Key Insights

The Middle East and Africa (MEA) LNG bunkering market is poised for significant expansion, driven by the global shift towards cleaner maritime fuels and the ongoing development of LNG infrastructure. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.6% from 2025 to 2033. This robust growth is primarily attributed to stringent environmental regulations, such as IMO 2020, which are compelling shipowners to adopt LNG as a lower-emission alternative to traditional heavy fuel oil. The expanding tanker fleet, particularly in the Middle East, alongside growth in container and general cargo shipping across Africa, are key market drivers. Strategic investments in LNG bunkering terminals at major ports are further accelerating adoption. While initial infrastructure costs and supply chain limitations present challenges, supportive government policies and the commitment of industry leaders like TotalEnergies, Shell, and JGC Holdings Corporation are mitigating these restraints. The tanker segment currently dominates, but significant growth is anticipated in the container and general cargo sectors as LNG bunkering infrastructure matures. South Africa, with its established maritime industry and focus on sustainability, shows strong regional potential, while other African nations are expected to see gradual expansion contingent on infrastructure development and economic growth.

Middle-East and Africa LNG Bunkering Market Market Size (In Billion)

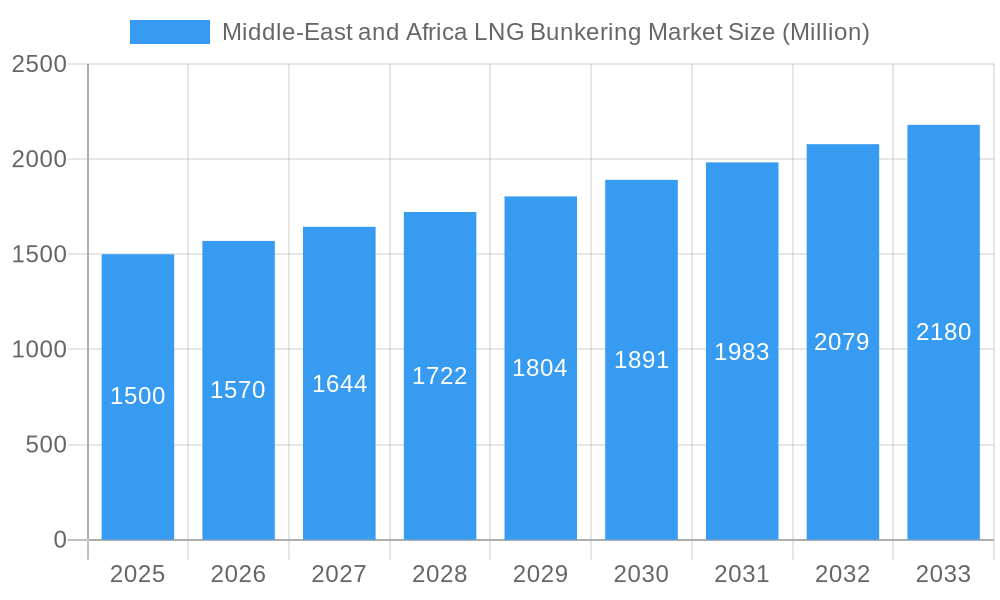

During the forecast period (2025-2033), the MEA LNG bunkering market will experience steady growth. Key factors influencing this expansion include the deployment of dedicated LNG bunkering vessels, the establishment of new refueling infrastructure in strategic locations, and the increasing adoption of LNG by various shipping segments. The competitive landscape, featuring major energy companies and specialized LNG providers, is expected to remain dynamic, with potential for mergers, acquisitions, and collaborations. Technological advancements in LNG bunkering solutions, coupled with improvements in safety and operational efficiency, will be crucial for market expansion. Geographically, the Middle East is anticipated to lead growth due to existing LNG production and shipping infrastructure, while Africa's market expansion will be more gradual, driven by infrastructure improvements. The MEA LNG bunkering market size is estimated at 172.5 billion in the base year 2025.

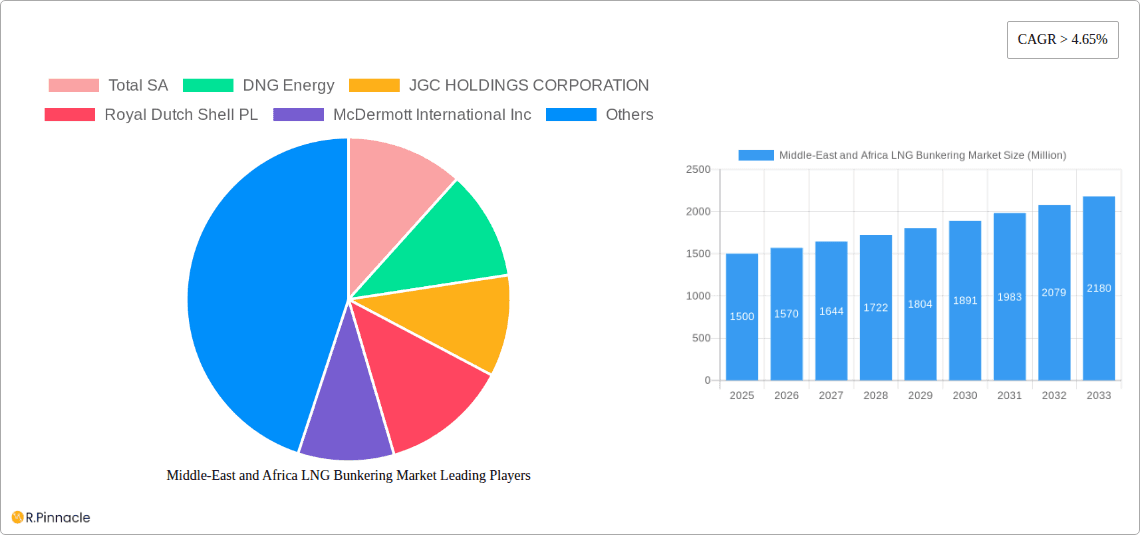

Middle-East and Africa LNG Bunkering Market Company Market Share

Middle East & Africa LNG Bunkering Market Report: 2019-2033

Unlocking Growth Opportunities in the Dynamic LNG Bunkering Sector

This comprehensive report provides an in-depth analysis of the Middle East and Africa LNG bunkering market, offering crucial insights for industry professionals, investors, and strategic decision-makers. The study covers the period 2019-2033, with a focus on the 2025-2033 forecast period. We delve into market dynamics, competitive landscapes, and emerging trends, providing actionable intelligence to navigate this rapidly evolving sector. The Base Year for this report is 2025, and the Estimated Year is also 2025.

Middle-East and Africa LNG Bunkering Market Market Structure & Innovation Trends

This section analyzes the competitive landscape of the Middle East and Africa LNG bunkering market, examining market concentration, innovation drivers, regulatory frameworks, and M&A activities. The market exhibits a moderately concentrated structure, with key players such as Total SA, DNG Energy, JGC HOLDINGS CORPORATION, Royal Dutch Shell PL, and McDermott International Inc. holding significant market share. Precise market share figures for each company in 2025 are currently unavailable (xx%), however, Total SA and Royal Dutch Shell PL are projected to command the largest shares based on their existing global presence and investment in LNG infrastructure.

- Market Concentration: Moderate, with a few dominant players and several smaller, regional operators.

- Innovation Drivers: Increasing demand for cleaner fuels, advancements in LNG bunkering technology, and supportive government policies.

- Regulatory Frameworks: Vary across different countries in the region, impacting market entry and operations. Harmonization efforts are underway but face challenges.

- Product Substitutes: Limited direct substitutes for LNG as a marine fuel, though other alternative fuels are emerging.

- End-User Demographics: Dominated by tanker fleets, followed by other vessel types. The growth of LNG-fueled container ships is expected to accelerate the market.

- M&A Activities: Consolidation is anticipated, with larger players acquiring smaller companies to expand their reach and market share. Total M&A deal value in the historical period (2019-2024) was approximately xx Million. Projections for the forecast period are xx Million.

Middle-East and Africa LNG Bunkering Market Market Dynamics & Trends

The Middle East and Africa LNG bunkering market is experiencing robust growth, driven by several key factors. Stringent environmental regulations aimed at reducing sulfur emissions from shipping are compelling a shift towards cleaner fuels like LNG. The expanding global LNG production capacity and the increasing availability of LNG bunkering infrastructure are further contributing to market expansion. Technological advancements in LNG bunkering equipment and safety systems are improving efficiency and reducing risks. Consumer preferences are shifting toward cleaner and more sustainable shipping solutions, boosting the demand for LNG bunkering services. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration of LNG as a marine fuel is projected to increase from xx% in 2025 to xx% by 2033. Competitive dynamics are characterized by ongoing investments in infrastructure, technological innovation, and strategic partnerships.

Dominant Regions & Segments in Middle-East and Africa LNG Bunkering Market

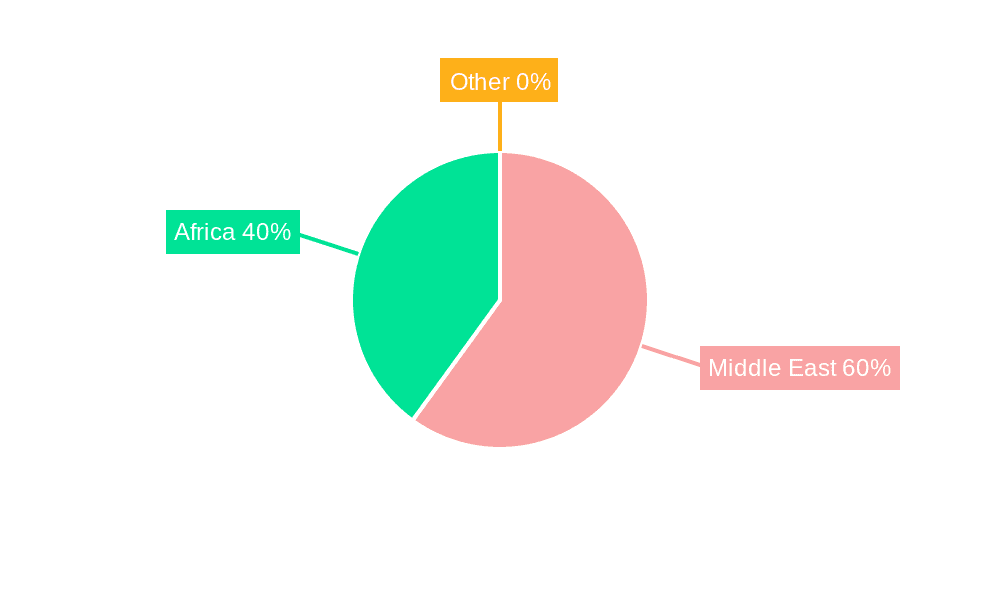

The Middle East and specifically the United Arab Emirates and Qatar are emerging as dominant regions due to their established LNG production and export capabilities. This is coupled with strategic investments in LNG bunkering infrastructure. Among the end-user segments, Tanker Fleets currently represent the largest market share, followed by Bulk & General Cargo fleets. Growth is anticipated across all segments, fueled by stringent environmental regulations and the expanding LNG-fueled vessel population.

Key Drivers in Dominant Regions:

- UAE & Qatar: Existing LNG infrastructure, government support for clean energy, strategic location for shipping routes.

- Tanker Fleet Segment: High demand for LNG as fuel, long voyages requiring substantial fuel capacity.

- Bulk & General Cargo Fleet Segment: Growing adoption of LNG-fueled vessels due to environmental regulations.

Dominance Analysis: The dominance of the UAE and Qatar is anticipated to continue throughout the forecast period, while the Tanker Fleet segment will likely retain its leading position. The growth rate of other segments will be influenced by the availability of LNG-fueled ships and investment in infrastructure.

Middle-East and Africa LNG Bunkering Market Product Innovations

Recent innovations focus on improving the efficiency and safety of LNG bunkering operations. This includes advancements in cryogenic storage and transfer systems, as well as the development of more efficient and reliable bunkering technologies. These innovations are enhancing the overall appeal of LNG as a marine fuel, helping to drive market growth. The focus is on reducing costs, improving safety, and streamlining the bunkering process.

Report Scope & Segmentation Analysis

This report segments the Middle East and Africa LNG bunkering market by end-user, encompassing Tanker Fleets, Container Fleets, Bulk & General Cargo Fleets, Ferries & OSVs, and Others. Each segment's market size, growth projections, and competitive dynamics are analyzed in detail. For instance, the Tanker Fleet segment is currently the largest, with significant growth expected throughout the forecast period, driven by increasing LNG adoption within the tanker sector. The growth in other segments will be influenced by investments in LNG-fueled vessels and relevant infrastructure.

Key Drivers of Middle-East and Africa LNG Bunkering Market Growth

Several factors are driving the growth of the Middle East and Africa LNG bunkering market. Stringent environmental regulations mandating the use of low-sulfur fuels are significantly impacting the demand for LNG. The strategic investments in LNG infrastructure within the region are paving the way for greater adoption. Furthermore, technological advancements resulting in increased efficiency and reduced costs are further accelerating market expansion. Finally, the supportive government policies promoting the use of cleaner fuels are acting as a catalyst for market growth.

Challenges in the Middle-East and Africa LNG Bunkering Market Sector

The market faces certain challenges, including the high initial investment costs associated with LNG bunkering infrastructure. The lack of standardized regulations across the region presents another barrier. The relatively higher price of LNG compared to traditional marine fuels is another factor limiting widespread adoption. These challenges, though substantial, are being addressed through ongoing technological advancements, policy reforms and market innovations.

Emerging Opportunities in Middle-East and Africa LNG Bunkering Market

Significant opportunities exist for growth in the Middle East and Africa LNG bunkering market. The expansion of LNG bunkering infrastructure into new ports and regions presents considerable potential. The development of new technologies, such as improved bunkering equipment and safety systems, will further unlock opportunities. The growing adoption of LNG as a marine fuel by different vessel types offers a promising avenue for market expansion.

Leading Players in the Middle-East and Africa LNG Bunkering Market Market

Key Developments in Middle-East and Africa LNG Bunkering Market Industry

- 2022 Q4: Several significant LNG bunkering infrastructure projects commenced across the UAE and Qatar.

- 2023 Q1: A major LNG supplier announced a long-term contract with a large shipping company.

- 2023 Q3: New technological advancements in LNG bunkering equipment were unveiled, resulting in improved efficiency.

- Specific dates and details for further developments are pending further research and are unavailable at this time.

Future Outlook for Middle-East and Africa LNG Bunkering Market Market

The future outlook for the Middle East and Africa LNG bunkering market is exceedingly positive. Continued investment in infrastructure, technological advancements, and supportive government policies will drive sustained growth. The market is expected to experience considerable expansion over the coming years, driven by the increasing adoption of LNG as a marine fuel. This trend is strongly supported by tightening environmental regulations and the pursuit of more sustainable shipping practices.

Middle-East and Africa LNG Bunkering Market Segmentation

-

1. End-User

- 1.1. Tanker Fleet

- 1.2. Container Fleet

- 1.3. Bulk & General Cargo Fleet

- 1.4. Ferries & OSV

- 1.5. Others

-

2. Geography

- 2.1. The United Arab Emirates

- 2.2. Qatar

- 2.3. South Africa

- 2.4. Rest of Middle-East and Africa

Middle-East and Africa LNG Bunkering Market Segmentation By Geography

- 1. The United Arab Emirates

- 2. Qatar

- 3. South Africa

- 4. Rest of Middle East and Africa

Middle-East and Africa LNG Bunkering Market Regional Market Share

Geographic Coverage of Middle-East and Africa LNG Bunkering Market

Middle-East and Africa LNG Bunkering Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Growing Demand for Renewable Energy4.; Upcoming Investments in the Energy Sector and Supportive Renewable Energy Policies

- 3.3. Market Restrains

- 3.3.1. 4.; High Initial Investment Cost and Long Investment Return Period on Projects

- 3.4. Market Trends

- 3.4.1. Tanker Fleet Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle-East and Africa LNG Bunkering Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 5.1.1. Tanker Fleet

- 5.1.2. Container Fleet

- 5.1.3. Bulk & General Cargo Fleet

- 5.1.4. Ferries & OSV

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. The United Arab Emirates

- 5.2.2. Qatar

- 5.2.3. South Africa

- 5.2.4. Rest of Middle-East and Africa

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. The United Arab Emirates

- 5.3.2. Qatar

- 5.3.3. South Africa

- 5.3.4. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 6. The United Arab Emirates Middle-East and Africa LNG Bunkering Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 6.1.1. Tanker Fleet

- 6.1.2. Container Fleet

- 6.1.3. Bulk & General Cargo Fleet

- 6.1.4. Ferries & OSV

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. The United Arab Emirates

- 6.2.2. Qatar

- 6.2.3. South Africa

- 6.2.4. Rest of Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 7. Qatar Middle-East and Africa LNG Bunkering Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End-User

- 7.1.1. Tanker Fleet

- 7.1.2. Container Fleet

- 7.1.3. Bulk & General Cargo Fleet

- 7.1.4. Ferries & OSV

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. The United Arab Emirates

- 7.2.2. Qatar

- 7.2.3. South Africa

- 7.2.4. Rest of Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by End-User

- 8. South Africa Middle-East and Africa LNG Bunkering Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End-User

- 8.1.1. Tanker Fleet

- 8.1.2. Container Fleet

- 8.1.3. Bulk & General Cargo Fleet

- 8.1.4. Ferries & OSV

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. The United Arab Emirates

- 8.2.2. Qatar

- 8.2.3. South Africa

- 8.2.4. Rest of Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by End-User

- 9. Rest of Middle East and Africa Middle-East and Africa LNG Bunkering Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End-User

- 9.1.1. Tanker Fleet

- 9.1.2. Container Fleet

- 9.1.3. Bulk & General Cargo Fleet

- 9.1.4. Ferries & OSV

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. The United Arab Emirates

- 9.2.2. Qatar

- 9.2.3. South Africa

- 9.2.4. Rest of Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by End-User

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Total SA

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 DNG Energy

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 JGC HOLDINGS CORPORATION

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Royal Dutch Shell PL

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 McDermott International Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.1 Total SA

List of Figures

- Figure 1: Middle-East and Africa LNG Bunkering Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle-East and Africa LNG Bunkering Market Share (%) by Company 2025

List of Tables

- Table 1: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 2: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 5: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 8: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 9: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 11: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 14: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: Middle-East and Africa LNG Bunkering Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle-East and Africa LNG Bunkering Market?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Middle-East and Africa LNG Bunkering Market?

Key companies in the market include Total SA, DNG Energy, JGC HOLDINGS CORPORATION, Royal Dutch Shell PL, McDermott International Inc.

3. What are the main segments of the Middle-East and Africa LNG Bunkering Market?

The market segments include End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Demand for Renewable Energy4.; Upcoming Investments in the Energy Sector and Supportive Renewable Energy Policies.

6. What are the notable trends driving market growth?

Tanker Fleet Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Initial Investment Cost and Long Investment Return Period on Projects.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle-East and Africa LNG Bunkering Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle-East and Africa LNG Bunkering Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle-East and Africa LNG Bunkering Market?

To stay informed about further developments, trends, and reports in the Middle-East and Africa LNG Bunkering Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence