Key Insights

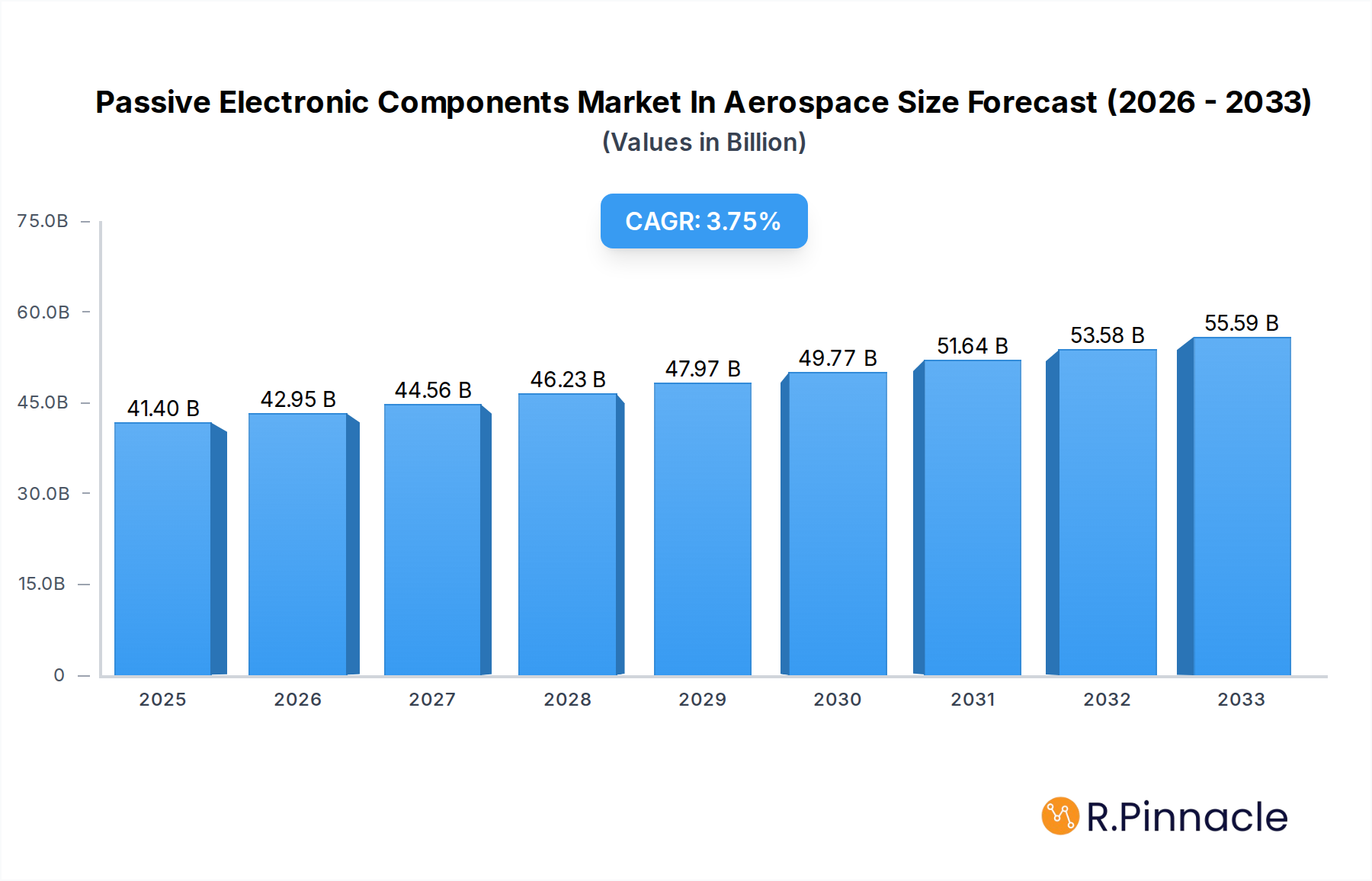

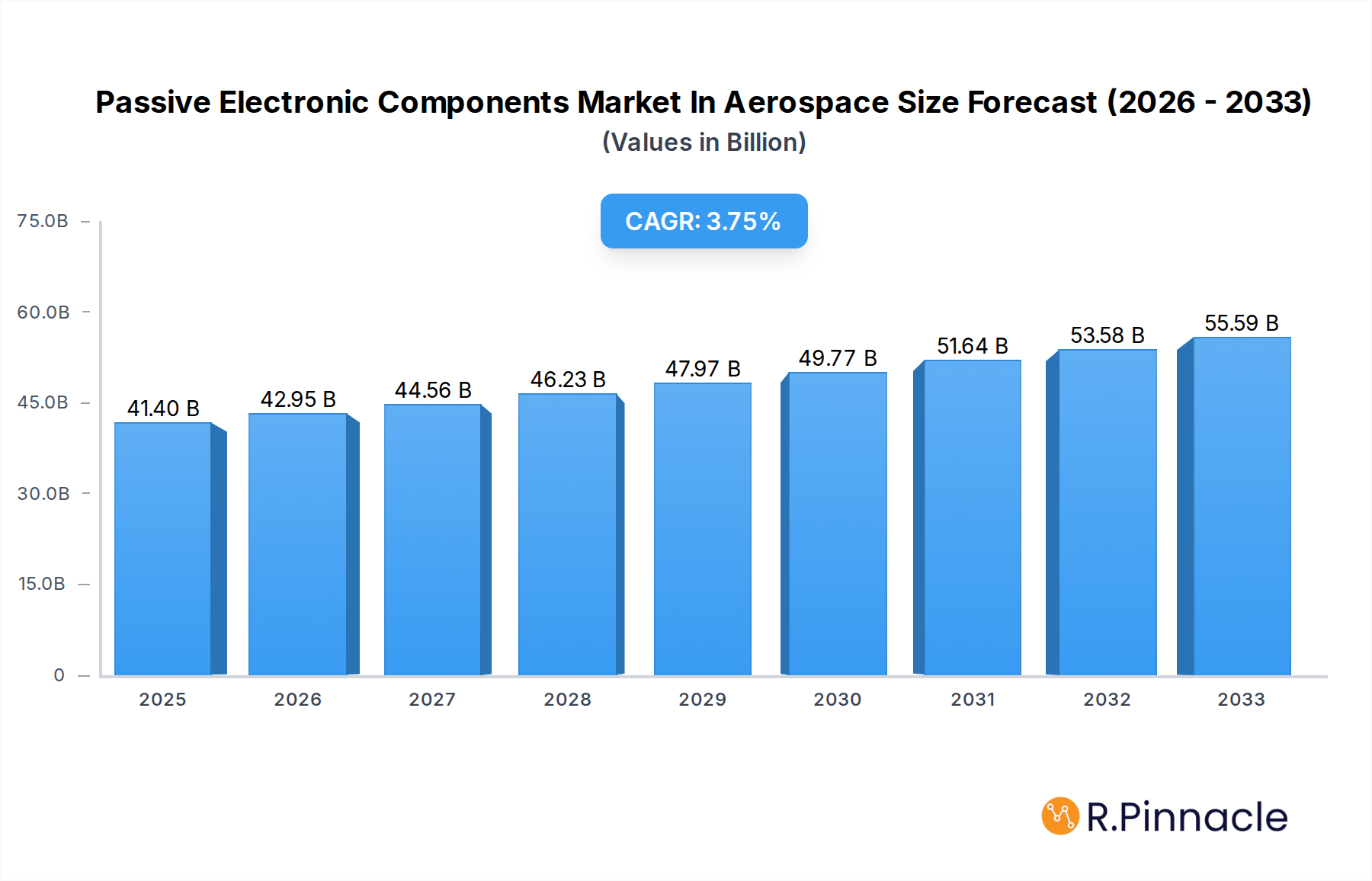

The Aerospace & Defense (A&D) industry's demand for passive electronic components is poised for steady expansion, driven by escalating defense budgets and the increasing integration of advanced technologies in aerospace platforms. The market for passive electronic components within this sector is estimated to reach $41.4 billion in 2025, reflecting a robust Compound Annual Growth Rate (CAGR) of 3.74%. This sustained growth is primarily fueled by the relentless pursuit of enhanced performance, reliability, and miniaturization in critical aerospace and defense systems. Key drivers include the ongoing modernization of military fleets, the development of next-generation fighter jets and surveillance drones, and the expansion of commercial aviation infrastructure demanding sophisticated navigation, communication, and control systems. The increasing adoption of advanced sensor technologies and the growing complexity of electronic warfare capabilities further bolster the demand for high-performance capacitors, inductors, and resistors that can withstand extreme environmental conditions and deliver unwavering accuracy.

Passive Electronic Components Market In Aerospace & Defense Industry Market Size (In Billion)

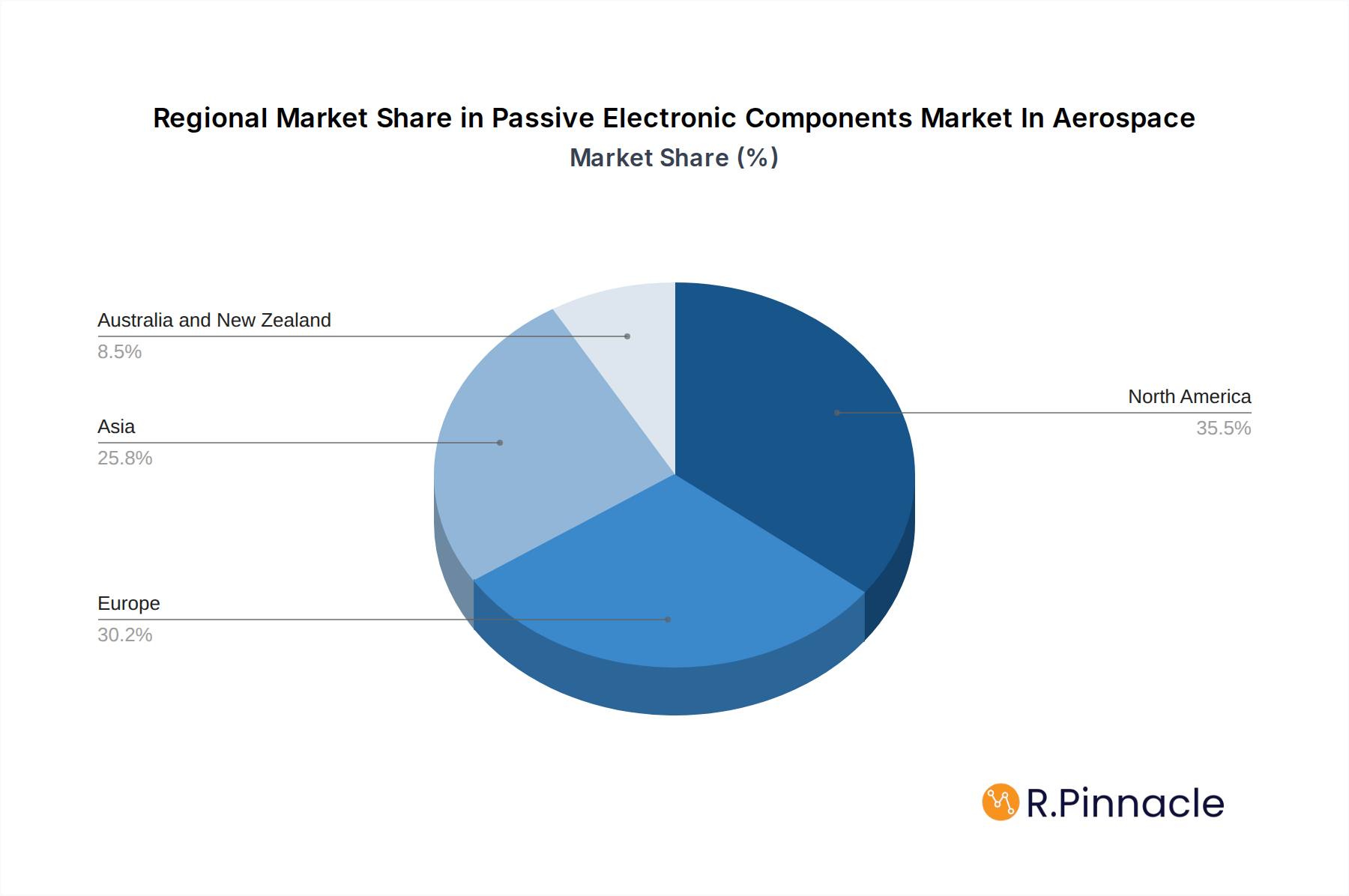

The market landscape is characterized by significant trends such as the shift towards higher reliability and radiation-hardened components, essential for space-based applications and strategic defense systems. Innovations in materials science and manufacturing processes are enabling the development of smaller, lighter, and more power-efficient passive components, crucial for weight-sensitive aerospace applications. While the market benefits from strong growth drivers, certain restraints, such as stringent regulatory compliance and the high cost of specialized, defense-grade components, need to be navigated. The competitive environment is marked by the presence of established global players like Vishay Intertechnology Inc., AVX Corporation (Kyocera Corporation), KEMET Corporation (Yageo Company), and TE Connectivity, who are investing in R&D to offer cutting-edge solutions. The market is segmented into Capacitors, Inductors, and Resistors, with each segment experiencing unique growth trajectories influenced by evolving technological demands. Regional insights indicate a significant presence and growth potential across North America, Europe, and Asia, driven by government investments in defense modernization and the expansion of their respective aerospace sectors.

Passive Electronic Components Market In Aerospace & Defense Industry Company Market Share

Unlock the Future of Aerospace & Defense Electronics: Comprehensive Passive Component Market Report (2019-2033)

Gain critical insights into the burgeoning passive electronic components market within the high-stakes Aerospace & Defense industry. This definitive report, covering 2019-2033 with a base year of 2025, provides in-depth analysis of market structure, dynamics, and future trajectory, essential for strategic planning and competitive advantage. We dissect key segments like Capacitors, Inductors, and Resistors, and highlight crucial industry developments from leading players, offering actionable intelligence for manufacturers, suppliers, and defense contractors.

Passive Electronic Components Market In Aerospace & Defense Industry Market Structure & Innovation Trends

The passive electronic components market in the aerospace and defense sector is characterized by a moderately concentrated structure, with a significant presence of established global players alongside specialized niche manufacturers. Innovation is a critical driver, fueled by the relentless demand for miniaturization, enhanced reliability, higher operating frequencies, and extreme environmental resilience in modern aircraft, spacecraft, and defense systems. Regulatory frameworks, particularly stringent quality and safety standards (e.g., MIL-SPEC, DO-160), profoundly shape product development and market entry. While direct product substitutes are limited due to the specialized nature of aerospace and defense applications, advancements in active components or integrated solutions can indirectly influence demand for certain passive components. End-user demographics are primarily defense organizations, major aerospace manufacturers, and their extensive supply chains, all prioritizing performance and longevity over cost alone. Mergers and acquisitions (M&A) activities are strategic, often aimed at consolidating market share, acquiring proprietary technologies, or expanding geographical reach. For instance, the acquisition of KEMET Corporation by Yageo Company in 2020 exemplifies this trend, strengthening the combined entity's position in high-performance capacitor markets. The overall market share distribution reflects the dominance of companies with proven track records in producing high-reliability components for demanding environments.

Passive Electronic Components Market In Aerospace & Defense Industry Market Dynamics & Trends

The passive electronic components market within the aerospace and defense industry is poised for robust growth, driven by a confluence of technological advancements, increasing defense expenditure globally, and the evolving landscape of aerospace applications. The continuous evolution of aerospace and defense platforms, from next-generation fighter jets and advanced surveillance drones to space exploration missions and satellite constellations, necessitates the integration of highly sophisticated electronic systems. These systems are critically dependent on passive components like capacitors, inductors, and resistors that can withstand extreme operating conditions, including wide temperature fluctuations, high radiation levels, and severe vibration. Technological disruptions, such as the increasing adoption of GaN and SiC technologies for power electronics, are creating new demands for specialized passive components capable of handling higher frequencies and power densities. Furthermore, the miniaturization trend across all electronic devices is compelling manufacturers to develop smaller, lighter, and more efficient passive components without compromising performance or reliability, a key preference for aerospace applications where weight and space are at a premium. The competitive dynamics are intense, with companies vying for market leadership through continuous product innovation, strategic partnerships, and adherence to stringent qualification processes. Market penetration is steadily increasing as defense budgets rise and new aerospace projects gain momentum, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period. The ongoing digital transformation within defense, including the rise of AI-enabled systems, advanced communication networks, and electronic warfare capabilities, further amplifies the demand for high-performance passive components.

Dominant Regions & Segments in Passive Electronic Components Market In Aerospace & Defense Industry

The North American region currently holds a dominant position in the passive electronic components market for the aerospace and defense industry, largely driven by the substantial defense budgets of the United States, coupled with its pioneering role in space exploration and a highly developed aerospace manufacturing ecosystem. Key economic policies supporting defense modernization, significant investments in research and development, and the presence of major aerospace primes and their extensive supply chains contribute to this regional dominance. Within this dominant region, the Capacitors segment is a significant revenue generator.

North America:

- Key Drivers: High defense spending, robust aerospace R&D, presence of leading aerospace and defense manufacturers (e.g., Boeing, Lockheed Martin, Raytheon), stringent quality standards, and continuous demand for advanced electronic systems in military aircraft, satellites, and space missions.

- Dominance Analysis: The region's established infrastructure, skilled workforce, and advanced technological capabilities allow for the development and production of high-reliability capacitors, inductors, and resistors that meet the rigorous specifications of aerospace and defense applications. Government initiatives and long-term defense contracts further solidify its leadership.

Capacitors Segment:

- Key Drivers: Essential for energy storage, filtering, decoupling, and timing functions in virtually all electronic circuits within aircraft and defense systems. The increasing complexity of electronic warfare systems, communication devices, and power management units demands a wide array of capacitor types, including ceramic, tantalum, electrolytic, and film capacitors, often requiring specialized materials and construction for high-temperature and high-reliability applications. The advancement in supercapacitors for energy storage in hybrid-electric aircraft also represents a growing sub-segment.

Inductors Segment:

- Key Drivers: Crucial for power conversion, filtering, and impedance matching in power supplies, communication systems, and electronic warfare modules. The need for miniaturized, high-performance inductors with excellent temperature stability and low outgassing properties is paramount for space and aerospace applications. The development of space-grade SMD inductors, as exemplified by API Delevan's recent releases, underscores the segment's focus on meeting harsh environment engineering challenges.

Resistors Segment:

- Key Drivers: Vital for current limiting, voltage division, and precision measurement in control systems, sensors, and power circuits. High-reliability resistors, including surface mount and through-hole types, are required to operate consistently under extreme conditions. The demand for precision resistors in sophisticated avionics and guidance systems is a key growth factor.

Passive Electronic Components Market In Aerospace & Defense Industry Product Innovations

Product innovation in passive electronic components for aerospace and defense is primarily driven by the need for enhanced performance in extreme environments. This includes the development of components with superior temperature resistance, radiation hardness, and miniaturization without compromising reliability. For instance, advancements in ceramic capacitor technology offer higher volumetric efficiency and broader operating temperature ranges, crucial for space-constrained applications. Similarly, specialized inductors are being engineered to provide tighter tolerances and higher Q factors at elevated frequencies, supporting the evolution of advanced communication and radar systems. The increasing adoption of high-density interconnect (HDI) technologies in defense electronics also necessitates the development of smaller, more integrated passive components.

Report Scope & Segmentation Analysis

This comprehensive report segments the passive electronic components market in the aerospace and defense industry by product type: Capacitors, Inductors, and Resistors.

Capacitors: This segment is projected to exhibit significant growth due to their ubiquitous use in filtering, energy storage, and decoupling across all aerospace and defense platforms. The demand for high-reliability, high-temperature, and radiation-hardened capacitors for critical applications in avionics, defense electronics, and space missions will continue to drive market expansion.

Inductors: The inductor segment is expected to witness steady growth, fueled by advancements in power electronics and communication systems. The increasing need for compact, high-performance inductors in radar, electronic warfare, and satellite communication systems, especially those designed for harsh environmental conditions, will be a key growth driver.

Resistors: This segment, while fundamental, will see consistent demand driven by the need for precision and reliability in control systems, sensors, and power management. The evolution of advanced avionics and signal processing applications will continue to necessitate high-quality, stable resistor solutions.

Key Drivers of Passive Electronic Components Market In Aerospace & Defense Industry Growth

The growth of the passive electronic components market in the aerospace and defense industry is propelled by several key factors. Escalating global defense budgets and ongoing modernization programs for military fleets worldwide are paramount drivers. The increasing complexity and sophistication of modern aircraft, spacecraft, and unmanned aerial vehicles (UAVs) demand a higher density of advanced electronic components. Technological advancements, including the push for miniaturization, higher operating frequencies, and enhanced reliability in extreme environments, are creating sustained demand for cutting-edge passive components. Furthermore, the burgeoning space sector, with its ambitious missions and the proliferation of satellite constellations, represents a significant growth opportunity.

Challenges in the Passive Electronic Components Market In Aerospace & Defense Industry Sector

Despite robust growth prospects, the passive electronic components market in the aerospace and defense sector faces several significant challenges. Stringent regulatory compliance and rigorous qualification processes, essential for ensuring safety and reliability in these critical applications, can lead to extended development cycles and increased costs. Supply chain disruptions, particularly for specialized raw materials and components, pose a constant threat, exacerbated by geopolitical uncertainties. The high cost of development and manufacturing for aerospace-grade components, coupled with the relatively lower volume compared to consumer electronics, can impact profitability. Furthermore, the intense competition from global manufacturers and the need for continuous innovation to keep pace with rapidly evolving technological demands present ongoing hurdles.

Emerging Opportunities in Passive Electronic Components Market In Aerospace & Defense Industry

The passive electronic components market in the aerospace and defense industry is brimming with emerging opportunities. The growing trend towards electric and hybrid-electric propulsion in aviation presents a significant avenue for supercapacitors and advanced power electronic components. The expansion of satellite-based services, including high-speed internet and advanced Earth observation, is driving demand for specialized passive components for satellite payloads and ground stations. The increasing adoption of AI and IoT in defense applications necessitates highly reliable and compact electronic systems, boosting the need for advanced passive components. Furthermore, the push for greater localization of defense manufacturing in various countries creates opportunities for component suppliers to establish local partnerships and supply chains.

Leading Players in the Passive Electronic Components Market In Aerospace & Defense Industry Market

- Vishay Intertechnology Inc.

- AVX Corporation (Kyocera Corporation)

- KEMET Corporation (Yageo Company)

- WIMA GmbH & Co KG

- TT Electronics PLC

- TE Connectivity

- Cornell Dubilier Electronics Inc.

- API Delevan (Fortive Corporation)

- Taiyo Yuden Co Ltd

- Bourns Inc.

- TDK Corporation

- Ohmite Manufacturing Company

- Panasonic Corporation

- Honeywell International Inc

- Eaton Corporation

Key Developments in Passive Electronic Components Market In Aerospace & Defense Industry Industry

- April 2023: Cornell Dubilier Electronics Inc. announced a new line of standard supercapacitor modules, the DSM series. This addresses the need for higher voltage supercapacitor storage beyond individual device capabilities, with packs offering 18V, 9V, and 30V outputs. This development supports the growing interest in energy storage for electric and hybrid-electric aircraft.

- March 2023: API Delevan announced the release of its S0603 and S0402 space SMD inductors. These small, high-reliability inductors are designed for harsh environments, including space and aerospace applications, offering excellent temperature stability, low outgassing properties, high Q, and ultra-high SRF values, with an operating temperature range of -55 to +125°C. This highlights the focus on specialized components for demanding aerospace missions.

Future Outlook for Passive Electronic Components Market In Aerospace & Defense Industry Market

The future outlook for the passive electronic components market in the aerospace and defense industry remains exceptionally strong, driven by ongoing technological advancements and sustained global investment in defense and space exploration. The increasing demand for advanced avionics, sophisticated communication systems, and next-generation weapon platforms will continue to fuel the need for high-performance, reliable passive components. The integration of AI, IoT, and advanced sensing technologies in defense will further accelerate this trend. Emerging markets and defense modernization programs in various regions present significant expansion opportunities. Companies that can consistently deliver innovative, high-reliability components that meet stringent environmental and performance requirements, while also adapting to miniaturization and power efficiency demands, are poised for substantial growth and market leadership in the coming years. Strategic collaborations and a focus on supply chain resilience will be critical for navigating the evolving landscape.

Passive Electronic Components Market In Aerospace & Defense Industry Segmentation

-

1. Type

- 1.1. Capacitors

- 1.2. Inductors

- 1.3. Resistors

Passive Electronic Components Market In Aerospace & Defense Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

Passive Electronic Components Market In Aerospace & Defense Industry Regional Market Share

Geographic Coverage of Passive Electronic Components Market In Aerospace & Defense Industry

Passive Electronic Components Market In Aerospace & Defense Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Capacitors

- 5.1.2. Inductors

- 5.1.3. Resistors

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia

- 5.2.4. Australia and New Zealand

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Passive Electronic Components Market In Aerospace & Defense Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Capacitors

- 6.1.2. Inductors

- 6.1.3. Resistors

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Passive Electronic Components Market In Aerospace & Defense Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Capacitors

- 7.1.2. Inductors

- 7.1.3. Resistors

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Passive Electronic Components Market In Aerospace & Defense Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Capacitors

- 8.1.2. Inductors

- 8.1.3. Resistors

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Passive Electronic Components Market In Aerospace & Defense Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Capacitors

- 9.1.2. Inductors

- 9.1.3. Resistors

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia and New Zealand Passive Electronic Components Market In Aerospace & Defense Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Capacitors

- 10.1.2. Inductors

- 10.1.3. Resistors

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Vishay Intertechnology Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 AVX Corporation (Kyocera Corporation)

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 KEMET Corporation (Yageo Company)

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 WIMA GmbH & Co KG

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 TT Electronics PLC

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 TE Connectivity

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Cornell Dubilier Electronics Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 API Delevan ( Fortive Corporation)

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Taiyo Yuden Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Bourns Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 TDK Corporation

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Ohmite Manufacturing Company

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Panasonic Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Honeywell International Inc *List Not Exhaustive

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 Eaton Corporation

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.1 Vishay Intertechnology Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Type 2025 & 2033

- Figure 7: Europe Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Asia Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Australia and New Zealand Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Australia and New Zealand Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Australia and New Zealand Passive Electronic Components Market In Aerospace & Defense Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Australia and New Zealand Passive Electronic Components Market In Aerospace & Defense Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Passive Electronic Components Market In Aerospace & Defense Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Passive Electronic Components Market In Aerospace & Defense Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Passive Electronic Components Market In Aerospace & Defense Industry?

Key companies in the market include Vishay Intertechnology Inc, AVX Corporation (Kyocera Corporation), KEMET Corporation (Yageo Company), WIMA GmbH & Co KG, TT Electronics PLC, TE Connectivity, Cornell Dubilier Electronics Inc, API Delevan ( Fortive Corporation), Taiyo Yuden Co Ltd, Bourns Inc, TDK Corporation, Ohmite Manufacturing Company, Panasonic Corporation, Honeywell International Inc *List Not Exhaustive, Eaton Corporation.

3. What are the main segments of the Passive Electronic Components Market In Aerospace & Defense Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 44.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Usage of Advanced Electronic Devices in Aerospace & Defense Industry.

6. What are the notable trends driving market growth?

Increase in Defense Spending is Expected to Propel the Industry's Growth.

7. Are there any restraints impacting market growth?

Increasing Price of Critical Metals Used in Manufacturing of Passive Electronic Components.

8. Can you provide examples of recent developments in the market?

April 2023: Cornell Dubilier Electronics Inc. announced a new line of standard supercapacitor modules. The DSM series addresses the need for supercapacitor storage capability at higher voltages than individual devices can provide. The new modules come in packs of 6, 3, or 10 cells in series for 18V, 9V, and 30V outputs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Passive Electronic Components Market In Aerospace & Defense Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Passive Electronic Components Market In Aerospace & Defense Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Passive Electronic Components Market In Aerospace & Defense Industry?

To stay informed about further developments, trends, and reports in the Passive Electronic Components Market In Aerospace & Defense Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence