Key Insights

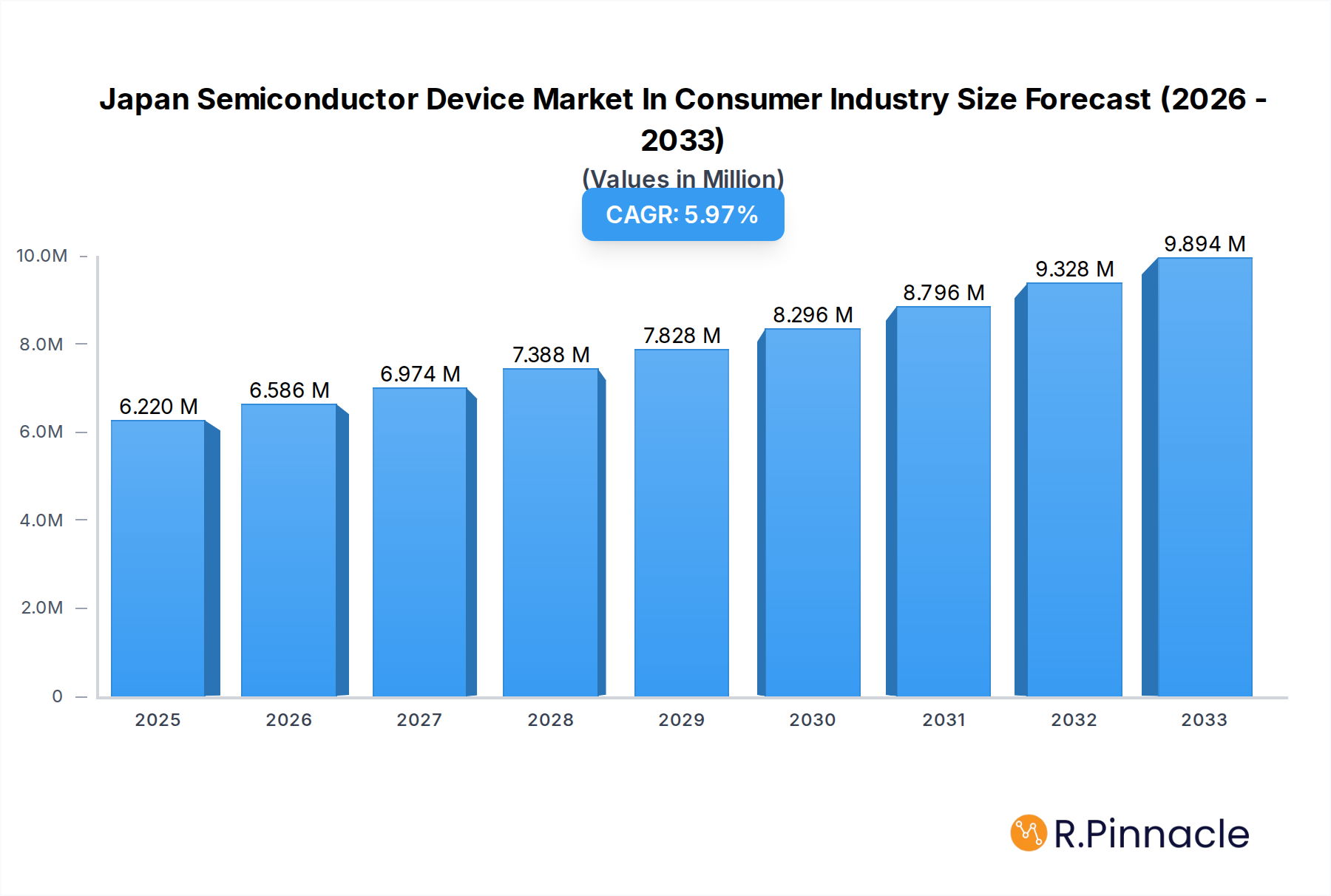

The Japan Semiconductor Device Market in the Consumer Industry is poised for significant expansion, projected to reach 6.22 Million Value Unit by 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.90% anticipated over the forecast period. This growth is primarily fueled by the burgeoning demand for sophisticated consumer electronics, including smartphones, smart home devices, wearable technology, and advanced gaming consoles. The increasing integration of artificial intelligence (AI) and the Internet of Things (IoT) into everyday appliances necessitates higher-performance and more energy-efficient semiconductor solutions. Key drivers include the continuous innovation in consumer product design, the rising disposable incomes among Japanese consumers, and the government's strategic initiatives to bolster domestic semiconductor manufacturing and R&D. Furthermore, the ongoing evolution of display technologies, advancements in audio-visual equipment, and the widespread adoption of 5G connectivity are creating sustained demand for a diverse range of semiconductor components, from advanced microprocessors and microcontrollers to specialized optoelectronics and sensors.

Japan Semiconductor Device Market In Consumer Industry Market Size (In Million)

While the market presents a promising outlook, certain factors may present challenges. The intense global competition and the high capital expenditure required for semiconductor fabrication facilities could impact profit margins. Additionally, supply chain disruptions, particularly those stemming from geopolitical factors or natural disasters, remain a persistent concern for the electronics industry. However, Japan's strong foundational expertise in precision manufacturing, its commitment to quality, and its established presence in niche semiconductor segments like optoelectronics and specialized ICs position it favorably to navigate these challenges. The market is characterized by a dynamic segmentation, with integrated circuits, particularly microprocessors (MPU), microcontrollers (MCU), and digital signal processors, alongside discrete semiconductors and sensors, forming the core demand. Leading players like Infineon Technologies AG, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Samsung Electronics Co Ltd, and Texas Instruments Inc. are actively investing in R&D and strategic partnerships to capitalize on emerging opportunities within the Japanese consumer electronics landscape.

Japan Semiconductor Device Market In Consumer Industry Company Market Share

Gain unparalleled insights into Japan's dynamic semiconductor device market for the consumer industry. This definitive report, spanning the 2019–2033 period with a 2025 base and estimated year, delivers actionable intelligence for industry stakeholders. Leveraging the latest data, we dissect market structure, dynamics, key drivers, challenges, and emerging opportunities.

Japan Semiconductor Device Market In Consumer Industry Market Structure & Innovation Trends

The Japan semiconductor device market within the consumer industry exhibits a moderate concentration, characterized by intense competition among both established global giants and specialized domestic players. Innovation is primarily driven by the relentless pursuit of enhanced performance, miniaturization, and energy efficiency in consumer electronics. Regulatory frameworks, while supportive of domestic semiconductor development, also foster international collaboration. Product substitutes are limited in the core semiconductor functionalities, but advancements in alternative technologies continually pressure established players to innovate. End-user demographics are increasingly sophisticated, demanding smarter, more connected, and personalized devices. Mergers and acquisitions (M&A) are strategic, aiming to acquire cutting-edge technologies, expand market reach, and consolidate market share. For instance, the ongoing government investments in Rapidus Corp for 2nm logic chip mass production highlight a significant strategic push.

- Market Concentration: Moderate, with key global players holding substantial shares, alongside strong domestic capabilities.

- Innovation Drivers: Miniaturization, power efficiency, enhanced processing capabilities, AI integration, and IoT connectivity.

- Regulatory Frameworks: Government support for domestic manufacturing, R&D incentives, and trade policies influence market dynamics.

- Product Substitutes: While direct substitutes for core semiconductor functions are few, advancements in alternative component architectures and system-level integration pose evolving challenges.

- End-User Demographics: Growing demand for premium features, seamless connectivity, and sustainable electronic products.

- M&A Activities: Strategic acquisitions and partnerships focused on technology acquisition, capacity expansion, and market access. Estimated M&A deal values are expected to be in the tens to hundreds of millions of USD for smaller tech acquisitions, and potentially in the billions for significant capacity expansions or company acquisitions.

Japan Semiconductor Device Market In Consumer Industry Market Dynamics & Trends

The Japan semiconductor device market for the consumer industry is poised for robust growth, propelled by several interconnected factors. A primary growth driver is the insatiable consumer demand for advanced electronics, including smartphones, wearables, smart home devices, and next-generation gaming consoles. These products continuously integrate more sophisticated semiconductor components, driving up volume and value. Technological disruptions, such as the pervasive adoption of Artificial Intelligence (AI) and the Internet of Things (IoT), necessitate specialized processors, memory chips, and sensors, creating significant market opportunities. The increasing focus on energy efficiency in consumer devices, driven by both environmental concerns and battery life demands, spurs innovation in low-power semiconductor designs. Furthermore, the competitive dynamics are intensifying, with Japanese companies leveraging their strengths in high-performance and specialized semiconductor technologies to compete globally. The continuous evolution of consumer preferences towards personalized experiences, immersive entertainment, and seamless connectivity fuels the demand for semiconductors capable of supporting these features. The projected Compound Annual Growth Rate (CAGR) for this segment is estimated to be between 6% and 8% over the forecast period. Market penetration for advanced semiconductors in emerging consumer electronics categories is expected to reach over 90% in the coming years, reflecting the indispensable role of these components. The industry is also seeing a trend towards customized semiconductor solutions tailored to specific consumer product requirements, fostering closer collaboration between semiconductor manufacturers and device makers.

Dominant Regions & Segments in Japan Semiconductor Device Market In Consumer Industry

The Japanese market for semiconductor devices in the consumer industry is dominated by integrated circuits (ICs), specifically Logic and Micro processors (MPUs and MCUs), due to their pervasive use in almost every consumer electronic device. This dominance is underpinned by Japan's strong presence in the consumer electronics manufacturing sector, a continuous drive for innovation in processing power, and the increasing complexity of consumer products requiring advanced embedded intelligence. The Memory segment also holds significant sway, driven by the exponential growth in data storage needs for multimedia content, gaming, and AI applications.

Leading Segment: Integrated Circuits (ICs) – Logic and Microprocessors (MPU, MCU)

- Key Drivers:

- Advanced Consumer Electronics: Proliferation of smartphones, tablets, smart TVs, gaming consoles, and IoT devices.

- AI and Machine Learning Integration: Demand for powerful processors to enable on-device AI capabilities in consumer products.

- Increased Data Processing: Growing volumes of data generated and consumed by consumers necessitate high-performance computing.

- Government Support for Domestic Semiconductor Industry: Initiatives to bolster domestic R&D and manufacturing capabilities in advanced logic and micro-processing.

- Dominance Analysis: Japan's prowess in consumer electronics manufacturing, coupled with significant investments in advanced logic and micro-processing capabilities by companies like Toshiba and Renesas, solidifies the dominance of this segment. The demand for microcontrollers in increasingly sophisticated appliances, automotive infotainment systems integrated into consumer vehicles, and advanced sensor fusion in wearables further amplifies this segment's importance. Market share for Logic and Micro ICs within the consumer segment is estimated to be upwards of 60%.

- Key Drivers:

Significant Segments:

- Memory: Essential for data storage and retrieval in all consumer electronics. Driven by high-definition content, cloud integration, and AI model storage.

- Optoelectronics: Crucial for displays (LEDs, OLEDs), sensors (image sensors), and lighting. Japan's leadership in imaging technology and display manufacturing contributes to this segment's strength.

- Discrete Semiconductors: While less prominent than ICs in high-end devices, they remain vital for power management and signal conditioning in a wide array of consumer products.

Japan Semiconductor Device Market In Consumer Industry Product Innovations

Product innovation in the Japan semiconductor device market for the consumer industry centers on enhancing performance, reducing power consumption, and enabling new functionalities. This includes the development of highly integrated System-on-Chips (SoCs) for mobile devices, advanced image sensors with superior low-light performance, and energy-efficient microcontrollers for IoT applications. Competitive advantages are derived from miniaturization, improved thermal management, and specialized architectures tailored for AI acceleration and enhanced connectivity, directly addressing the consumer demand for smarter, faster, and more power-efficient electronics.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Japan semiconductor device market within the consumer industry, segmenting it by device type. The core segments investigated include Discrete Semiconductors, Optoelectronics, Sensors, and Integrated Circuits (ICs), with ICs further broken down into Analog, Logic, Memory, and Microprocessors (MPU, MCU, Digital Signal Processors). Each segment's growth projections, current market sizes, and competitive dynamics are meticulously examined. The forecast period from 2025–2033 will reveal significant market share shifts and compound annual growth rates for each category, driven by evolving consumer demands and technological advancements.

- Discrete Semiconductors: Stable growth driven by power management and rectification needs in diverse consumer products.

- Optoelectronics: Robust growth expected, fueled by advancements in display technologies, imaging sensors for cameras, and solid-state lighting.

- Sensors: High growth projected, driven by the proliferation of IoT devices, wearables, and the need for environmental and biometric data capture.

- Integrated Circuits (ICs):

- Analog: Consistent demand driven by signal processing and power management in all consumer electronics.

- Logic: Dominant segment, experiencing high growth due to the increasing complexity of consumer devices and AI integration.

- Memory: Significant growth, propelled by the insatiable demand for data storage in multimedia, gaming, and AI applications.

- Micro (MPU, MCU, DSP): Experiencing substantial growth, critical for embedded intelligence, control functions, and specialized processing in advanced consumer products.

Key Drivers of Japan Semiconductor Device Market In Consumer Industry Growth

The Japan semiconductor device market for the consumer industry is propelled by a confluence of powerful forces. The relentless innovation in consumer electronics, from smartphones to smart home devices, directly translates into increased demand for sophisticated semiconductors. The pervasive adoption of Artificial Intelligence (AI) and the Internet of Things (IoT) necessitates specialized processing power and connectivity solutions. Furthermore, government initiatives and subsidies aimed at strengthening Japan's domestic semiconductor manufacturing capabilities and research and development are a significant catalyst. Growing consumer preference for energy-efficient and feature-rich devices also drives the adoption of advanced semiconductor technologies.

- Technological Advancements: Integration of AI, IoT, 5G, and advanced display technologies.

- Economic Factors: Increasing disposable incomes and consumer spending on premium electronics.

- Regulatory Support: Government investments and policies fostering domestic semiconductor production and innovation.

- Consumer Demand: Growing appetite for smarter, more connected, and personalized consumer experiences.

Challenges in the Japan Semiconductor Device Market In Consumer Industry Sector

Despite strong growth prospects, the Japan semiconductor device market in the consumer industry faces notable challenges. Intense global competition, particularly from South Korea and Taiwan, exerts significant pricing pressure. Supply chain disruptions, as evidenced by recent global shortages, pose a constant threat to production continuity and lead times. The high cost of advanced semiconductor manufacturing, including the development of cutting-edge fabrication facilities, requires substantial capital investment. Furthermore, the rapid pace of technological evolution necessitates continuous and significant R&D expenditure to remain competitive, posing a risk of obsolescence for older technologies. Navigating complex international trade policies and intellectual property rights also adds to the operational complexities.

- Global Competition: Intense rivalry from international semiconductor manufacturers.

- Supply Chain Volatility: Vulnerability to disruptions in raw material sourcing and component availability.

- High Capital Investment: Significant costs associated with advanced fabrication and R&D.

- Rapid Technological Obsolescence: Need for continuous innovation to stay ahead.

- Regulatory Hurdles: Navigating trade regulations and intellectual property challenges.

Emerging Opportunities in Japan Semiconductor Device Market In Consumer Industry

Emerging opportunities in the Japan semiconductor device market for the consumer industry are centered around key technological megatrends and evolving consumer lifestyles. The continued expansion of the Internet of Things (IoT) in both homes and wearables presents a vast market for low-power, highly integrated sensors and microcontrollers. The increasing demand for immersive entertainment, including virtual and augmented reality (VR/AR) applications, will drive the need for high-performance graphics processors and advanced display driver ICs. Furthermore, the growing emphasis on sustainable consumption is creating opportunities for energy-efficient semiconductor solutions and eco-friendly manufacturing processes. The burgeoning market for advanced driver-assistance systems (ADAS) in consumer vehicles also represents a significant growth avenue for specialized automotive-grade semiconductors.

- IoT Expansion: Demand for sensors, microcontrollers, and connectivity chips.

- AR/VR and Metaverse: Growth in high-performance processors and display technologies.

- Sustainable Electronics: Focus on energy efficiency and eco-friendly materials.

- Automotive Integration: Increasing demand for ADAS and in-car entertainment semiconductors.

- Edge AI: Development of semiconductors for on-device AI processing in consumer products.

Leading Players in the Japan Semiconductor Device Market In Consumer Industry Market

- Infineon Technologies AG

- NXP Semiconductors NV

- Toshiba Corporation

- Micron Technology Inc

- Kyocera Corporation

- Xilinx Inc

- Samsung Electronics Co Ltd

- Texas Instruments Inc

- Qualcomm Incorporated

- STMicroelectronics NV

- ON Semiconductor Corporation

- Nvidia Corporation

- Intel Corporation

Key Developments in Japan Semiconductor Device Market In Consumer Industry Industry

- April 2024: The Japanese government allocated JPY590 billion (USD 3.9 billion) to bolster Rapidus Corp's efforts in mass-producing 2nm logic chips. This funding supplements previous subsidies provided to Taiwan Semiconductor Manufacturing Co (TSMC) and Micron Technology.

- February 2024: Sony Semiconductor Solutions Corporation ("SSS"), DENSO Corporation ("DENSO"), and Toyota Motor Corporation ("Toyota") revealed plans for additional investments in Japan Advanced Semiconductor Manufacturing, Inc. ("JASM"), a subsidiary primarily owned by TSMC, located in Kumamoto Prefecture, Japan. This investment aims to establish a second fab, slated to commence operations by the end of 2027. Coupled with JASM's first fab, set to be operational in 2024, the collective investment in JASM is poised to surpass USD20 billion, bolstered by substantial backing from the Japanese government.

Future Outlook for Japan Semiconductor Device Market In Consumer Industry Market

The future outlook for the Japan semiconductor device market in the consumer industry is exceptionally bright, driven by sustained demand for innovation and technological integration. The ongoing digital transformation across various consumer touchpoints will continue to fuel the need for advanced semiconductors. Strategic government support for domestic manufacturing, coupled with private sector investments in cutting-edge research and development, will solidify Japan's position in critical semiconductor segments. Emerging technologies like AI, 5G, and the metaverse will create new product categories and necessitate even more powerful and specialized semiconductor solutions. Companies that can effectively navigate the evolving technological landscape, address supply chain complexities, and capitalize on consumer demand for personalized and efficient devices are poised for significant growth. The increasing focus on sustainability also presents an opportunity for the development of eco-friendly semiconductor technologies.

Japan Semiconductor Device Market In Consumer Industry Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessors (MPU)

- 1.4.4.2. Microcontrollers (MCU)

- 1.4.4.3. Digital Signal Processors

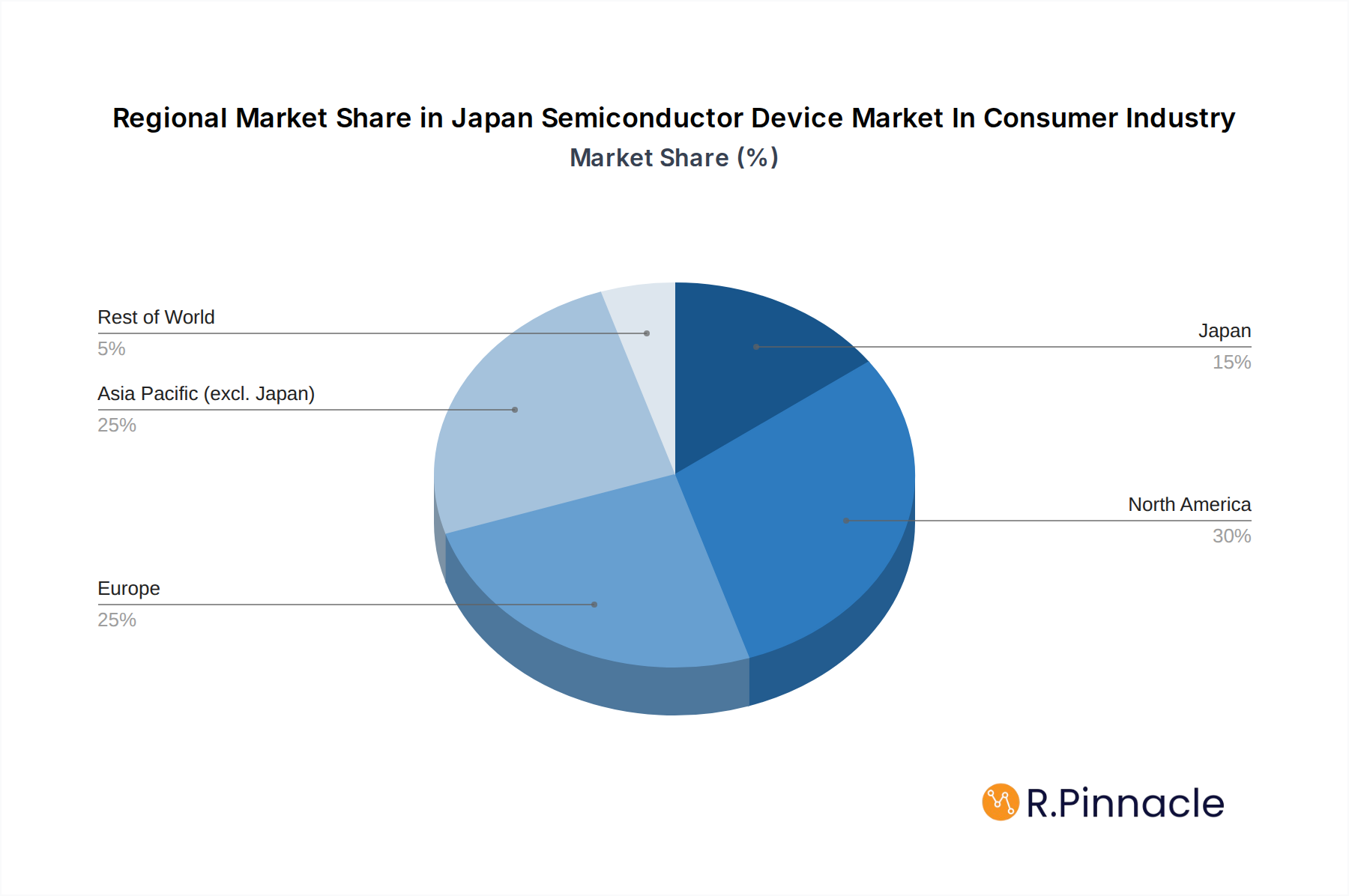

Japan Semiconductor Device Market In Consumer Industry Segmentation By Geography

- 1. Japan

Japan Semiconductor Device Market In Consumer Industry Regional Market Share

Geographic Coverage of Japan Semiconductor Device Market In Consumer Industry

Japan Semiconductor Device Market In Consumer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessors (MPU)

- 5.1.4.4.2. Microcontrollers (MCU)

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Japan Semiconductor Device Market In Consumer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.1.4.1. Analog

- 6.1.4.2. Logic

- 6.1.4.3. Memory

- 6.1.4.4. Micro

- 6.1.4.4.1. Microprocessors (MPU)

- 6.1.4.4.2. Microcontrollers (MCU)

- 6.1.4.4.3. Digital Signal Processors

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 NXP Semiconductors NV

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toshiba Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Micron Technology Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kyocera Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Xilinx Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Samsung Electronics Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Texas Instruments Inc *List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Qualcomm Incorporated

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 STMicroelectronics NV

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 ON Semiconductor Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Nvidia Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Intel Corporation

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Infineon Technologies AG

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Semiconductor Device Market In Consumer Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Semiconductor Device Market In Consumer Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Semiconductor Device Market In Consumer Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 2: Japan Semiconductor Device Market In Consumer Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Japan Semiconductor Device Market In Consumer Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 4: Japan Semiconductor Device Market In Consumer Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Semiconductor Device Market In Consumer Industry?

The projected CAGR is approximately 5.90%.

2. Which companies are prominent players in the Japan Semiconductor Device Market In Consumer Industry?

Key companies in the market include Infineon Technologies AG, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Xilinx Inc, Samsung Electronics Co Ltd, Texas Instruments Inc *List Not Exhaustive, Qualcomm Incorporated, STMicroelectronics NV, ON Semiconductor Corporation, Nvidia Corporation, Intel Corporation.

3. What are the main segments of the Japan Semiconductor Device Market In Consumer Industry?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.22 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for 5G Smartphones; Growing Adoption of Technologies like IoT and AI.

6. What are the notable trends driving market growth?

Increasing Smartphone Penetration.

7. Are there any restraints impacting market growth?

Technological Complexities Arising due to Miniaturization.

8. Can you provide examples of recent developments in the market?

April 2024: The Japanese government allocated JPY590 billion (USD 3.9 billion) to bolster Rapidus Corp's efforts in mass-producing 2nm logic chips. This funding supplements previous subsidies provided to Taiwan Semiconductor Manufacturing Co (TSMC) and Micron Technology.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Semiconductor Device Market In Consumer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Semiconductor Device Market In Consumer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Semiconductor Device Market In Consumer Industry?

To stay informed about further developments, trends, and reports in the Japan Semiconductor Device Market In Consumer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence