Key Insights

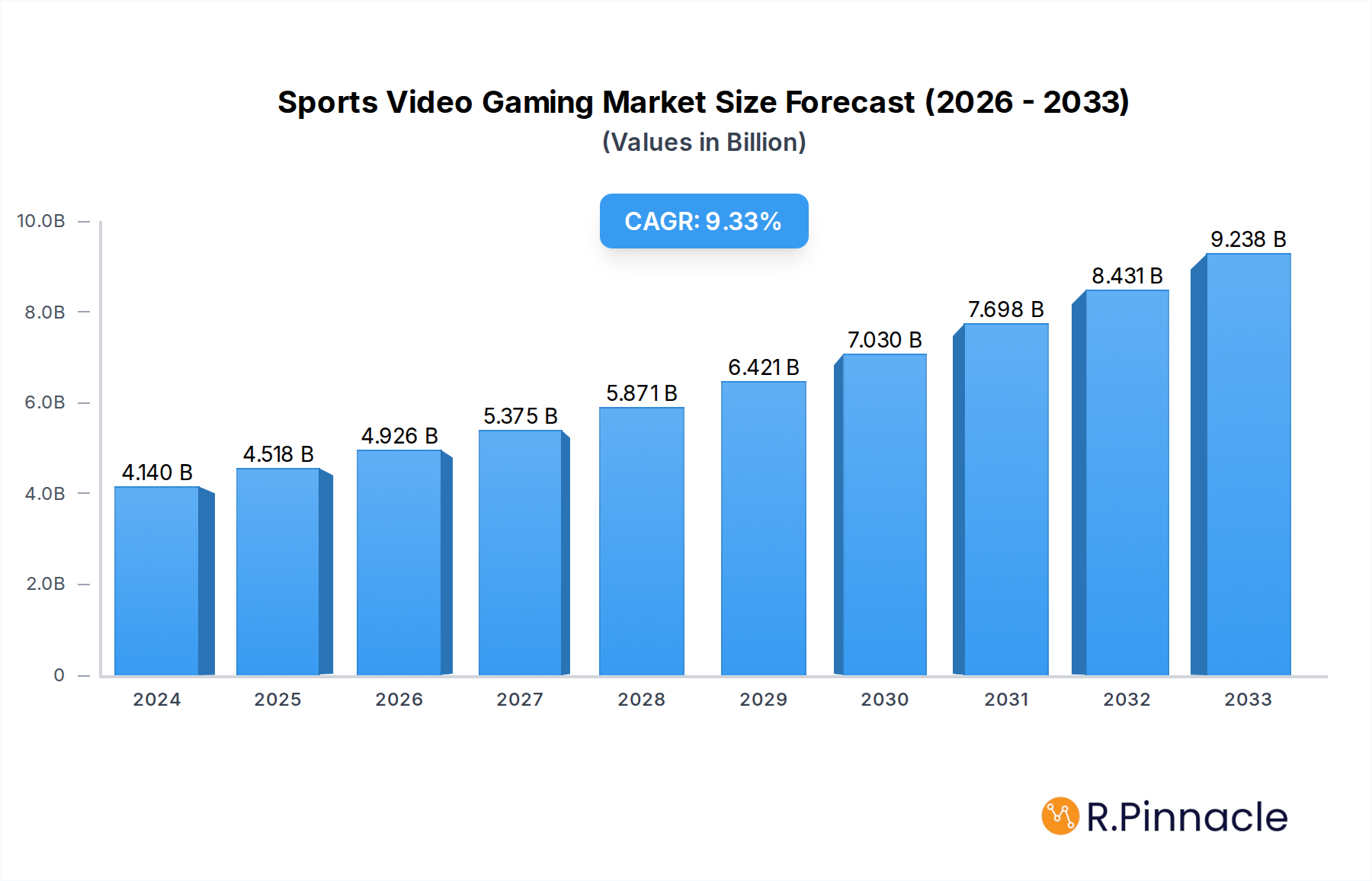

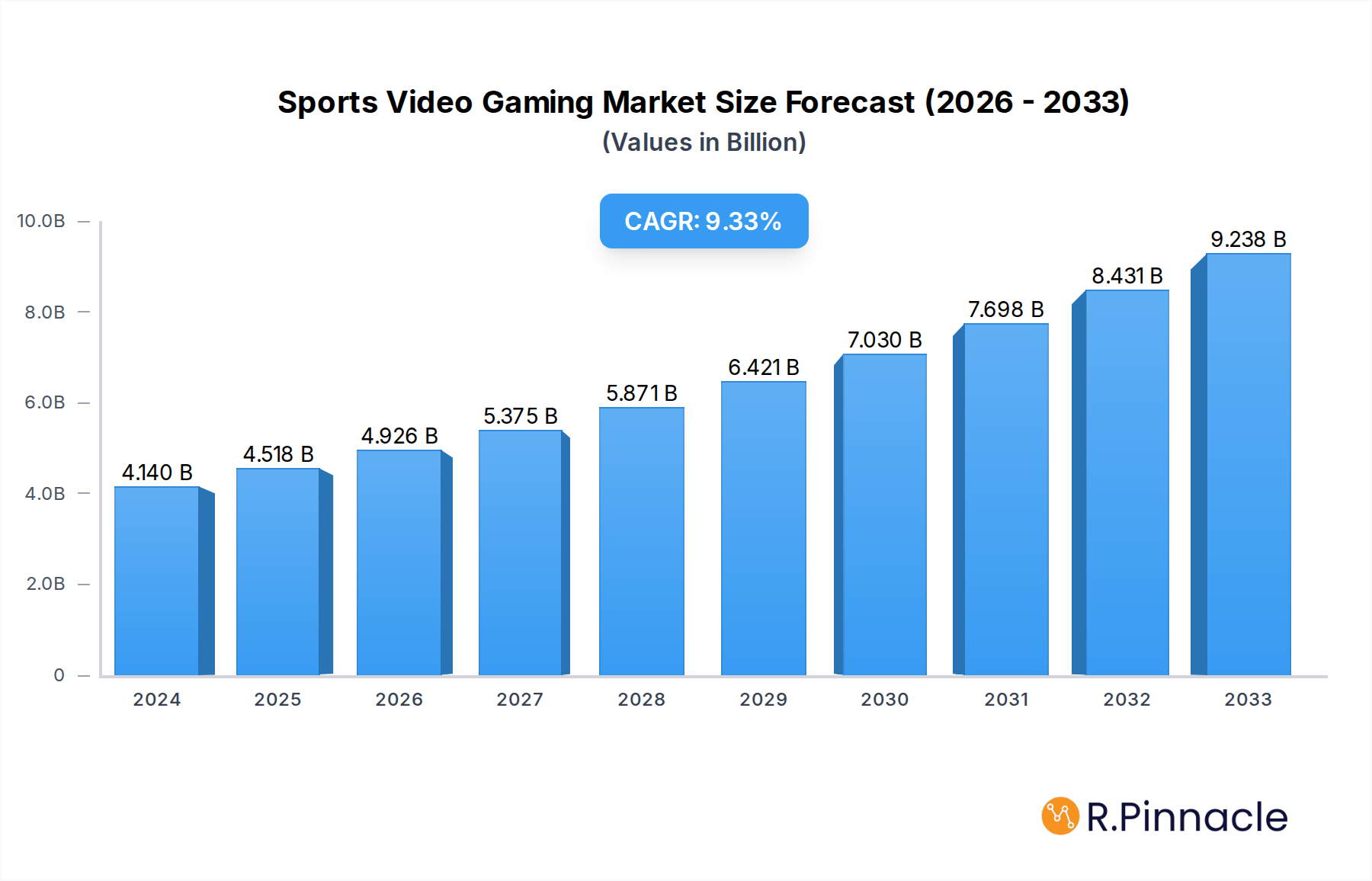

The global Sports Video Gaming market is experiencing robust growth, projected to reach $4.14 billion in 2024 with a remarkable Compound Annual Growth Rate (CAGR) of 9.04% through 2033. This expansion is fueled by several key drivers, including the increasing popularity of esports, the continuous innovation in gaming technology that offers more immersive and realistic experiences, and the growing accessibility of high-speed internet and powerful gaming hardware across developing economies. The market is segmented by application into Desktop, Notebook, Console, and Others, with consoles continuing to hold a significant share due to their dedicated gaming ecosystem. In terms of game types, Racing Car games, Fighting games, and Other sports simulations each contribute to the diverse appeal of the sector. Major players like Electronic Arts, Activision Blizzard, and NINTENDO are at the forefront, investing heavily in content development and marketing to capture a larger share of this dynamic market. The Asia Pacific region, particularly China and India, is emerging as a significant growth engine, driven by a burgeoning young population and increasing disposable incomes.

Sports Video Gaming Market Size (In Billion)

The sports video gaming landscape is characterized by evolving trends such as the integration of virtual reality (VR) and augmented reality (AR) for more interactive gameplay, the rise of mobile sports gaming, and the increasing demand for user-generated content within games. However, the market also faces certain restraints, including the high cost of premium gaming titles and hardware, which can limit adoption among price-sensitive consumers, and concerns over excessive screen time and potential addiction. Despite these challenges, the overall outlook for the sports video gaming market remains exceptionally positive. The continuous development of compelling narratives, realistic graphics, and competitive multiplayer features, coupled with strategic partnerships with sports leagues and athletes, will further solidify its position as a dominant force in the entertainment industry. The North American and European markets, while mature, continue to innovate and drive revenue, while emerging markets offer substantial untapped potential for future expansion.

Sports Video Gaming Company Market Share

Sports Video Gaming Market Report: Industry Analysis, Trends, and Forecasts (2019-2033)

Unlock unparalleled insights into the rapidly evolving global sports video gaming market with this comprehensive, SEO-optimized report. Delve deep into market dynamics, technological innovations, and future projections shaping this multi-billion dollar industry. Designed for industry professionals, investors, and strategists, this report offers actionable intelligence, critical data, and expert analysis to navigate the competitive landscape and capitalize on emerging opportunities.

Sports Video Gaming Market Structure & Innovation Trends

The sports video gaming market exhibits a dynamic structure characterized by significant innovation drivers and a concentrated competitive landscape. Leading players such as Electronic Arts, Activision Blizzard, and 2K Games dominate a substantial portion of the market share, estimated to be in the billions, reflecting their established intellectual property and extensive player bases. Innovation is primarily fueled by advancements in graphics technology, artificial intelligence for more realistic gameplay, and the integration of esports, driving continuous product development. Regulatory frameworks, while present to ensure fair play and protect consumer interests, generally support growth within established guidelines. The threat of product substitutes, such as live sports viewership or other entertainment options, remains a consideration, but the immersive and interactive nature of sports video games offers a distinct value proposition. End-user demographics span a broad spectrum, from casual gamers to highly engaged esports enthusiasts, with a growing segment of mobile and cross-platform players. Mergers and acquisitions (M&A) activity, with deal values reaching billions, plays a crucial role in market consolidation and the acquisition of new technologies and talent. For instance, major acquisitions in the past few years have reshaped the competitive terrain, impacting market concentration and driving synergistic growth. The market structure is thus a complex interplay of established giants, innovative startups, and strategic consolidation.

- Market Concentration: Dominated by a few key players with significant market share.

- Innovation Drivers: Advanced graphics, AI, VR/AR integration, esports proliferation.

- Regulatory Frameworks: Focused on consumer protection, fair competition, and age appropriateness.

- Product Substitutes: Live sports, other gaming genres, alternative entertainment forms.

- End-User Demographics: Broad appeal from casual to hardcore gamers, across age groups.

- M&A Activities: Significant deal values in the billions, driving consolidation and talent acquisition.

Sports Video Gaming Market Dynamics & Trends

The global sports video gaming market is experiencing robust expansion, driven by a confluence of factors that are reshaping its trajectory. The estimated market size for the base year of 2025 is projected to be in the billions, with a compound annual growth rate (CAGR) expected to sustain strong momentum throughout the forecast period of 2025–2033. This growth is intrinsically linked to escalating consumer disposable incomes and a burgeoning interest in interactive entertainment, leading to increased market penetration across diverse demographics. Technological disruptions are at the forefront of this evolution. The proliferation of high-speed internet, cloud gaming services, and the continuous refinement of graphics processing units (GPUs) are enabling more immersive and accessible gameplay experiences. Mobile gaming, in particular, has witnessed exponential growth, breaking down traditional barriers to entry and expanding the player base significantly. Furthermore, the rise of esports, with its professional leagues, tournaments, and substantial prize pools often in the millions, has transformed sports video games from a pastime into a spectator sport, attracting significant investment and media attention. Consumer preferences are also evolving, with a growing demand for realistic simulations, deeper customization options, and more compelling narrative-driven experiences within sports titles. The competitive dynamics are intense, characterized by fierce competition among established publishers and the emergence of new entrants leveraging innovative business models and technologies. The integration of virtual reality (VR) and augmented reality (AR) technologies, while still in its nascent stages for mainstream sports gaming, holds immense potential to revolutionize player engagement and create entirely new gameplay paradigms, contributing to the ongoing market penetration and sustained growth. The increasing popularity of free-to-play models with in-game purchases also plays a crucial role in revenue generation and player acquisition, further fueling market expansion and innovation within the sector.

Dominant Regions & Segments in Sports Video Gaming

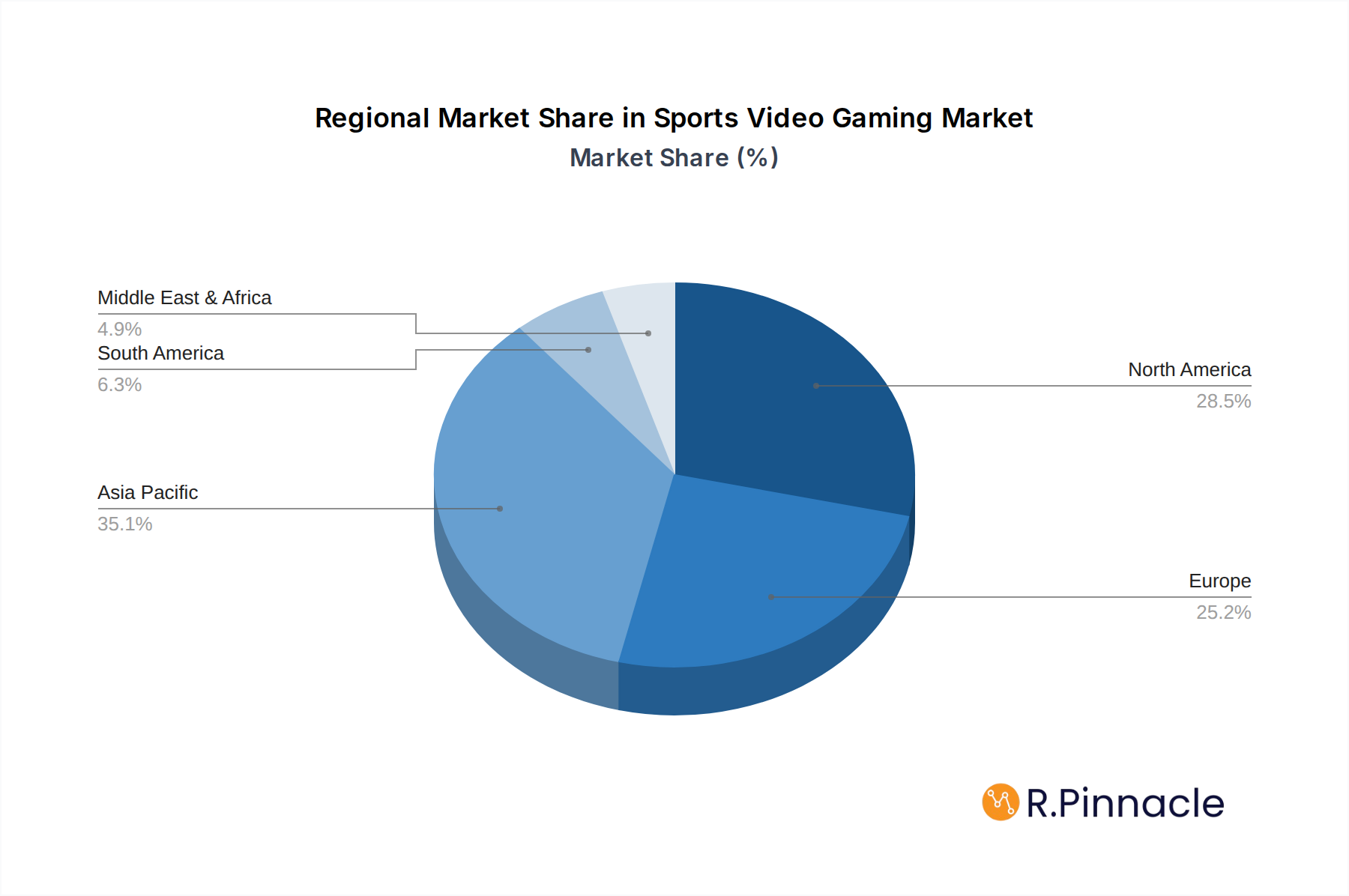

The global sports video gaming market's dominance is intricately tied to specific regions and segments, with North America consistently leading due to its high disposable incomes, advanced technological infrastructure, and a deeply ingrained gaming culture. The United States, in particular, stands out as a paramount market, driven by a significant concentration of key industry players, substantial consumer spending on video games, and a robust esports ecosystem that generates billions in revenue annually. Economic policies that foster innovation and investment in the technology sector, coupled with widespread availability of high-speed internet and powerful gaming hardware, create an ideal environment for market growth.

Within the Application segmentation, the Console segment continues to be a cornerstone of the sports video gaming market, boasting billions in revenue. This dominance is fueled by dedicated gaming consoles like PlayStation and Xbox, offering high-fidelity graphics and immersive gameplay experiences that resonate deeply with sports enthusiasts. The sheer volume of console sales and the consistent release of AAA sports titles ensure its perpetual relevance and significant market share.

The Notebook segment is also experiencing substantial growth, projected to contribute billions to the market. This rise is attributed to the increasing power and portability of gaming laptops, making them a viable option for players who value flexibility and performance. The growing popularity of esports and the demand for cross-platform play further bolster the notebook segment’s importance.

The Desktop segment, while a traditional stronghold, continues to hold its ground, generating billions through PC gaming. The customization options, affordability of hardware upgrades, and the prevalence of free-to-play PC titles ensure its enduring appeal. Many competitive esports titles are primarily played on desktop PCs, underscoring its significance.

The Others segment, encompassing mobile gaming and emerging platforms, is a rapidly expanding frontier, projected to reach billions in the coming years. The accessibility of smartphones and tablets, coupled with a vast array of casual and simulation-based sports games, has democratized gaming and opened up new revenue streams, significantly impacting overall market dynamics.

In terms of Type, the Racing Car segment remains a perennial favorite, consistently generating billions in sales. Titles like Forza Motorsport and Gran Turismo captivate audiences with their realistic simulations, cutting-edge graphics, and competitive online multiplayer modes, demonstrating enduring consumer appeal.

The Fighting game genre, while perhaps not as broadly categorized under "sports" in the traditional sense, often features competitive play that mirrors athletic prowess and generates billions in revenue. Franchises such as Mortal Kombat and Street Fighter have cult followings and robust esports scenes, contributing significantly to the overall market value.

The Other type segment, encompassing a wide array of sports simulation and management games, is also a considerable contributor, projected to reach billions. This broad category includes titles that simulate various sports like soccer, basketball, and American football, offering strategic depth and management gameplay that appeals to a dedicated audience.

- Leading Region: North America, driven by the United States, with billions in market contribution.

- Dominant Application Segment: Console gaming, accounting for billions in revenue.

- Growth Application Segment: Notebook and Others (mobile gaming), exhibiting strong upward trends and billions in projected value.

- Key Type Segments: Racing Car and Other sports simulations, consistently generating billions.

- Economic Drivers: High disposable income, robust technological infrastructure, supportive government policies.

- Infrastructure Impact: Widespread high-speed internet access, advanced gaming hardware availability.

Sports Video Gaming Product Innovations

The sports video gaming sector is a hotbed of continuous product innovation, driven by a relentless pursuit of realism and engagement. Technological advancements in graphics rendering, physics engines, and artificial intelligence are creating increasingly lifelike player models, stadium environments, and in-game physics, significantly enhancing the player experience. Developers are integrating sophisticated AI to create more strategic and unpredictable opponents and teammates, pushing the boundaries of simulation. The application of virtual and augmented reality is also becoming more prominent, offering immersive perspectives that bring players closer to the action, creating unique competitive advantages for titles that effectively leverage these technologies. Furthermore, the integration of real-world sports data and analytics is enabling more authentic and dynamic gameplay. These innovations collectively contribute to a richer, more engaging, and competitive gaming environment, ensuring that sports video games remain at the cutting edge of entertainment technology and maintain strong market fit.

Report Scope & Segmentation Analysis

This comprehensive report analyzes the global sports video gaming market across key segmentation dimensions to provide a granular understanding of its structure and growth potential. The Application segmentation includes Desktop, Notebook, Console, and Others (primarily mobile gaming). The Type segmentation encompasses Racing Car games, Fighting games, and Other sports-related titles.

Desktop: This segment, projected to grow at a steady CAGR and contribute billions, is characterized by a loyal user base and a vast library of competitive titles. Its market dynamics are influenced by hardware advancements and the continued popularity of PC-centric esports.

Notebook: Experiencing significant growth with billions in projected market size, the notebook segment benefits from increasing laptop performance and the demand for portable gaming solutions. Cross-platform compatibility and the rise of esports are key growth accelerators.

Console: Remaining a dominant force with billions in market value, the console segment is driven by dedicated gaming platforms. Consistent hardware upgrades and the release of flagship sports titles ensure its continued strength and competitive landscape.

Others: This rapidly expanding segment, encompassing mobile gaming and emerging platforms, is poised for substantial growth, with projected market sizes in the billions. The accessibility of smartphones and the proliferation of casual sports games are key drivers, indicating a significant shift in consumer engagement.

Racing Car: This established genre, a consistent revenue generator with billions in market size, thrives on realistic simulations and competitive online play. Innovation in graphics and vehicle physics are crucial for maintaining its appeal.

Fighting: While often considered a distinct genre, fighting games share many characteristics with sports, including competitive play and a strong esports presence, contributing billions to the overall market. Their market dynamics are shaped by character rosters, combat mechanics, and community engagement.

Other: This broad category, encompassing a diverse range of sports simulations and management games, contributes billions to the market. Its growth is fueled by niche sports fandom and the desire for strategic gameplay experiences.

Key Drivers of Sports Video Gaming Growth

The sports video gaming market is propelled by a potent combination of technological, economic, and regulatory factors. Technologically, advancements in graphics rendering, virtual and augmented reality, and cloud gaming are creating more immersive and accessible experiences, expanding the player base and encouraging deeper engagement. Economically, rising disposable incomes globally, particularly in emerging markets, translate into increased spending on entertainment, with video games being a prime beneficiary. The significant investment in esports infrastructure, including professional leagues and broadcasting platforms, with prize pools often in the billions, is a major economic driver, attracting both players and sponsors. Regulatory frameworks, when supportive of innovation and intellectual property protection, create a favorable environment for growth, ensuring fair competition and incentivizing developers. The increasing adoption of free-to-play models with in-game monetization strategies, generating billions in revenue, also fuels market expansion by lowering entry barriers and fostering continuous player engagement.

- Technological Advancements: Enhanced graphics, VR/AR integration, cloud gaming accessibility.

- Economic Factors: Rising disposable incomes, substantial esports investment (billions), global market expansion.

- Regulatory Environment: Supportive intellectual property laws, fair competition policies.

- Monetization Models: Growth of free-to-play with in-game purchases, contributing billions.

Challenges in the Sports Video Gaming Sector

Despite its robust growth, the sports video gaming sector faces several significant challenges that can impede its progress and impact market potential. Regulatory hurdles, such as varying age rating systems across different countries and evolving guidelines for loot boxes and in-game purchases, can create compliance complexities and marketing limitations, potentially costing billions in missed opportunities. Supply chain issues, particularly concerning the availability of crucial hardware components like GPUs and advanced chipsets, have historically led to shortages and inflated prices, impacting console and PC game accessibility and sales, with economic repercussions in the billions. Competitive pressures are immense, with established publishers constantly vying for market share, and the threat of emerging disruptive technologies or entirely new entertainment forms always present. Furthermore, the significant investment required for AAA game development, often reaching hundreds of millions, makes market entry and sustained success a daunting prospect for smaller studios. The increasing cost of user acquisition in a crowded digital marketplace also presents a continuous challenge.

- Regulatory Hurdles: Diverse rating systems, evolving in-game purchase regulations.

- Supply Chain Disruptions: Hardware component shortages impacting availability and pricing.

- Intense Competition: Market saturation and the need for constant innovation.

- High Development Costs: Significant investment (hundreds of millions) for AAA titles.

Emerging Opportunities in Sports Video Gaming

The sports video gaming market is ripe with emerging opportunities that promise to reshape its future and unlock billions in new revenue streams. The continued expansion of esports globally presents a significant avenue for growth, with the development of new leagues, professional teams, and broadcast rights deals. The integration of Web3 technologies, such as NFTs and blockchain-based gaming, offers novel ways for players to own in-game assets and participate in decentralized economies, potentially creating entirely new player-driven markets valued in the billions. The burgeoning market in developing economies, with their rapidly growing middle class and increasing smartphone penetration, represents a vast untapped consumer base hungry for accessible and engaging sports gaming experiences. Furthermore, the advancement of cloud gaming technologies is poised to democratize high-fidelity gaming, removing hardware barriers and making sophisticated sports simulations available on a wider range of devices. The increasing focus on social gaming and the metaverse offers opportunities for players to connect, compete, and socialize within virtual sports arenas, fostering deeper community engagement and new forms of interactive entertainment.

- Esports Expansion: New leagues, professional teams, broadcast rights deals.

- Web3 Integration: NFTs, blockchain gaming, decentralized player economies.

- Emerging Markets: Tapping into growing consumer bases in developing economies.

- Cloud Gaming Advancement: Democratizing access to high-fidelity gaming experiences.

- Metaverse & Social Gaming: Creating immersive virtual sports communities and experiences.

Leading Players in the Sports Video Gaming Market

- Electronic Arts

- Activision Blizzard

- 2K Games

- NINTENDO

- SONY

- Ubisoft

- KONAMI

- CAPCOM

- SQUARE ENIX

- SEGA

Key Developments in Sports Video Gaming Industry

- 2019: Release of EA Sports FIFA 20, featuring new gameplay modes and enhanced player customization, impacting market trends.

- 2020: Launch of PlayStation 5 and Xbox Series X/S, ushering in a new era of console gaming with significant implications for sports titles.

- 2021: Acquisition of ZeniMax Media by Microsoft for $7.5 billion, influencing competitive dynamics in the gaming industry.

- 2022: The continued growth and professionalization of esports leagues for titles like League of Legends and Valorant, with major tournaments attracting millions in viewership and prize pools.

- 2023: Increased investment and development in VR/AR sports gaming experiences, exploring new avenues for player immersion.

- 2024: Rise of cross-platform play becoming a standard feature in major sports video games, expanding player accessibility and market reach.

- 2025 (Estimated): Significant advancements in AI for more realistic player behavior and game dynamics expected in flagship sports titles.

- 2026 (Projected): Wider adoption of cloud gaming solutions for sports titles, enabling play on a broader range of devices.

- 2027 (Projected): Increased integration of player-generated content and community-driven features in sports games.

- 2028 (Projected): Growing exploration of NFTs and Web3 integration for in-game asset ownership in sports gaming.

- 2029 (Projected): Maturation of mobile esports for sports simulation titles, further expanding the player base.

- 2030 (Projected): Enhanced integration of real-world sports data for more dynamic and responsive in-game simulations.

- 2031 (Projected): Greater focus on accessibility features and inclusive game design in sports video games.

- 2032 (Projected): Emerging use of generative AI for dynamic content creation within sports game environments.

- 2033 (Projected): Continued evolution of player engagement models, potentially incorporating interactive storytelling in sports titles.

Future Outlook for Sports Video Gaming Market

The future outlook for the sports video gaming market is exceptionally bright, characterized by sustained growth and transformative innovation, with projections indicating a market value in the tens of billions. Growth accelerators include the continued technological evolution of graphics and AI, leading to unparalleled realism and immersion. The expanding global reach of esports, attracting massive audiences and significant investment, will continue to fuel player engagement and commercial opportunities. The increasing penetration of cloud gaming and mobile technologies will democratize access, bringing sophisticated sports simulations to a broader demographic. Furthermore, the integration of emerging technologies like VR/AR and Web3 elements, while still developing, holds the potential to unlock entirely new forms of player interaction and economic models. Strategic opportunities lie in catering to the evolving preferences of younger generations, embracing new monetization strategies, and fostering vibrant online communities. The market is poised for continued expansion, driven by a passionate player base and relentless innovation.

Sports Video Gaming Segmentation

-

1. Application

- 1.1. Desktop

- 1.2. Notebook

- 1.3. Console

- 1.4. Others

-

2. Type

- 2.1. Racing Car

- 2.2. Fighting

- 2.3. Other

Sports Video Gaming Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Sports Video Gaming Regional Market Share

Geographic Coverage of Sports Video Gaming

Sports Video Gaming REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Desktop

- 5.1.2. Notebook

- 5.1.3. Console

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Racing Car

- 5.2.2. Fighting

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Sports Video Gaming Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Desktop

- 6.1.2. Notebook

- 6.1.3. Console

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Racing Car

- 6.2.2. Fighting

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Sports Video Gaming Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Desktop

- 7.1.2. Notebook

- 7.1.3. Console

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Racing Car

- 7.2.2. Fighting

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Sports Video Gaming Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Desktop

- 8.1.2. Notebook

- 8.1.3. Console

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Racing Car

- 8.2.2. Fighting

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Sports Video Gaming Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Desktop

- 9.1.2. Notebook

- 9.1.3. Console

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Racing Car

- 9.2.2. Fighting

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Sports Video Gaming Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Desktop

- 10.1.2. Notebook

- 10.1.3. Console

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Racing Car

- 10.2.2. Fighting

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Sports Video Gaming Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Desktop

- 11.1.2. Notebook

- 11.1.3. Console

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Racing Car

- 11.2.2. Fighting

- 11.2.3. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ElectronicArts

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Activision Blizzard

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 2K Games

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 NINTENDO

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SONY

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Ubisoft

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 KONAMI

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CAPCOM

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SQUARE ENIX

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SEGA

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 ElectronicArts

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Sports Video Gaming Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Sports Video Gaming Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Sports Video Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Sports Video Gaming Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Sports Video Gaming Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Sports Video Gaming Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Sports Video Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Sports Video Gaming Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Sports Video Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Sports Video Gaming Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Sports Video Gaming Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Sports Video Gaming Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Sports Video Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Sports Video Gaming Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Sports Video Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Sports Video Gaming Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Sports Video Gaming Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Sports Video Gaming Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Sports Video Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Sports Video Gaming Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Sports Video Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Sports Video Gaming Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Sports Video Gaming Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Sports Video Gaming Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Sports Video Gaming Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Sports Video Gaming Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Sports Video Gaming Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Sports Video Gaming Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Sports Video Gaming Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Sports Video Gaming Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Sports Video Gaming Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Sports Video Gaming Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Sports Video Gaming Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Sports Video Gaming Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Sports Video Gaming Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Sports Video Gaming Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Sports Video Gaming Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Sports Video Gaming Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Sports Video Gaming Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Sports Video Gaming Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sports Video Gaming?

The projected CAGR is approximately 9.04%.

2. Which companies are prominent players in the Sports Video Gaming?

Key companies in the market include ElectronicArts, Activision Blizzard, 2K Games, NINTENDO, SONY, Ubisoft, KONAMI, CAPCOM, SQUARE ENIX, SEGA.

3. What are the main segments of the Sports Video Gaming?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.14 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sports Video Gaming," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sports Video Gaming report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sports Video Gaming?

To stay informed about further developments, trends, and reports in the Sports Video Gaming, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence