Key Insights

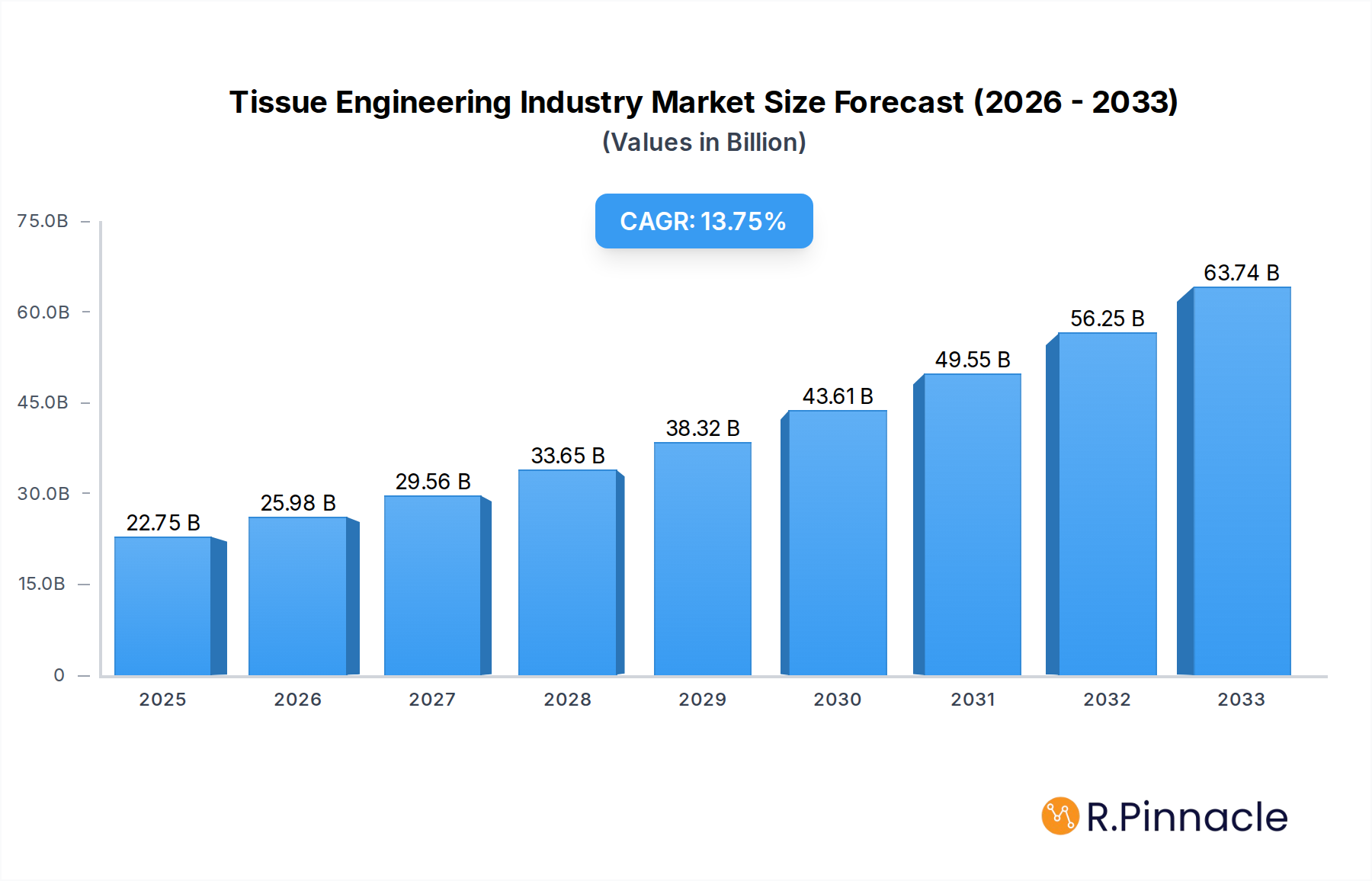

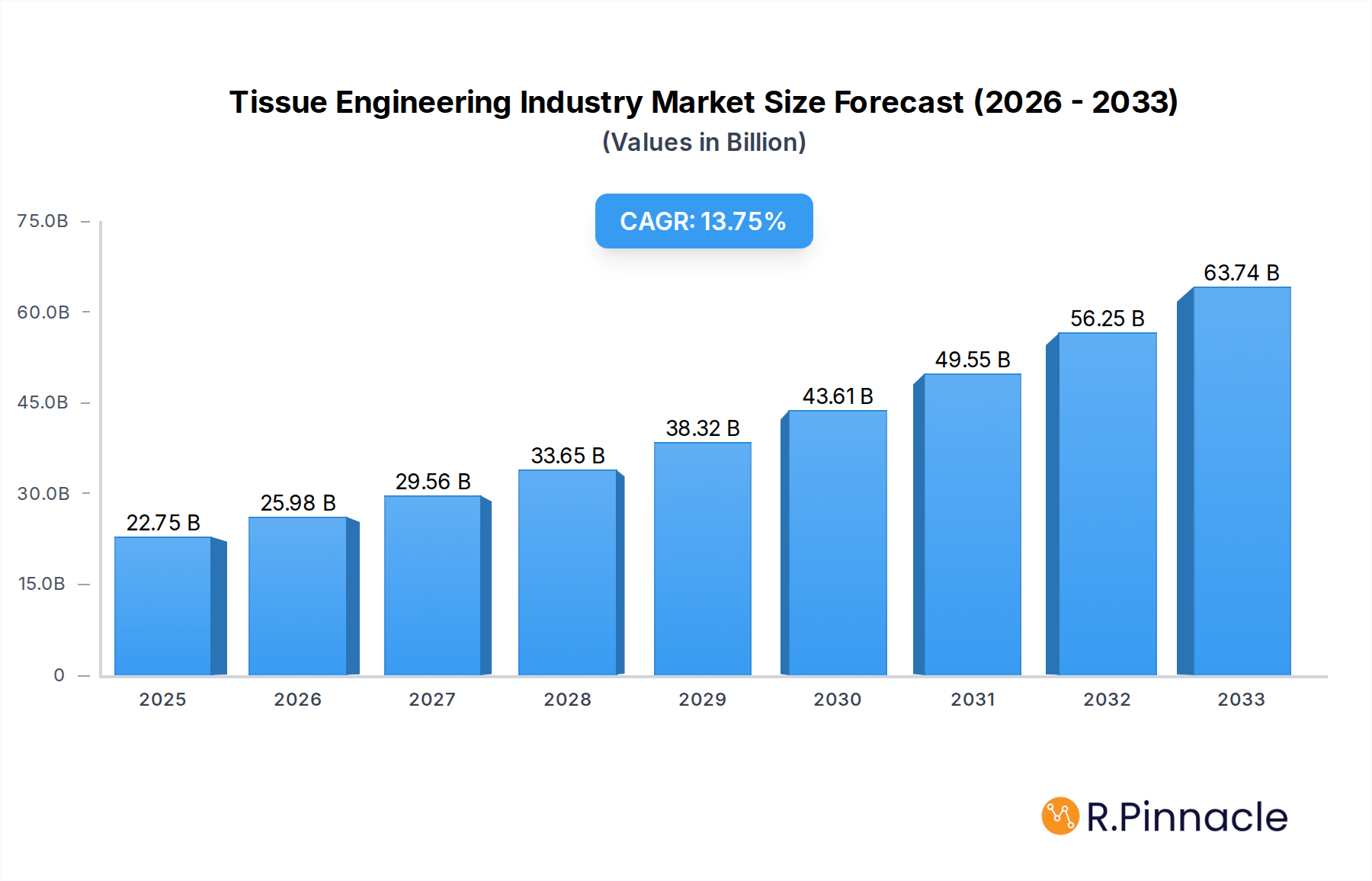

The global Tissue Engineering market is poised for significant expansion, projected to reach USD 22.75 billion by 2025. This robust growth is underpinned by an impressive Compound Annual Growth Rate (CAGR) of 14.6% throughout the forecast period of 2025-2033. A primary driver fueling this surge is the escalating prevalence of chronic diseases and injuries that necessitate advanced regenerative therapies. The increasing demand for innovative solutions in orthopedics, musculoskeletal and spine conditions, neurology, cardiology and vascular treatments, and skin and integumentary repair is a key catalyst. Advancements in biomaterials, including both synthetic and biologically derived options, coupled with sophisticated cell culture techniques, are continuously expanding the therapeutic potential of tissue engineering. Furthermore, a growing emphasis on personalized medicine and the development of off-the-shelf regenerative products are anticipated to further accelerate market penetration and adoption across various medical specialties.

Tissue Engineering Industry Market Size (In Billion)

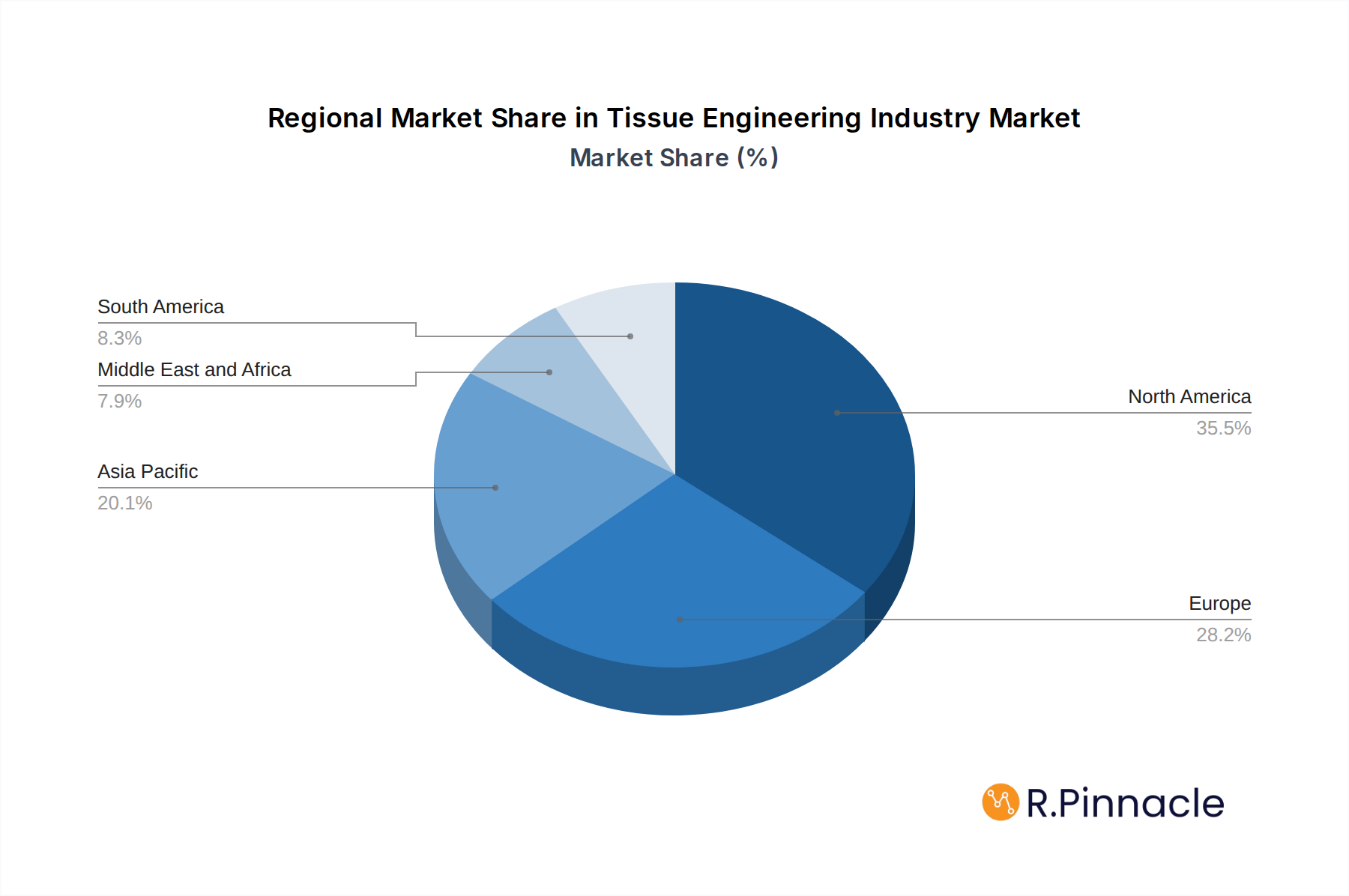

The market landscape is characterized by a dynamic interplay of technological innovation and strategic collaborations among leading companies such as Smith and Nephew, AbbVie Inc., Becton Dickinson and Company, and Zimmer Biomet. These players are actively investing in research and development to introduce novel tissue-engineered products and therapies. While the market presents substantial opportunities, certain restraints, such as the high cost of research and development, stringent regulatory hurdles, and the need for extensive clinical trials, may pose challenges. However, the overarching trend towards regenerative medicine as a sustainable and effective treatment modality for a wide range of medical conditions is expected to outweigh these limitations. The Asia Pacific region, with its burgeoning healthcare infrastructure and increasing patient access to advanced treatments, is projected to emerge as a significant growth frontier alongside established markets like North America and Europe.

Tissue Engineering Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the global Tissue Engineering Industry, a rapidly expanding sector poised for significant growth. Leveraging cutting-edge research and meticulously collected data, this report provides unparalleled insights into market dynamics, innovation trends, competitive landscapes, and future projections. The study spans from the historical period of 2019-2024, with a base year of 2025, and forecasts market trajectories through 2033. Understand the forces shaping the regenerative medicine future, from advanced biomaterials to life-changing therapeutic applications.

Tissue Engineering Industry Market Structure & Innovation Trends

The Tissue Engineering Industry exhibits a dynamic market structure characterized by a growing number of innovative players and increasing R&D investments. Market concentration is moderate, with a trend towards strategic collaborations and acquisitions as larger entities seek to integrate novel technologies. Key innovation drivers include advancements in biomaterial science, stem cell technologies, and 3D bioprinting, enabling the creation of more sophisticated and functional tissue constructs. Regulatory frameworks, while evolving to accommodate novel regenerative therapies, remain a critical factor influencing market entry and product development timelines. Product substitutes, such as traditional prosthetics and conventional surgical procedures, are gradually being displaced by the superior efficacy and regenerative potential of engineered tissues. End-user demographics are broadening, encompassing aging populations requiring restorative therapies and a growing demand for advanced medical treatments across diverse specialties. Merger and acquisition activities are expected to continue, with estimated deal values reaching billions, as companies strategically consolidate their positions and acquire valuable intellectual property.

- Market Share Analysis: Detailed company market shares are provided for key players.

- M&A Deal Values: Insights into the financial scale and strategic implications of recent and projected mergers and acquisitions.

- Innovation Drivers:

- Breakthroughs in biocompatible scaffolds.

- Development of patient-specific cell therapies.

- Advancements in high-resolution bioprinting techniques.

- Regulatory Landscape: Overview of FDA, EMA, and other regional regulatory pathways for regenerative medicines.

Tissue Engineering Industry Market Dynamics & Trends

The Tissue Engineering Industry is propelled by a confluence of potent growth drivers, technological disruptions, evolving consumer preferences, and intense competitive dynamics, projecting a robust Compound Annual Growth Rate (CAGR) that is estimated to be in the high single digits. The increasing global prevalence of chronic diseases, degenerative conditions, and traumatic injuries is a primary catalyst, fueling the demand for regenerative solutions that offer improved patient outcomes and quality of life. Technological advancements are at the forefront of this market's evolution. Innovations in material science are yielding advanced biocompatible and biodegradable scaffolds, while progress in stem cell biology and gene editing techniques are unlocking new therapeutic possibilities. Furthermore, the advent of 3D bioprinting is revolutionizing the fabrication of complex tissue structures, paving the way for patient-specific organoids and tissue grafts.

Consumer preferences are shifting towards less invasive and more effective treatments, with tissue engineering offering a paradigm shift from palliative care to true regeneration. Patients are increasingly seeking therapies that can restore function rather than merely manage symptoms. This heightened demand, coupled with a growing awareness of the potential of regenerative medicine, is driving market penetration across various therapeutic areas.

The competitive landscape is characterized by a mix of established medical device companies, burgeoning biotechnology firms, and academic research institutions. Strategic partnerships, licensing agreements, and acquisitions are common as companies strive to gain a competitive edge by acquiring novel technologies and expanding their product portfolios. The market is witnessing significant investment from venture capitalists and strategic corporate partners, underscoring the immense growth potential and therapeutic promise of this industry. Emerging markets are also presenting significant opportunities as healthcare infrastructure improves and the adoption of advanced medical technologies accelerates. The continuous refinement of existing products and the development of new applications for tissue-engineered solutions are further contributing to the market's dynamism.

- Market Penetration: Analysis of the increasing adoption rates of tissue-engineered products across various medical fields.

- Technological Disruptions:

- Impact of AI in drug discovery and tissue design.

- Advancements in microfluidics for tissue culture.

- Integration of nanotechnology for enhanced biomaterial properties.

- Consumer Preferences:

- Demand for personalized regenerative therapies.

- Preference for minimally invasive regenerative procedures.

- Growing interest in autologous cell-based treatments.

Dominant Regions & Segments in Tissue Engineering Industry

The Tissue Engineering Industry's global landscape is characterized by distinct regional strengths and dominant market segments, driven by a complex interplay of economic policies, healthcare infrastructure, research capabilities, and regulatory environments. North America, particularly the United States, currently leads the market, propelled by substantial investments in R&D, a high prevalence of chronic diseases, a well-established healthcare system, and favorable reimbursement policies for advanced medical treatments. The region boasts a robust ecosystem of leading research institutions and biotechnology companies actively engaged in pioneering tissue engineering innovations.

Geographically, the Orthopedics, Musculoskeletal & Spine segment stands out as a dominant application area. This dominance is attributed to the high incidence of sports injuries, degenerative joint diseases like osteoarthritis, and spinal conditions, which necessitate advanced restorative solutions. The availability of biocompatible implants, scaffolds for bone and cartilage regeneration, and tissue grafts for tendon and ligament repair has significantly driven the growth of this segment. Significant economic policies in these regions often support medical device innovation and patient access to cutting-edge treatments, further solidifying this segment's leadership.

From a material perspective, Synthetic Materials are witnessing significant traction. While Biologically Derived Materials continue to hold a strong position, synthetic alternatives offer advantages such as precise control over properties, scalability, and reduced immunogenicity, making them attractive for mass production and diverse applications. The development of advanced polymers, hydrogels, and ceramics tailored for specific tissue regeneration purposes is a key driver for this segment's growth. Economic incentives for domestic manufacturing of medical materials also contribute to the prominence of synthetic materials.

The Cardiology & Vascular segment, while perhaps not yet as mature as orthopedics, is exhibiting rapid growth. Advances in tissue-engineered heart valves, blood vessels, and cardiac patches are offering promising alternatives for patients with cardiovascular diseases. Technological advancements in biomaterials and cell culture techniques are crucial for this segment's progress. The increasing burden of cardiovascular diseases globally makes this a significant area for future market expansion.

Emerging regions like Europe and Asia-Pacific are rapidly catching up, driven by increasing healthcare expenditure, growing awareness of regenerative medicine, and supportive government initiatives to foster innovation. The Asia-Pacific region, in particular, presents immense growth potential due to its large population, increasing disposable incomes, and a burgeoning medical tourism industry.

- Leading Region: North America's dominance due to strong R&D, funding, and regulatory support.

- Dominant Segment (Application): Orthopedics, Musculoskeletal & Spine – driven by high incidence of injuries and degenerative diseases.

- Key Drivers: Advancements in cartilage and bone regeneration technologies.

- Economic Policies: Favorable reimbursement for orthopedic implants and procedures.

- Dominant Segment (Material): Synthetic Materials – offering tunable properties and scalability.

- Key Drivers: Development of advanced biodegradable polymers and hydrogels.

- Infrastructure: Robust manufacturing capabilities for medical-grade synthetic materials.

- High-Growth Segment (Application): Cardiology & Vascular – driven by unmet needs in heart and blood vessel repair.

- Technological Advancements: Innovations in bio-printed vascular grafts and cardiac patches.

- Emerging Regions: Asia-Pacific's rapid growth potential fueled by increasing healthcare investments.

Tissue Engineering Industry Product Innovations

Product innovations in the Tissue Engineering Industry are characterized by the development of advanced biomaterials, sophisticated cell-based therapies, and integrated biofabrication techniques. Companies are focusing on creating scaffolds that closely mimic the native extracellular matrix, enhancing cell adhesion, proliferation, and differentiation. The application of these innovations spans a wide range of medical needs, from regenerating damaged cartilage in orthopedics to developing functional cardiac tissues for cardiovascular repair. Competitive advantages are derived from enhanced efficacy, reduced invasiveness, and personalized treatment approaches.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Tissue Engineering Industry across key material and application segments. The Material segmentation includes Synthetic Materials, Biologically Derived Materials, and Others, each with distinct growth trajectories influenced by material science advancements and cost-effectiveness. The Application segmentation encompasses Orthopedics, Musculoskeletal & Spine, Neurology, Cardiology & Vascular, Skin & Integumentary, and Others. Growth projections and market sizes for each segment are provided, considering current market penetration and future demand drivers. Competitive dynamics within each segment are also detailed, highlighting key players and their strategies.

- Synthetic Materials: Expected to experience robust growth due to customization and scalability.

- Biologically Derived Materials: Continued relevance for specific applications requiring natural cues.

- Orthopedics, Musculoskeletal & Spine: Projected to maintain its leading position with ongoing advancements.

- Cardiology & Vascular: Anticipated to witness significant expansion driven by unmet clinical needs.

Key Drivers of Tissue Engineering Industry Growth

The growth of the Tissue Engineering Industry is primarily driven by a synergy of technological advancements, economic factors, and supportive regulatory environments. Key technological drivers include breakthroughs in biomaterials science, enabling the creation of scaffolds that precisely mimic native tissues, and advancements in cell biology, particularly in stem cell research and gene editing, which facilitate the development of more potent regenerative therapies. Economically, an aging global population and the increasing prevalence of chronic and degenerative diseases are creating a substantial unmet need for effective restorative treatments. Furthermore, rising healthcare expenditures and growing patient awareness of the benefits of regenerative medicine are stimulating market demand. Supportive regulatory frameworks, although evolving, are increasingly streamlining the approval process for innovative tissue-engineered products, thereby accelerating market entry.

Challenges in the Tissue Engineering Industry Sector

Despite its promising growth, the Tissue Engineering Industry faces significant challenges. Regulatory hurdles remain a primary concern, as the complexity of regenerative therapies necessitates rigorous safety and efficacy testing, often leading to lengthy and costly approval processes. Supply chain complexities, particularly for sourcing consistent and high-quality biological materials and ensuring the scalability of advanced manufacturing processes, can also pose significant restraints. Furthermore, high development costs and reimbursement uncertainties can impact market penetration and accessibility for certain patient populations. Competitive pressures from traditional treatment modalities and the need for extensive clinical validation also contribute to the barriers within this sector.

Emerging Opportunities in Tissue Engineering Industry

Emerging opportunities in the Tissue Engineering Industry are vast and driven by continuous innovation and evolving market needs. The development of off-the-shelf, allogeneic cell-based therapies presents a significant opportunity to overcome the limitations of autologous treatments. Advances in 3D bioprinting are opening doors for the creation of complex, vascularized tissues and organs, potentially addressing the organ donor shortage. The burgeoning field of regenerative aesthetics and personalized medicine also offers substantial growth potential, with an increasing demand for solutions that can repair and rejuvenate damaged tissues. Furthermore, exploring new therapeutic applications in areas like neurodegenerative diseases and metabolic disorders presents exciting avenues for future expansion.

Leading Players in the Tissue Engineering Industry Market

- Smith and Nephew

- Osiris Therapeutics

- AbbVie Inc

- Allergan

- Biotime Inc

- Becton Dickinson and Company

- C R Bard

- Athersys Inc

- Bio Tissue Technologies

- Organogenesis

- B Braun Melsungen AG

- Tissue Regenix Group plc

- Zimmer Biomet

- Acell Inc

- Integra Lifesciences

Key Developments in Tissue Engineering Industry Industry

- May 2022: Rousselot, Darling Ingredients' health brand, launched Quali-Pure HGP 2000, a new endotoxin-controlled, pharmaceutical-grade gelatin specifically designed for vaccines and wound healing applications.

- February 2022: Orthofix Medical launched a synthetic bioactive bone graft solution, Opus BA, for cervical and lumbar spine fusion procedures.

Future Outlook for Tissue Engineering Industry Market

The future outlook for the Tissue Engineering Industry is exceptionally positive, driven by continued technological advancements, expanding therapeutic applications, and increasing global healthcare investments. The convergence of biomaterials science, stem cell technology, and advanced manufacturing techniques will unlock novel regenerative solutions for a wide array of unmet medical needs. Strategic collaborations, mergers, and acquisitions will likely shape the competitive landscape, fostering innovation and accelerating market penetration. As regulatory pathways become more defined and reimbursement models evolve, the accessibility and adoption of tissue-engineered therapies are expected to surge, transforming patient care and improving health outcomes worldwide. The industry is poised to witness a significant increase in market value, reaching billions in the coming years.

Tissue Engineering Industry Segmentation

-

1. Material

- 1.1. Synthetic Materials

- 1.2. Biologically Derived Materials

- 1.3. Others

-

2. Application

- 2.1. Orthopedics

- 2.2. Musculoskeletal & Spine

- 2.3. Neurology

- 2.4. Cardiology & Vascular

- 2.5. Skin & Integumentary

- 2.6. Others

Tissue Engineering Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Tissue Engineering Industry Regional Market Share

Geographic Coverage of Tissue Engineering Industry

Tissue Engineering Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Synthetic Materials

- 5.1.2. Biologically Derived Materials

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Orthopedics

- 5.2.2. Musculoskeletal & Spine

- 5.2.3. Neurology

- 5.2.4. Cardiology & Vascular

- 5.2.5. Skin & Integumentary

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Tissue Engineering Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Synthetic Materials

- 6.1.2. Biologically Derived Materials

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Orthopedics

- 6.2.2. Musculoskeletal & Spine

- 6.2.3. Neurology

- 6.2.4. Cardiology & Vascular

- 6.2.5. Skin & Integumentary

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. North America Tissue Engineering Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Synthetic Materials

- 7.1.2. Biologically Derived Materials

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Orthopedics

- 7.2.2. Musculoskeletal & Spine

- 7.2.3. Neurology

- 7.2.4. Cardiology & Vascular

- 7.2.5. Skin & Integumentary

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Europe Tissue Engineering Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Synthetic Materials

- 8.1.2. Biologically Derived Materials

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Orthopedics

- 8.2.2. Musculoskeletal & Spine

- 8.2.3. Neurology

- 8.2.4. Cardiology & Vascular

- 8.2.5. Skin & Integumentary

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Asia Pacific Tissue Engineering Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Synthetic Materials

- 9.1.2. Biologically Derived Materials

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Orthopedics

- 9.2.2. Musculoskeletal & Spine

- 9.2.3. Neurology

- 9.2.4. Cardiology & Vascular

- 9.2.5. Skin & Integumentary

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Middle East and Africa Tissue Engineering Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Synthetic Materials

- 10.1.2. Biologically Derived Materials

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Orthopedics

- 10.2.2. Musculoskeletal & Spine

- 10.2.3. Neurology

- 10.2.4. Cardiology & Vascular

- 10.2.5. Skin & Integumentary

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. South America Tissue Engineering Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Synthetic Materials

- 11.1.2. Biologically Derived Materials

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Orthopedics

- 11.2.2. Musculoskeletal & Spine

- 11.2.3. Neurology

- 11.2.4. Cardiology & Vascular

- 11.2.5. Skin & Integumentary

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smith and Nephew (Osiris Therapeutics)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 AbbVie Inc (Allergan)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Biotime Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Becton Dickinson and Company (C R Bard)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Athersys Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bio Tissue Technologies

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Organogenesis

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 B Braun Melsungen AG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Tissue Regenix Group plc*List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Zimmer Biomet

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Acell Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Integra Lifesciences

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Smith and Nephew (Osiris Therapeutics)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Tissue Engineering Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Tissue Engineering Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Tissue Engineering Industry Revenue (billion), by Material 2025 & 2033

- Figure 4: North America Tissue Engineering Industry Volume (K Unit), by Material 2025 & 2033

- Figure 5: North America Tissue Engineering Industry Revenue Share (%), by Material 2025 & 2033

- Figure 6: North America Tissue Engineering Industry Volume Share (%), by Material 2025 & 2033

- Figure 7: North America Tissue Engineering Industry Revenue (billion), by Application 2025 & 2033

- Figure 8: North America Tissue Engineering Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Tissue Engineering Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Tissue Engineering Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Tissue Engineering Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Tissue Engineering Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Tissue Engineering Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Tissue Engineering Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Tissue Engineering Industry Revenue (billion), by Material 2025 & 2033

- Figure 16: Europe Tissue Engineering Industry Volume (K Unit), by Material 2025 & 2033

- Figure 17: Europe Tissue Engineering Industry Revenue Share (%), by Material 2025 & 2033

- Figure 18: Europe Tissue Engineering Industry Volume Share (%), by Material 2025 & 2033

- Figure 19: Europe Tissue Engineering Industry Revenue (billion), by Application 2025 & 2033

- Figure 20: Europe Tissue Engineering Industry Volume (K Unit), by Application 2025 & 2033

- Figure 21: Europe Tissue Engineering Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Tissue Engineering Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: Europe Tissue Engineering Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Tissue Engineering Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Tissue Engineering Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Tissue Engineering Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Tissue Engineering Industry Revenue (billion), by Material 2025 & 2033

- Figure 28: Asia Pacific Tissue Engineering Industry Volume (K Unit), by Material 2025 & 2033

- Figure 29: Asia Pacific Tissue Engineering Industry Revenue Share (%), by Material 2025 & 2033

- Figure 30: Asia Pacific Tissue Engineering Industry Volume Share (%), by Material 2025 & 2033

- Figure 31: Asia Pacific Tissue Engineering Industry Revenue (billion), by Application 2025 & 2033

- Figure 32: Asia Pacific Tissue Engineering Industry Volume (K Unit), by Application 2025 & 2033

- Figure 33: Asia Pacific Tissue Engineering Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Asia Pacific Tissue Engineering Industry Volume Share (%), by Application 2025 & 2033

- Figure 35: Asia Pacific Tissue Engineering Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Pacific Tissue Engineering Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Tissue Engineering Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Tissue Engineering Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Tissue Engineering Industry Revenue (billion), by Material 2025 & 2033

- Figure 40: Middle East and Africa Tissue Engineering Industry Volume (K Unit), by Material 2025 & 2033

- Figure 41: Middle East and Africa Tissue Engineering Industry Revenue Share (%), by Material 2025 & 2033

- Figure 42: Middle East and Africa Tissue Engineering Industry Volume Share (%), by Material 2025 & 2033

- Figure 43: Middle East and Africa Tissue Engineering Industry Revenue (billion), by Application 2025 & 2033

- Figure 44: Middle East and Africa Tissue Engineering Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Middle East and Africa Tissue Engineering Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Middle East and Africa Tissue Engineering Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Middle East and Africa Tissue Engineering Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East and Africa Tissue Engineering Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Tissue Engineering Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Tissue Engineering Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Tissue Engineering Industry Revenue (billion), by Material 2025 & 2033

- Figure 52: South America Tissue Engineering Industry Volume (K Unit), by Material 2025 & 2033

- Figure 53: South America Tissue Engineering Industry Revenue Share (%), by Material 2025 & 2033

- Figure 54: South America Tissue Engineering Industry Volume Share (%), by Material 2025 & 2033

- Figure 55: South America Tissue Engineering Industry Revenue (billion), by Application 2025 & 2033

- Figure 56: South America Tissue Engineering Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: South America Tissue Engineering Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: South America Tissue Engineering Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: South America Tissue Engineering Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: South America Tissue Engineering Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Tissue Engineering Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Tissue Engineering Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 3: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Tissue Engineering Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Tissue Engineering Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 8: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 9: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Global Tissue Engineering Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Tissue Engineering Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 20: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 21: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Global Tissue Engineering Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Tissue Engineering Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Germany Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: France Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Italy Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Spain Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 38: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 39: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 40: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Global Tissue Engineering Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Global Tissue Engineering Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: China Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Japan Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: India Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Australia Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: South Korea Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 56: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 57: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 58: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 59: Global Tissue Engineering Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Tissue Engineering Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: GCC Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: South Africa Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Tissue Engineering Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 68: Global Tissue Engineering Industry Volume K Unit Forecast, by Material 2020 & 2033

- Table 69: Global Tissue Engineering Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 70: Global Tissue Engineering Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 71: Global Tissue Engineering Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 72: Global Tissue Engineering Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: Brazil Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Argentina Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Tissue Engineering Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Tissue Engineering Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Tissue Engineering Industry?

The projected CAGR is approximately 14.6%.

2. Which companies are prominent players in the Tissue Engineering Industry?

Key companies in the market include Smith and Nephew (Osiris Therapeutics), AbbVie Inc (Allergan), Biotime Inc, Becton Dickinson and Company (C R Bard), Athersys Inc, Bio Tissue Technologies, Organogenesis, B Braun Melsungen AG, Tissue Regenix Group plc*List Not Exhaustive, Zimmer Biomet, Acell Inc, Integra Lifesciences.

3. What are the main segments of the Tissue Engineering Industry?

The market segments include Material, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.75 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase Incidences of Chronic Diseases. Road Accidents. and Trauma Injuries; Technological Advancements in 3D Tissue Engineering; Increase in Funding and Research for Tissue Regeneration.

6. What are the notable trends driving market growth?

Orthopedic Segment is Expected to Show the Fastest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Treatments Related to Tissue Engineering; Lack of Awareness Regarding Tissue Engineering.

8. Can you provide examples of recent developments in the market?

In May 2022, Rousselot, Darling Ingredients' health brand, has launched Quali-Pure HGP 2000, a new endotoxin-controlled, pharmaceutical-grade gelatin specifically designed for vaccines and wound healing applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Tissue Engineering Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Tissue Engineering Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Tissue Engineering Industry?

To stay informed about further developments, trends, and reports in the Tissue Engineering Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence