Key Insights

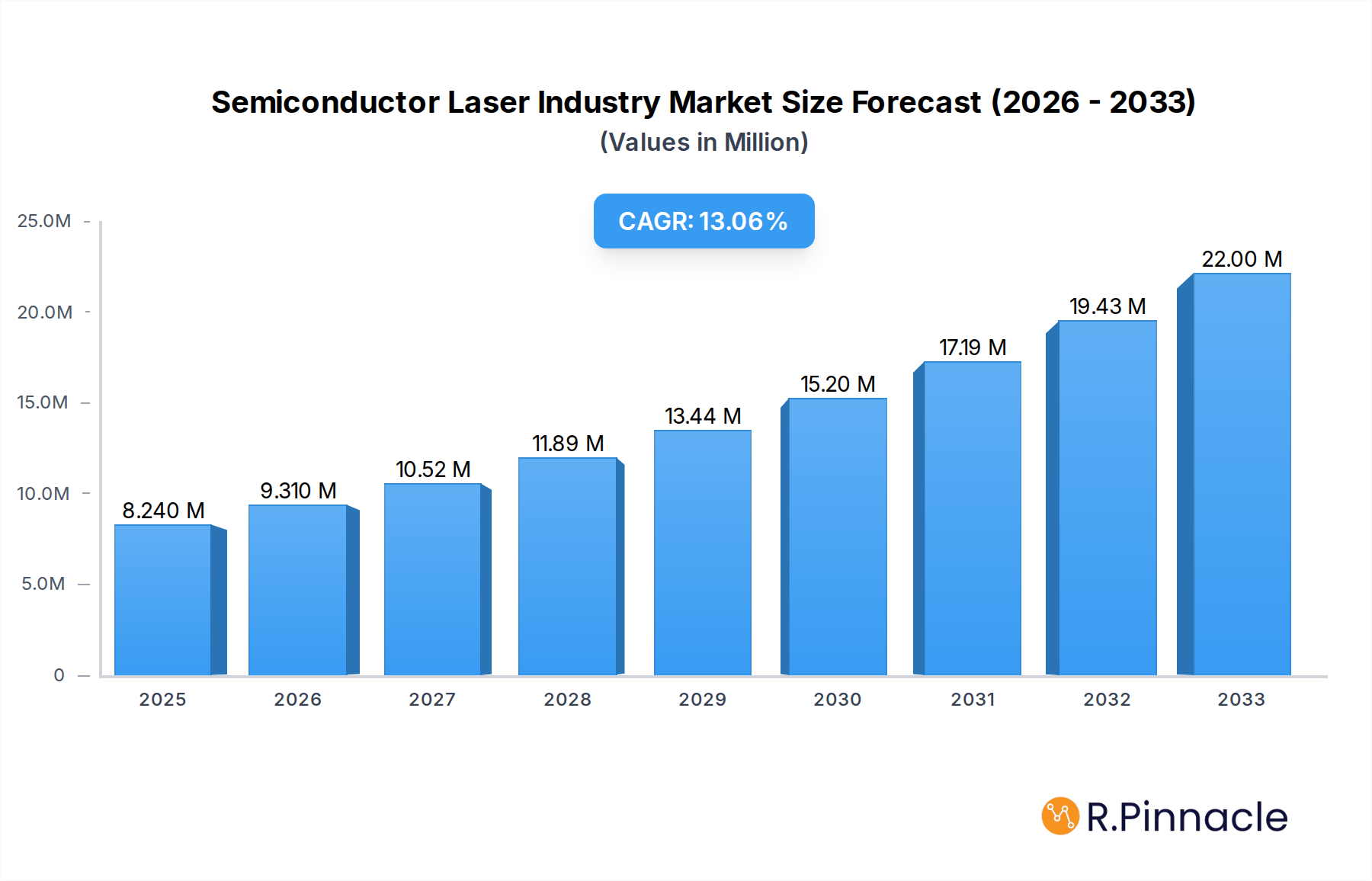

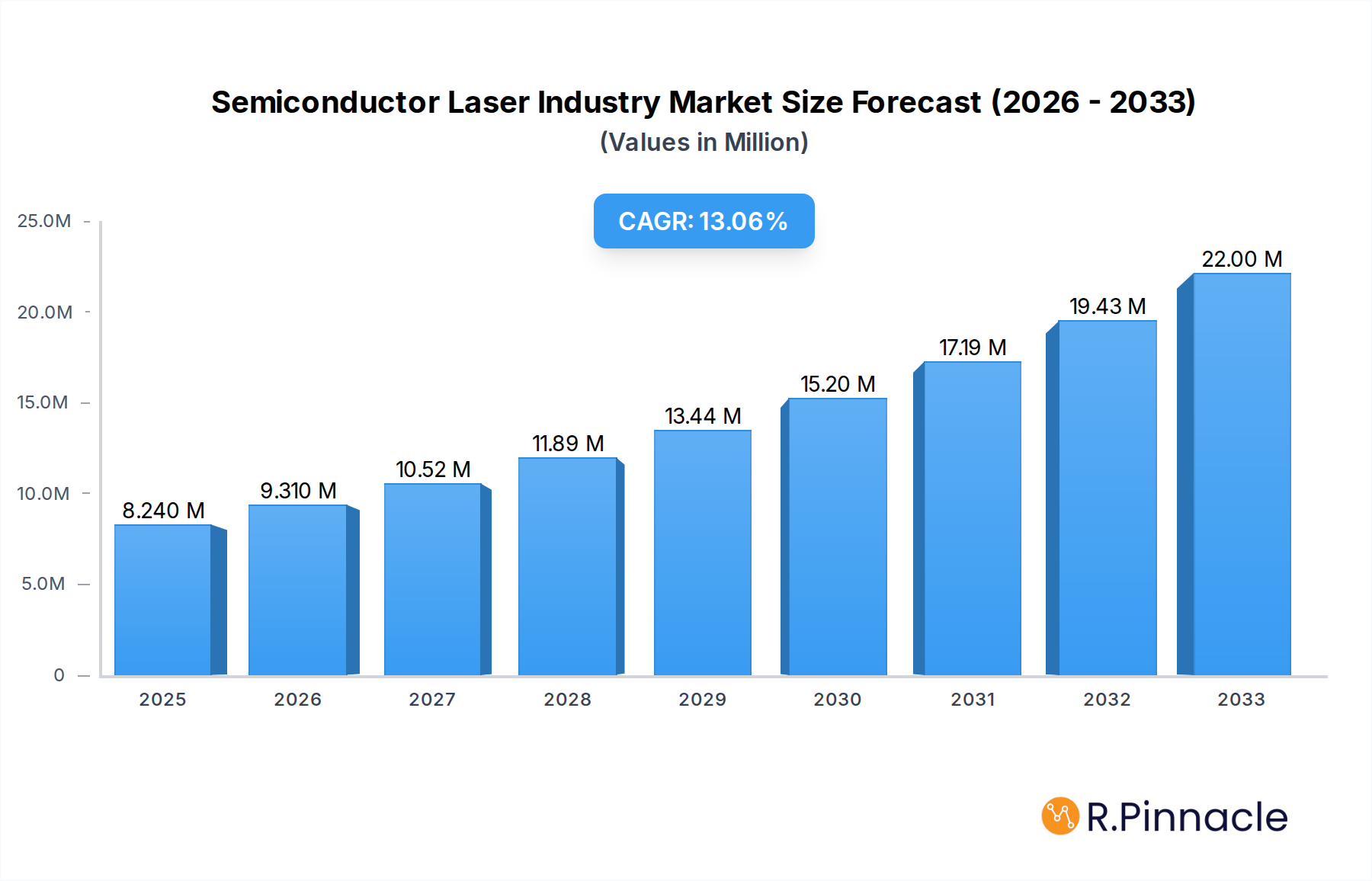

The global Semiconductor Laser Industry is poised for substantial growth, projected to reach $8.24 Million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 13.40% during the forecast period of 2025-2033. This robust expansion is fueled by a confluence of dynamic drivers, including the escalating demand for high-speed data transmission in communication networks, the rapid advancements in medical laser technologies for minimally invasive procedures and diagnostics, and the increasing integration of laser systems in sophisticated industrial automation and manufacturing processes. The automotive sector's adoption of lidar for autonomous driving and advanced driver-assistance systems (ADAS) is also a significant contributor. Emerging trends such as the development of more energy-efficient and compact semiconductor lasers, the expansion of quantum cascade lasers for specialized applications like gas sensing, and the growing use of ultraviolet (UV) lasers in sterilization and additive manufacturing are further accelerating market penetration. The industry is characterized by innovation across various laser types, including Edge-Emitting Lasers (EELs), Vertical-Cavity Surface-Emitting Lasers (VCSELs), and Fiber Lasers, catering to diverse application needs.

Semiconductor Laser Industry Market Size (In Million)

Despite the optimistic outlook, certain restraints could influence the pace of growth. These include the high initial investment costs associated with advanced laser manufacturing and R&D, stringent regulatory compliance for medical and defense applications, and the ongoing challenge of developing lasers with even higher power outputs and greater wavelength precision for specialized scientific and industrial purposes. Geographically, the market is expected to see strong performance across North America and Europe due to significant R&D investments and advanced technological adoption. Asia, however, is anticipated to emerge as a dominant force, driven by its expanding manufacturing capabilities, burgeoning telecommunications infrastructure, and increasing healthcare expenditure, making it a crucial region for market expansion and innovation. The interplay between these drivers, trends, and restraints will shape the competitive landscape, with key players like Coherent Inc., Lumentum Holdings Inc., and IPG Photonics Corporation actively investing in new product development and strategic collaborations to maintain their market leadership.

Semiconductor Laser Industry Company Market Share

Semiconductor Laser Industry Market Report: Forecast to 2033

This comprehensive report offers an in-depth analysis of the global Semiconductor Laser Industry, providing actionable insights and strategic intelligence for stakeholders. Leveraging extensive historical data from 2019–2024 and robust market forecasts up to 2033, this study details market size, growth drivers, challenges, and emerging opportunities. With a base year of 2025 and an estimated year also of 2025, the forecast period spans 2025–2033. This report is essential for understanding the evolving landscape of semiconductor laser technology and its impact across diverse applications.

Semiconductor Laser Industry Market Structure & Innovation Trends

The Semiconductor Laser Industry exhibits a moderate to high market concentration, with key players like Coherent Inc., IPG Photonics Corporation, and ams OSRAM AG holding significant market share, estimated at over 20% combined for the top three entities. Innovation is primarily driven by advancements in material science, epitaxy techniques, and device architectures such as VCSELs and advanced EELs. The integration of AI in laser design and manufacturing is also a notable trend. Regulatory frameworks are evolving, particularly concerning export controls and environmental standards for manufacturing. Product substitutes exist in some niche applications, such as solid-state lasers for certain industrial tasks, but semiconductor lasers maintain a distinct advantage in terms of efficiency, size, and cost-effectiveness for high-volume applications. End-user demographics are increasingly shifting towards telecommunications and consumer electronics, driving demand for high-performance, miniaturized laser components. Merger and acquisition (M&A) activities are prevalent, with significant deal values in the hundreds of millions to low billions of dollars, aimed at consolidating market positions, acquiring new technologies, and expanding geographical reach. For instance, M&A deals worth approximately $1.5 Billion were recorded in the historical period.

Semiconductor Laser Industry Market Dynamics & Trends

The Semiconductor Laser Industry is poised for significant growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 8.5% over the forecast period (2025–2033). This expansion is fueled by a confluence of powerful market growth drivers. The insatiable demand for high-speed data transmission in telecommunications, driven by the proliferation of 5G networks, cloud computing, and the Internet of Things (IoT), is a primary catalyst. Semiconductor lasers, particularly those operating in the infrared spectrum, are indispensable for optical communication infrastructure. Technological disruptions, such as the increasing adoption of VCSELs in short-range communication and sensing applications, are further reshaping the market. These surface-emitting lasers offer cost advantages, ease of integration, and improved performance for applications like facial recognition, LiDAR, and virtual reality. Consumer preferences are increasingly dictating market trends, with a growing demand for smaller, more energy-efficient, and cost-effective laser solutions in consumer electronics, healthcare, and automotive sectors. The miniaturization of devices and the need for precise sensing capabilities are pushing innovation in semiconductor laser technology. Competitive dynamics within the industry are intense, characterized by continuous R&D investment, strategic partnerships, and a race to develop next-generation laser devices. Companies are actively investing in advanced manufacturing processes to improve yield, reduce costs, and enhance performance. Market penetration for semiconductor lasers is expanding rapidly across traditional and emerging application areas. The automotive sector, for example, is witnessing a surge in demand for LiDAR systems for autonomous driving, which heavily rely on semiconductor lasers. Similarly, the medical industry is adopting semiconductor lasers for minimally invasive surgery, diagnostics, and therapeutic applications. The drive towards Industry 4.0, with its emphasis on automation and smart manufacturing, further bolsters the demand for industrial lasers in applications like welding, cutting, and marking. This sustained demand, coupled with ongoing technological advancements, positions the semiconductor laser market for robust and sustained growth.

Dominant Regions & Segments in Semiconductor Laser Industry

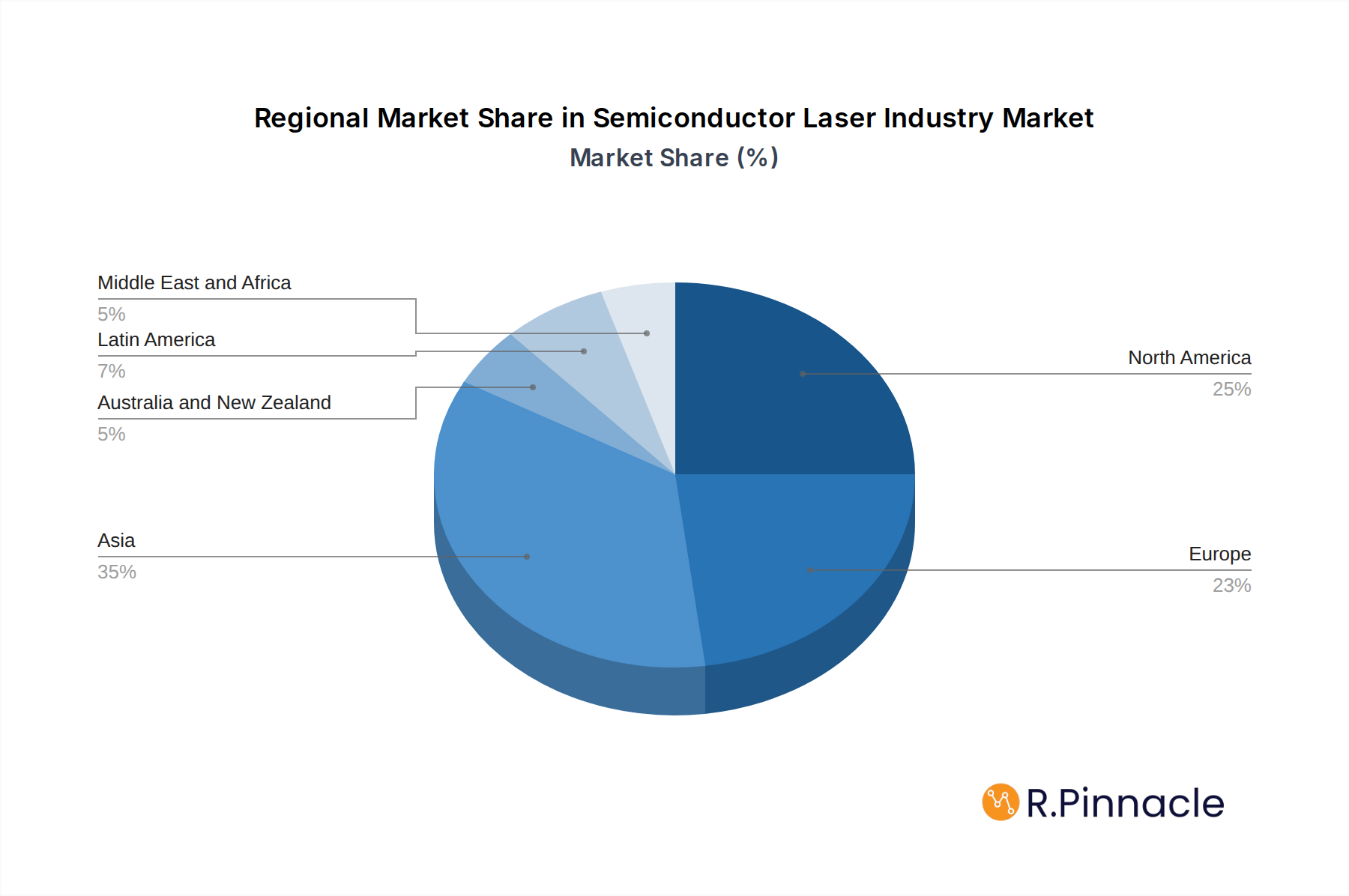

The Asia Pacific region is the dominant force in the Semiconductor Laser Industry, accounting for an estimated 45% of the global market share. This dominance is propelled by robust manufacturing capabilities, significant government investments in research and development, and the presence of major end-user industries, particularly in telecommunications and consumer electronics. China, in particular, plays a pivotal role due to its extensive semiconductor manufacturing infrastructure and the rapid expansion of its digital economy.

Within the Segments, the Infrared Lasers wavelength segment is leading the market, driven by their critical role in telecommunications, industrial applications, and emerging areas like LiDAR. The projected market size for infrared lasers is expected to reach over $12 Billion by 2033.

In terms of Type, EEL (Edge-emitting Laser) technology continues to hold a substantial market share, benefiting from its established applications in optical communications and industrial processes. However, VCSEL (Vertical-cavity Surface-emitting Laser) technology is experiencing the fastest growth, projected at a CAGR of over 10% due to its expanding applications in sensing, consumer electronics, and automotive LiDAR. The market for VCSELs is estimated to reach approximately $4 Billion by 2033.

The Application segment of Communication remains the largest contributor to the Semiconductor Laser Industry's revenue, accounting for over 30% of the market. The ongoing deployment of fiber optic networks and the demand for higher bandwidth are key drivers. The Automotive sector is emerging as a high-growth segment, with the adoption of LiDAR and advanced driver-assistance systems (ADAS) expected to drive substantial demand for semiconductor lasers.

Key Drivers for Dominance:

- Economic Policies and Investments: Government incentives and direct investments in semiconductor manufacturing and R&D, particularly in Asia Pacific, have fostered significant growth.

- Infrastructure Development: Extensive development of telecommunications infrastructure, including high-speed internet and 5G networks, directly fuels demand for optical components.

- Technological Advancements: Continuous innovation in laser design, materials, and manufacturing processes originating from key players in the dominant regions.

- Skilled Workforce: Availability of a skilled workforce in semiconductor fabrication and research and development contributes to manufacturing prowess.

- Consumer Electronics Hubs: Proximity to major consumer electronics manufacturing bases in Asia Pacific creates a strong local demand for semiconductor lasers.

Semiconductor Laser Industry Product Innovations

Semiconductor laser product innovations are continuously enhancing performance, miniaturization, and cost-effectiveness. Key developments include advancements in high-power output for industrial applications, increased efficiency for telecommunications, and specialized wavelengths for medical imaging and sensing. The integration of VCSELs into compact sensing modules for smartphones and automotive LiDAR systems is a significant trend, offering precise distance measurement and object detection capabilities with a competitive advantage in form factor and power consumption. Furthermore, research into novel materials and epitaxial growth techniques is paving the way for more robust and reliable semiconductor lasers across all application spectrums.

Report Scope & Segmentation Analysis

The Semiconductor Laser Industry is analyzed across several key dimensions. The Wavelength segmentation includes Infrared Lasers, Red Lasers, Green Lasers, Blue Lasers, and Ultraviolet Lasers, with Infrared and Blue lasers projected for robust growth. The Type segmentation encompasses EEL (Edge-emitting Laser), VCSEL (Vertical-cavity Surface-emitting Laser), Quantum Cascade Laser, Fiber Laser, and Other Types, with VCSELs exhibiting the highest growth trajectory. The Application segmentation covers Communication, Medical, Military and Defense, Industrial, Instrumentation and Sensor, Automotive, and Other Applications. Communication and Industrial applications are current market leaders, while Automotive and Medical are identified as high-growth areas with projected market sizes of approximately $6 Billion and $5 Billion respectively by 2033. Competitive dynamics vary significantly across these segments, with specialized players often dominating niche areas.

Key Drivers of Semiconductor Laser Industry Growth

The growth of the Semiconductor Laser Industry is propelled by several critical factors. The insatiable demand for high-bandwidth telecommunications, driven by 5G expansion and cloud computing, necessitates advanced semiconductor lasers for fiber optic networks. Technological advancements in VCSELs and EELs, enabling higher power, greater efficiency, and miniaturization, are opening new application frontiers. The burgeoning automotive sector, with its increasing adoption of LiDAR for autonomous driving and ADAS, represents a significant growth accelerator. Furthermore, the healthcare industry's expanding use of lasers for minimally invasive surgery, diagnostics, and therapy creates consistent demand. Government initiatives supporting semiconductor innovation and R&D also play a crucial role.

Challenges in the Semiconductor Laser Industry Sector

Despite robust growth, the Semiconductor Laser Industry faces notable challenges. Supply chain disruptions and geopolitical tensions can impact the availability and cost of raw materials, particularly rare earth elements and specialized chemicals. Intensifying competition and price pressures, especially in high-volume segments, can erode profit margins. Stringent regulatory requirements concerning environmental impact and product safety, while essential, can increase compliance costs and R&D timelines. The high cost of research and development for next-generation laser technologies requires substantial investment, posing a barrier for smaller players. Furthermore, the rapid pace of technological obsolescence necessitates continuous innovation to remain competitive.

Emerging Opportunities in Semiconductor Laser Industry

Emerging opportunities in the Semiconductor Laser Industry are diverse and promising. The expanding market for LiDAR systems in autonomous vehicles and advanced robotics presents substantial growth potential. The increasing adoption of optical sensing in consumer electronics, smart home devices, and industrial IoT applications is creating new demand for miniaturized and cost-effective semiconductor lasers. Developments in quantum computing and advanced scientific instrumentation are also opening niche, high-value markets. Furthermore, the use of semiconductor lasers in precision agriculture for crop monitoring and in advanced manufacturing for additive manufacturing and inspection offers untapped potential. The drive towards energy-efficient lighting solutions also presents opportunities for specialized laser diodes.

Leading Players in the Semiconductor Laser Industry Market

- Coherent Inc.

- Panasonic Industry Co Ltd

- Jenoptik Laser GMBH

- Nichia Corporation

- TRUmpF Group

- Lumentum Holdings Inc

- Rohm Company Limited

- TT Electronics

- ams OSRAM AG

- Sheaumann Laser Inc

- Newport Corporation (mks Instruments Inc )

- IPG Photonics Corporation

- Sharp Corporation

- Hamamatsu Photonics K K

- Sumitomo Electric Industries Ltd

Key Developments in Semiconductor Laser Industry Industry

- November 2023: The Air Force Research Laboratory opened a new Semiconductor Laser Indoor Propagation Range, known as SLIPR, at Kirtland Air Force Base in New Mexico. This facility is designed to support research and development of future laser system propagation studies. SLIPR features 100-meter-long broadcast ranges within an indoor facility to test semiconductor laser technology concepts and includes photoluminescence and X-ray laboratories for characterizing molecular beam epitaxy products, signifying a significant investment in defense-related laser R&D.

- September 2023: AMS OSRAM AG and the Malaysian Investment Development Authority (MIDA) announced mutual support for continued investment and expansion in Malaysia. Through a Collaborative Agreement, MIDA demonstrated significant support for AMS OSRAM’s initiatives in Malaysia, underscoring the strategic importance of regional manufacturing hubs for semiconductor laser production.

Future Outlook for Semiconductor Laser Industry Market

The future outlook for the Semiconductor Laser Industry is exceptionally positive, driven by sustained innovation and expanding applications. Growth accelerators include the continued rollout of 5G and future communication networks, which will significantly boost demand for optical transceivers. The automotive industry's transition to electric and autonomous vehicles will create a massive market for LiDAR and other laser-based sensors. Furthermore, the medical sector's increasing reliance on laser technology for diagnostics and minimally invasive procedures, coupled with the growth of consumer electronics featuring advanced sensing capabilities, will further propel market expansion. Strategic opportunities lie in developing higher-power, more energy-efficient, and cost-effective laser solutions for these burgeoning markets, alongside continued R&D in novel materials and device architectures.

Semiconductor Laser Industry Segmentation

-

1. Wavelength

- 1.1. Infrared Lasers

- 1.2. Red Lasers

- 1.3. Green Lasers

- 1.4. Blue lasers

- 1.5. Ultraviolet Lasers

-

2. Type

- 2.1. EEL (Edge-emitting Laser)

- 2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 2.3. Quantum Cascade Laser

- 2.4. Fiber Laser

- 2.5. Other Types

-

3. Application

- 3.1. Communication

- 3.2. Medical

- 3.3. Military and Defense

- 3.4. Industrial

- 3.5. Instrumentation and Sensor

- 3.6. Automotive

- 3.7. Other Applications

Semiconductor Laser Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Semiconductor Laser Industry Regional Market Share

Geographic Coverage of Semiconductor Laser Industry

Semiconductor Laser Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Wavelength

- 5.1.1. Infrared Lasers

- 5.1.2. Red Lasers

- 5.1.3. Green Lasers

- 5.1.4. Blue lasers

- 5.1.5. Ultraviolet Lasers

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. EEL (Edge-emitting Laser)

- 5.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 5.2.3. Quantum Cascade Laser

- 5.2.4. Fiber Laser

- 5.2.5. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Communication

- 5.3.2. Medical

- 5.3.3. Military and Defense

- 5.3.4. Industrial

- 5.3.5. Instrumentation and Sensor

- 5.3.6. Automotive

- 5.3.7. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Wavelength

- 6. Global Semiconductor Laser Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Wavelength

- 6.1.1. Infrared Lasers

- 6.1.2. Red Lasers

- 6.1.3. Green Lasers

- 6.1.4. Blue lasers

- 6.1.5. Ultraviolet Lasers

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. EEL (Edge-emitting Laser)

- 6.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 6.2.3. Quantum Cascade Laser

- 6.2.4. Fiber Laser

- 6.2.5. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Communication

- 6.3.2. Medical

- 6.3.3. Military and Defense

- 6.3.4. Industrial

- 6.3.5. Instrumentation and Sensor

- 6.3.6. Automotive

- 6.3.7. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Wavelength

- 7. North America Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Wavelength

- 7.1.1. Infrared Lasers

- 7.1.2. Red Lasers

- 7.1.3. Green Lasers

- 7.1.4. Blue lasers

- 7.1.5. Ultraviolet Lasers

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. EEL (Edge-emitting Laser)

- 7.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 7.2.3. Quantum Cascade Laser

- 7.2.4. Fiber Laser

- 7.2.5. Other Types

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Communication

- 7.3.2. Medical

- 7.3.3. Military and Defense

- 7.3.4. Industrial

- 7.3.5. Instrumentation and Sensor

- 7.3.6. Automotive

- 7.3.7. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Wavelength

- 8. Europe Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Wavelength

- 8.1.1. Infrared Lasers

- 8.1.2. Red Lasers

- 8.1.3. Green Lasers

- 8.1.4. Blue lasers

- 8.1.5. Ultraviolet Lasers

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. EEL (Edge-emitting Laser)

- 8.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 8.2.3. Quantum Cascade Laser

- 8.2.4. Fiber Laser

- 8.2.5. Other Types

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Communication

- 8.3.2. Medical

- 8.3.3. Military and Defense

- 8.3.4. Industrial

- 8.3.5. Instrumentation and Sensor

- 8.3.6. Automotive

- 8.3.7. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Wavelength

- 9. Asia Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Wavelength

- 9.1.1. Infrared Lasers

- 9.1.2. Red Lasers

- 9.1.3. Green Lasers

- 9.1.4. Blue lasers

- 9.1.5. Ultraviolet Lasers

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. EEL (Edge-emitting Laser)

- 9.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 9.2.3. Quantum Cascade Laser

- 9.2.4. Fiber Laser

- 9.2.5. Other Types

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Communication

- 9.3.2. Medical

- 9.3.3. Military and Defense

- 9.3.4. Industrial

- 9.3.5. Instrumentation and Sensor

- 9.3.6. Automotive

- 9.3.7. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Wavelength

- 10. Australia and New Zealand Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Wavelength

- 10.1.1. Infrared Lasers

- 10.1.2. Red Lasers

- 10.1.3. Green Lasers

- 10.1.4. Blue lasers

- 10.1.5. Ultraviolet Lasers

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. EEL (Edge-emitting Laser)

- 10.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 10.2.3. Quantum Cascade Laser

- 10.2.4. Fiber Laser

- 10.2.5. Other Types

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Communication

- 10.3.2. Medical

- 10.3.3. Military and Defense

- 10.3.4. Industrial

- 10.3.5. Instrumentation and Sensor

- 10.3.6. Automotive

- 10.3.7. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Wavelength

- 11. Latin America Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Wavelength

- 11.1.1. Infrared Lasers

- 11.1.2. Red Lasers

- 11.1.3. Green Lasers

- 11.1.4. Blue lasers

- 11.1.5. Ultraviolet Lasers

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. EEL (Edge-emitting Laser)

- 11.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 11.2.3. Quantum Cascade Laser

- 11.2.4. Fiber Laser

- 11.2.5. Other Types

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Communication

- 11.3.2. Medical

- 11.3.3. Military and Defense

- 11.3.4. Industrial

- 11.3.5. Instrumentation and Sensor

- 11.3.6. Automotive

- 11.3.7. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Wavelength

- 12. Middle East and Africa Semiconductor Laser Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Wavelength

- 12.1.1. Infrared Lasers

- 12.1.2. Red Lasers

- 12.1.3. Green Lasers

- 12.1.4. Blue lasers

- 12.1.5. Ultraviolet Lasers

- 12.2. Market Analysis, Insights and Forecast - by Type

- 12.2.1. EEL (Edge-emitting Laser)

- 12.2.2. VCSEL (Vertical-cavity Surface-emitting Laser)

- 12.2.3. Quantum Cascade Laser

- 12.2.4. Fiber Laser

- 12.2.5. Other Types

- 12.3. Market Analysis, Insights and Forecast - by Application

- 12.3.1. Communication

- 12.3.2. Medical

- 12.3.3. Military and Defense

- 12.3.4. Industrial

- 12.3.5. Instrumentation and Sensor

- 12.3.6. Automotive

- 12.3.7. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Wavelength

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Coherent Inc

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Panasonic Industry Co Ltd

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Jenoptik Laser GMBH

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Nichia Corporation

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 TRUmpF Group

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Lumentum Holdings Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Rohm Company Limited

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 TT Electronics

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 ams OSRAM AG

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Sheaumann Laser Inc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Newport Corporation (mks Instruments Inc )

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 IPG Photonics Corporation

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Sharp Corporation

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Hamamatsu Photonics K K

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Sumitomo Electric Industries Ltd

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.1 Coherent Inc

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Laser Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 3: North America Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 4: North America Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 5: North America Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: North America Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 11: Europe Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 12: Europe Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 13: Europe Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 14: Europe Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Europe Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 19: Asia Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 20: Asia Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: Asia Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Asia Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Asia Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Asia Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 27: Australia and New Zealand Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 28: Australia and New Zealand Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 29: Australia and New Zealand Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Australia and New Zealand Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 31: Australia and New Zealand Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: Australia and New Zealand Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 35: Latin America Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 36: Latin America Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 37: Latin America Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 38: Latin America Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Latin America Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Semiconductor Laser Industry Revenue (Million), by Wavelength 2025 & 2033

- Figure 43: Middle East and Africa Semiconductor Laser Industry Revenue Share (%), by Wavelength 2025 & 2033

- Figure 44: Middle East and Africa Semiconductor Laser Industry Revenue (Million), by Type 2025 & 2033

- Figure 45: Middle East and Africa Semiconductor Laser Industry Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East and Africa Semiconductor Laser Industry Revenue (Million), by Application 2025 & 2033

- Figure 47: Middle East and Africa Semiconductor Laser Industry Revenue Share (%), by Application 2025 & 2033

- Figure 48: Middle East and Africa Semiconductor Laser Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Semiconductor Laser Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 2: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Semiconductor Laser Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 6: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 7: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 10: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 14: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 15: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 18: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 19: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 22: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 23: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Semiconductor Laser Industry Revenue Million Forecast, by Wavelength 2020 & 2033

- Table 26: Global Semiconductor Laser Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 27: Global Semiconductor Laser Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Laser Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Laser Industry?

The projected CAGR is approximately 13.40%.

2. Which companies are prominent players in the Semiconductor Laser Industry?

Key companies in the market include Coherent Inc, Panasonic Industry Co Ltd, Jenoptik Laser GMBH, Nichia Corporation, TRUmpF Group, Lumentum Holdings Inc, Rohm Company Limited, TT Electronics, ams OSRAM AG, Sheaumann Laser Inc, Newport Corporation (mks Instruments Inc ), IPG Photonics Corporation, Sharp Corporation, Hamamatsu Photonics K K, Sumitomo Electric Industries Ltd.

3. What are the main segments of the Semiconductor Laser Industry?

The market segments include Wavelength, Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.24 Million as of 2022.

5. What are some drivers contributing to market growth?

Proliferation of Semiconductor Laser Applications; Growth in the Fiber Laser Market; Preference for Semiconductor Lasers Over Other Light Sources.

6. What are the notable trends driving market growth?

Communication Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Increase in Network Complexity.

8. Can you provide examples of recent developments in the market?

November 2023 - The Air Force Research Laboratory opened a new Semiconductor Laser Indoor Propagation Range, known as SLIPR, at Kirtland Air Force Base in New Mexico to support research and development of future laser system propagation studies. SLIPR has 100-meter-long broadcast ranges in an indoor facility to test semiconductor laser technology concepts and includes photoluminescence and X-ray laboratories to characterize molecular beam epitaxy products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Laser Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Laser Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Laser Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Laser Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence