Key Insights

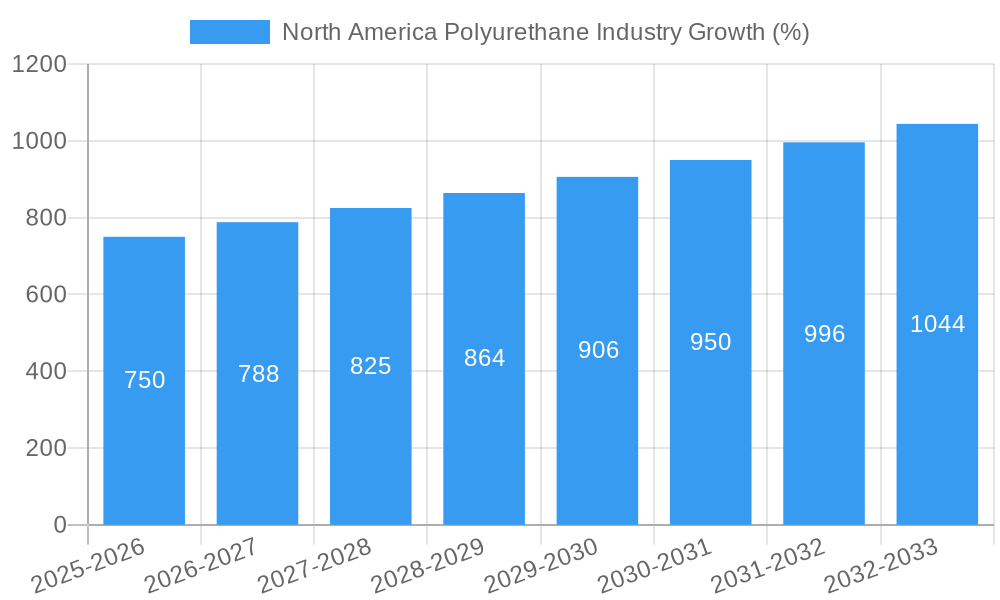

The North American polyurethane market, currently valued at approximately $XX billion in 2025 (assuming a logical estimation based on global market size and regional distribution), is projected to experience robust growth, exceeding a 5% CAGR through 2033. This expansion is fueled by several key drivers. The burgeoning construction industry, particularly in residential and commercial segments, significantly boosts demand for polyurethane foams in insulation and roofing applications. Simultaneously, the automotive sector's increasing adoption of lightweight, high-performance materials fuels the use of polyurethane in seating, dashboards, and other components. Growth in the furniture and interiors sector, driven by consumer preference for comfortable and durable products, further contributes to market expansion. Technological advancements leading to the development of bio-based and recycled polyurethane alternatives are also shaping market dynamics, fostering sustainability initiatives and attracting environmentally conscious consumers. However, fluctuating raw material prices and concerns regarding the environmental impact of certain polyurethane production processes pose potential restraints on market growth. Segmentation analysis reveals significant contributions from flexible foam applications (coatings, adhesives, sealants, and binders) and the building and construction end-user industry. Leading companies like BASF, Dow, and Huntsman are actively investing in research and development, expanding their product portfolios to cater to evolving market needs and enhance their competitive positioning within this dynamic landscape.

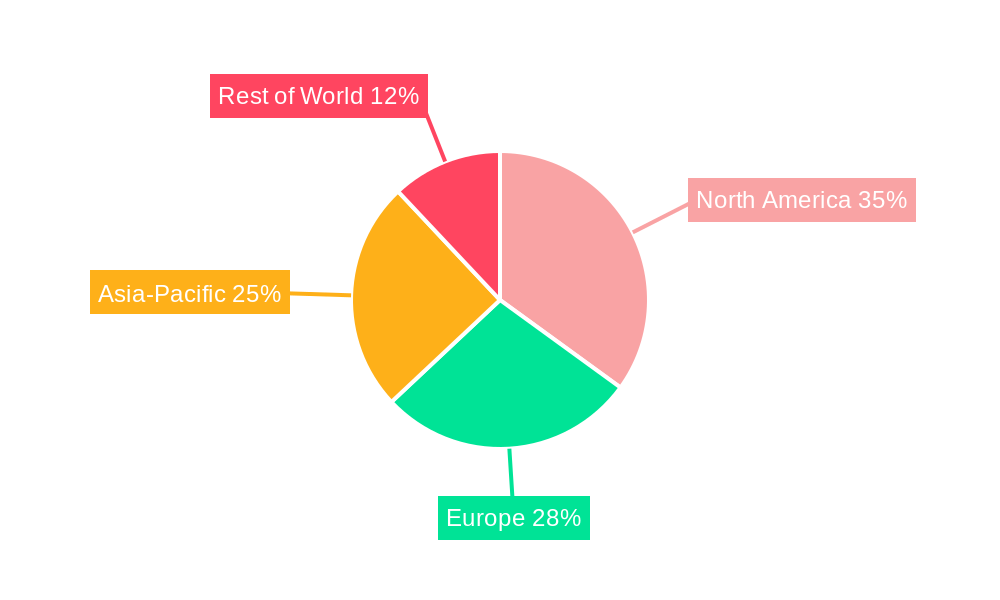

Within the North American market, the United States represents the largest segment, followed by Canada and Mexico. The Rest of North America region exhibits considerable growth potential, driven by increasing industrialization and infrastructure development. The competitive landscape is characterized by the presence of both established multinational corporations and regional players. While established players leverage their extensive distribution networks and brand recognition, smaller companies focus on niche applications and innovative product development. Overall, the North American polyurethane market offers significant opportunities for growth, provided companies effectively address the challenges posed by fluctuating raw material costs and environmental concerns, while capitalizing on the escalating demand driven by key end-user industries. Future market success will hinge on companies' ability to innovate, diversify their product offerings, and embrace sustainable manufacturing practices.

North America Polyurethane Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the North America polyurethane industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The report covers the period 2019-2033, with a focus on the 2025-2033 forecast period, utilizing data from the base year 2025 and incorporating historical data from 2019-2024. The report leverages rigorous market research and data analysis to present a clear picture of the market's current state and its future trajectory. Expect actionable intelligence on market size (in Millions), CAGR, key players, and emerging trends.

North America Polyurethane Industry Market Structure & Innovation Trends

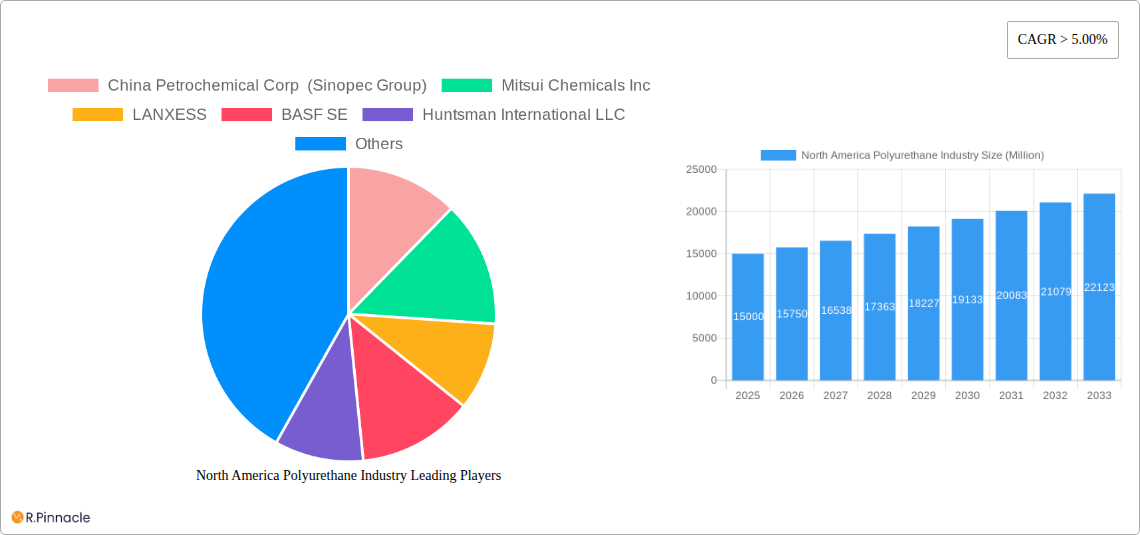

This section analyzes the competitive landscape of the North American polyurethane industry, examining market concentration, innovation drivers, and regulatory influences. The analysis incorporates data on mergers and acquisitions (M&A) activity, including deal values, and provides a detailed look at the market share held by key players such as China Petrochemical Corp (Sinopec Group), Mitsui Chemicals Inc, LANXESS, BASF SE, Huntsman International LLC, Fujian Southeast Electrochemical Co Ltd, Dow, Covestro AG, Tosoh Corporation, and Perstorp.

Market Concentration: The North American polyurethane market exhibits a moderately concentrated structure, with the top five players holding an estimated xx% market share in 2025. This concentration is influenced by the significant capital investment required for production and the presence of established multinational corporations.

Innovation Drivers: Key innovation drivers include the demand for high-performance materials in automotive and construction applications, the development of sustainable and bio-based polyurethane alternatives, and advancements in foam technology.

Regulatory Framework: Environmental regulations, particularly those related to VOC emissions and the use of hazardous chemicals, significantly influence the industry's innovation trajectory.

Product Substitutes: The industry faces competition from alternative materials, such as bioplastics and other polymers, particularly in certain niche applications.

End-User Demographics: Growth in the construction, automotive, and furniture sectors directly impacts polyurethane demand, influencing market expansion.

M&A Activity: The past five years have witnessed significant M&A activity in the North American polyurethane industry, with deal values totaling an estimated xx Million. These transactions have reshaped the competitive landscape, fostering consolidation and driving innovation.

North America Polyurethane Industry Market Dynamics & Trends

This section delves into the key factors shaping the market's growth trajectory. We explore market growth drivers, technological disruptions, consumer preferences, and competitive dynamics, providing a comprehensive overview of the industry's evolving landscape. The analysis includes projected compound annual growth rates (CAGRs) and penetration rates for key segments.

The North American polyurethane market is expected to witness significant growth over the forecast period, driven by factors such as the increasing demand for lightweight and energy-efficient materials in the automotive and construction sectors. Technological advancements such as the development of bio-based polyurethanes are expected to further fuel market growth. Changing consumer preferences toward sustainable products and a rising focus on environmental concerns are also influencing market trends. Intense competition among major players is driving innovation and cost optimization. The projected CAGR for the forecast period (2025-2033) is estimated at xx%. Market penetration in key end-user segments is anticipated to increase by xx% by 2033.

Dominant Regions & Segments in North America Polyurethane Industry

This section identifies the leading regions and segments within the North American polyurethane market. The analysis highlights key drivers of growth in these areas, examining economic policies, infrastructure development, and other contributing factors.

Leading Region: The [Specific Region - e.g., South-East] region of North America is projected to dominate the market due to [Specific Reason - e.g., robust construction activity and a high concentration of automotive manufacturing facilities].

Leading Application Segment: The foams segment, particularly flexible foams, is expected to hold the largest market share in 2025, driven by [Reason - e.g., its extensive use in the furniture and automotive industries].

Leading End-user Industry: The building and construction sector represents a significant end-user industry for polyurethanes, owing to [Reasons - e.g., its use in insulation, roofing, and flooring applications].

Key Drivers (across segments):

- Favorable economic conditions stimulating construction and manufacturing activities.

- Growing investments in infrastructure development.

- Increasing demand for energy-efficient building materials.

- Technological advancements leading to improved product performance and cost-effectiveness.

North America Polyurethane Industry Product Innovations

Recent years have witnessed significant advancements in polyurethane technology. The development of high-performance materials with enhanced properties, such as improved thermal insulation, durability, and flexibility, has expanded the application range of polyurethane. The integration of nanomaterials and bio-based components is driving the creation of sustainable and environmentally friendly polyurethane products. These innovations cater to increasing demands in various sectors, ensuring a strong market fit and providing competitive advantages to manufacturers.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North American polyurethane market, segmented by application (Foams, Flexible Foams, Coatings, Adhesives, Sealants and Binders, Elastomers, Other Applications) and end-user industry (Furniture and Interiors, Building and Construction, Electronics and Appliances, Automotive and Transportation, Packaging, Other End-user Industries). Each segment's growth projection, market size (in Millions), and competitive dynamics are detailed. For example, the flexible foams segment is expected to witness significant growth, driven by rising demand from the automotive and furniture sectors. Similarly, the building and construction industry is expected to remain a key driver for polyurethane demand.

Key Drivers of North America Polyurethane Industry Growth

Several factors fuel the growth of the North American polyurethane industry. Technological advancements, particularly in the development of sustainable and high-performance materials, are a major driver. The robust growth of end-user industries, such as construction and automotive, significantly boosts demand. Furthermore, favorable government policies promoting energy efficiency and sustainable building practices contribute positively to market expansion.

Challenges in the North America Polyurethane Industry Sector

The North American polyurethane industry faces challenges, including stringent environmental regulations impacting production costs and the availability of raw materials. Fluctuations in raw material prices and supply chain disruptions pose significant operational hurdles. Moreover, intensifying competition and the emergence of substitute materials exert pressure on profitability and market share. These factors collectively impact industry growth and profitability.

Emerging Opportunities in North America Polyurethane Industry

Emerging opportunities in the North American polyurethane industry include the increasing demand for sustainable and bio-based polyurethane products, driven by environmental concerns. Technological advancements, such as 3D printing and additive manufacturing, are creating new applications and market segments. Furthermore, expanding into niche markets and exploring innovative applications in areas like aerospace and renewable energy represent promising growth avenues.

Leading Players in the North America Polyurethane Industry Market

- China Petrochemical Corp (Sinopec Group)

- Mitsui Chemicals Inc

- LANXESS

- BASF SE

- Huntsman International LLC

- Fujian Southeast Electrochemical Co Ltd

- Dow

- Covestro AG

- Tosoh Corporation

- Perstorp

Key Developments in North America Polyurethane Industry Industry

- 2023-Q4: Covestro AG announced the expansion of its production capacity for sustainable polyurethane raw materials.

- 2022-Q3: BASF SE launched a new range of high-performance polyurethanes for automotive applications.

- 2021-Q2: Huntsman International LLC acquired a smaller polyurethane producer, strengthening its market position.

- [Add more relevant developments with year/month and brief description of impact.]

Future Outlook for North America Polyurethane Industry Market

The North American polyurethane industry's future looks promising, fueled by continuous technological advancements and increasing demand from key end-user sectors. Strategic initiatives focusing on sustainability and innovation will be crucial for sustained growth. The expanding applications of polyurethane in renewable energy and advanced manufacturing further enhance market prospects. The market is poised for significant expansion, driven by both established and emerging applications, promising substantial growth opportunities for key players.

North America Polyurethane Industry Segmentation

-

1. Application

- 1.1. Foams

- 1.2. Coatings

- 1.3. Adhesives, Sealants, and Binders

- 1.4. Elastomers

- 1.5. Other Applications

-

2. End-user Industry

- 2.1. Furniture and Interiors

- 2.2. Building and Construction

- 2.3. Electronics and Appliances

- 2.4. Automotive and Transportation

- 2.5. Packaging

- 2.6. Other End-user Industries

-

3. Geography

- 3.1. United States

- 3.2. Mexico

- 3.3. Canada

- 3.4. Rest of North America

North America Polyurethane Industry Segmentation By Geography

- 1. United States

- 2. Mexico

- 3. Canada

- 4. Rest of North America

North America Polyurethane Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Use of Durable Plastics in Construction; Increasing Emphasis on Recycling

- 3.3. Market Restrains

- 3.3.1. ; Volatile Raw Material Prices; Competition from Polystyrene and Polypropylene Foam

- 3.4. Market Trends

- 3.4.1. Foams Application is Expected to Hold the Largest Share of the Application Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Foams

- 5.1.2. Coatings

- 5.1.3. Adhesives, Sealants, and Binders

- 5.1.4. Elastomers

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Furniture and Interiors

- 5.2.2. Building and Construction

- 5.2.3. Electronics and Appliances

- 5.2.4. Automotive and Transportation

- 5.2.5. Packaging

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Mexico

- 5.3.3. Canada

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Mexico

- 5.4.3. Canada

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. United States North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Foams

- 6.1.2. Coatings

- 6.1.3. Adhesives, Sealants, and Binders

- 6.1.4. Elastomers

- 6.1.5. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Furniture and Interiors

- 6.2.2. Building and Construction

- 6.2.3. Electronics and Appliances

- 6.2.4. Automotive and Transportation

- 6.2.5. Packaging

- 6.2.6. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Mexico

- 6.3.3. Canada

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Mexico North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Foams

- 7.1.2. Coatings

- 7.1.3. Adhesives, Sealants, and Binders

- 7.1.4. Elastomers

- 7.1.5. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Furniture and Interiors

- 7.2.2. Building and Construction

- 7.2.3. Electronics and Appliances

- 7.2.4. Automotive and Transportation

- 7.2.5. Packaging

- 7.2.6. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Mexico

- 7.3.3. Canada

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Canada North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Foams

- 8.1.2. Coatings

- 8.1.3. Adhesives, Sealants, and Binders

- 8.1.4. Elastomers

- 8.1.5. Other Applications

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Furniture and Interiors

- 8.2.2. Building and Construction

- 8.2.3. Electronics and Appliances

- 8.2.4. Automotive and Transportation

- 8.2.5. Packaging

- 8.2.6. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Mexico

- 8.3.3. Canada

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Rest of North America North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Foams

- 9.1.2. Coatings

- 9.1.3. Adhesives, Sealants, and Binders

- 9.1.4. Elastomers

- 9.1.5. Other Applications

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Furniture and Interiors

- 9.2.2. Building and Construction

- 9.2.3. Electronics and Appliances

- 9.2.4. Automotive and Transportation

- 9.2.5. Packaging

- 9.2.6. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Mexico

- 9.3.3. Canada

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. United States North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 China Petrochemical Corp (Sinopec Group)

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Mitsui Chemicals Inc

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 LANXESS

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 BASF SE

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Huntsman International LLC

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Fujian Southeast Electrochemical Co Ltd

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Dow

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Covestro AG

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Tosoh Corporation

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Perstorp

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 China Petrochemical Corp (Sinopec Group)

List of Figures

- Figure 1: North America Polyurethane Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Polyurethane Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Polyurethane Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Region 2019 & 2032

- Table 3: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 5: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 6: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 7: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 9: North America Polyurethane Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Region 2019 & 2032

- Table 11: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 13: United States North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United States North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 15: Canada North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Mexico North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 19: Rest of North America North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of North America North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 21: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 22: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 23: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 24: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 25: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 27: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 29: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 30: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 31: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 32: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 33: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 34: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 35: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 37: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 39: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 40: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 41: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 42: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 43: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 44: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 45: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 46: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 47: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 48: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 49: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 50: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 51: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Polyurethane Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Polyurethane Industry?

Key companies in the market include China Petrochemical Corp (Sinopec Group), Mitsui Chemicals Inc, LANXESS, BASF SE, Huntsman International LLC, Fujian Southeast Electrochemical Co Ltd, Dow, Covestro AG, Tosoh Corporation, Perstorp.

3. What are the main segments of the North America Polyurethane Industry?

The market segments include Application, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Use of Durable Plastics in Construction; Increasing Emphasis on Recycling.

6. What are the notable trends driving market growth?

Foams Application is Expected to Hold the Largest Share of the Application Segment.

7. Are there any restraints impacting market growth?

; Volatile Raw Material Prices; Competition from Polystyrene and Polypropylene Foam.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in kilograms per cubic meter.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Polyurethane Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Polyurethane Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Polyurethane Industry?

To stay informed about further developments, trends, and reports in the North America Polyurethane Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence