Key Insights

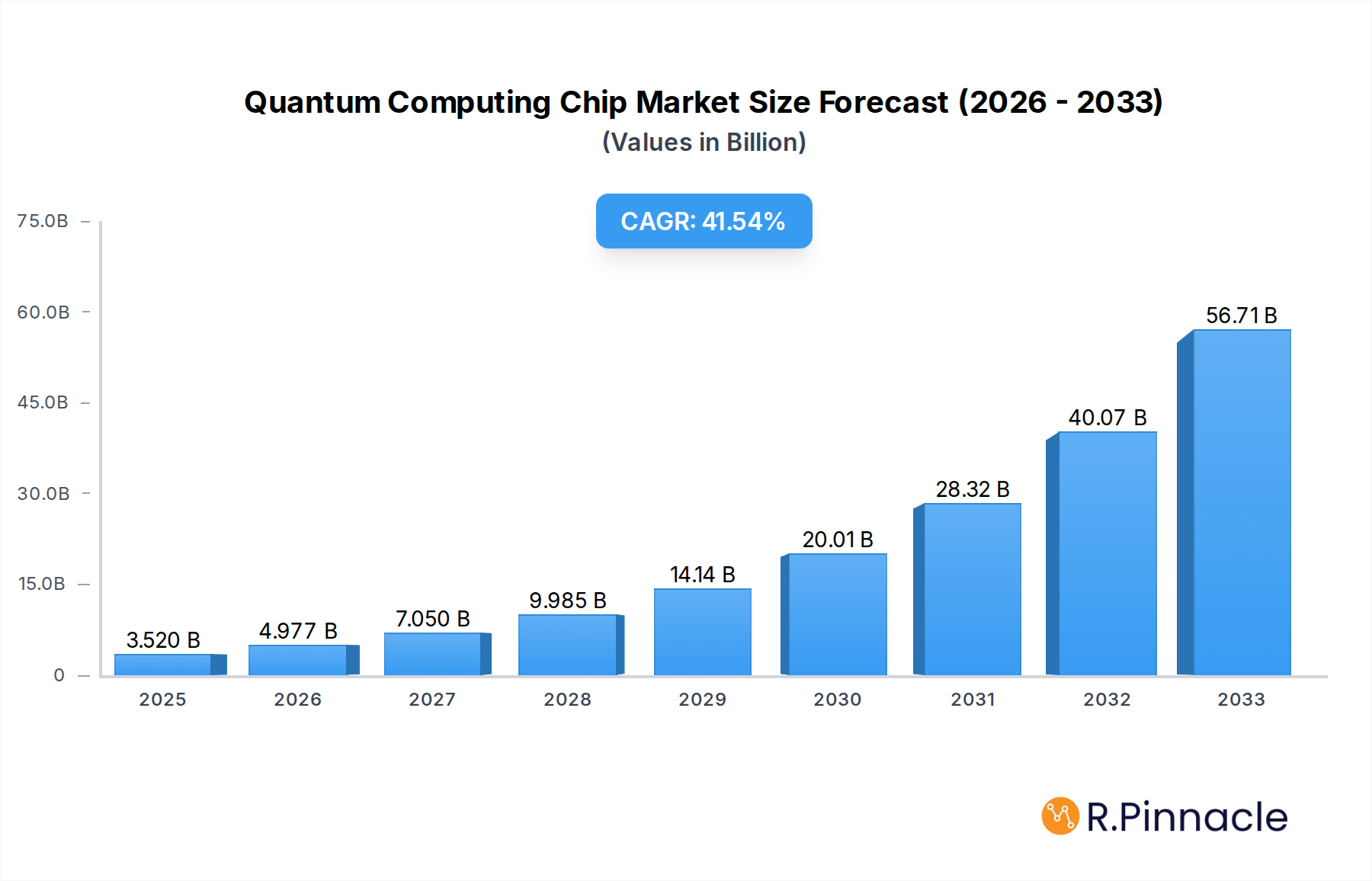

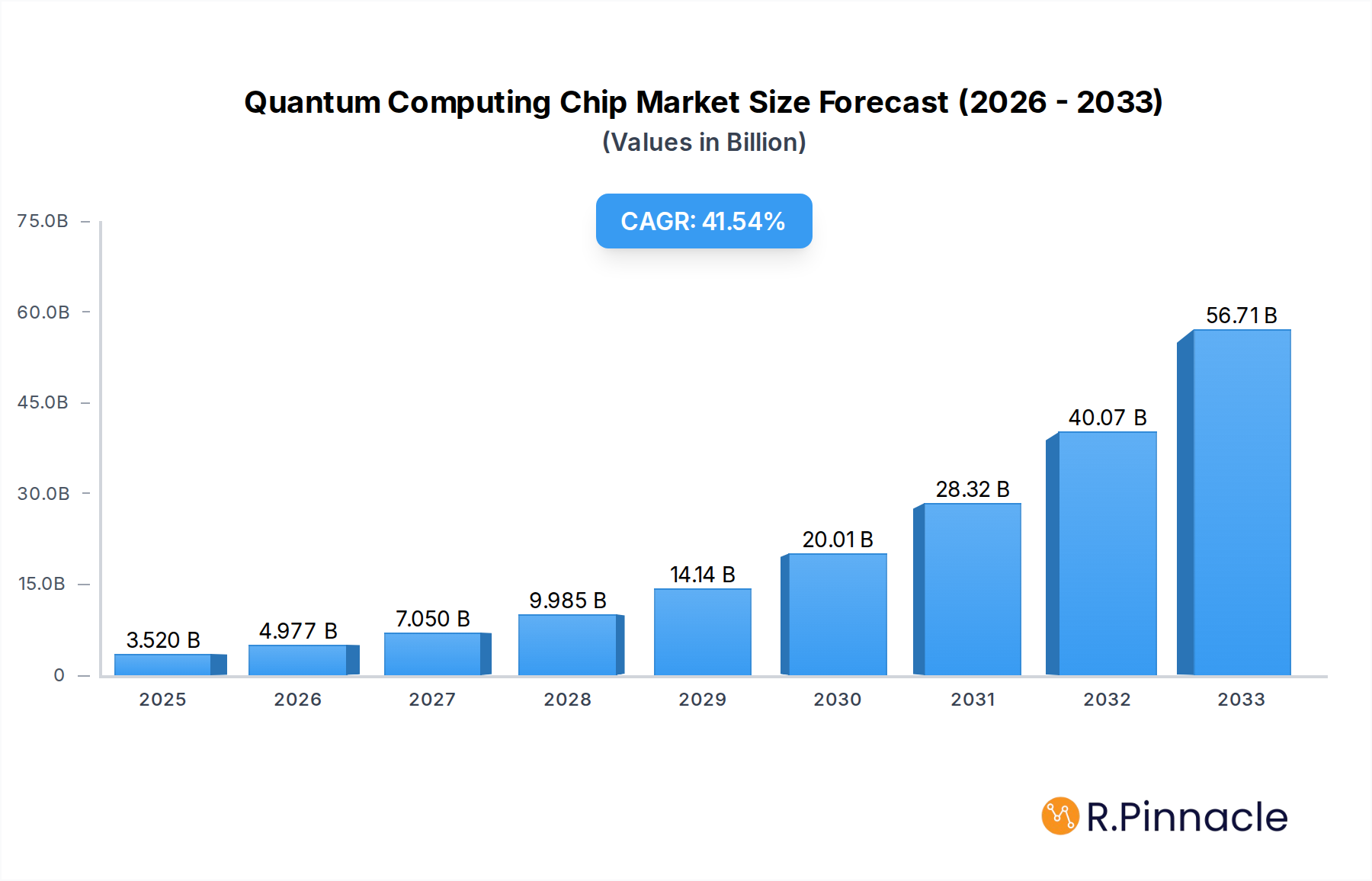

The global Quantum Computing Chip market is poised for explosive growth, projected to reach USD 3.52 billion in 2025, driven by an unprecedented Compound Annual Growth Rate (CAGR) of 41.8% through 2033. This remarkable expansion is fueled by significant advancements in qubit technology, a burgeoning demand for high-performance computing solutions in complex problem-solving, and substantial investments from both government bodies and private enterprises. The increasing sophistication of quantum processors, moving towards larger qubit counts and improved coherence times, is fundamentally reshaping industries. Applications ranging from drug discovery and materials science to financial modeling and artificial intelligence are being revolutionized by the potential of quantum computing. The market is experiencing a robust surge in research and development, with key players continually innovating to create more stable and scalable quantum hardware.

Quantum Computing Chip Market Size (In Billion)

The quantum computing chip landscape is characterized by intense innovation across various chip types, with superconducting and photonic chips currently leading the charge, complemented by emerging topological chip designs. The market is segmented by qubit count, with a significant focus on the development of computers with between 30-50 and 50-60 qubits, as these represent critical milestones for achieving quantum advantage in numerous applications. The United States, China, and Europe are at the forefront of this technological revolution, investing heavily in research infrastructure and fostering a competitive ecosystem. While the immense potential of quantum computing is clear, challenges such as high manufacturing costs, the need for specialized infrastructure, and the scarcity of skilled quantum engineers are moderating factors. However, the overwhelming trend points towards accelerated adoption and a transformative impact across a wide spectrum of scientific and industrial domains.

Quantum Computing Chip Company Market Share

Quantum Computing Chip Market: Global Outlook and Strategic Insights (2019-2033)

This comprehensive report offers an in-depth analysis of the global Quantum Computing Chip market, a rapidly evolving sector poised for transformative growth. Delving into market structure, dynamics, regional dominance, and future potential, this report is an indispensable resource for industry professionals, investors, and strategists seeking to navigate the complex landscape of quantum technology. With a study period spanning 2019 to 2033, a base year of 2025, and a forecast period of 2025-2033, this report provides robust data-driven insights for strategic decision-making.

Quantum Computing Chip Market Structure & Innovation Trends

The Quantum Computing Chip market is characterized by a dynamic and consolidating structure, driven by intense innovation from leading technology giants and ambitious startups. Major players like IBM, Google, Microsoft, Intel, D-Wave, Rigetti Computing, Fujitsu, Xanadu, Origin Quantum Computing Technology, and IonQ are at the forefront of research and development, pushing the boundaries of qubit stability and scalability. Market concentration is increasing as significant M&A activities are observed, with deal values projected to reach hundreds of billions in the coming years. For instance, acquisitions of promising quantum computing startups by established tech firms are strategically aimed at securing intellectual property and talent. Innovation is primarily fueled by the pursuit of fault-tolerant quantum computers, with ongoing advancements in superconducting, topological, and photonic chip architectures. Regulatory frameworks, while still nascent, are beginning to address quantum security and ethical considerations, influencing research priorities and market entry strategies. Product substitutes for classical computing are gradually being displaced by the unique capabilities of quantum processors for specific complex problems. End-user demographics are shifting from academic research to enterprise adoption across finance, pharmaceuticals, and materials science, indicating a broadening market appeal.

Quantum Computing Chip Market Dynamics & Trends

The Quantum Computing Chip market is experiencing a period of accelerated growth, driven by a confluence of technological breakthroughs, burgeoning investment, and an expanding ecosystem of research and development. The projected Compound Annual Growth Rate (CAGR) is estimated to be in the triple digits, reflecting the nascent but explosive nature of this sector. Market penetration, currently low, is expected to surge as quantum hardware becomes more accessible and application development matures. Key growth drivers include the increasing demand for computational power to solve problems intractable for classical computers, such as drug discovery, materials design, financial modeling, and complex optimization challenges. Technological disruptions are constant, with rapid advancements in qubit coherence times, error correction techniques, and chip architectures. Consumer preferences, evolving from a basic understanding of quantum potential to specific demands for quantum advantage in particular domains, are shaping product development. Competitive dynamics are characterized by intense R&D investment, strategic partnerships, and a race to achieve quantum supremacy for commercially viable applications. The increasing availability of quantum cloud platforms is democratizing access, further stimulating market expansion. The development of quantum algorithms and software is crucial for unlocking the full potential of these advanced chips, leading to a synergistic growth in both hardware and software segments. The global R&D expenditure on quantum computing is projected to exceed tens of billions annually by the end of the forecast period, underscoring the significant investment fueling market expansion.

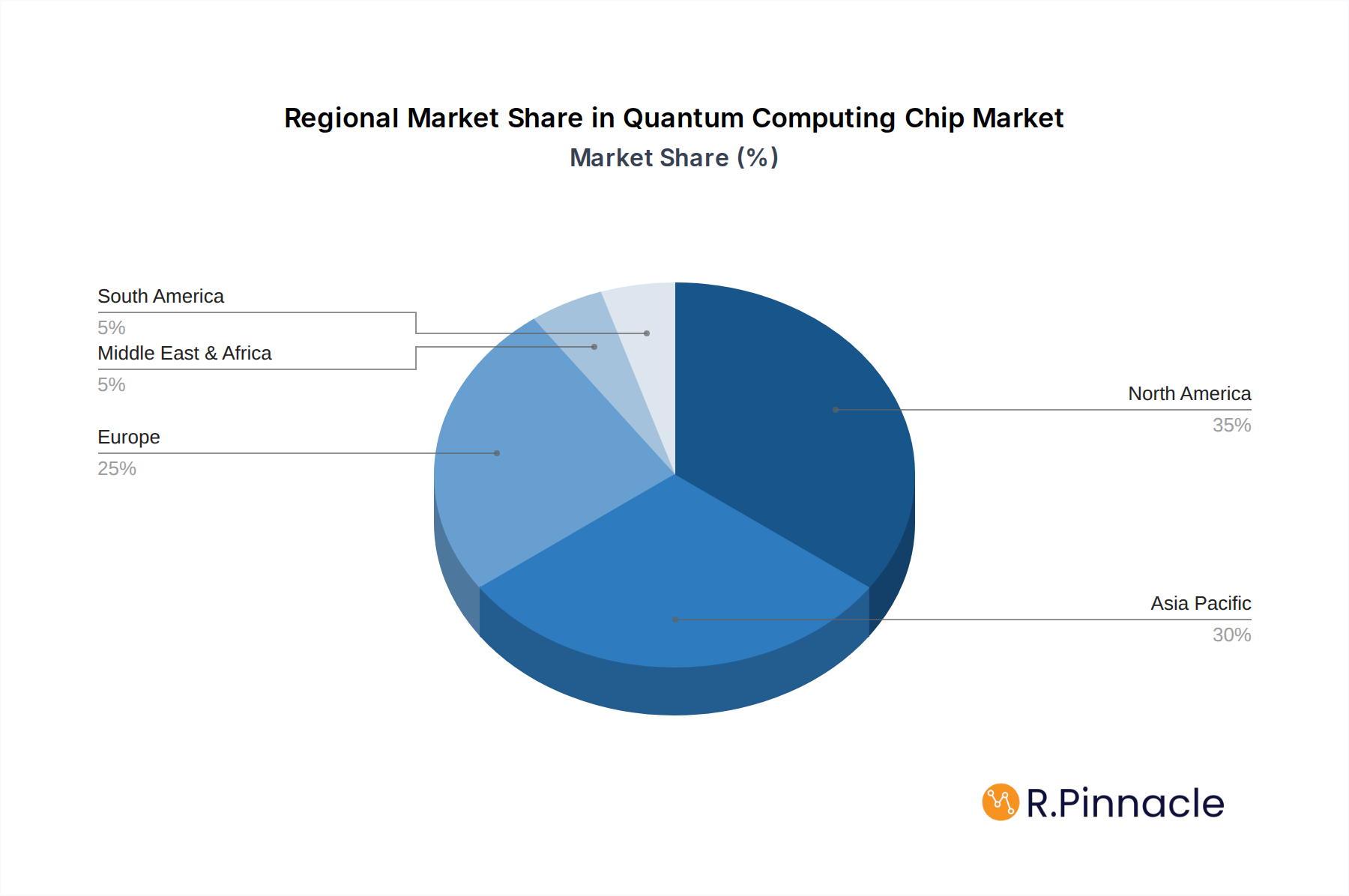

Dominant Regions & Segments in Quantum Computing Chip

North America, particularly the United States, currently dominates the Quantum Computing Chip market, propelled by robust government funding, leading research institutions, and a concentrated presence of major technology companies like IBM, Google, and Microsoft. Economic policies supportive of advanced technology research and development, coupled with significant private sector investment exceeding hundreds of billions, create a fertile ground for quantum innovation. The region's strong academic-industrial collaboration fosters rapid prototyping and commercialization of quantum technologies.

Within the Application segment, Above Qubit Quantum Computer systems represent the leading edge, attracting substantial investment and driving innovation, although Below 30 Qubit Quantum Computer and 30-50 Qubit Quantum Computer systems are gaining traction for specific, niche applications and research purposes. The 50-60 Qubit Quantum Computer segment is an emerging area of intense focus for achieving greater computational power.

In terms of Chip Types, Superconducting Chip technology currently holds a dominant position due to its relative maturity and the established expertise of key players like IBM and Google. However, Photonic Chip technology is rapidly gaining ground, driven by companies like Xanadu, promising scalability and room-temperature operation. Topological Chip technology, while still in its nascent stages, holds significant promise for robust quantum computation with companies like Microsoft investing heavily in its development. The exploration of Others such as trapped-ion and neutral-atom platforms by companies like IonQ and Rigetti Computing are also contributing to the diversification and advancement of quantum chip architectures.

Key drivers for regional dominance include significant venture capital funding, estimated to be in the billions, dedicated national quantum initiatives, and a highly skilled workforce. Infrastructure development, including specialized fabrication facilities and high-performance computing centers, further solidifies leadership positions.

Quantum Computing Chip Product Innovations

Product innovation in the Quantum Computing Chip market is rapidly advancing, focusing on increasing qubit count, improving qubit coherence, and developing error correction mechanisms. Companies are introducing more powerful quantum processors with enhanced connectivity and reduced noise levels. Applications are expanding from theoretical research to practical use cases in materials science, drug discovery, and financial modeling, promising to deliver quantum advantage. Competitive advantages are being built on superior qubit quality, scalable architectures, and integrated software stacks that simplify programming and application development, leading to a projected market value exceeding hundreds of billions.

Report Scope & Segmentation Analysis

This report meticulously segments the Quantum Computing Chip market across key parameters to provide granular insights. The Application segmentation includes Below 30 Qubit Quantum Computer, 30-50 Qubit Quantum Computer, 50-60 Qubit Quantum Computer, and Above Qubit Quantum Computer. The Types segmentation covers Superconducting Chip, Topological Chip, Photonic Chip, and Others. Each segment is analyzed for its projected growth, estimated market size in billions, and competitive dynamics. For instance, the Above Qubit Quantum Computer segment, though currently niche, is projected to witness the highest growth rate, with its market size expected to reach hundreds of billions within the forecast period, driven by intensive R&D and a growing demand for complex problem-solving.

Key Drivers of Quantum Computing Chip Growth

The Quantum Computing Chip market is propelled by several interconnected growth drivers. Technologically, breakthroughs in qubit stability, entanglement, and error correction are fundamental. Economically, substantial government funding, projected to be in the billions globally, and increasing private sector investment are fueling R&D and infrastructure development. Regulatory factors, while still evolving, are increasingly recognizing the strategic importance of quantum computing, leading to supportive policies and initiatives. The escalating demand for solving complex computational problems in fields like pharmaceuticals, finance, and artificial intelligence, where classical computing falls short, is a primary market pull. Furthermore, the development of quantum algorithms and the emergence of quantum-ready talent are critical accelerators for market adoption and growth.

Challenges in the Quantum Computing Chip Sector

Despite its immense potential, the Quantum Computing Chip sector faces significant challenges. Key barriers include the inherent instability of qubits, leading to high error rates and short coherence times, necessitating complex and costly error correction mechanisms. Supply chain issues for specialized materials and fabrication processes are also a constraint, potentially impacting production scalability and cost-effectiveness. Intense competitive pressures and the high cost of R&D and manufacturing, requiring billions in investment, pose significant financial hurdles. Regulatory uncertainty surrounding intellectual property, national security implications, and ethical considerations can also create hesitancy for widespread adoption and investment. Furthermore, the lack of a standardized quantum programming language and the need for specialized expertise create a talent gap.

Emerging Opportunities in Quantum Computing Chip

The Quantum Computing Chip market presents numerous emerging opportunities driven by continuous innovation and the exploration of new frontiers. The development of hybrid quantum-classical computing approaches offers immediate avenues for leveraging existing infrastructure while benefiting from quantum acceleration for specific tasks. Opportunities lie in developing specialized quantum processors tailored for niche applications in drug discovery, materials science, and financial risk analysis, where early quantum advantage can be demonstrated. The growth of quantum cloud platforms is creating new revenue streams and expanding market access. Furthermore, the burgeoning field of quantum cryptography and secure communication presents a significant long-term opportunity. The establishment of quantum computing as a service (QCaaS) model is also opening doors for broader industry adoption and innovation.

Leading Players in the Quantum Computing Chip Market

- IBM

- Microsoft

- Intel

- D-Wave

- Rigetti Computing

- Fujitsu

- Xanadu

- Origin Quantum Computing Technology

- IonQ

Key Developments in Quantum Computing Chip Industry

- 2024: IBM announces the development of a new superconducting quantum processor with an increased number of qubits, pushing the boundaries of quantum computation for complex simulations.

- 2023: Google showcases advancements in its quantum AI research, demonstrating potential applications in materials science and optimization problems.

- 2023: Microsoft continues its focus on topological qubits, reporting progress in achieving stable qubit states for error-resilient quantum computing.

- 2022: IonQ introduces a new trapped-ion quantum computer with enhanced performance metrics and accessibility through cloud platforms.

- 2022: Xanadu unveils a photonic quantum computer designed for scalability and integration with existing fiber optic infrastructure.

- 2021: Rigetti Computing announces plans for next-generation superconducting quantum processors, emphasizing increased qubit connectivity and reduced noise.

- 2020: D-Wave Systems launches its latest quantum annealing system, focusing on solving complex optimization problems for industries like logistics and finance.

- 2019: Fujitsu reports significant progress in developing superconducting quantum computing technology, aiming for practical applications in various sectors.

- 2019: Origin Quantum Computing Technology showcases its advancements in indigenous quantum computing hardware and software development.

Future Outlook for Quantum Computing Chip Market

The future outlook for the Quantum Computing Chip market is exceptionally promising, driven by sustained technological advancements and increasing market adoption. The continued scaling of qubit counts, coupled with significant improvements in qubit quality and error correction, will unlock the potential for fault-tolerant quantum computers. Strategic partnerships between hardware providers, software developers, and end-users will accelerate the development and deployment of quantum solutions across diverse industries, with market value expected to reach hundreds of billions. The expansion of quantum cloud services will democratize access, fostering a broader ecosystem of innovation. Emerging opportunities in quantum machine learning, drug discovery, and advanced materials design are poised to redefine scientific and industrial capabilities, solidifying quantum computing's role as a transformative technology.

Quantum Computing Chip Segmentation

-

1. Application

- 1.1. Below 30 Qubit Quantum Computer

- 1.2. 30-50 Qubit Quantum Computer

- 1.3. 50-60 Qubit Quantum Computer

- 1.4. Above Qubit Quantum Computer

-

2. Types

- 2.1. Superconducting Chip

- 2.2. Topological Chip

- 2.3. Photonic Chip

- 2.4. Others

Quantum Computing Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Quantum Computing Chip Regional Market Share

Geographic Coverage of Quantum Computing Chip

Quantum Computing Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 41.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Below 30 Qubit Quantum Computer

- 5.1.2. 30-50 Qubit Quantum Computer

- 5.1.3. 50-60 Qubit Quantum Computer

- 5.1.4. Above Qubit Quantum Computer

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Superconducting Chip

- 5.2.2. Topological Chip

- 5.2.3. Photonic Chip

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Below 30 Qubit Quantum Computer

- 6.1.2. 30-50 Qubit Quantum Computer

- 6.1.3. 50-60 Qubit Quantum Computer

- 6.1.4. Above Qubit Quantum Computer

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Superconducting Chip

- 6.2.2. Topological Chip

- 6.2.3. Photonic Chip

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Below 30 Qubit Quantum Computer

- 7.1.2. 30-50 Qubit Quantum Computer

- 7.1.3. 50-60 Qubit Quantum Computer

- 7.1.4. Above Qubit Quantum Computer

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Superconducting Chip

- 7.2.2. Topological Chip

- 7.2.3. Photonic Chip

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Below 30 Qubit Quantum Computer

- 8.1.2. 30-50 Qubit Quantum Computer

- 8.1.3. 50-60 Qubit Quantum Computer

- 8.1.4. Above Qubit Quantum Computer

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Superconducting Chip

- 8.2.2. Topological Chip

- 8.2.3. Photonic Chip

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Below 30 Qubit Quantum Computer

- 9.1.2. 30-50 Qubit Quantum Computer

- 9.1.3. 50-60 Qubit Quantum Computer

- 9.1.4. Above Qubit Quantum Computer

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Superconducting Chip

- 9.2.2. Topological Chip

- 9.2.3. Photonic Chip

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Quantum Computing Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Below 30 Qubit Quantum Computer

- 10.1.2. 30-50 Qubit Quantum Computer

- 10.1.3. 50-60 Qubit Quantum Computer

- 10.1.4. Above Qubit Quantum Computer

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Superconducting Chip

- 10.2.2. Topological Chip

- 10.2.3. Photonic Chip

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 IBM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Google

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Microsoft

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Intel

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 D-Wave

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Rigetti Computing

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Fujitsu

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Xanadu

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Origin Quantum Computing Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ion Q

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 IBM

List of Figures

- Figure 1: Global Quantum Computing Chip Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Quantum Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Quantum Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Quantum Computing Chip Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Quantum Computing Chip Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Quantum Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Quantum Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Quantum Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Quantum Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Quantum Computing Chip Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Quantum Computing Chip Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Quantum Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Quantum Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Quantum Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Quantum Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Quantum Computing Chip Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Quantum Computing Chip Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Quantum Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Quantum Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Quantum Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Quantum Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Quantum Computing Chip Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Quantum Computing Chip Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Quantum Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Quantum Computing Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Quantum Computing Chip Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Quantum Computing Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Quantum Computing Chip Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Quantum Computing Chip Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Quantum Computing Chip Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Quantum Computing Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Quantum Computing Chip Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Quantum Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Quantum Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Quantum Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Quantum Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Quantum Computing Chip Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Quantum Computing Chip Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Quantum Computing Chip Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Quantum Computing Chip Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Quantum Computing Chip?

The projected CAGR is approximately 41.8%.

2. Which companies are prominent players in the Quantum Computing Chip?

Key companies in the market include IBM, Google, Microsoft, Intel, D-Wave, Rigetti Computing, Fujitsu, Xanadu, Origin Quantum Computing Technology, Ion Q.

3. What are the main segments of the Quantum Computing Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.52 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Quantum Computing Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Quantum Computing Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Quantum Computing Chip?

To stay informed about further developments, trends, and reports in the Quantum Computing Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence