Key Insights

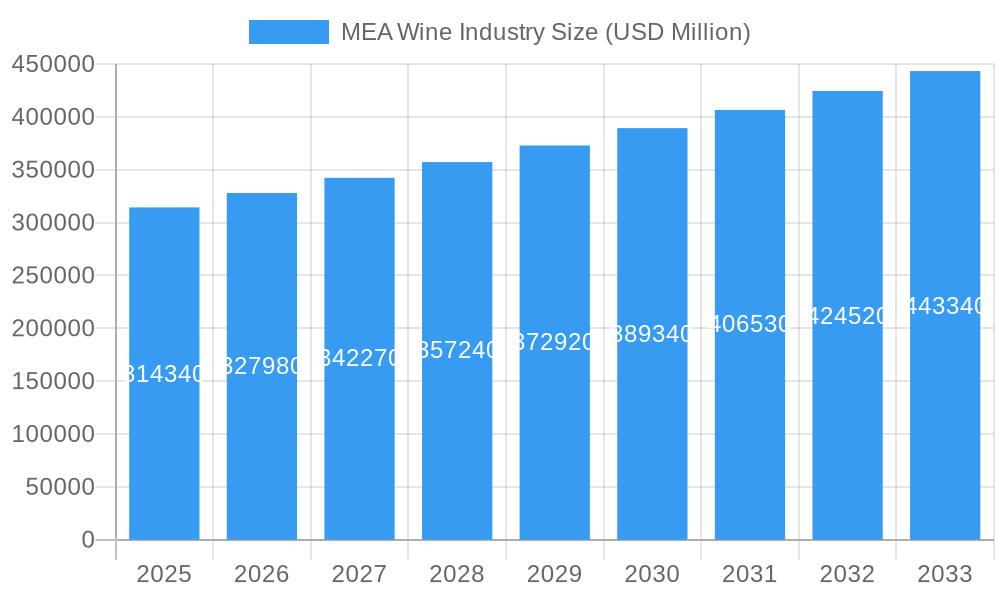

The Middle East & Africa (MEA) wine market is poised for robust growth, projected to reach an estimated $314.34 billion by 2025, driven by a significant Compound Annual Growth Rate (CAGR) of 4.3%. This expansion is fueled by a confluence of factors including rising disposable incomes across key African nations, a burgeoning tourism sector in regions like the GCC, and an increasing acceptance and appreciation for wine culture in traditionally non-wine-consuming areas. The evolving consumer preferences, leaning towards premium and diverse wine varietals, are further stimulating demand. Furthermore, the growth of the on-trade segment, encompassing hotels, restaurants, and bars catering to both domestic and international clientele, plays a crucial role in market penetration. Initiatives by governments and industry bodies to promote viticulture and wine tourism in countries like South Africa and Turkey are also expected to bolster market dynamics, creating new opportunities for both established and emerging players.

MEA Wine Industry Market Size (In Billion)

The MEA wine market is characterized by a dynamic interplay of traditional consumption patterns and emerging trends. While established markets in North Africa and South Africa continue to be significant contributors, countries like the UAE and Saudi Arabia are witnessing a notable uptick in wine consumption, primarily driven by expatriate populations and a growing affluent local consumer base seeking sophisticated beverage options. The distribution landscape is also evolving, with a steady shift towards off-trade channels like supermarkets and hypermarkets, alongside specialized wine stores that offer curated selections and expert advice. The report highlights key market segments such as Still Wine, which dominates the market share, followed by Sparkling Wine, driven by celebratory occasions and a growing desire for premium experiences. Restraints include evolving regulatory landscapes in some countries and the historical cultural perceptions surrounding alcohol consumption, though these are gradually being overcome by economic development and globalization.

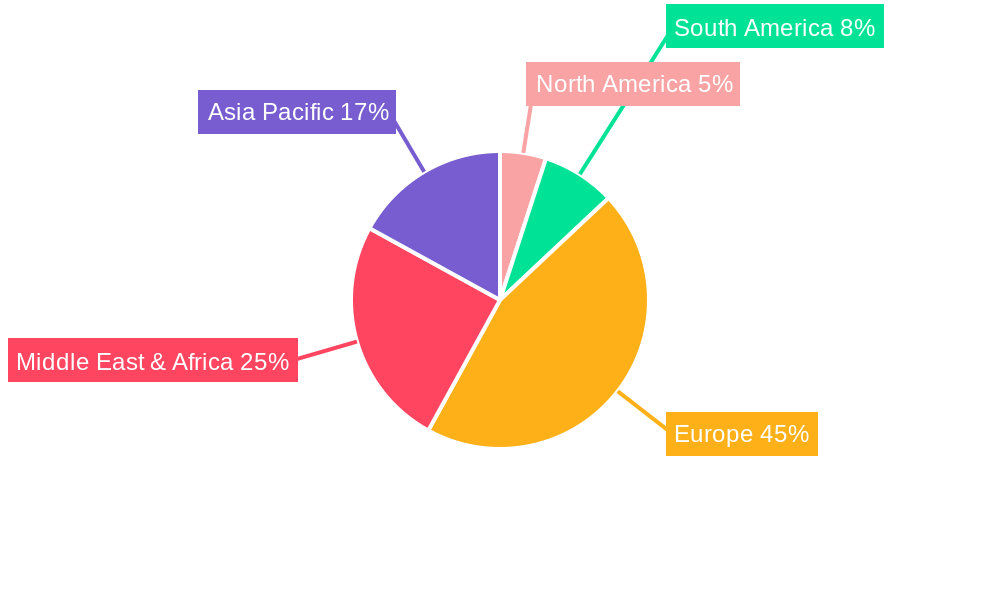

MEA Wine Industry Company Market Share

Here is an SEO-optimized, reader-centric report description for the MEA Wine Industry:

MEA Wine Industry Market Structure & Innovation Trends

This comprehensive report delves into the intricate market structure of the Middle East and Africa (MEA) wine industry, providing deep insights into its current landscape and future trajectory. We meticulously analyze market concentration, identifying key players and their respective market shares, estimated to be in the billions across the region. Innovation drivers are thoroughly examined, revealing how emerging technologies and changing consumer preferences are reshaping product development and marketing strategies. Understanding the prevailing regulatory frameworks is crucial for navigating this dynamic market, and our report offers clarity on compliance and potential trade barriers. We also assess the impact of product substitutes and the evolving end-user demographics, particularly the growing demand from younger, affluent consumers and the increasing interest in premium and specialized wine offerings. Mergers and acquisitions (M&A) activities are a significant indicator of market consolidation and growth potential, with deal values also estimated in the billions. Strategic insights into these M&A trends will empower stakeholders to make informed investment decisions.

- Market Concentration: Detailed analysis of key players and their market share dominance.

- Innovation Drivers: Examination of technological advancements and consumer-led innovations.

- Regulatory Frameworks: Insights into legal and compliance landscapes impacting the industry.

- Product Substitutes: Assessment of alternative beverage options and their market influence.

- End-User Demographics: Analysis of changing consumer profiles and their purchasing behaviors.

- M&A Activities: Overview of recent mergers, acquisitions, and their strategic implications.

MEA Wine Industry Market Dynamics & Trends

The MEA wine industry is poised for significant expansion, driven by a confluence of factors meticulously detailed in this report. We project a robust Compound Annual Growth Rate (CAGR) for the forecast period of 2025–2033, underscoring the burgeoning market penetration across various segments. Economic growth in key MEA nations, coupled with rising disposable incomes, is directly fueling consumer spending on premium and lifestyle beverages, with wine experiencing a notable surge. Technological disruptions are revolutionizing supply chains, enhancing distribution networks, and enabling more targeted marketing campaigns through digital platforms. Furthermore, a discernible shift in consumer preferences towards artisanal, organic, and sustainably produced wines is creating new market niches and driving product diversification. The competitive dynamics within the MEA wine market are intensifying, with both established global giants and agile local producers vying for market share. This section provides a granular look at these forces, offering actionable intelligence for stakeholders to capitalize on emerging trends and mitigate potential challenges. The estimated market size in 2025 is expected to exceed one hundred billion dollars, with significant growth projected in the subsequent years.

Dominant Regions & Segments in MEA Wine Industry

This section meticulously dissects the MEA wine industry to pinpoint the dominant regions and segments, offering a clear roadmap for market entry and strategic focus. South Africa continues to lead as the primary wine-producing and exporting region, benefiting from established viticultural practices and a strong international reputation. Within this region, specific countries like the UAE are emerging as significant consumption hubs, driven by tourism and a growing expatriate population with a taste for international wines.

The market segmentation analysis highlights the overwhelming dominance of Still Wine, which is expected to command a substantial market share throughout the forecast period. This is attributed to its broad appeal and versatility across diverse culinary pairings and occasions. However, Sparkling Wine is witnessing a rapid ascent, particularly in urban centers and among younger demographics celebrating special occasions, with its market penetration accelerating.

In terms of distribution channels, Off-Trade remains the stronghold, with Supermarkets/Hypermarkets playing a pivotal role in accessibility and volume sales, accounting for billions in revenue. The rise of e-commerce and online wine retailers is also significantly boosting the "Other Distribution Channels" within the Off-Trade segment, offering convenience and a wider selection to consumers. The On-Trade channel, encompassing hotels, restaurants, and bars, continues to be crucial for premium brand positioning and experiential marketing, though its recovery post-pandemic is still a key consideration. Economic policies supporting tourism and hospitality, coupled with robust retail infrastructure, are key drivers for the dominance of these segments.

- Dominant Region: South Africa (production and export), UAE (consumption hub).

- Leading Segment (Type): Still Wine (broad appeal), Sparkling Wine (rapid growth).

- Dominant Distribution Channel: Off-Trade (Supermarkets/Hypermarkets, growing Online presence).

- Key Drivers of Dominance: Favorable economic policies, robust retail infrastructure, growing tourism, evolving consumer lifestyles.

MEA Wine Industry Product Innovations

Product innovation within the MEA wine industry is characterized by a strong emphasis on premiumization, sustainability, and unique varietals. Companies are investing in advanced winemaking techniques to enhance flavor profiles and shelf appeal, with a particular focus on local indigenous grape varietals that offer distinct market advantages. The development of organic and biodynamic wines is a significant trend, catering to the increasing consumer demand for healthier and environmentally conscious products. Packaging innovations, including lightweight glass bottles and alternative closures, are also gaining traction, contributing to both cost-effectiveness and reduced environmental impact. These innovations provide competitive advantages by differentiating brands in a crowded marketplace and appealing to discerning consumers seeking quality and ethical sourcing.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the MEA Wine Industry, segmented by product type and distribution channel, covering the historical period of 2019–2024 and projecting growth through 2033, with a base year of 2025. The market size is projected to reach hundreds of billions in the coming years.

Type:

- Still Wine: Expected to maintain its dominant market share, driven by consistent demand across diverse consumer bases. Projected market value in the tens of billions.

- Sparkling Wine: Poised for significant growth, fueled by celebratory occasions and evolving lifestyle trends. Anticipated CAGR of xx%.

- Dessert Wine: Niche but stable segment, catering to specific consumer preferences for post-meal indulgence.

- Fortified Wine: Consistent demand, particularly in regions with established consumption habits.

Distribution Channel:

- On-Trade: Recovery and growth expected in hospitality sectors, essential for premium brand building.

- Off-Trade:

- Supermarkets/Hypermarkets: Continues to be the largest channel by volume, offering accessibility and competitive pricing.

- Specialty Stores: Caters to connoisseurs and niche markets, offering curated selections.

- Other Distribution Channels: Includes a rapidly expanding online retail segment and direct-to-consumer (DTC) sales, exhibiting high growth potential.

Key Drivers of MEA Wine Industry Growth

The MEA wine industry's growth is propelled by several key drivers. Rising disposable incomes and a growing middle class across the region are increasing consumer purchasing power and demand for premium beverages. Evolving lifestyle trends and a desire for experiential consumption are driving interest in wine as a social beverage and a symbol of sophistication. Increased tourism and a growing expatriate population in key markets like the UAE and GCC countries are further boosting wine consumption. Furthermore, favorable government initiatives and investment in the agricultural and hospitality sectors in countries like South Africa are supporting production and market development. The proliferation of e-commerce and digital platforms is also expanding market reach and accessibility for wine producers.

Challenges in the MEA Wine Industry Sector

Despite robust growth prospects, the MEA wine industry faces several challenges. Stringent and varying regulatory frameworks across different countries can create complexities for market entry and distribution, particularly regarding import duties, licensing, and local content requirements. Cultural sensitivities and religious restrictions in some parts of the region can limit the mainstream adoption of alcoholic beverages. Supply chain disruptions and logistical complexities, including inefficient infrastructure and cold chain management, can impact product quality and availability. Intense price competition, particularly from imported bulk wines, poses a challenge for local producers seeking to establish premium brands. Finally, limited consumer education and awareness about different wine types and varietals in certain markets can hinder broader market penetration.

Emerging Opportunities in MEA Wine Industry

The MEA wine industry is brimming with emerging opportunities. The growing demand for premium and ultra-premium wines presents a significant avenue for producers focusing on quality and exclusivity. The expansion of the health and wellness trend is creating opportunities for organic, low-alcohol, and low-sulfite wines. Untapped markets in sub-Saharan Africa with growing economies and younger demographics represent significant future growth potential. E-commerce and direct-to-consumer (DTC) sales channels offer a direct pathway to reach a wider audience and build brand loyalty. Furthermore, partnerships with the burgeoning tourism and hospitality sectors can drive significant on-trade sales and brand visibility.

Leading Players in the MEA Wine Industry Market

- E & J Gallo Winery

- Birthmark of Africa Wines

- Compagnia del Vino

- Suntory Holdings Limited

- Constellation Brands Inc

- Treasury Wine Estates

- Accolade Wines

- The Wine Group

- Davide Campari-Milano N V

- Pernod Ricard

Key Developments in MEA Wine Industry Industry

- December 2021: Nigerian pharmacists launched new wine brands in Nigeria, partnering with leading French wine makers to produce Princi wines like Princi Pinal, Princi Merlot, and Princi Cabernet Sauvignon for the Nigerian market.

- April 2021: South Africa's Birthmark of Africa Wines launched its new collection, including Brut Chardonnay MCC - Méthode Cap Classique; Heritage Premium Red Blend; Heritage Premium White Blend; Premium Chardonnay; Premium Chenin Blanc; Premium Merlot; Premium Pinotage; and Premium Pinotage Rose.

- April 2020: Spinneys Liquor, part of the MMI group, launched its own home delivery service for wine, beer, and spirits in Abu Dhabi.

Future Outlook for MEA Wine Industry Market

The future outlook for the MEA wine industry is exceptionally bright, with projected growth in the hundreds of billions. Accelerated growth will be driven by the sustained rise in disposable incomes, increasing urbanization, and a growing appreciation for wine culture across diverse demographics. The continued expansion of e-commerce and direct-to-consumer channels will democratize access to a wider array of wines, fostering greater consumer engagement. Strategic investments in sustainable viticulture, innovative product development, and targeted marketing campaigns will be crucial for capitalizing on emerging opportunities. Furthermore, the increasing demand for premium and niche wine products, coupled with the potential for further market consolidation through strategic acquisitions, positions the MEA wine industry for sustained and robust expansion in the coming years.

MEA Wine Industry Segmentation

-

1. Type

- 1.1. Still Wine

- 1.2. Sparkling Wine

- 1.3. Dessert Wine

- 1.4. Fortified Wine

-

2. Distribution Channel

- 2.1. On-Trade

-

2.2. Off-Trade

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Specialty Stores

- 2.2.3. Other Distribution Channels

MEA Wine Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

MEA Wine Industry Regional Market Share

Geographic Coverage of MEA Wine Industry

MEA Wine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Still Wine

- 5.1.2. Sparkling Wine

- 5.1.3. Dessert Wine

- 5.1.4. Fortified Wine

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Specialty Stores

- 5.2.2.3. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global MEA Wine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Still Wine

- 6.1.2. Sparkling Wine

- 6.1.3. Dessert Wine

- 6.1.4. Fortified Wine

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-Trade

- 6.2.2. Off-Trade

- 6.2.2.1. Supermarkets/Hypermarkets

- 6.2.2.2. Specialty Stores

- 6.2.2.3. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Still Wine

- 7.1.2. Sparkling Wine

- 7.1.3. Dessert Wine

- 7.1.4. Fortified Wine

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. On-Trade

- 7.2.2. Off-Trade

- 7.2.2.1. Supermarkets/Hypermarkets

- 7.2.2.2. Specialty Stores

- 7.2.2.3. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Still Wine

- 8.1.2. Sparkling Wine

- 8.1.3. Dessert Wine

- 8.1.4. Fortified Wine

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. On-Trade

- 8.2.2. Off-Trade

- 8.2.2.1. Supermarkets/Hypermarkets

- 8.2.2.2. Specialty Stores

- 8.2.2.3. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Still Wine

- 9.1.2. Sparkling Wine

- 9.1.3. Dessert Wine

- 9.1.4. Fortified Wine

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. On-Trade

- 9.2.2. Off-Trade

- 9.2.2.1. Supermarkets/Hypermarkets

- 9.2.2.2. Specialty Stores

- 9.2.2.3. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Still Wine

- 10.1.2. Sparkling Wine

- 10.1.3. Dessert Wine

- 10.1.4. Fortified Wine

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. On-Trade

- 10.2.2. Off-Trade

- 10.2.2.1. Supermarkets/Hypermarkets

- 10.2.2.2. Specialty Stores

- 10.2.2.3. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific MEA Wine Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Still Wine

- 11.1.2. Sparkling Wine

- 11.1.3. Dessert Wine

- 11.1.4. Fortified Wine

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. On-Trade

- 11.2.2. Off-Trade

- 11.2.2.1. Supermarkets/Hypermarkets

- 11.2.2.2. Specialty Stores

- 11.2.2.3. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 E & J Gallo Winery

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Birthmark of Africa Wines

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Compagnia del Vino*List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Suntory Holdings Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Constellation Brands Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Treasury Wine Estates

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Accolade Wines

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 The Wine Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Davide Campari-Milano N V

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pernod Ricard

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 E & J Gallo Winery

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global MEA Wine Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: South America MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Europe MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific MEA Wine Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific MEA Wine Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific MEA Wine Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific MEA Wine Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific MEA Wine Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific MEA Wine Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global MEA Wine Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global MEA Wine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global MEA Wine Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global MEA Wine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific MEA Wine Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Wine Industry?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the MEA Wine Industry?

Key companies in the market include E & J Gallo Winery, Birthmark of Africa Wines, Compagnia del Vino*List Not Exhaustive, Suntory Holdings Limited, Constellation Brands Inc, Treasury Wine Estates, Accolade Wines, The Wine Group, Davide Campari-Milano N V, Pernod Ricard.

3. What are the main segments of the MEA Wine Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 549.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Focus on Maintaining Health and Well-Being; Launching Supplements For Specific Purposes and Targeted Population.

6. What are the notable trends driving market growth?

Changing Lifestyle and Consumption Habits of Wine.

7. Are there any restraints impacting market growth?

Supplement Consumption and Their Side-effects; Inclination Towards Substitute Products.

8. Can you provide examples of recent developments in the market?

In December 2021, Nigerian pharmacists launched new wine brands in Nigeria. He partnered with leading wine makers in France to produce Princi wines like Princi Pinal, Princi Merlot, and Princi Cabernet Sauvignon for the Nigerian market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Wine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Wine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Wine Industry?

To stay informed about further developments, trends, and reports in the MEA Wine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence