Key Insights

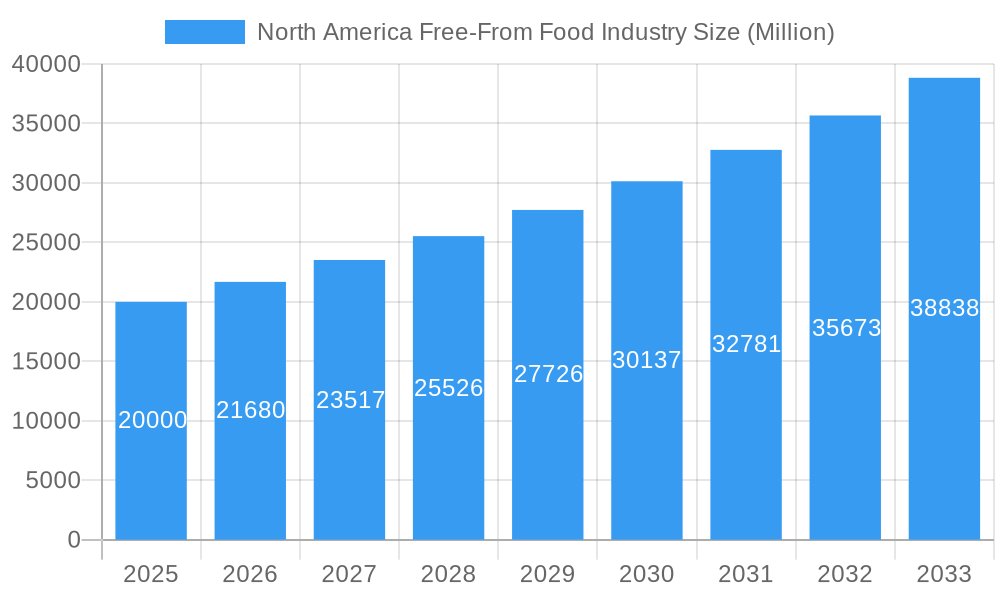

The North American free-from food market, encompassing gluten-free, dairy-free, and allergen-free products across bakery, confectionery, dairy alternatives, snacks, and beverages, exhibits robust growth. Driven by increasing consumer awareness of food allergies and intolerances, coupled with rising demand for healthier and specialized dietary options, the market is experiencing significant expansion. The convenience of online retail channels further fuels this growth, alongside the increasing availability of free-from products in supermarkets and convenience stores. While the exact market size for 2025 isn't explicitly provided, based on a CAGR of 8.40% and considering the market trends, a reasonable estimate would place the North American market value at approximately $20 billion in 2025. This estimate reflects the substantial market penetration of free-from foods and the continued acceleration in consumer adoption. The forecast period (2025-2033) projects continued expansion, with projected growth driven by innovation in product development, addressing both taste and nutritional aspects for diverse consumer needs. Major players like General Mills, Conagra Brands, and Hain Celestial are strategically positioning themselves to capitalize on this expanding market segment through product diversification and acquisitions.

North America Free-From Food Industry Market Size (In Billion)

The market segmentation reveals significant opportunities. The bakery and confectionery segment is a major revenue contributor, fueled by the constant demand for delicious treats with dietary restrictions accommodated. Dairy-free foods, specifically plant-based milks and yogurts, are experiencing rapid growth, demonstrating increasing consumer acceptance of dairy alternatives. However, pricing and potential limitations in taste and texture compared to conventional products remain potential restraints, although technological innovation continually seeks to address these challenges. Regional differences in consumer preferences and purchasing habits may also influence market segmentation and growth rates within North America. Future growth strategies will rely on increased R&D to improve product quality and expand product variety while simultaneously managing the pricing to maintain market accessibility.

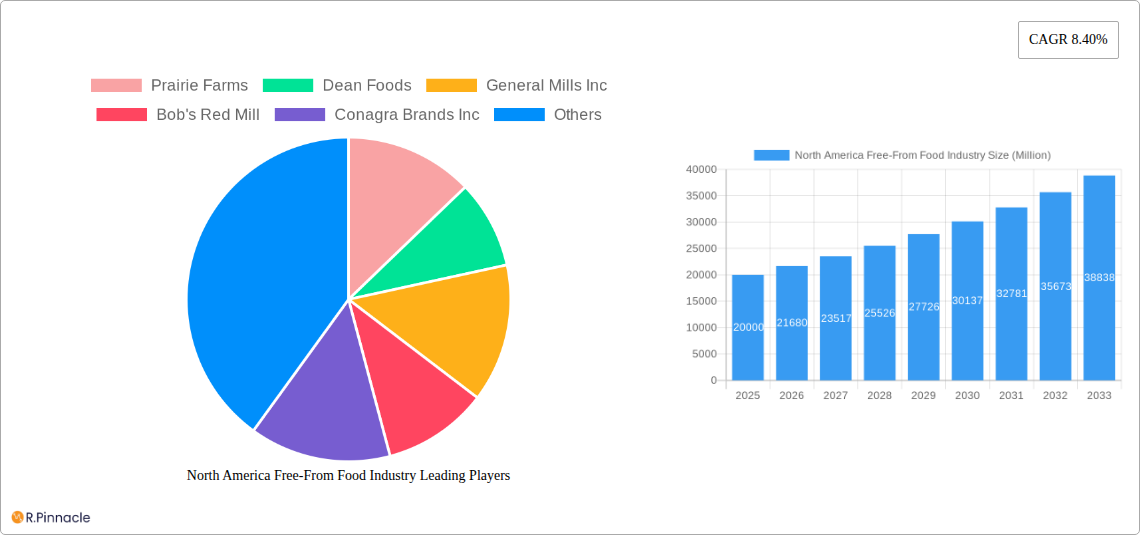

North America Free-From Food Industry Company Market Share

North America Free-From Food Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the North America free-from food industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report unveils the market's structure, dynamics, and future trajectory. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a robust CAGR of xx%.

North America Free-From Food Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory factors shaping the North America free-from food market. Market concentration is moderately high, with key players like General Mills Inc, Conagra Brands Inc, and Hain Celestial Group Inc holding significant market share. However, the presence of numerous smaller, specialized brands indicates a dynamic market with opportunities for both established players and new entrants. The market share of the top 5 players is estimated at xx% in 2025.

- Market Concentration: Moderately high, with top 5 players holding xx% market share in 2025.

- Innovation Drivers: Growing consumer demand for healthier and specialized food options, coupled with advancements in food technology.

- Regulatory Frameworks: Increasingly stringent regulations regarding allergen labeling and ingredient sourcing are shaping industry practices.

- Product Substitutes: The emergence of plant-based alternatives and improved processing technologies are impacting the competitiveness of traditional free-from products.

- End-User Demographics: The primary consumer base comprises individuals with specific dietary restrictions, health-conscious consumers, and those seeking novel culinary experiences. This demographic is expected to expand significantly over the forecast period.

- M&A Activities: The free-from food sector has witnessed considerable M&A activity in recent years, with deal values totaling an estimated xx Million in the period 2019-2024, primarily driven by consolidation efforts and expansion into new product segments.

North America Free-From Food Industry Market Dynamics & Trends

The North America free-from food market is characterized by strong growth driven by several key factors. Rising prevalence of food allergies and intolerances is the primary growth driver. Increasing consumer awareness of health and wellness, coupled with a rising preference for clean-label products and convenient options, further fuels market expansion. Technological advancements in food processing and ingredient sourcing are enabling the creation of innovative and improved free-from products. The market is also witnessing the emergence of new distribution channels, including online retail and direct-to-consumer models. Competitive dynamics are characterized by both intense competition among established players and the continuous entry of new players, particularly in niche segments. The market's CAGR during the forecast period is projected at xx%, and market penetration is expected to increase from xx% in 2025 to xx% by 2033.

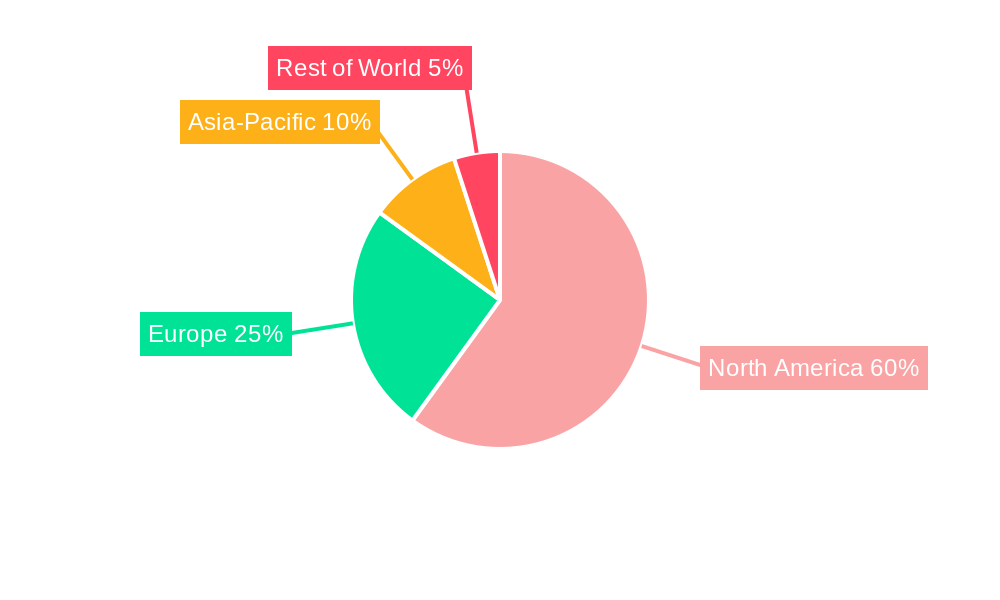

Dominant Regions & Segments in North America Free-From Food Industry

The United States dominates the North America free-from food market, driven by its large population, high disposable income, and advanced healthcare infrastructure. Within the market, Dairy-free foods represent the largest segment by end product, driven by the increasing popularity of plant-based diets. Supermarkets/Hypermarkets account for the largest share of the distribution channel segment, while Gluten-Free products constitute the leading type segment.

- Key Drivers in the US: High consumer awareness, strong regulatory framework supporting free-from food production, and robust distribution networks.

- Dairy-free Foods Dominance: Driven by veganism and lactose intolerance.

- Supermarkets/Hypermarkets Dominance: Due to established distribution networks and wide product accessibility.

- Gluten-Free Dominance: Driven by increased awareness of celiac disease and gluten sensitivity.

Regional Analysis: The US holds the largest market share, followed by Canada.

North America Free-From Food Industry Product Innovations

Recent innovations include the development of gluten-free baked goods with improved texture and taste, dairy-free alternatives mimicking the taste and texture of traditional dairy products, and allergen-free snacks with enhanced nutritional value. Technological advancements such as 3D printing and precision fermentation are enabling the creation of novel free-from products with customized characteristics. These innovations cater to the growing demand for healthier, more appealing, and convenient free-from foods.

Report Scope & Segmentation Analysis

This report segments the North America free-from food market by end product (Bakery and Confectionery, Dairy-free Foods, Snacks, Beverages, Other End Products), distribution channel (Supermarkets/Hypermarkets, Online Retail Stores, Convenience Stores, Other Distribution Channels), and type (Gluten Free, Dairy Free, Allergen Free, Other Types). Each segment's growth projection, market size, and competitive dynamics are thoroughly analyzed, providing a comprehensive overview of the market's structure and future potential. For example, the Dairy-free Foods segment is expected to experience significant growth due to increasing consumer demand for plant-based products and alternatives to traditional dairy products, while the Online Retail Stores segment is expected to show notable growth fuelled by an increased preference for online grocery shopping.

Key Drivers of North America Free-From Food Industry Growth

Key growth drivers include the rising prevalence of food allergies and intolerances, increasing consumer awareness of health and wellness, technological advancements in food processing, and supportive government regulations. The expanding consumer base for health-conscious and specialized foods further fuels market expansion. The growing preference for clean-label products and the rise of veganism and vegetarianism also significantly contribute to market growth.

Challenges in the North America Free-From Food Industry Sector

Challenges include maintaining product quality and consistency, managing supply chain complexities, navigating stringent regulatory requirements, and facing intense competition. Cost fluctuations in raw materials and the need for specialized production facilities pose further obstacles. The high cost of free-from products compared to conventional food options also affects market penetration.

Emerging Opportunities in North America Free-From Food Industry

Emerging opportunities include expanding into new product categories, like free-from pet food, developing personalized free-from products, and tapping into emerging markets. Exploring new technologies, such as precision fermentation and plant-based protein alternatives, promises significant growth potential. Leveraging data-driven insights to customize product offerings and cater to evolving consumer preferences is crucial.

Leading Players in the North America Free-From Food Industry Market

Key Developments in North America Free-From Food Industry Industry

- Q1 2023: General Mills launches a new line of gluten-free snacks.

- Q3 2022: Conagra Brands acquires a smaller free-from food producer.

- Q4 2021: New regulations on allergen labeling come into effect in the US.

- Q2 2020: Increased demand for free-from products due to pandemic-related disruptions.

Future Outlook for North America Free-From Food Industry Market

The future of the North America free-from food market is bright, with continued growth driven by robust consumer demand, innovative product development, and supportive regulatory frameworks. Opportunities abound in expanding product lines, improving product quality, and increasing market penetration. Strategic collaborations and technological advancements will further shape market dynamics and create new opportunities for growth and innovation. The market is poised for significant expansion over the forecast period.

North America Free-From Food Industry Segmentation

-

1. Type

- 1.1. Gluten Free

- 1.2. Dairy Free

- 1.3. Allergen Free

- 1.4. Other Types

-

2. End Product

- 2.1. Bakery and Confectionery

- 2.2. Dairy-free Foods

- 2.3. Snacks

- 2.4. Beverages

- 2.5. Other End Products

-

3. Distribution Channel

- 3.1. Supermarkets/Hypermarkets

- 3.2. Online Retail Stores

- 3.3. Convenience Stores

- 3.4. Other Distribution Channels

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

- 4.4. Rest of North America

North America Free-From Food Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Free-From Food Industry Regional Market Share

Geographic Coverage of North America Free-From Food Industry

North America Free-From Food Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Convenient Snacking Options; Increase in Demand for New and Innovative Flavored Meat Snacks

- 3.3. Market Restrains

- 3.3.1. Fluctuations in the Price of Raw Materials

- 3.4. Market Trends

- 3.4.1. Increasing Demand For Allergen Free Products

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Free-From Food Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Gluten Free

- 5.1.2. Dairy Free

- 5.1.3. Allergen Free

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End Product

- 5.2.1. Bakery and Confectionery

- 5.2.2. Dairy-free Foods

- 5.2.3. Snacks

- 5.2.4. Beverages

- 5.2.5. Other End Products

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/Hypermarkets

- 5.3.2. Online Retail Stores

- 5.3.3. Convenience Stores

- 5.3.4. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.5.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Free-From Food Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Gluten Free

- 6.1.2. Dairy Free

- 6.1.3. Allergen Free

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End Product

- 6.2.1. Bakery and Confectionery

- 6.2.2. Dairy-free Foods

- 6.2.3. Snacks

- 6.2.4. Beverages

- 6.2.5. Other End Products

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Supermarkets/Hypermarkets

- 6.3.2. Online Retail Stores

- 6.3.3. Convenience Stores

- 6.3.4. Other Distribution Channels

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.4.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Canada North America Free-From Food Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Gluten Free

- 7.1.2. Dairy Free

- 7.1.3. Allergen Free

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End Product

- 7.2.1. Bakery and Confectionery

- 7.2.2. Dairy-free Foods

- 7.2.3. Snacks

- 7.2.4. Beverages

- 7.2.5. Other End Products

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Supermarkets/Hypermarkets

- 7.3.2. Online Retail Stores

- 7.3.3. Convenience Stores

- 7.3.4. Other Distribution Channels

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.4.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Mexico North America Free-From Food Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Gluten Free

- 8.1.2. Dairy Free

- 8.1.3. Allergen Free

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End Product

- 8.2.1. Bakery and Confectionery

- 8.2.2. Dairy-free Foods

- 8.2.3. Snacks

- 8.2.4. Beverages

- 8.2.5. Other End Products

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Supermarkets/Hypermarkets

- 8.3.2. Online Retail Stores

- 8.3.3. Convenience Stores

- 8.3.4. Other Distribution Channels

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.4.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of North America North America Free-From Food Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Gluten Free

- 9.1.2. Dairy Free

- 9.1.3. Allergen Free

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End Product

- 9.2.1. Bakery and Confectionery

- 9.2.2. Dairy-free Foods

- 9.2.3. Snacks

- 9.2.4. Beverages

- 9.2.5. Other End Products

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Supermarkets/Hypermarkets

- 9.3.2. Online Retail Stores

- 9.3.3. Convenience Stores

- 9.3.4. Other Distribution Channels

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Mexico

- 9.4.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Prairie Farms

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Dean Foods

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 General Mills Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Bob's Red Mill

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Conagra Brands Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Hain Celestial Group Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Johnson & Johnson (Lactaid)

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 AMY'S KITCHEN INC*List Not Exhaustive

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.1 Prairie Farms

List of Figures

- Figure 1: North America Free-From Food Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: North America Free-From Food Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Free-From Food Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: North America Free-From Food Industry Revenue undefined Forecast, by End Product 2020 & 2033

- Table 3: North America Free-From Food Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 4: North America Free-From Food Industry Revenue undefined Forecast, by Geography 2020 & 2033

- Table 5: North America Free-From Food Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: North America Free-From Food Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 7: North America Free-From Food Industry Revenue undefined Forecast, by End Product 2020 & 2033

- Table 8: North America Free-From Food Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 9: North America Free-From Food Industry Revenue undefined Forecast, by Geography 2020 & 2033

- Table 10: North America Free-From Food Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 11: North America Free-From Food Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: North America Free-From Food Industry Revenue undefined Forecast, by End Product 2020 & 2033

- Table 13: North America Free-From Food Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 14: North America Free-From Food Industry Revenue undefined Forecast, by Geography 2020 & 2033

- Table 15: North America Free-From Food Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 16: North America Free-From Food Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 17: North America Free-From Food Industry Revenue undefined Forecast, by End Product 2020 & 2033

- Table 18: North America Free-From Food Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 19: North America Free-From Food Industry Revenue undefined Forecast, by Geography 2020 & 2033

- Table 20: North America Free-From Food Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: North America Free-From Food Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: North America Free-From Food Industry Revenue undefined Forecast, by End Product 2020 & 2033

- Table 23: North America Free-From Food Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 24: North America Free-From Food Industry Revenue undefined Forecast, by Geography 2020 & 2033

- Table 25: North America Free-From Food Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Free-From Food Industry?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the North America Free-From Food Industry?

Key companies in the market include Prairie Farms, Dean Foods, General Mills Inc, Bob's Red Mill, Conagra Brands Inc, Hain Celestial Group Inc, Johnson & Johnson (Lactaid), AMY'S KITCHEN INC*List Not Exhaustive.

3. What are the main segments of the North America Free-From Food Industry?

The market segments include Type, End Product, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Convenient Snacking Options; Increase in Demand for New and Innovative Flavored Meat Snacks.

6. What are the notable trends driving market growth?

Increasing Demand For Allergen Free Products.

7. Are there any restraints impacting market growth?

Fluctuations in the Price of Raw Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Free-From Food Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Free-From Food Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Free-From Food Industry?

To stay informed about further developments, trends, and reports in the North America Free-From Food Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence