Key Insights

The UK aviation industry, encompassing commercial aviation and other segments like general aviation and helicopter operations, presents a dynamic landscape with significant growth potential. While the provided CAGR of 0.04 suggests relatively modest growth, this figure likely underrepresents the sector's complexity. The base year of 2025 suggests a recovery from the pandemic's impact, and future growth will depend on several interconnected factors. Strong drivers include increasing passenger numbers, particularly on domestic and short-haul European routes, fueled by a growing tourism sector and business travel. Furthermore, advancements in aircraft technology, focusing on fuel efficiency and reduced emissions, will influence market expansion. However, significant restraints exist, such as rising fuel costs, stringent environmental regulations (particularly concerning carbon emissions), and potential disruptions from geopolitical instability. The industry's segmentation between commercial aviation (dominating the market) and other segments (including private aviation, air freight, and maintenance services) provides insights into diverse growth trajectories. Major players like Boeing, Airbus, and Embraer significantly influence the commercial sector, while smaller companies dominate the general aviation and helicopter markets.

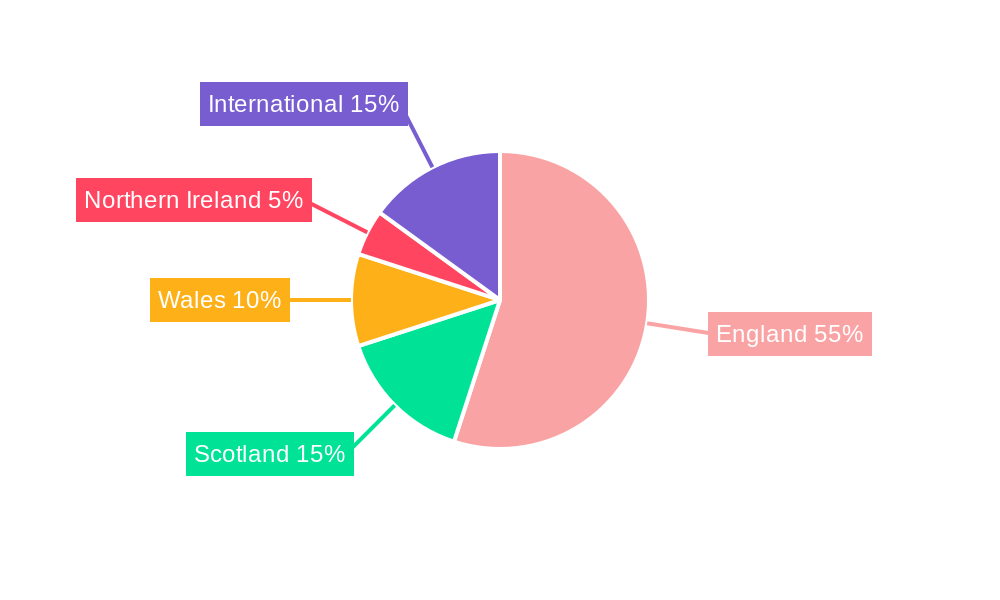

The regional data focusing on the UK (England, Wales, Scotland, Northern Ireland) indicates strong internal demand. However, Brexit's impact on air travel arrangements with the EU remains a factor affecting international connectivity. The forecast period (2025-2033) suggests a gradual but steady expansion, driven primarily by the recovery and growth of commercial aviation. The historical period (2019-2024) provides a valuable baseline for understanding the impact of the pandemic and the subsequent recovery. Successfully navigating the environmental challenges and maintaining robust international partnerships will be crucial for maximizing the industry's potential over the next decade. A deeper analysis into specific sub-segments and their growth rates would provide a more granular understanding of the market's future. Given the limited data, projections are based on reasonable assumptions and industry trends.

UK Aviation Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the UK aviation industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with a base year of 2025 and a forecast period spanning 2025-2033. The report leverages extensive data from the historical period (2019-2024) to provide accurate and reliable projections. Expect detailed breakdowns of market segments, key players, and emerging trends, all presented in a clear and actionable format. Discover the potential for growth and identify key challenges facing this dynamic sector. The report also includes substantial financial data, using Millions (£) for all values where available; otherwise, estimated figures are provided.

UK Aviation Industry Market Structure & Innovation Trends

The UK aviation industry exhibits a moderately concentrated market structure, with a few major players dominating specific segments. Market share data for 2024 suggests Airbus SE and The Boeing Company hold the largest shares in commercial aviation, while regional variations exist depending on the aircraft type (e.g., helicopters). Innovation is driven by several factors:

- Stringent Regulatory Frameworks: The UK's Civil Aviation Authority (CAA) plays a key role in shaping safety standards and technological advancements.

- Sustainability Concerns: Growing pressure to reduce carbon emissions is driving innovation in fuel-efficient aircraft and alternative propulsion systems.

- Technological Advancements: The integration of AI, big data analytics, and advanced materials is transforming aircraft design and operations.

- M&A Activity: Consolidation through mergers and acquisitions (M&A) is reshaping the competitive landscape. While precise deal values for 2019-2024 in the UK are difficult to completely capture (xx Million estimated), notable transactions have impacted market dynamics significantly.

Product substitution is limited in some segments (e.g., large commercial aircraft) but more prevalent in others (e.g., general aviation), due to technological disruption and evolving customer preferences. End-user demographics encompass diverse groups, from airlines and freight companies to private jet owners and military operators. The report includes detailed analysis of these segments and their distinct needs.

UK Aviation Industry Market Dynamics & Trends

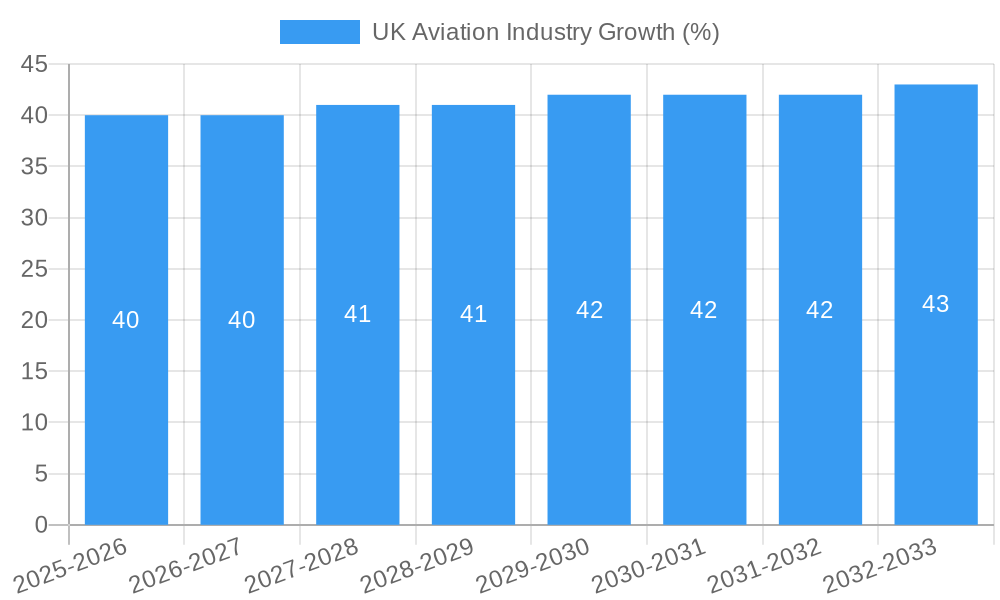

The UK aviation market experienced significant fluctuation between 2019 and 2024, notably impacted by the COVID-19 pandemic. However, the market is projected to recover and exhibit a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by:

- Increased Passenger Traffic: Post-pandemic recovery in air travel is driving demand for commercial aircraft.

- Growth in E-commerce: The rise of e-commerce fuels the demand for air freight services.

- Government Investments: Infrastructure development and supportive government policies are expected to contribute to the industry’s growth.

- Technological Disruptions: Innovations in aircraft design, propulsion systems, and air traffic management are enhancing efficiency and sustainability.

Competitive dynamics are characterized by intense rivalry among major players, with market penetration strategies varying across segments. The report provides detailed analysis of market share dynamics, competitive strategies, and future growth prospects.

Dominant Regions & Segments in UK Aviation Industry

The UK's aviation industry is primarily concentrated within England, driven by its advanced infrastructure including major airports like Heathrow and Gatwick. While Scotland and Wales have regional airports, these contribute less significantly to overall market value in this study. Scotland's focus on offshore oil and gas operations could impact helicopter-based transport and maintenance, however, specific market share numbers are unavailable (xx% estimated).

Key Drivers for England's Dominance:

- Robust Infrastructure: Extensive airport network and well-developed air traffic management systems.

- Strong Economic Base: London's status as a global financial center drives substantial business travel and air freight.

- Skilled Workforce: A large pool of qualified aviation professionals supports industry operations.

Commercial Aviation constitutes a much larger segment compared to “Others”. Further analysis regarding the relative size comparison requires more extensive internal data.

UK Aviation Industry Product Innovations

Recent years have witnessed significant product innovations, including the development of more fuel-efficient aircraft, the integration of advanced avionics, and the exploration of electric and hybrid-electric propulsion systems. These innovations aim to address environmental concerns, enhance operational efficiency, and improve passenger experience. The market is also seeing growth in the development of unmanned aerial vehicles (UAVs) and advanced air mobility (AAM) solutions, which have the potential to transform various sectors.

Report Scope & Segmentation Analysis

This report segments the UK aviation market by aircraft type:

Commercial Aviation: This segment includes large passenger aircraft, regional jets, and turboprops. The market size is estimated at xx Million in 2025, projected to reach xx Million by 2033. Competitive dynamics are intense, dominated by major aircraft manufacturers.

Others: This segment encompasses general aviation aircraft, helicopters, military aircraft, and other specialized aircraft types. The market size is projected to increase from xx Million in 2025 to xx Million by 2033, with significant growth opportunities in areas like UAVs and AAM. This segment demonstrates high diversity, with a wide array of manufacturers and applications.

Key Drivers of UK Aviation Industry Growth

The UK aviation industry's growth is driven by several factors:

- Technological advancements: Fuel-efficient aircraft and advanced air traffic management systems are enhancing efficiency.

- Economic growth: A growing economy boosts passenger and cargo traffic.

- Government support: Favorable regulatory frameworks and investments in airport infrastructure create a conducive environment for industry growth.

Challenges in the UK Aviation Industry Sector

Several challenges hinder UK aviation industry growth:

- Brexit-related uncertainties: Changes in regulations and trade agreements pose complexities for UK airlines.

- Environmental concerns: Pressure to reduce carbon emissions requires significant investments in sustainable technologies.

- Supply chain disruptions: Global supply chain disruptions and labor shortages impacting the industry's ability to deliver services.

Emerging Opportunities in UK Aviation Industry

The UK aviation industry is poised for growth in several areas:

- Sustainable aviation fuels (SAFs): Growing investment in SAFs presents a significant opportunity to reduce the sector's carbon footprint.

- Advanced Air Mobility (AAM): The development of electric vertical takeoff and landing (eVTOL) aircraft offers the potential for new services and applications.

- Airport expansion and modernization: Planned improvements to airport infrastructure will enhance capacity and efficiency.

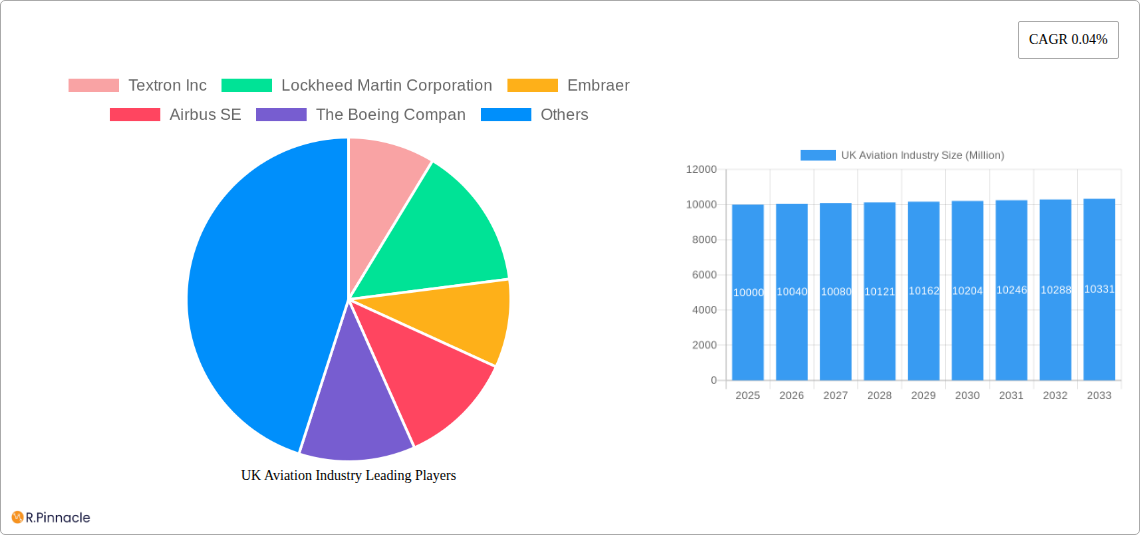

Leading Players in the UK Aviation Industry Market

- Textron Inc

- Lockheed Martin Corporation

- Embraer

- Airbus SE

- The Boeing Company

- Robinson Helicopter Company Inc

- MD Helicopters LLC

- Cirrus Design Corporation

- Leonardo S p A

- Bombardier Inc

Key Developments in UK Aviation Industry Industry

- December 2022: The US Army awarded Textron Inc.'s Bell unit a contract to supply next-generation helicopters, impacting the helicopter market segment.

- November 2022: Bell Textron Inc. secured a deal to sell 10 Bell 505 helicopters to the Royal Jordanian Air Force, boosting Bell's international sales.

- July 2022: EmbraerX established a presence in the Netherlands, signaling its commitment to innovation and sustainable aviation technology.

Future Outlook for UK Aviation Industry Market

The UK aviation industry is expected to experience robust growth over the forecast period, driven by technological advancements, increased passenger demand, and supportive government policies. Strategic opportunities exist in sustainable aviation fuels, advanced air mobility, and airport infrastructure development. The industry will need to address challenges related to environmental sustainability, supply chain resilience, and Brexit-related uncertainties to realize its full potential.

UK Aviation Industry Segmentation

-

1. Aircraft Type

-

1.1. Commercial Aviation

-

1.1.1. By Sub Aircraft Type

- 1.1.1.1. Freighter Aircraft

-

1.1.1.2. Passenger Aircraft

-

1.1.1.2.1. By Body Type

- 1.1.1.2.1.1. Narrowbody Aircraft

- 1.1.1.2.1.2. Widebody Aircraft

-

1.1.1.2.1. By Body Type

-

1.1.1. By Sub Aircraft Type

-

1.2. General Aviation

-

1.2.1. Business Jets

- 1.2.1.1. Large Jet

- 1.2.1.2. Light Jet

- 1.2.1.3. Mid-Size Jet

- 1.2.2. Piston Fixed-Wing Aircraft

- 1.2.3. Others

-

1.2.1. Business Jets

-

1.3. Military Aviation

- 1.3.1. Multi-Role Aircraft

- 1.3.2. Training Aircraft

- 1.3.3. Transport Aircraft

-

1.3.4. Rotorcraft

- 1.3.4.1. Multi-Mission Helicopter

- 1.3.4.2. Transport Helicopter

-

1.1. Commercial Aviation

UK Aviation Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 0.04% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. By Sub Aircraft Type

- 5.1.1.1.1. Freighter Aircraft

- 5.1.1.1.2. Passenger Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1.2.1.1. Narrowbody Aircraft

- 5.1.1.1.2.1.2. Widebody Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1. By Sub Aircraft Type

- 5.1.2. General Aviation

- 5.1.2.1. Business Jets

- 5.1.2.1.1. Large Jet

- 5.1.2.1.2. Light Jet

- 5.1.2.1.3. Mid-Size Jet

- 5.1.2.2. Piston Fixed-Wing Aircraft

- 5.1.2.3. Others

- 5.1.2.1. Business Jets

- 5.1.3. Military Aviation

- 5.1.3.1. Multi-Role Aircraft

- 5.1.3.2. Training Aircraft

- 5.1.3.3. Transport Aircraft

- 5.1.3.4. Rotorcraft

- 5.1.3.4.1. Multi-Mission Helicopter

- 5.1.3.4.2. Transport Helicopter

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. North America UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. By Sub Aircraft Type

- 6.1.1.1.1. Freighter Aircraft

- 6.1.1.1.2. Passenger Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1.2.1.1. Narrowbody Aircraft

- 6.1.1.1.2.1.2. Widebody Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1. By Sub Aircraft Type

- 6.1.2. General Aviation

- 6.1.2.1. Business Jets

- 6.1.2.1.1. Large Jet

- 6.1.2.1.2. Light Jet

- 6.1.2.1.3. Mid-Size Jet

- 6.1.2.2. Piston Fixed-Wing Aircraft

- 6.1.2.3. Others

- 6.1.2.1. Business Jets

- 6.1.3. Military Aviation

- 6.1.3.1. Multi-Role Aircraft

- 6.1.3.2. Training Aircraft

- 6.1.3.3. Transport Aircraft

- 6.1.3.4. Rotorcraft

- 6.1.3.4.1. Multi-Mission Helicopter

- 6.1.3.4.2. Transport Helicopter

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. South America UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.1.1. Commercial Aviation

- 7.1.1.1. By Sub Aircraft Type

- 7.1.1.1.1. Freighter Aircraft

- 7.1.1.1.2. Passenger Aircraft

- 7.1.1.1.2.1. By Body Type

- 7.1.1.1.2.1.1. Narrowbody Aircraft

- 7.1.1.1.2.1.2. Widebody Aircraft

- 7.1.1.1.2.1. By Body Type

- 7.1.1.1. By Sub Aircraft Type

- 7.1.2. General Aviation

- 7.1.2.1. Business Jets

- 7.1.2.1.1. Large Jet

- 7.1.2.1.2. Light Jet

- 7.1.2.1.3. Mid-Size Jet

- 7.1.2.2. Piston Fixed-Wing Aircraft

- 7.1.2.3. Others

- 7.1.2.1. Business Jets

- 7.1.3. Military Aviation

- 7.1.3.1. Multi-Role Aircraft

- 7.1.3.2. Training Aircraft

- 7.1.3.3. Transport Aircraft

- 7.1.3.4. Rotorcraft

- 7.1.3.4.1. Multi-Mission Helicopter

- 7.1.3.4.2. Transport Helicopter

- 7.1.1. Commercial Aviation

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8. Europe UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.1.1. Commercial Aviation

- 8.1.1.1. By Sub Aircraft Type

- 8.1.1.1.1. Freighter Aircraft

- 8.1.1.1.2. Passenger Aircraft

- 8.1.1.1.2.1. By Body Type

- 8.1.1.1.2.1.1. Narrowbody Aircraft

- 8.1.1.1.2.1.2. Widebody Aircraft

- 8.1.1.1.2.1. By Body Type

- 8.1.1.1. By Sub Aircraft Type

- 8.1.2. General Aviation

- 8.1.2.1. Business Jets

- 8.1.2.1.1. Large Jet

- 8.1.2.1.2. Light Jet

- 8.1.2.1.3. Mid-Size Jet

- 8.1.2.2. Piston Fixed-Wing Aircraft

- 8.1.2.3. Others

- 8.1.2.1. Business Jets

- 8.1.3. Military Aviation

- 8.1.3.1. Multi-Role Aircraft

- 8.1.3.2. Training Aircraft

- 8.1.3.3. Transport Aircraft

- 8.1.3.4. Rotorcraft

- 8.1.3.4.1. Multi-Mission Helicopter

- 8.1.3.4.2. Transport Helicopter

- 8.1.1. Commercial Aviation

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9. Middle East & Africa UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.1.1. Commercial Aviation

- 9.1.1.1. By Sub Aircraft Type

- 9.1.1.1.1. Freighter Aircraft

- 9.1.1.1.2. Passenger Aircraft

- 9.1.1.1.2.1. By Body Type

- 9.1.1.1.2.1.1. Narrowbody Aircraft

- 9.1.1.1.2.1.2. Widebody Aircraft

- 9.1.1.1.2.1. By Body Type

- 9.1.1.1. By Sub Aircraft Type

- 9.1.2. General Aviation

- 9.1.2.1. Business Jets

- 9.1.2.1.1. Large Jet

- 9.1.2.1.2. Light Jet

- 9.1.2.1.3. Mid-Size Jet

- 9.1.2.2. Piston Fixed-Wing Aircraft

- 9.1.2.3. Others

- 9.1.2.1. Business Jets

- 9.1.3. Military Aviation

- 9.1.3.1. Multi-Role Aircraft

- 9.1.3.2. Training Aircraft

- 9.1.3.3. Transport Aircraft

- 9.1.3.4. Rotorcraft

- 9.1.3.4.1. Multi-Mission Helicopter

- 9.1.3.4.2. Transport Helicopter

- 9.1.1. Commercial Aviation

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10. Asia Pacific UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.1.1. Commercial Aviation

- 10.1.1.1. By Sub Aircraft Type

- 10.1.1.1.1. Freighter Aircraft

- 10.1.1.1.2. Passenger Aircraft

- 10.1.1.1.2.1. By Body Type

- 10.1.1.1.2.1.1. Narrowbody Aircraft

- 10.1.1.1.2.1.2. Widebody Aircraft

- 10.1.1.1.2.1. By Body Type

- 10.1.1.1. By Sub Aircraft Type

- 10.1.2. General Aviation

- 10.1.2.1. Business Jets

- 10.1.2.1.1. Large Jet

- 10.1.2.1.2. Light Jet

- 10.1.2.1.3. Mid-Size Jet

- 10.1.2.2. Piston Fixed-Wing Aircraft

- 10.1.2.3. Others

- 10.1.2.1. Business Jets

- 10.1.3. Military Aviation

- 10.1.3.1. Multi-Role Aircraft

- 10.1.3.2. Training Aircraft

- 10.1.3.3. Transport Aircraft

- 10.1.3.4. Rotorcraft

- 10.1.3.4.1. Multi-Mission Helicopter

- 10.1.3.4.2. Transport Helicopter

- 10.1.1. Commercial Aviation

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11. England UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 12. Wales UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 13. Scotland UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 14. Northern UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 15. Ireland UK Aviation Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Textron Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Lockheed Martin Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Embraer

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Airbus SE

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 The Boeing Compan

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Robinson Helicopter Company Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 MD Helicopters LLC

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Cirrus Design Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Leonardo S p A

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Bombardier Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Textron Inc

List of Figures

- Figure 1: Global UK Aviation Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: United kingdom Region UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: United kingdom Region UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America UK Aviation Industry Revenue (Million), by Aircraft Type 2024 & 2032

- Figure 5: North America UK Aviation Industry Revenue Share (%), by Aircraft Type 2024 & 2032

- Figure 6: North America UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: North America UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America UK Aviation Industry Revenue (Million), by Aircraft Type 2024 & 2032

- Figure 9: South America UK Aviation Industry Revenue Share (%), by Aircraft Type 2024 & 2032

- Figure 10: South America UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: Europe UK Aviation Industry Revenue (Million), by Aircraft Type 2024 & 2032

- Figure 13: Europe UK Aviation Industry Revenue Share (%), by Aircraft Type 2024 & 2032

- Figure 14: Europe UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: Europe UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Middle East & Africa UK Aviation Industry Revenue (Million), by Aircraft Type 2024 & 2032

- Figure 17: Middle East & Africa UK Aviation Industry Revenue Share (%), by Aircraft Type 2024 & 2032

- Figure 18: Middle East & Africa UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Middle East & Africa UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific UK Aviation Industry Revenue (Million), by Aircraft Type 2024 & 2032

- Figure 21: Asia Pacific UK Aviation Industry Revenue Share (%), by Aircraft Type 2024 & 2032

- Figure 22: Asia Pacific UK Aviation Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific UK Aviation Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global UK Aviation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 3: Global UK Aviation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: England UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Wales UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Scotland UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Northern UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Ireland UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 11: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: United States UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Canada UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Mexico UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 16: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: Brazil UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Argentina UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Rest of South America UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 21: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: United Kingdom UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Germany UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: France UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Italy UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Spain UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Russia UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Benelux UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Nordics UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of Europe UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 32: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 33: Turkey UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Israel UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: GCC UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: North Africa UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: South Africa UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of Middle East & Africa UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global UK Aviation Industry Revenue Million Forecast, by Aircraft Type 2019 & 2032

- Table 40: Global UK Aviation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: China UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: India UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Japan UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: South Korea UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Oceania UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific UK Aviation Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Aviation Industry?

The projected CAGR is approximately 0.04%.

2. Which companies are prominent players in the UK Aviation Industry?

Key companies in the market include Textron Inc, Lockheed Martin Corporation, Embraer, Airbus SE, The Boeing Compan, Robinson Helicopter Company Inc, MD Helicopters LLC, Cirrus Design Corporation, Leonardo S p A, Bombardier Inc.

3. What are the main segments of the UK Aviation Industry?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

December 2022: The US Army was awarded a contract to supply next-generation helicopters to Textron Inc.'s Bell unit. The Army`s "Future Vertical Lift" competition aimed at finding a replacement as the Army looks to retire more than 2,000 medium-class UH-60 Black Hawk utility helicopters.November 2022: Bell Textron Inc., a company of Textron Inc., forged an agreement to sell 10 Bell 505 helicopters to the Royal Jordanian Air Force (RJAF) at the Forces Exhibition and Conference. Combat Air Force (SOFEX) in Aqaba, Jordan.July 2022: EmbraerX establishes a presence in the Netherlands to further the development of innovative and sustainable aviation technology.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Aviation Industry?

To stay informed about further developments, trends, and reports in the UK Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence