Key Insights

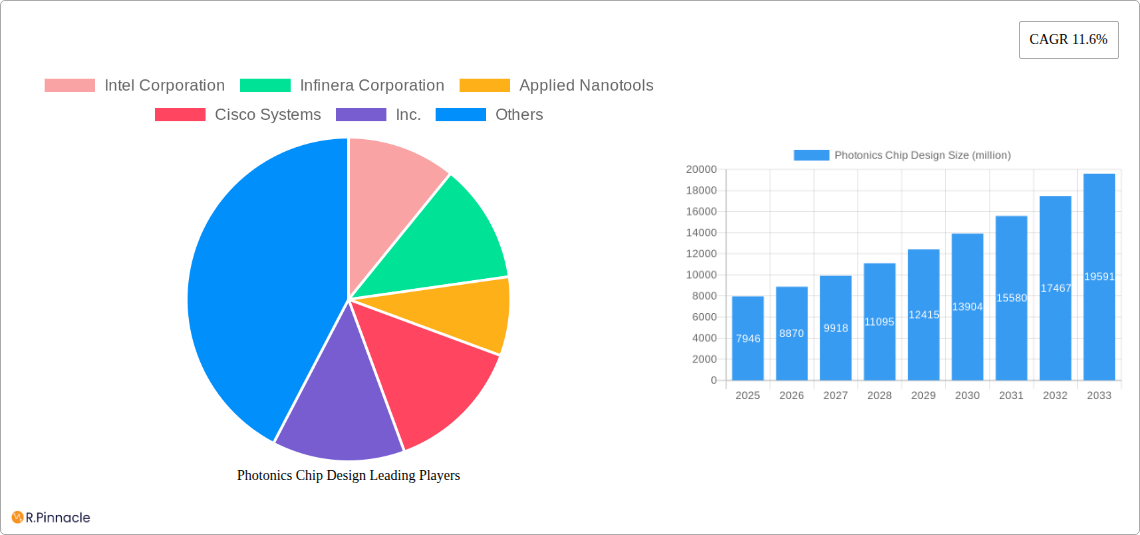

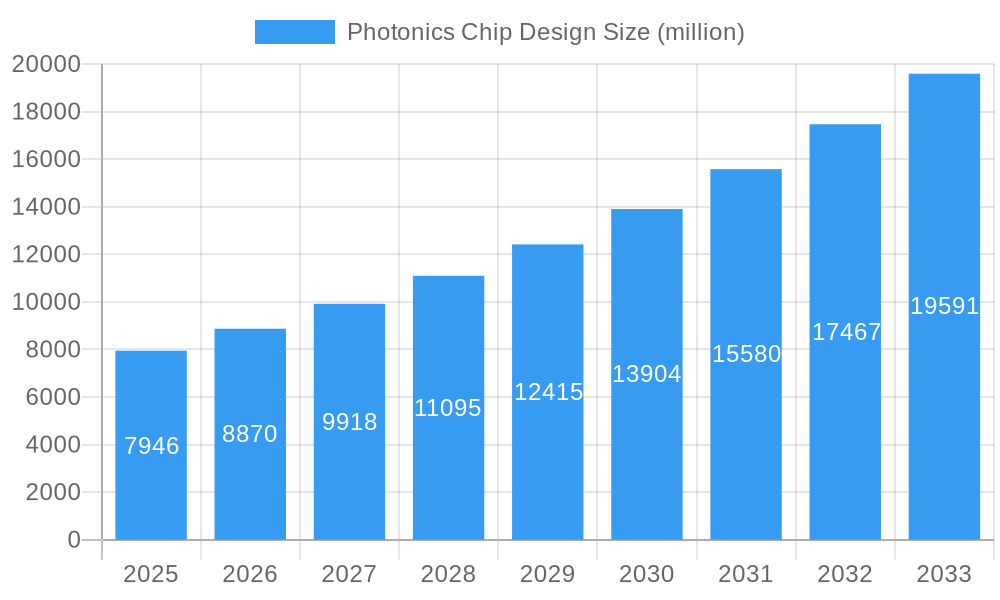

The global Photonics Chip Design market is poised for significant expansion, projected to reach \$7,946 million in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 11.6% expected over the forecast period of 2025-2033. This robust growth is primarily fueled by the burgeoning demand across critical sectors such as Telecom and Data Centers, where optical communication solutions are indispensable for handling escalating data traffic and enabling higher bandwidth. The advancement of quantum computing is emerging as a powerful new driver, necessitating sophisticated photonic components for its complex operations. Furthermore, continuous innovation in laser chip technologies, including VCSEL, FP, DFB, and EML, alongside advancements in detector chips like PIN and APD, are expanding the capabilities and applications of photonic chips, thereby propelling market growth.

Photonics Chip Design Market Size (In Billion)

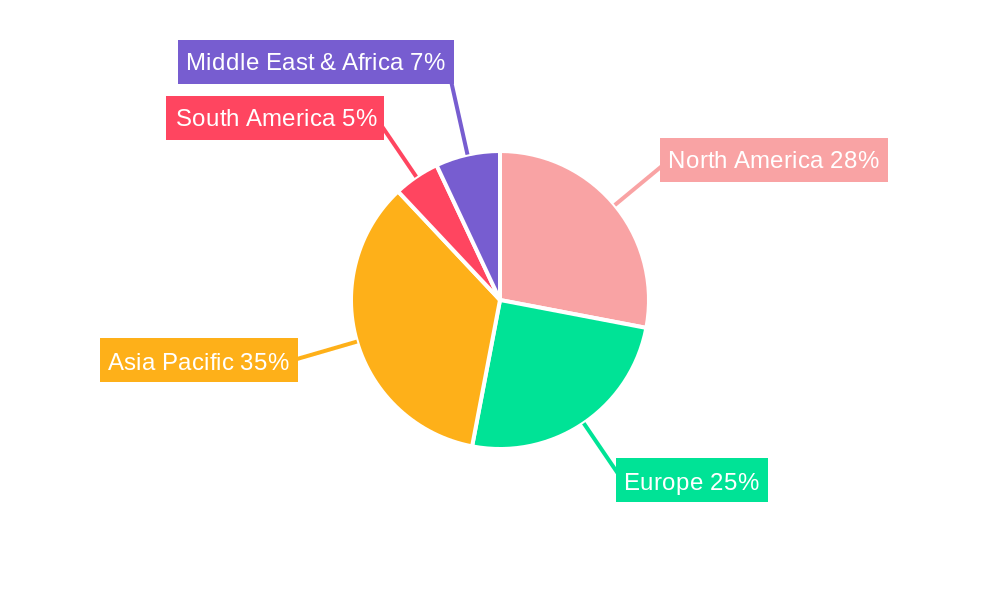

The market is characterized by a dynamic interplay of growth drivers and restraints, alongside evolving trends. Key growth enablers include the relentless pursuit of faster and more efficient data transmission, miniaturization of optical components, and the increasing integration of photonics with other technologies like AI and machine learning. Emerging trends such as the development of silicon photonics for cost-effective manufacturing and the exploration of new applications in areas like sensing and imaging are further shaping the market landscape. However, challenges such as high initial R&D costs, complex manufacturing processes, and the need for skilled expertise in photonics design and fabrication present considerable restraints. Despite these hurdles, the strategic investments by leading companies like Intel Corporation, Broadcom, and Cisco Systems, Inc., coupled with a strong regional presence in Asia Pacific, North America, and Europe, indicate a highly competitive yet opportunistic market.

Photonics Chip Design Company Market Share

Photonics Chip Design Market Structure & Innovation Trends

The photonics chip design market exhibits a moderately concentrated structure, with key players like Intel Corporation, Infinera Corporation, Broadcom, and Marvell (Inphi) holding significant market share. Innovation is the primary driver, fueled by advancements in silicon photonics, integrated photonics, and heterogeneous integration. The research and development expenditure is estimated to be in the range of several hundred million dollars annually across leading companies. Regulatory frameworks primarily focus on standardization and interoperability, with initiatives from bodies like IEEE influencing design specifications. Product substitutes, while existing in the form of traditional electronic components for certain low-speed applications, are rapidly being displaced by the superior performance of photonic solutions in high-bandwidth scenarios. End-user demographics are increasingly sophisticated, demanding higher speeds, lower latency, and greater energy efficiency, particularly within the telecom and data center segments. Mergers and acquisitions are a notable trend, with deal values often exceeding several hundred million dollars as companies seek to consolidate expertise, expand product portfolios, and gain market access. For instance, recent M&A activities have seen acquisitions valued at over $500 million, aimed at acquiring specialized photonic design capabilities. The market is characterized by a continuous cycle of innovation, with companies investing significantly to stay ahead of technological curves and meet evolving industry demands.

Photonics Chip Design Market Dynamics & Trends

The global photonics chip design market is poised for substantial growth, driven by the insatiable demand for higher data processing and transmission speeds across critical sectors. The compound annual growth rate (CAGR) is projected to be robust, estimated at over 15% during the forecast period. This growth is fundamentally propelled by the exponential rise in data traffic generated by cloud computing, artificial intelligence (AI), machine learning (ML), and the burgeoning Internet of Things (IoT) ecosystem. The increasing adoption of 5G and future wireless technologies necessitates ultra-high-speed optical interconnects, directly benefiting the photonics chip design market. Data centers, in particular, are undergoing rapid expansion and upgrades, requiring more sophisticated and energy-efficient optical transceivers and components to handle the massive data flows. The transition from traditional copper interconnects to optical solutions in these environments is a significant trend, driven by the limitations of copper in terms of bandwidth and distance. Furthermore, the emerging quantum computing sector, while still nascent, presents a long-term growth opportunity, with specialized photonic chips playing a crucial role in qubit manipulation and interconnectivity. Consumer preferences are increasingly leaning towards devices and services that offer seamless, high-speed connectivity, pushing the boundaries of what is technologically feasible. This translates into a continuous demand for advanced photonics chips capable of delivering unprecedented performance. Competitive dynamics are intense, with established semiconductor giants and specialized photonics firms vying for market dominance. Strategic partnerships and collaborations are common as companies aim to leverage complementary technologies and accelerate product development. The market penetration of advanced photonic solutions is steadily increasing across various applications, replacing older technologies and opening up new possibilities for innovation and efficiency. The ongoing miniaturization of electronic components, coupled with the inherent advantages of light for data transmission, ensures that photonics chip design will remain at the forefront of technological advancement for the foreseeable future.

Dominant Regions & Segments in Photonics Chip Design

North America, particularly the United States, stands out as a dominant region in the photonics chip design market. This leadership is underpinned by several factors, including a strong ecosystem of research institutions, venture capital funding, and a concentration of leading technology companies such as Intel Corporation, Cisco Systems, Inc., Broadcom, and Marvell (Inphi). The presence of robust telecommunications infrastructure and the rapid adoption of advanced data center technologies further bolster its position. Government initiatives supporting semiconductor manufacturing and research also play a crucial role.

Within the application segments, the Telecom sector is a major driver of growth. The ongoing global rollout of 5G networks and the expansion of fiber optic infrastructure worldwide require high-performance, cost-effective photonics chips for optical transceivers, switches, and other networking components. The demand for increased bandwidth and lower latency in telecommunication networks directly translates to a higher need for advanced laser chips (e.g., DFB, EML) and detector chips (e.g., PIN, APD).

The Data Center segment is another significant contributor, fueled by the exponential growth of cloud computing, AI, and big data analytics. Data centers are continuously expanding and upgrading their infrastructure to handle massive data volumes. Photonics chips are essential for high-speed optical interconnects within servers, racks, and between data centers, enabling faster data transfer and reduced power consumption. Companies like Cisco Systems, Inc., and Infinera Corporation are key players in this space, offering solutions for high-density, high-speed data communication.

While currently smaller in market size, the Quantum segment represents a significant emerging opportunity. Photonics plays a pivotal role in quantum computing for entanglement generation, qubit manipulation, and quantum communication. Research institutions and specialized companies are actively developing advanced photonic chips for quantum processors, which could revolutionize computing in the future.

The Others application segment encompasses a diverse range of applications including high-speed computing, industrial automation, medical imaging, and sensing. The increasing integration of optical technologies in these areas, driven by the need for precision, speed, and miniaturization, contributes to market growth.

In terms of Types, Laser Chips are a cornerstone of the photonics chip design market.

- VCSEL (Vertical-Cavity Surface-Emitting Laser) chips are widely used in short-reach optical interconnects within data centers and for consumer electronics due to their cost-effectiveness and ease of integration.

- FP (Fabry-Perot) lasers find applications in cost-sensitive segments requiring moderate bandwidth.

- DFB (Distributed Feedback) lasers are crucial for longer-reach telecommunication applications, offering superior wavelength stability and narrower linewidths.

- EML (Electro-absorption Modulator Lasers) combine laser emission and modulation, enabling higher data rates and longer reach, critical for high-end telecom and data center interconnects.

Detector Chips are equally vital.

- PIN (Positive-Intrinsic-Negative) photodiodes are commonly used for their reliability and cost-effectiveness in various optical communication systems.

- APD (Avalanche Photodiode) chips offer higher sensitivity and are employed in applications requiring the detection of weak optical signals, such as long-haul optical networks and certain sensing applications.

The dominance of these regions and segments is driven by a combination of economic policies promoting technological development, substantial investments in R&D and infrastructure, and a clear demand for high-performance optical solutions that transcend the limitations of electronic components.

Photonics Chip Design Product Innovations

Photonics chip design is witnessing a surge in product innovations aimed at enhancing speed, efficiency, and integration. Key developments include the advancement of silicon photonics platforms, enabling the monolithic integration of optical and electronic functions onto a single chip. This leads to smaller, more power-efficient, and cost-effective optical interconnects for data centers and telecom. Companies are also focusing on higher-performance laser and detector chips, such as those incorporating advanced materials and novel architectures to achieve higher data rates and lower error rates. The development of tunable lasers and co-packaged optics solutions further pushes the boundaries of optical communication. These innovations offer significant competitive advantages by enabling denser integration, reducing form factors, and ultimately lowering the total cost of ownership for end-users, driving market adoption across a wider range of applications.

Report Scope & Segmentation Analysis

This report meticulously analyzes the photonics chip design market across its key segmentations. The Application segmentation includes Telecom, characterized by its extensive network infrastructure upgrades and the demand for high-speed optical transceivers, projecting significant growth in the coming years. The Data Center segment is experiencing rapid expansion due to cloud computing and AI, requiring dense, high-bandwidth optical interconnects, with substantial market share and continued growth. The Quantum segment, though nascent, presents a high-growth potential driven by advancements in quantum computing and communication, with specialized photonic chips being critical enablers. The Others segment encompasses a broad spectrum of industrial, medical, and sensing applications, demonstrating steady growth as optical technologies find wider adoption.

The Types segmentation focuses on crucial photonic components. Laser Chips, including VCSEL, FP, DFB, and EML, are critical for generating and modulating light. The demand for each sub-type varies by application, with VCSELs prevalent in short-reach and EMLs in high-speed long-reach scenarios. Detector Chips, comprising PIN and APD, are essential for converting optical signals back into electrical signals. The market for these components is directly tied to the growth of the application segments, with continuous innovation driving improved performance and functionality across all types.

Key Drivers of Photonics Chip Design Growth

The growth of the photonics chip design market is propelled by several interconnected factors. The escalating demand for data bandwidth, driven by cloud computing, AI, and 5G deployment, is a primary catalyst, necessitating faster and more efficient optical interconnects. Technological advancements in silicon photonics and integrated photonics allow for higher levels of integration, reduced power consumption, and lower costs, making optical solutions more accessible. Regulatory push for energy efficiency in data centers and telecommunication networks also favors photonics due to its inherent power advantages over traditional electronics for high-speed data transmission. Furthermore, the increasing investment in R&D by both established players and startups, as exemplified by significant funding rounds and strategic partnerships, fosters continuous innovation and the development of next-generation photonic chips.

Challenges in the Photonics Chip Design Sector

Despite its robust growth, the photonics chip design sector faces several challenges. High development costs associated with complex fabrication processes and specialized equipment can be a significant barrier, especially for smaller companies. Supply chain complexities, including the availability of specialized raw materials and manufacturing capacity, can lead to lead time issues and cost volatility. Standardization challenges across different photonic technologies and interfaces can hinder interoperability and market adoption. Intense competition from both established players and emerging innovators necessitates continuous investment in R&D to maintain a competitive edge. Finally, the skill gap in highly specialized areas of photonics design and fabrication can limit the pace of innovation and production.

Emerging Opportunities in Photonics Chip Design

The photonics chip design sector is ripe with emerging opportunities. The growth of AI and machine learning is creating unprecedented demand for high-speed, low-latency interconnects within AI accelerators and data centers, a perfect use case for advanced photonic chips. The nascent but rapidly developing quantum computing field presents a significant long-term opportunity, as photonic technologies are crucial for building and operating quantum computers. Edge computing and the proliferation of IoT devices will drive demand for compact, power-efficient photonic solutions for localized data processing and communication. Furthermore, the application of photonics in emerging areas like augmented and virtual reality (AR/VR), advanced medical diagnostics, and high-resolution sensing offers substantial new market avenues for innovative photonic chip designs.

Leading Players in the Photonics Chip Design Market

- Intel Corporation

- Infinera Corporation

- Applied Nanotools

- Cisco Systems, Inc.

- Broadcom

- Bright Photonics

- Acacia

- Marvell (Inphi)

- Ciena

- Coherent

- CMC Microsystems

- ANELLO Photonics

- Ansys

- Eoptolink

Key Developments in Photonics Chip Design Industry

- 2024: Significant advancements in co-packaged optics (CPO) technology, aiming to integrate optical engines directly with high-performance networking chips, leading to substantial improvements in power efficiency and density.

- 2023: Increased investment and research into silicon nitride photonics platforms, offering enhanced performance characteristics for applications requiring low loss and broadband operation.

- 2023: Major breakthroughs in laser efficiency and wavelength tunability for DFB and EML chips, enabling higher data rates and more flexible optical network configurations.

- 2023: Expansion of photonic integrated circuits (PICs) for quantum computing applications, with companies demonstrating novel designs for qubit interconnects and control.

- 2022: Acquisitions and strategic partnerships focused on consolidating expertise in high-speed optical transceivers and silicon photonics, such as the acquisition of a key photonics startup by a major semiconductor firm.

- 2021: Introduction of next-generation PIN and APD detector chips with improved bandwidth and sensitivity, supporting the higher data rates in 400G and 800G optical networks.

Future Outlook for Photonics Chip Design Market

The future outlook for the photonics chip design market is exceptionally bright, characterized by sustained high growth driven by ongoing digital transformation. The relentless demand for higher data speeds and lower latency in telecom and data centers will continue to be the primary growth accelerator, pushing the boundaries of optical interconnect technologies. The increasing integration of photonics with advanced computing paradigms like AI and quantum computing will open up entirely new markets and applications. Furthermore, advancements in manufacturing techniques and materials science will lead to more cost-effective and higher-performance photonic chips, broadening their applicability across diverse industries. Strategic collaborations and continued R&D investment will be crucial for players to capitalize on these opportunities and maintain a competitive edge in this dynamic and rapidly evolving market. The projected market size is expected to reach several tens of billions of dollars by the end of the forecast period.

Photonics Chip Design Segmentation

-

1. Application

- 1.1. Telecom

- 1.2. Data Center

- 1.3. Quantum

- 1.4. Others

-

2. Types

- 2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 2.2. Detector Chips (PIN and APD)

Photonics Chip Design Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Photonics Chip Design Regional Market Share

Geographic Coverage of Photonics Chip Design

Photonics Chip Design REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Telecom

- 5.1.2. Data Center

- 5.1.3. Quantum

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 5.2.2. Detector Chips (PIN and APD)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Telecom

- 6.1.2. Data Center

- 6.1.3. Quantum

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 6.2.2. Detector Chips (PIN and APD)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Telecom

- 7.1.2. Data Center

- 7.1.3. Quantum

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 7.2.2. Detector Chips (PIN and APD)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Telecom

- 8.1.2. Data Center

- 8.1.3. Quantum

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 8.2.2. Detector Chips (PIN and APD)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Telecom

- 9.1.2. Data Center

- 9.1.3. Quantum

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 9.2.2. Detector Chips (PIN and APD)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Photonics Chip Design Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Telecom

- 10.1.2. Data Center

- 10.1.3. Quantum

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Laser Chips (VCSEL, FP, DFB, EML)

- 10.2.2. Detector Chips (PIN and APD)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Intel Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Infinera Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Applied Nanotools

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cisco Systems

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Broadcom

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bright Photonics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Acacia

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Marvell (Inphi)

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ciena

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Coherent

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 CMC Microsystems

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ANELLO Photonics

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ansys

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Eoptolink

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Intel Corporation

List of Figures

- Figure 1: Global Photonics Chip Design Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Photonics Chip Design Revenue (million), by Application 2025 & 2033

- Figure 3: North America Photonics Chip Design Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Photonics Chip Design Revenue (million), by Types 2025 & 2033

- Figure 5: North America Photonics Chip Design Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Photonics Chip Design Revenue (million), by Country 2025 & 2033

- Figure 7: North America Photonics Chip Design Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Photonics Chip Design Revenue (million), by Application 2025 & 2033

- Figure 9: South America Photonics Chip Design Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Photonics Chip Design Revenue (million), by Types 2025 & 2033

- Figure 11: South America Photonics Chip Design Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Photonics Chip Design Revenue (million), by Country 2025 & 2033

- Figure 13: South America Photonics Chip Design Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Photonics Chip Design Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Photonics Chip Design Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Photonics Chip Design Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Photonics Chip Design Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Photonics Chip Design Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Photonics Chip Design Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Photonics Chip Design Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Photonics Chip Design Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Photonics Chip Design Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Photonics Chip Design Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Photonics Chip Design Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Photonics Chip Design Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Photonics Chip Design Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Photonics Chip Design Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Photonics Chip Design Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Photonics Chip Design Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Photonics Chip Design Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Photonics Chip Design Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Photonics Chip Design Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Photonics Chip Design Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Photonics Chip Design Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Photonics Chip Design Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Photonics Chip Design Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Photonics Chip Design Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Photonics Chip Design Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Photonics Chip Design Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Photonics Chip Design Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photonics Chip Design?

The projected CAGR is approximately 11.6%.

2. Which companies are prominent players in the Photonics Chip Design?

Key companies in the market include Intel Corporation, Infinera Corporation, Applied Nanotools, Cisco Systems, Inc., Broadcom, Bright Photonics, Acacia, Marvell (Inphi), Ciena, Coherent, CMC Microsystems, ANELLO Photonics, Ansys, Eoptolink.

3. What are the main segments of the Photonics Chip Design?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 7946 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photonics Chip Design," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photonics Chip Design report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photonics Chip Design?

To stay informed about further developments, trends, and reports in the Photonics Chip Design, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence