Key Insights

India's electric vehicle (EV) sector is experiencing robust expansion, projected at a Compound Annual Growth Rate (CAGR) of 57.23% from 2025 to 2033. This growth is propelled by supportive government incentives, increasing fuel costs, heightened environmental consciousness, and technological advancements in battery technology, charging infrastructure, and vehicle performance. The market encompasses diverse vehicle types, including two-wheelers, passenger cars, and commercial vehicles (ranging from medium-duty trucks to buses), and fuel categories such as Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and Fuel Cell Electric Vehicles (FCEVs). Leading manufacturers like Tata Motors, Mahindra & Mahindra, Hyundai, and prominent two-wheeler brands are significantly investing in research and development and expanding their EV offerings to meet escalating demand across India's various regions. While two-wheelers currently lead in market share, passenger and commercial vehicle segments are anticipated to witness substantial growth. Key challenges include the need for enhanced charging infrastructure, particularly in rural areas, and addressing consumer concerns regarding range and battery life. Despite these, the Indian EV market presents a highly promising outlook with significant opportunities for established and emerging players. The estimated market size in 2025 is 2.3 million units, with a projected market size of $10 billion by the base year 2025. This signifies a lucrative investment landscape, contingent on strategic adaptation to consumer preferences, efficient supply chain management, and navigating regulatory shifts. The competitive environment is dynamic, with both domestic and international companies competing fiercely. Companies are prioritizing localization to reduce costs and leverage government support. Future growth will be driven by advancements in battery technology, charging solutions, and sustained government support for sustainable transportation. The growth of India's EV industry is critical for economic development and achieving the nation's climate change objectives.

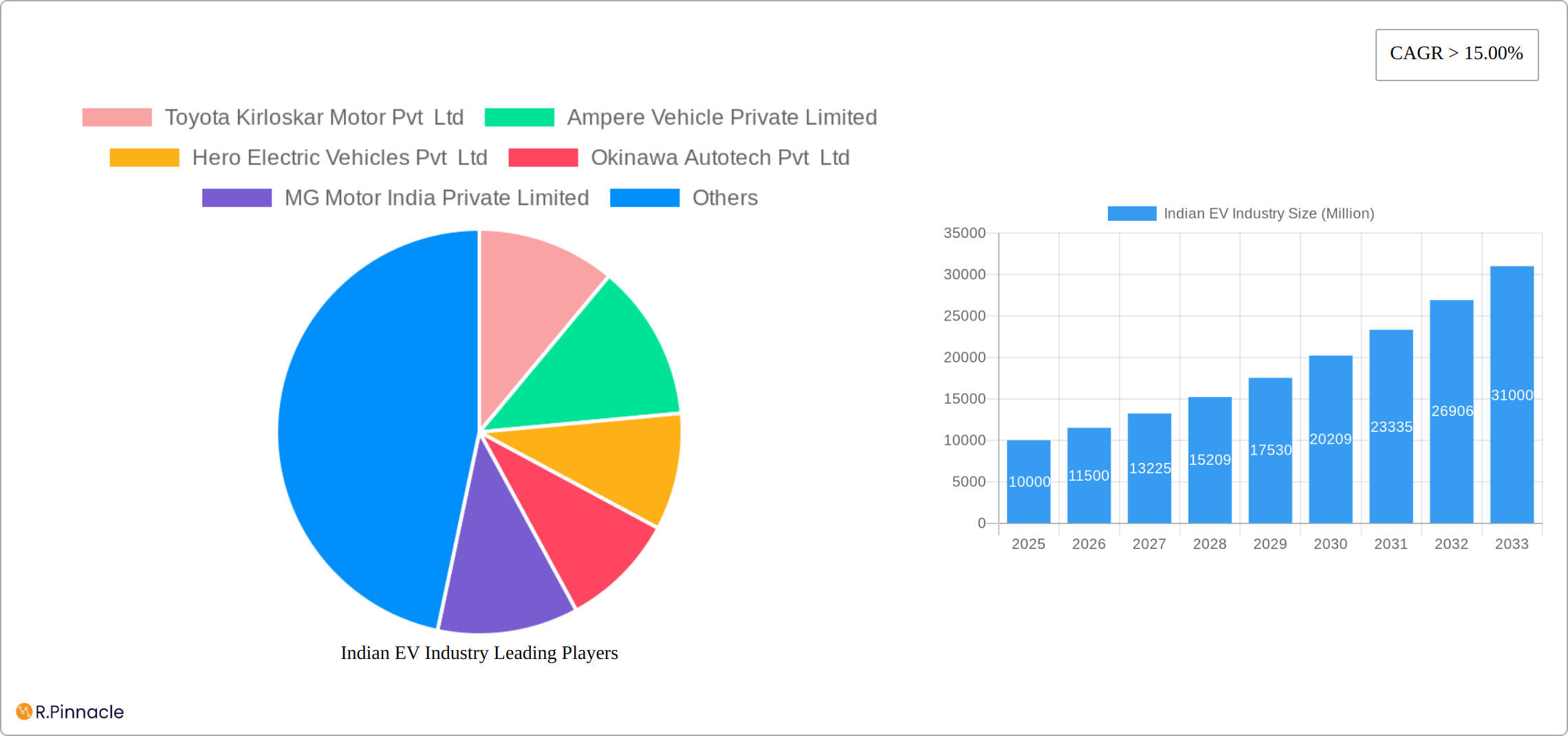

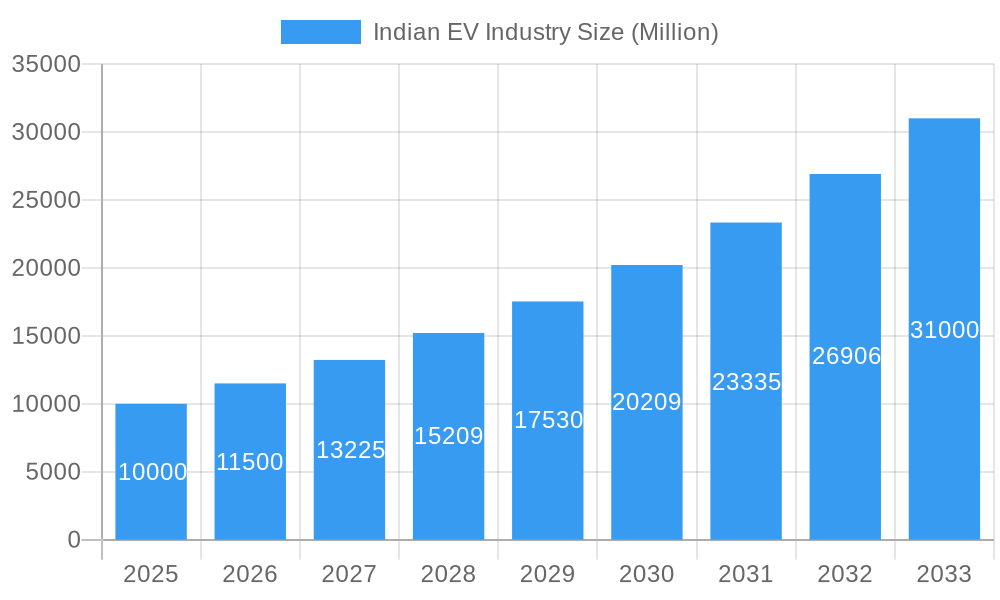

Indian EV Industry Market Size (In Million)

Indian EV Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Indian Electric Vehicle (EV) industry, offering invaluable insights for industry professionals, investors, and policymakers. Covering the period from 2019 to 2033, with a base year of 2025, this report projects a dynamic market poised for significant growth. The report leverages robust data and analysis to forecast market trends and identify key opportunities and challenges. Expect detailed segmentation analysis across vehicle types, fuel categories, and geographic regions, incorporating the latest industry developments and competitive landscape. This report is essential for anyone seeking a complete understanding of the burgeoning Indian EV market.

Indian EV Industry Company Market Share

Indian EV Industry Market Structure & Innovation Trends

The Indian EV market presents a dynamic landscape, characterized by a blend of established automotive giants and agile startups, resulting in a moderately fragmented yet rapidly evolving structure. While Tata Motors and Mahindra & Mahindra maintain significant market share in the passenger vehicle segment, exhibiting strong brand recognition and established distribution networks, the two-wheeler segment showcases intense competition. Key players like Ola Electric, Ather Energy, Hero Electric, and Okinawa Autotech are aggressively vying for dominance, leveraging innovative technologies and aggressive marketing strategies. Innovation within the industry is fueled by a confluence of factors: government incentives designed to accelerate adoption (such as the Faster Adoption and Manufacturing of (Hybrid &) Electric Vehicles in India (FAME) scheme), rapid advancements in battery technology leading to increased range and reduced charging times, the development of robust charging infrastructure, and a burgeoning consumer preference for environmentally sustainable transportation solutions. The regulatory environment, shaped by initiatives like FAME, plays a pivotal role in guiding the industry's growth trajectory. Internal combustion engine (ICE) vehicles, while still present, face a shrinking market share as consumer attitudes shift and the cost-effectiveness of EVs improves. The end-user demographic is broadening, driven by rising middle-class disposable incomes and a growing awareness of environmental issues. A notable surge in mergers and acquisitions (M&A) activity, with deal values exceeding xx Million in recent years, signals industry consolidation and strategic partnerships aimed at accelerating growth and enhancing competitiveness. This trend suggests a move towards greater market concentration in the coming years.

- Market Concentration: Moderately fragmented, shifting towards consolidation with key players strengthening their positions.

- Innovation Drivers: Government incentives (FAME), breakthroughs in battery technology (e.g., solid-state batteries), expanding charging infrastructure, and evolving consumer preferences.

- Regulatory Frameworks: FAME scheme, supportive policies promoting domestic manufacturing and R&D, and evolving emission standards.

- M&A Activity: Significant deal values exceeding xx Million in recent years, indicating strategic alliances and market consolidation.

Indian EV Industry Market Dynamics & Trends

The Indian EV market exhibits robust growth, driven by several key factors. The Compound Annual Growth Rate (CAGR) is projected to be xx% during the forecast period (2025-2033), indicating significant market expansion. This growth is fueled by government initiatives promoting EV adoption, decreasing battery costs, and rising consumer awareness regarding environmental sustainability. Technological disruptions, such as advancements in battery technology and charging infrastructure, are accelerating the transition to EVs. Consumer preferences are shifting towards electric two-wheelers and smaller passenger vehicles due to affordability and practicality. Competitive dynamics are intense, with both established and new players aggressively pursuing market share through product innovation, strategic partnerships, and aggressive pricing strategies. Market penetration is expected to reach xx% by 2033.

Dominant Regions & Segments in Indian EV Industry

The Indian EV market exhibits diverse growth patterns across geographical regions and vehicle segments. While comprehensive data is needed to definitively identify the most dominant region, urban centers and states with proactive EV policies are experiencing accelerated adoption rates. This is largely due to better charging infrastructure availability and consumer awareness campaigns. The two-wheeler segment consistently demonstrates strong performance, capturing a substantial portion of the overall market share. This is attributed to its affordability, suitability for urban commuting, and the availability of a wider range of models catering to different needs and budgets.

- Two-Wheelers: High demand fueled by affordability, practicality for urban commuting, increasing urbanization, government incentives, and rising fuel prices. The segment is witnessing intense innovation in battery technology and design.

- Passenger Vehicles: A rapidly growing segment propelled by rising disposable incomes, a preference for electric SUVs and hatchbacks, and advancements in battery technology resulting in extended vehicle range and improved performance.

- Commercial Vehicles: This segment is poised for substantial expansion driven by the escalating demand for sustainable transportation solutions within logistics and fleet operations. Cost savings on fuel and government incentives are significant drivers.

- Fuel Category: Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs) currently dominate the market, with Fuel Cell Electric Vehicles (FCEVs) still in their early stages of development due to infrastructure limitations.

- Medium-duty Commercial Trucks: Significant growth is anticipated due to the growing need for efficient and environmentally friendly logistics solutions, particularly in last-mile delivery.

Indian EV Industry Product Innovations

The Indian EV industry is witnessing rapid product innovation, particularly in the two-wheeler segment. Manufacturers are focusing on improving battery technology, range, charging infrastructure, and integrating smart features. Competitive advantages are increasingly defined by battery life, charging speed, and cost-effectiveness. Technological trends include the development of solid-state batteries, advanced battery management systems, and improved motor efficiency. Market fit is crucial, with products tailored to specific customer needs and price points.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Indian EV market, segmented by vehicle type (two-wheelers, passenger vehicles, commercial vehicles, medium-duty commercial trucks), fuel category (FCEV, HEV, Battery Electric Vehicles), and region. Growth projections vary significantly across segments, with two-wheelers and passenger vehicles anticipated to experience the most rapid expansion. Market sizes are estimated in Millions of units, and revenue is projected in Millions of Indian Rupees, offering a detailed financial perspective. The competitive landscape is thoroughly examined, highlighting the varying levels of market concentration and competitive intensity across different segments.

Key Drivers of Indian EV Industry Growth

The remarkable growth of the Indian EV industry is propelled by several key factors, creating a powerful synergy for expansion:

- Robust Government Support: Policies like FAME-II provide substantial subsidies and incentives, significantly reducing the upfront cost of EVs for consumers.

- Decreasing Battery Costs: Continuous advancements in battery technology and economies of scale are driving down battery prices, making EVs increasingly cost-competitive with ICE vehicles.

- Rising Fuel Prices: The escalating cost of petrol and diesel fuels is making EVs a more financially attractive proposition for consumers, particularly in the long run.

- Growing Environmental Awareness: Increasing consumer consciousness regarding environmental sustainability and the impact of carbon emissions is fueling demand for eco-friendly transportation options.

- Technological Advancements: Rapid innovation in battery technology, charging infrastructure, and vehicle design is continually improving the performance, range, and convenience of EVs.

Challenges in the Indian EV Industry Sector

The Indian EV industry faces several challenges including:

- Limited charging infrastructure, especially outside major cities.

- High initial cost of EVs compared to ICE vehicles.

- Range anxiety among consumers.

- Dependence on imports for certain EV components.

- The need for substantial investment in battery manufacturing and recycling facilities.

Emerging Opportunities in Indian EV Industry

The Indian EV industry presents several emerging opportunities, including:

- Growth in rural markets with the development of appropriate charging infrastructure and affordable EV models.

- Expansion into the commercial vehicle segment with specialized EV solutions for various applications.

- Development of innovative battery technologies with extended range and faster charging times.

- Integration of smart features and connectivity solutions.

- Investments in the battery recycling industry.

Leading Players in the Indian EV Industry Market

- Toyota Kirloskar Motor Pvt Ltd

- Ampere Vehicle Private Limited

- Hero Electric Vehicles Pvt Ltd

- Okinawa Autotech Pvt Ltd

- MG Motor India Private Limited

- Tata Motors Limited

- Olectra Greentech Ltd

- BYD India Private Limited

- TVS Motor Company Limited

- Mahindra & Mahindra Limited

- JBM Auto Limited

- Switch Mobility (Ashok Leyland Limited)

- Hyundai Motor India Limited

- Ola Electric Mobility Pvt Ltd

- Ather Energy Pvt Ltd

Key Developments in Indian EV Industry Industry

- August 2023: Ola Electric launched the S1X electric scooter at INR 79,999, offering two battery options with ranges of 91 km and 151 km.

- August 2023: Gabriel India Limited announced the development of components for Maruti Suzuki Jimny and Stellantis electric Citroen C3, and ongoing development for other manufacturers like VW, Tata, and Mahindra.

- August 2023: Hyundai Motor India Limited signed an asset purchase agreement for the acquisition of General Motors India's Talegaon Plant.

Future Outlook for Indian EV Industry Market

The Indian EV market is projected to experience substantial growth over the next decade. Continued government support, technological advancements, decreasing battery costs, and increasing consumer awareness are all expected to contribute to this growth. Strategic investments in charging infrastructure and battery manufacturing are crucial to realizing the full potential of the market. Opportunities exist for both established players and new entrants to innovate and capture market share in this rapidly expanding sector.

Indian EV Industry Segmentation

-

1. Vehicle Type

-

1.1. Commercial Vehicles

- 1.1.1. Buses

- 1.1.2. Heavy-duty Commercial Trucks

- 1.1.3. Light Commercial Pick-up Trucks

- 1.1.4. Light Commercial Vans

- 1.1.5. Medium-duty Commercial Trucks

-

1.2. Passenger Vehicles

- 1.2.1. Hatchback

- 1.2.2. Multi-purpose Vehicle

- 1.2.3. Sedan

- 1.2.4. Sports Utility Vehicle

- 1.3. Two-Wheelers

-

1.1. Commercial Vehicles

-

2. Fuel Category

- 2.1. FCEV

- 2.2. HEV

Indian EV Industry Segmentation By Geography

- 1. India

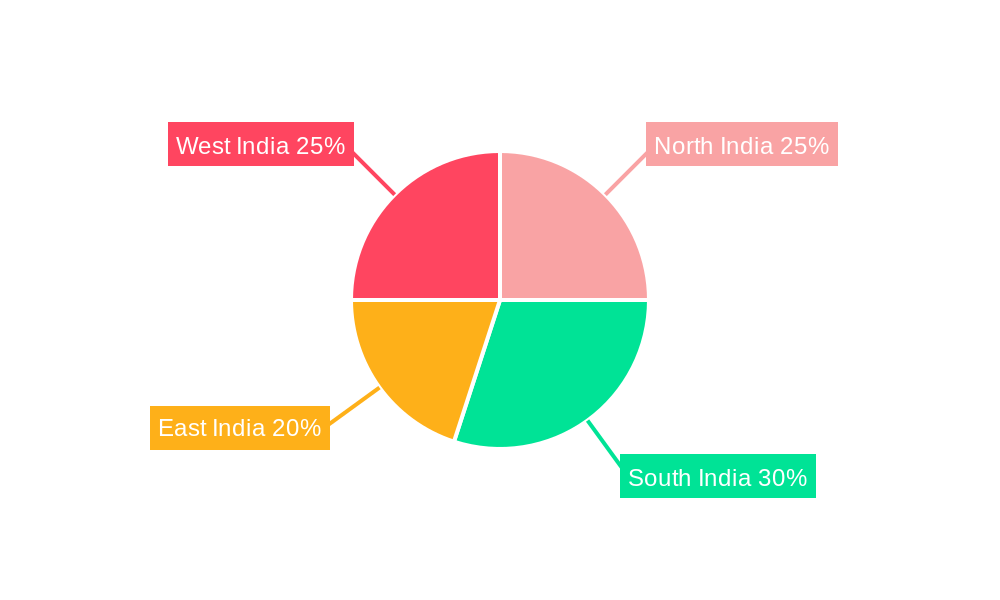

Indian EV Industry Regional Market Share

Geographic Coverage of Indian EV Industry

Indian EV Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 57.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise in Vehicle Electrification

- 3.3. Market Restrains

- 3.3.1. The Cost of Raw Materials Used in the Manufacturing of Switches is High

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indian EV Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.1.1. Buses

- 5.1.1.2. Heavy-duty Commercial Trucks

- 5.1.1.3. Light Commercial Pick-up Trucks

- 5.1.1.4. Light Commercial Vans

- 5.1.1.5. Medium-duty Commercial Trucks

- 5.1.2. Passenger Vehicles

- 5.1.2.1. Hatchback

- 5.1.2.2. Multi-purpose Vehicle

- 5.1.2.3. Sedan

- 5.1.2.4. Sports Utility Vehicle

- 5.1.3. Two-Wheelers

- 5.1.1. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Fuel Category

- 5.2.1. FCEV

- 5.2.2. HEV

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Toyota Kirloskar Motor Pvt Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Ampere Vehicle Private Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Hero Electric Vehicles Pvt Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Okinawa Autotech Pvt Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 MG Motor India Private Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Tata Motors Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Olectra Greentech Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 BYD India Private Limited

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 TVS Motor Company Limite

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Mahindra & Mahindra Limited

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 JBM Auto Limited

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Switch Mobility (Ashok Leyland Limited)

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Hyundai Motor India Limited

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Ola Electric Mobility Pvt Ltd

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Ather Energy Pvt Ltd

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.1 Toyota Kirloskar Motor Pvt Ltd

List of Figures

- Figure 1: Indian EV Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Indian EV Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian EV Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Indian EV Industry Revenue million Forecast, by Fuel Category 2020 & 2033

- Table 3: Indian EV Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Indian EV Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 5: Indian EV Industry Revenue million Forecast, by Fuel Category 2020 & 2033

- Table 6: Indian EV Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian EV Industry?

The projected CAGR is approximately 57.23%.

2. Which companies are prominent players in the Indian EV Industry?

Key companies in the market include Toyota Kirloskar Motor Pvt Ltd, Ampere Vehicle Private Limited, Hero Electric Vehicles Pvt Ltd, Okinawa Autotech Pvt Ltd, MG Motor India Private Limited, Tata Motors Limited, Olectra Greentech Ltd, BYD India Private Limited, TVS Motor Company Limite, Mahindra & Mahindra Limited, JBM Auto Limited, Switch Mobility (Ashok Leyland Limited), Hyundai Motor India Limited, Ola Electric Mobility Pvt Ltd, Ather Energy Pvt Ltd.

3. What are the main segments of the Indian EV Industry?

The market segments include Vehicle Type, Fuel Category.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.3 million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Vehicle Electrification.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

The Cost of Raw Materials Used in the Manufacturing of Switches is High.

8. Can you provide examples of recent developments in the market?

August 2023: Ola Electric launched S1X for INR 79,999. Ola S1X will be offered in two battery capacities 2-kWh and 3-kWh. The 2-kWh variant will have a range of 91 km while the 3-kWh will have a 151 km range. The scooter has a 3.5-inch segmented display, the physical key unlocks and comes Without smart connectivity.August 2023: Gabriel India Limited (Gabriel India), a flagship company of Anand Group, announced that during the quarter that ended on June 30, 2023, it has developed components for Maruti Suzuki Jimny and Stellantis electric Citroen C3. At present it is developing parts for new models of VW, Tata, Stellantis, Mahindra, and Maruti Suzuki.August 2023: Hyundai Motor India Limited (HMIL) signed an asset purchase agreement (APA), in Gurugram, Haryana, for the acquisition and assignment of identified assets related to General Motors India (GMI)’s Talegaon Plant in Maharashtra.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian EV Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian EV Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian EV Industry?

To stay informed about further developments, trends, and reports in the Indian EV Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence