors, exhibiting significant potential fueled by ongoing infrastructure development and a steady rise in disposable incomes.

The prevailing dominance of specific regions and segments is intricately linked to a confluence of influencing factors:

- Economic Policies: Proactive government initiatives, particularly those promoting vehicle electrification, fostering robust infrastructure development, and incentivizing domestic manufacturing, contribute significantly to the growth dynamics of various regions.

- Infrastructure: The presence of well-developed road networks, coupled with the expansion of charging infrastructure, plays a critical role in facilitating broader vehicle adoption and enhancing consumer confidence.

India Automobile Industry Product Innovations

The Indian automobile industry is currently experiencing a remarkable period of product innovation, characterized by significant advancements in vehicle electrification, enhanced connectivity features, and a heightened emphasis on safety technologies. Manufacturers are strategically prioritizing the development of cost-effective and highly fuel-efficient vehicles to effectively cater to the price-sensitive nature of the Indian market. The integration of sophisticated technologies such as Advanced Driver-Assistance Systems (ADAS) and intuitive infotainment systems is steadily gaining traction, leading to a richer and more engaging user experience. The market is witnessing a pronounced surge in the adoption of electric two-wheelers and three-wheelers, propelled by attractive government incentives and a growing societal consciousness towards environmental sustainability.

Report Scope & Segmentation Analysis

This report segments the Indian automobile market by vehicle type (two-wheelers, passenger cars, commercial vehicles, three-wheelers), fuel type (diesel, petrol/gasoline, CNG and LPG, electric, others), and region (North, South, East, West India). Each segment is analyzed in detail, including growth projections, market size estimates, and competitive dynamics. Growth is expected to be substantial across all segments, driven by a combination of macroeconomic trends and technological innovations. The competitive landscape is highly fragmented, with a mix of domestic and international players.

Key Drivers of India Automobile Industry Growth

A confluence of powerful factors is acting as catalysts for the robust growth of the Indian automobile industry. These include the continuous expansion of the middle class, accompanied by a corresponding increase in disposable income, supportive government policies that champion infrastructure development and bolster domestic manufacturing capabilities, and ongoing technological advancements that are yielding improvements in fuel efficiency and the introduction of enhanced vehicle features. The government's unwavering commitment to promoting electric vehicles further significantly contributes to the industry's upward growth trajectory.

Challenges in the India Automobile Industry Sector

Despite its promising outlook, the Indian automobile industry grapples with a set of persistent challenges. These include vulnerability to supply chain disruptions, the significant capital investment and technological recalibration required to comply with increasingly stringent emission norms, and the volatility of raw material prices. The competitive landscape is exceptionally fierce, and the market's inherent susceptibility to macroeconomic fluctuations presents additional hurdles. Furthermore, evolving regulatory frameworks and existing infrastructure limitations in certain geographic areas can impede the industry's overall progress. For instance, the substantial cost associated with transitioning to electric vehicles and the ongoing lack of widespread and accessible charging infrastructure represent considerable obstacles to widespread EV adoption.

Emerging Opportunities in India Automobile Industry

The Indian automobile industry presents numerous opportunities. The rising adoption of electric vehicles and connected car technologies offers significant growth potential. Expanding into rural markets and focusing on affordable and fuel-efficient vehicles presents substantial opportunities. The government's focus on infrastructure development creates further avenues for growth.

Leading Players in the India Automobile Industry Market

- Maruti Suzuki India Limited

- Piaggio & C SpA

- MG Motor India Pvt Ltd

- Bajaj Auto Corp

- Tata Motors Limited

- Hero Moto Corp

- Atul Auto Limited

- Mercedes-Benz India Pvt Ltd

- Honda Motorcycle & Scooter India Pvt Ltd

- Terra Motors India Corp

- Renault Group

- TVS Motor Company

- Volkswagen India

- Kinetic Green Energy & Power Solutions Lt

- Mahindra & Mahindra Limited

- Suzuki Motorcycle India Private Limited

- Royal Enfield

- Scooters India Ltd

- Honda Cars India Ltd

- Lohia Auto Industries

- Hyundai Motor India Ltd

- BMW AG

- BYD Company Ltd

Key Developments in India Automobile Industry Industry

- January 2024: Maruti Suzuki announced plans to build a new car manufacturing facility in Gujarat with an annual capacity of 1 Million vehicles, representing a significant investment of INR 35,000 crore (USD 4.2 Billion).

- February 2024: TVS Mobility secured a 32% stake from Mitsubishi Corporation, a Japanese conglomerate, in TVS Vehicles Mobility Solutions (TVS VMS) through an investment of INR 300 crore (USD 40 Million), signifying growing interest in the Indian electric vehicle sector.

Future Outlook for India Automobile Industry Market

The future of the Indian automobile industry is bright, fueled by continued economic growth, technological advancements, and government support for the electric vehicle sector. The market is poised for sustained expansion, with significant opportunities for players who can adapt to changing consumer preferences and technological disruptions. Strategic partnerships, product innovation, and a focus on sustainable practices will be key factors in determining future success.

India Automobile Industry Segmentation

-

1. Vehicle Type

- 1.1. Two-wheelers

- 1.2. Passenger Cars

- 1.3. Commercial Vehicles

- 1.4. Three-wheelers

-

2. Fuel Type

- 2.1. Diesel

- 2.2. Petrol/Gasoline

- 2.3. CNG and LPG

- 2.4. Electric

- 2.5. Others

India Automobile Industry Segmentation By Geography

- 1. India

India Automobile Industry Regional Market Share

Geographic Coverage of India Automobile Industry

India Automobile Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 The Growing Economy

- 3.2.2 Coupled with Rising Disposal Incomes and Urbanization

- 3.2.3 Fuels Demand for the Market

- 3.3. Market Restrains

- 3.3.1 Various Regulatory Changes

- 3.3.2 Safety Standards

- 3.3.3 and Taxation Policies by the Government may Hamper the Market

- 3.4. Market Trends

- 3.4.1. The Two-Wheelers Segment to Register Fastest Growth over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Automobile Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Two-wheelers

- 5.1.2. Passenger Cars

- 5.1.3. Commercial Vehicles

- 5.1.4. Three-wheelers

- 5.2. Market Analysis, Insights and Forecast - by Fuel Type

- 5.2.1. Diesel

- 5.2.2. Petrol/Gasoline

- 5.2.3. CNG and LPG

- 5.2.4. Electric

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 1 Maruti Suzuki India Limited

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 2 Piaggio & C SpA

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 5 MG Motor India Pvt Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 5 Bajaj Auto Corp

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 2 Tata Motors Limited (includes Tata and Jaguar)

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 2 Hero Moto Corp

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 4 Atul Auto Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 11 Mercedes-Benz India Pvt Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 3 Honda Motorcycle & Scooter India Pvt Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 5 Terra Motors India Corp

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 7 Renault Group (Includes Nissan and Renault)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Two-wheelers

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 1 TVS Motor Company

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Three-wheelers

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 6 Volkswagen India

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 6 Kinetic Green Energy & Power Solutions Lt

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Passenger Cars and Commercial Vehicles

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 4 Mahindra & Mahindra Limited

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 6 Suzuki Motorcycle India Private Limited

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 4 Royal Enfield

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 3 Scooters India Ltd

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 8 Honda Cars India Ltd

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.23 1 Lohia Auto Industries

- 6.2.23.1. Overview

- 6.2.23.2. Products

- 6.2.23.3. SWOT Analysis

- 6.2.23.4. Recent Developments

- 6.2.23.5. Financials (Based on Availability)

- 6.2.24 3 Hyundai Motor India Ltd

- 6.2.24.1. Overview

- 6.2.24.2. Products

- 6.2.24.3. SWOT Analysis

- 6.2.24.4. Recent Developments

- 6.2.24.5. Financials (Based on Availability)

- 6.2.25 10 BMW AG (includes BMW and MINI)

- 6.2.25.1. Overview

- 6.2.25.2. Products

- 6.2.25.3. SWOT Analysis

- 6.2.25.4. Recent Developments

- 6.2.25.5. Financials (Based on Availability)

- 6.2.26 9 BYD Company Ltd

- 6.2.26.1. Overview

- 6.2.26.2. Products

- 6.2.26.3. SWOT Analysis

- 6.2.26.4. Recent Developments

- 6.2.26.5. Financials (Based on Availability)

- 6.2.1 1 Maruti Suzuki India Limited

List of Figures

- Figure 1: India Automobile Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Automobile Industry Share (%) by Company 2025

List of Tables

- Table 1: India Automobile Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: India Automobile Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 3: India Automobile Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: India Automobile Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 5: India Automobile Industry Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 6: India Automobile Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Automobile Industry?

The projected CAGR is approximately 8.20%.

2. Which companies are prominent players in the India Automobile Industry?

Key companies in the market include 1 Maruti Suzuki India Limited, 2 Piaggio & C SpA, 5 MG Motor India Pvt Ltd, 5 Bajaj Auto Corp, 2 Tata Motors Limited (includes Tata and Jaguar), 2 Hero Moto Corp, 4 Atul Auto Limited, 11 Mercedes-Benz India Pvt Ltd, 3 Honda Motorcycle & Scooter India Pvt Ltd, 5 Terra Motors India Corp, 7 Renault Group (Includes Nissan and Renault), Two-wheelers, 1 TVS Motor Company, Three-wheelers, 6 Volkswagen India, 6 Kinetic Green Energy & Power Solutions Lt, Passenger Cars and Commercial Vehicles, 4 Mahindra & Mahindra Limited, 6 Suzuki Motorcycle India Private Limited, 4 Royal Enfield, 3 Scooters India Ltd, 8 Honda Cars India Ltd, 1 Lohia Auto Industries, 3 Hyundai Motor India Ltd, 10 BMW AG (includes BMW and MINI), 9 BYD Company Ltd.

3. What are the main segments of the India Automobile Industry?

The market segments include Vehicle Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 126.67 Million as of 2022.

5. What are some drivers contributing to market growth?

The Growing Economy. Coupled with Rising Disposal Incomes and Urbanization. Fuels Demand for the Market.

6. What are the notable trends driving market growth?

The Two-Wheelers Segment to Register Fastest Growth over the Forecast Period.

7. Are there any restraints impacting market growth?

Various Regulatory Changes. Safety Standards. and Taxation Policies by the Government may Hamper the Market.

8. Can you provide examples of recent developments in the market?

January 2024: Maruti Suzuki India intended to build a car production facility in Gujarat, India, capable of manufacturing 1 million vehicles annually, with an estimated investment of around INR 35,000 crore (USD 4.2 billion). This move is expected to bolster the Indian automobile industry significantly.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Automobile Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Automobile Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Automobile Industry?

To stay informed about further developments, trends, and reports in the India Automobile Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence