Key Insights

The global Private Wireless Networks market is experiencing an unprecedented surge, driven by the escalating demand for enhanced connectivity, robust security, and dedicated network infrastructure across various industries. With a market size of approximately $1.2 billion in 2024, this sector is poised for explosive growth. The primary catalysts for this expansion include the burgeoning adoption of Industrial IoT (IIoT) applications, the critical need for reliable communication in mission-critical environments, and the transformative potential of 5G technology. Enterprises are increasingly recognizing the benefits of private networks, such as lower latency, higher bandwidth, and greater control over their data, leading to significant investments in deploying these advanced solutions. Furthermore, government initiatives focused on digital transformation and smart infrastructure development are also contributing to the robust market trajectory. The inherent advantages of private wireless networks in terms of performance, reliability, and tailored security are making them indispensable for sectors ranging from manufacturing and logistics to public safety and healthcare.

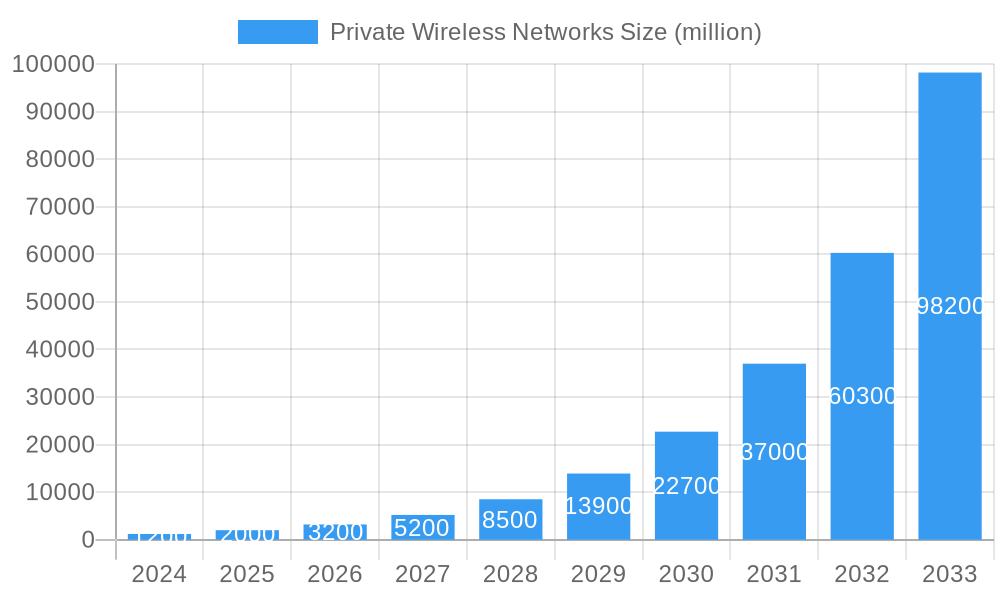

Private Wireless Networks Market Size (In Billion)

The market's impressive growth is further underscored by a remarkable Compound Annual Growth Rate (CAGR) of 62%. This phenomenal expansion is largely attributed to the accelerating rollout of 5G networks, which provide the foundational technology for high-performance private wireless solutions. The flexibility and scalability offered by these networks allow businesses to customize their connectivity to meet highly specific operational needs, a stark contrast to the limitations of public networks. While the adoption is broad, specific applications within enterprises and industrial settings are emerging as key growth engines. The market is also seeing increasing interest from government entities seeking to secure and optimize critical infrastructure. Despite significant opportunities, certain restraints such as the initial deployment costs and the need for specialized technical expertise in managing these networks may pose challenges. However, ongoing technological advancements and the growing ecosystem of service providers are actively addressing these concerns, paving the way for continued and substantial market penetration.

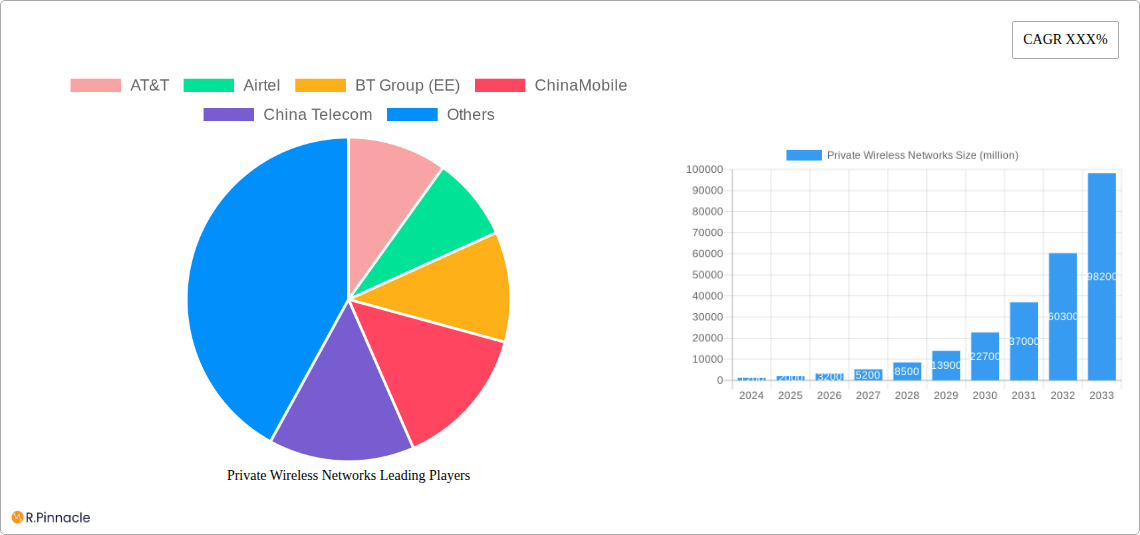

Private Wireless Networks Company Market Share

This comprehensive report provides an in-depth analysis of the private wireless networks market, a rapidly evolving sector poised for significant growth and transformation. Delve into the intricate dynamics, technological advancements, and strategic imperatives shaping the future of enterprise connectivity. With a study period spanning 2019–2033, a base year of 2025, and a forecast period from 2025–2033, this report offers unparalleled insights for industry stakeholders seeking to capitalize on the billion-dollar opportunities within this burgeoning market. We meticulously analyze market concentration, innovation drivers, regulatory frameworks, and the competitive landscape, presenting actionable intelligence for businesses across Enterprise, Industrial, and Government sectors utilizing LTE and 5G networks.

Private Wireless Networks Market Structure & Innovation Trends

The private wireless networks market exhibits a dynamic structure, characterized by both established telecommunications giants and innovative niche players. Market concentration is gradually evolving as enterprises increasingly recognize the strategic advantage of dedicated wireless infrastructure. Innovation is primarily driven by the relentless pursuit of enhanced security, reliability, and performance for critical operations. Key innovation drivers include the demand for low-latency applications in manufacturing and logistics, the need for robust connectivity in remote or challenging environments, and the integration of AI and IoT solutions. Regulatory frameworks are adapting to facilitate the deployment of private networks, with governments actively promoting spectrum allocation and policy adjustments to foster adoption. While direct product substitutes are limited, shared public networks and traditional wired solutions represent indirect competition. End-user demographics span a wide spectrum, from large industrial conglomerates to government agencies and specialized enterprise solutions. Mergers and acquisitions (M&A) activities are prevalent, with deal values in the hundreds of billions, as larger players seek to acquire specialized expertise and expand their service portfolios. Notable M&A activities have involved companies such as AT&T, Vodafone Limited, and Nokia acquiring smaller technology providers to bolster their private wireless capabilities. The overall market share distribution is shifting, with a growing portion being captured by dedicated private network providers and system integrators.

Private Wireless Networks Market Dynamics & Trends

The private wireless networks market is experiencing robust growth, propelled by a confluence of technological advancements, evolving business needs, and a strategic shift towards enhanced operational efficiency. A significant market growth driver is the escalating demand for ubiquitous, high-performance connectivity within enterprise environments, particularly in sectors like manufacturing, logistics, and public safety. These industries require the ultra-reliability and low-latency performance that private networks can consistently deliver, enabling real-time data processing, automation, and advanced robotics. Technological disruptions, such as the widespread adoption of 5G Networks, are fundamentally reshaping the market. 5G’s enhanced capabilities in terms of bandwidth, latency, and device density are unlocking new use cases and applications previously unfeasible with older wireless technologies. Consumer preferences, while indirectly influencing enterprise adoption, are increasingly oriented towards seamless, always-on connectivity, which translates into a demand for similar robust solutions within professional settings. The competitive dynamics are intensifying, with a diverse array of players, including network operators, infrastructure vendors, and specialized solutions providers, vying for market share. Key players like Ericsson, Nokia, and Huawei are investing heavily in R&D to offer comprehensive private network solutions, while Qualcomm Technologies, Inc. is instrumental in providing the underlying chipsets. The market penetration of private wireless networks is still in its nascent stages for many industries, presenting substantial headroom for future expansion. The projected Compound Annual Growth Rate (CAGR) is expected to be in the double digits, underscoring the significant growth trajectory. Furthermore, the increasing digitalization of operations across all sectors, from Smart Factories to connected cities, is acting as a powerful catalyst for private wireless network adoption. The ability of private networks to provide secure, dedicated bandwidth for mission-critical applications is a key differentiator, especially in an era of escalating cybersecurity concerns. The integration of edge computing capabilities with private wireless networks further enhances their appeal, enabling data processing closer to the source, thereby reducing latency and improving responsiveness for applications like autonomous systems and predictive maintenance. The ongoing evolution of private wireless network technologies, including advancements in spectrum management and network slicing, will continue to drive innovation and expand the addressable market.

Dominant Regions & Segments in Private Wireless Networks

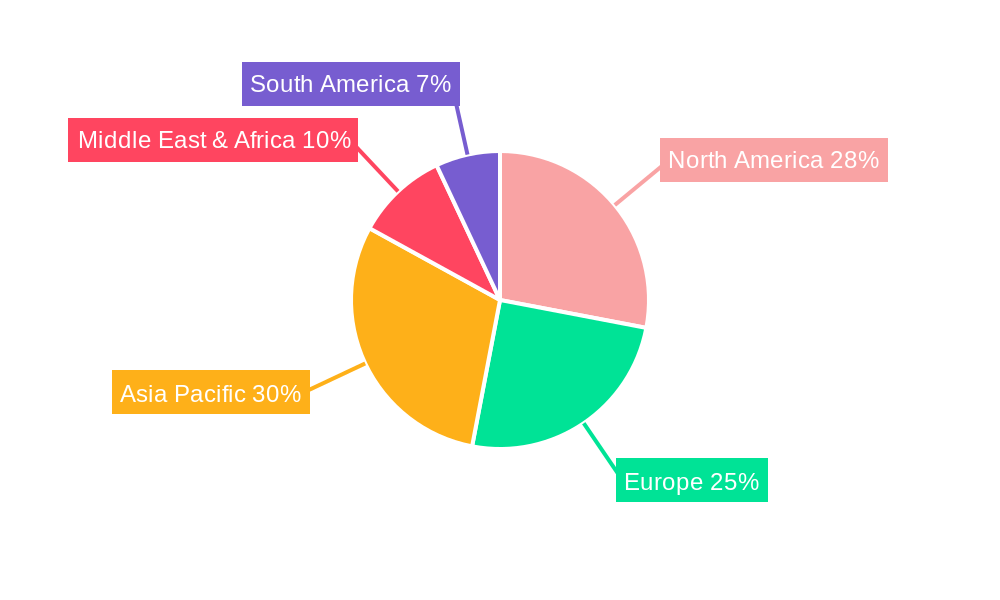

The private wireless networks market is witnessing pronounced dominance from specific regions and segments, driven by a combination of economic policies, existing infrastructure, and industry-specific demands. Asia Pacific, particularly China, is emerging as a leading region due to significant government investment in 5G infrastructure and a large industrial base actively pursuing digital transformation. The sheer scale of manufacturing and the rapid adoption of Industry 4.0 principles in countries like China, South Korea, and Japan are fueling the demand for robust private wireless solutions.

Application Dominance: The Enterprise and Industrial segments are the primary powerhouses within the private wireless networks market.

- Enterprise: This segment benefits from the growing need for secure, high-bandwidth, and low-latency connectivity for critical business operations, including enhanced mobility, real-time data analytics, and seamless collaboration. Companies are investing in private networks to improve productivity, streamline operations, and gain a competitive edge.

- Industrial: This segment is a major growth engine, driven by the adoption of Industry 4.0 technologies. Smart factories, automated warehouses, and sophisticated logistics operations rely heavily on the reliability and performance offered by private LTE and 5G networks for real-time control of machinery, autonomous guided vehicles (AGVs), and advanced sensor networks. The demand for predictable performance and enhanced safety in industrial settings makes private wireless networks an indispensable solution.

- Government: While a significant segment, its growth is often tied to specific national security initiatives, public safety deployments, and smart city projects. The robust security and dedicated spectrum capabilities of private networks are highly attractive for government applications.

Type Dominance: The transition towards 5G Networks is increasingly shaping segment dominance, although LTE Networks continue to hold significant ground.

- 5G Networks: This segment is experiencing the most rapid growth. Its superior bandwidth, ultra-low latency, and massive device connectivity capabilities are enabling transformative applications in industrial automation, private cellular broadband, and critical communications. Companies like Ericsson, Nokia, and Huawei are at the forefront of 5G private network deployments.

- LTE Networks: These continue to be a vital segment, especially for enterprises that require enhanced performance over existing Wi-Fi or cellular solutions but may not yet necessitate the full capabilities of 5G. LTE networks offer a proven, reliable, and cost-effective solution for many private network use cases, providing a solid foundation for future upgrades.

Economic policies, such as incentives for industrial digitalization and smart manufacturing initiatives, play a crucial role in driving adoption in leading regions. The availability of dedicated spectrum, either through licensing or shared access models, is another key driver. Furthermore, the presence of a well-developed telecommunications ecosystem, including experienced system integrators and solution providers like Cisco, Amdocs, and Affirmed Networks, facilitates the deployment and management of private wireless networks. The increasing complexity of industrial processes and the growing reliance on real-time data analytics further solidify the dominance of enterprise and industrial applications, powered by the most advanced wireless technologies available.

Private Wireless Networks Product Innovations

Recent product innovations in the private wireless networks market are focused on enhancing performance, security, and ease of deployment. Advancements in 5G standalone (SA) network capabilities are enabling ultra-low latency and network slicing, crucial for mission-critical industrial applications. Companies are developing integrated hardware and software solutions that simplify network management and integration with existing IT infrastructure. These innovations offer significant competitive advantages by providing enterprises with greater control, predictable performance, and robust security tailored to their specific needs, from enhanced factory automation to secure mobile workforce connectivity.

Report Scope & Segmentation Analysis

This report meticulously segments the private wireless networks market across key categories to provide granular insights.

Application Segmentation: The market is analyzed by Application, encompassing Enterprise, Industrial, Government, and Others.

- Enterprise: This segment is projected to exhibit strong growth driven by the increasing need for enhanced mobile broadband, reliable connectivity for IoT devices, and secure data transmission within corporate environments.

- Industrial: This segment is anticipated to be the largest and fastest-growing, fueled by the adoption of Industry 4.0, smart manufacturing, and automation, demanding ultra-reliable low-latency communication (URLLC) and massive machine-type communication (mMTC).

- Government: This segment will see steady growth, primarily driven by public safety initiatives, smart city deployments, and defense applications requiring secure and dedicated communication networks.

- Others: This includes segments such as healthcare, education, and transportation, which are gradually adopting private wireless solutions for specific use cases.

Type Segmentation: The market is further segmented by Type, including LTE Networks, 5G Networks, and Others.

- LTE Networks: This segment currently holds a substantial market share and will continue to be a significant contributor, offering mature and reliable solutions for various private network needs.

- 5G Networks: This segment is poised for exponential growth, driven by the superior capabilities of 5G technology, including enhanced mobile broadband (eMBB), URLLC, and mMTC, unlocking new use cases and applications.

- Others: This category comprises emerging or niche wireless technologies that may find application in specific private network scenarios.

Key Drivers of Private Wireless Networks Growth

The private wireless networks market is propelled by several critical growth drivers:

- Demand for Enhanced Connectivity: Enterprises across industries require higher bandwidth, lower latency, and greater reliability than traditional Wi-Fi or public cellular networks can consistently provide for mission-critical operations, automation, and IoT deployments.

- Industry 4.0 and Digital Transformation: The widespread adoption of Industry 4.0 principles, smart manufacturing, and the Internet of Things (IoT) necessitates robust, dedicated wireless infrastructure for real-time data exchange, machine-to-machine communication, and advanced automation.

- Security and Control: Private wireless networks offer enterprises greater control over their network infrastructure, data security, and spectrum usage, which is paramount for sensitive operations and compliance requirements.

- Technological Advancements (5G): The evolution of 5G technology, with its capabilities in ultra-low latency, massive device connectivity, and network slicing, is opening up new possibilities for private networks and driving adoption for next-generation applications.

- Economic Efficiency and Productivity: By enabling more efficient operations, automation, and real-time decision-making, private wireless networks contribute to significant improvements in productivity and cost savings for businesses.

Challenges in the Private Wireless Networks Sector

Despite its strong growth trajectory, the private wireless networks sector faces several challenges:

- Spectrum Availability and Cost: Securing suitable spectrum, whether through licensing or shared models, can be complex and costly, impacting deployment timelines and overall investment.

- Integration Complexity: Integrating private wireless networks with existing IT infrastructure and legacy systems can be technically challenging and require specialized expertise.

- Skills Gap: A shortage of skilled professionals in deploying, managing, and maintaining private wireless networks can hinder adoption and operational efficiency.

- Return on Investment (ROI) Justification: Demonstrating a clear and quantifiable ROI for private network investments can be a hurdle for some organizations, especially for smaller enterprises.

- Regulatory Uncertainty: Evolving regulatory frameworks and policies surrounding private network deployments can create uncertainty and impact long-term planning.

Emerging Opportunities in Private Wireless Networks

The private wireless networks market presents a wealth of emerging opportunities:

- Edge Computing Integration: The convergence of private wireless networks and edge computing offers immense potential for real-time data processing, AI-powered analytics, and low-latency applications, especially in industrial and IoT scenarios.

- Private 5G Network-as-a-Service (NaaS): The rise of NaaS models is making private wireless solutions more accessible and affordable for a broader range of enterprises, lowering the barrier to entry.

- Vertical-Specific Solutions: Developing tailored private network solutions for specific industry verticals, such as healthcare (remote surgery, patient monitoring) and agriculture (precision farming), presents significant growth avenues.

- Private Network Security Enhancements: The increasing focus on cybersecurity will drive demand for advanced security features and end-to-end encryption within private wireless networks.

- Hybrid Network Deployments: Exploring hybrid models that combine private networks with public 5G capabilities will offer flexibility and optimized performance for various enterprise needs.

Leading Players in the Private Wireless Networks Market

- AT&T

- Airtel

- BT Group (EE)

- ChinaMobile

- China Telecom

- Deutsche Telekom

- Qualcomm Technologies, Inc

- Ericsson

- Telstra

- Nokia

- Airspan

- Affirmed Networks

- Alibaba

- Adlink

- SuperCom(Alvarion)

- Vista

- Cisco

- Quortus

- iNet

- Amdocs

- Infrastructure Networks

- Huawei

- Altiostar

- SAMSUNG

- T-Systems International GmbH

- Vodafone Limited

- ZTE Corporation

Key Developments in Private Wireless Networks Industry

- 2024: Launch of new 5G Private Network solutions by major vendors like Ericsson and Nokia, focusing on enhanced performance and simplified deployment.

- 2023: Significant increase in M&A activity as large telcos and tech giants acquire specialized private network providers to bolster their portfolios.

- 2023: Growing adoption of Private 5G networks in industrial settings for automation and robotics, driven by performance demands.

- 2022: Increased focus on spectrum sharing models and innovative licensing frameworks to accelerate private network deployments.

- 2022: Integration of AI and ML capabilities within private network management platforms for enhanced efficiency and predictive maintenance.

- 2021: Expansion of Private LTE network deployments in enterprise environments, offering a robust and secure alternative to Wi-Fi.

- 2020: Growing interest in private wireless networks for critical infrastructure and public safety applications.

- 2019: Initial advancements and trials in private 5G network technology, laying the groundwork for future widespread adoption.

Future Outlook for Private Wireless Networks Market

The private wireless networks market is poised for substantial expansion in the coming years, driven by relentless technological innovation and the evolving digital transformation needs of businesses worldwide. The continued maturation of 5G technology, coupled with advancements in edge computing, will unlock a new wave of sophisticated applications and services, further cementing the value proposition of dedicated wireless infrastructure. Strategic opportunities lie in catering to niche industry requirements with vertical-specific solutions and in developing more accessible, service-oriented deployment models like Private 5G NaaS. The growing emphasis on cybersecurity and operational resilience will continue to favor the inherent advantages of private networks, positioning them as a critical component of future enterprise IT strategies. The market is expected to witness sustained investment and innovation, leading to increased adoption and a profound impact on how businesses operate and compete.

Private Wireless Networks Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Industrial

- 1.3. Government

- 1.4. Others

-

2. Type

- 2.1. LTE Networks

- 2.2. 5G Networks

- 2.3. Others

Private Wireless Networks Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Private Wireless Networks Regional Market Share

Geographic Coverage of Private Wireless Networks

Private Wireless Networks REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 35.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Industrial

- 5.1.3. Government

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. LTE Networks

- 5.2.2. 5G Networks

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Industrial

- 6.1.3. Government

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. LTE Networks

- 6.2.2. 5G Networks

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Industrial

- 7.1.3. Government

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. LTE Networks

- 7.2.2. 5G Networks

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Industrial

- 8.1.3. Government

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. LTE Networks

- 8.2.2. 5G Networks

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Industrial

- 9.1.3. Government

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. LTE Networks

- 9.2.2. 5G Networks

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Private Wireless Networks Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Industrial

- 10.1.3. Government

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. LTE Networks

- 10.2.2. 5G Networks

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AT&T

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Airtel

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BT Group (EE)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ChinaMobile

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 China Telecom

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Deutsche Telekom

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Qualcomm Technologies Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ericsson

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Telstra

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Nokia

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Airspan

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Affirmed Networks

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Alibaba

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Adlink

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 SuperCom(Alvarion)

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Vista

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Cisco

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Quortus

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 iNet

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Amdocs

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Infrastructure Networks

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Huawei

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Altiostar

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 SAMSUNG

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 T-Systems International GmbH

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Vodafone Limited

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 ZTE Corporation

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.1 AT&T

List of Figures

- Figure 1: Global Private Wireless Networks Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Private Wireless Networks Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Private Wireless Networks Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Private Wireless Networks Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Private Wireless Networks Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Private Wireless Networks Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Private Wireless Networks Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Private Wireless Networks Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Private Wireless Networks Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Private Wireless Networks Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Private Wireless Networks Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Private Wireless Networks Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Private Wireless Networks Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Private Wireless Networks Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Private Wireless Networks Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Private Wireless Networks Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Private Wireless Networks Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Private Wireless Networks Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Private Wireless Networks Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Private Wireless Networks Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Private Wireless Networks Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Private Wireless Networks Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Private Wireless Networks Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Private Wireless Networks Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Private Wireless Networks Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Private Wireless Networks Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Private Wireless Networks Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Private Wireless Networks Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Private Wireless Networks Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Private Wireless Networks Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Private Wireless Networks Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Private Wireless Networks Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Private Wireless Networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Private Wireless Networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Private Wireless Networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Private Wireless Networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Private Wireless Networks Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Private Wireless Networks Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Private Wireless Networks Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Private Wireless Networks Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Private Wireless Networks?

The projected CAGR is approximately 35.4%.

2. Which companies are prominent players in the Private Wireless Networks?

Key companies in the market include AT&T, Airtel, BT Group (EE), ChinaMobile, China Telecom, Deutsche Telekom, Qualcomm Technologies, Inc, Ericsson, Telstra, Nokia, Airspan, Affirmed Networks, Alibaba, Adlink, SuperCom(Alvarion), Vista, Cisco, Quortus, iNet, Amdocs, Infrastructure Networks, Huawei, Altiostar, SAMSUNG, T-Systems International GmbH, Vodafone Limited, ZTE Corporation.

3. What are the main segments of the Private Wireless Networks?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Private Wireless Networks," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Private Wireless Networks report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Private Wireless Networks?

To stay informed about further developments, trends, and reports in the Private Wireless Networks, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence