Key Insights

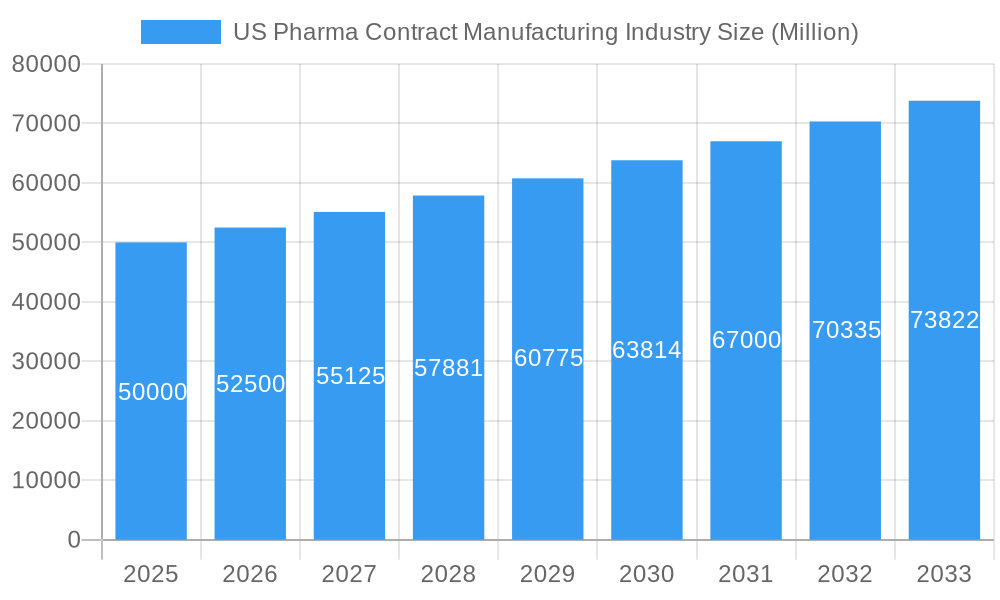

The US Pharma Contract Manufacturing (PCM) market is experiencing robust growth, driven by several key factors. The increasing complexity of drug development, coupled with rising R&D costs, is pushing pharmaceutical companies to outsource manufacturing activities to specialized contract manufacturers. This trend is further amplified by the growing demand for biologics, advanced therapies, and personalized medicines, all of which require sophisticated manufacturing capabilities beyond the reach of many smaller pharmaceutical firms. The market's segmentation reveals a strong focus on Active Pharmaceutical Ingredient (API) manufacturing, High Potency API (HPAPI) and Finished Dosage Formulation (FDF) development and manufacturing, and Injectable Dose Formulation including secondary packaging. This indicates a diverse range of services offered within the PCM landscape, catering to various stages of drug development and production. Major players like Thermo Fisher Scientific (Patheon), Siegfried, Aenova, Lonza, and Catalent are consolidating their positions through strategic acquisitions and technological advancements, leading to increased market concentration. The Northeast region of the US likely holds the largest market share due to its established pharmaceutical infrastructure and high concentration of pharmaceutical companies. Given a CAGR of 5.00% and a base year value of XX million (let's assume a plausible figure of $50 billion for 2025 based on industry reports), the market is poised for significant expansion through 2033.

US Pharma Contract Manufacturing Industry Market Size (In Billion)

The competitive landscape is dynamic, with both large multinational corporations and specialized smaller firms vying for market share. Successful companies are those that offer a broad range of services, possess advanced technological capabilities, comply rigorously with regulatory requirements (like FDA guidelines), and maintain robust quality control systems. Growth constraints may include fluctuating raw material prices, capacity limitations, regulatory hurdles, and increasing competition. However, the long-term outlook remains positive, fueled by ongoing innovation in drug development and the continued outsourcing trend among pharmaceutical companies. The focus on HPAPI and injectable formulations signals a move towards more complex and higher-value pharmaceutical products, which will further drive market growth and specialization within the industry.

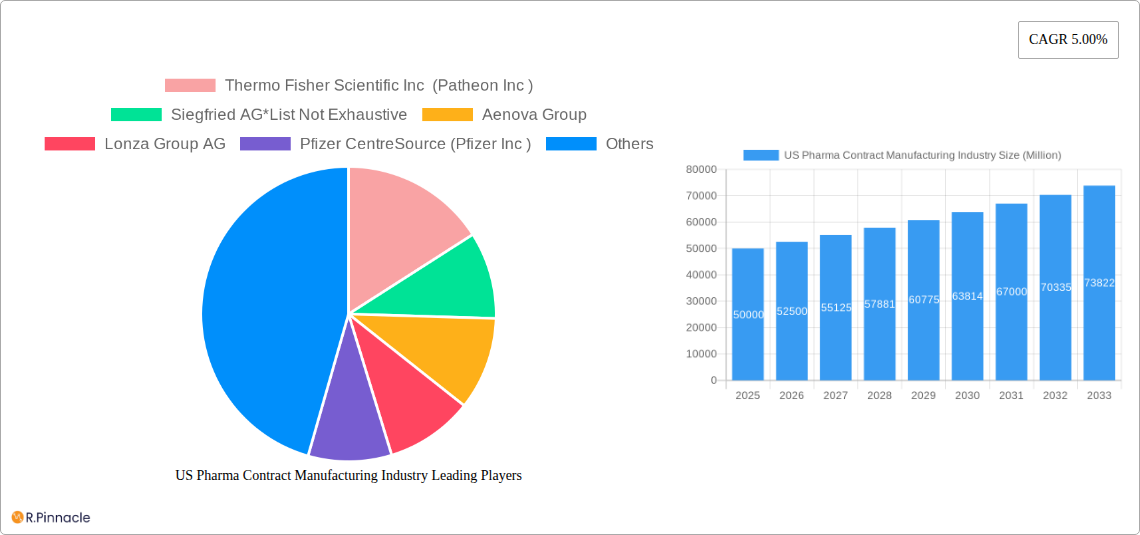

US Pharma Contract Manufacturing Industry Company Market Share

US Pharma Contract Manufacturing Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the US Pharma Contract Manufacturing industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a focus on 2025, this report unveils market dynamics, growth drivers, challenges, and future opportunities within this vital sector. The study encompasses key segments, leading players, and emerging trends, providing a 360° view of this dynamic landscape.

US Pharma Contract Manufacturing Industry Market Structure & Innovation Trends

The US Pharma Contract Manufacturing market exhibits a moderately concentrated structure, with several large players holding significant market share. Thermo Fisher Scientific Inc (Patheon Inc), Siegfried AG, Aenova Group, Lonza Group AG, and Catalent Inc are among the key players, collectively accounting for an estimated xx% of the market in 2025. Market share fluctuations are influenced by factors such as M&A activity, technological advancements, and regulatory changes. Innovation is driven by the need for advanced drug delivery systems, personalized medicine, and increasing demand for complex biologics. Stringent regulatory frameworks, including those from the FDA, significantly impact industry practices and product development. The industry faces competitive pressure from both domestic and international players, while the high cost of drug development and manufacturing necessitates ongoing innovation for cost-effectiveness. M&A activity has been robust in recent years, with deals valued at an estimated $xx Million in 2024 alone. This consolidation reflects the industry's pursuit of scale, technological capabilities, and broader service offerings.

- Market Concentration: Moderately concentrated, with top 5 players holding xx% market share (2025).

- Innovation Drivers: Advanced drug delivery, personalized medicine, complex biologics.

- Regulatory Landscape: Stringent FDA regulations drive quality and safety standards.

- M&A Activity: Significant M&A activity in recent years, with total deal values estimated at $xx Million in 2024.

US Pharma Contract Manufacturing Industry Market Dynamics & Trends

The US Pharma Contract Manufacturing market is experiencing robust and sustained growth, propelled by a confluence of critical factors. The escalating prevalence of chronic diseases globally necessitates a continuous pipeline of pharmaceutical treatments, directly fueling demand for contract manufacturing services. Furthermore, substantial increases in Research and Development (R&D) expenditure by pharmaceutical giants and emerging biotech firms translate into more drug candidates requiring efficient and scalable production. A discernible trend towards outsourcing manufacturing activities remains a significant growth driver, allowing pharma companies to focus on core competencies like drug discovery and commercialization while leveraging the specialized expertise and infrastructure of Contract Development and Manufacturing Organizations (CDMOs).

The market is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025-2033), with an estimated market valuation to reach $XX Million by 2033. Technological advancements are revolutionizing the landscape. Innovations such as advanced automation, AI-driven process optimization for enhanced yield and quality, and the transition towards continuous manufacturing methodologies are significantly boosting production efficiency, reducing lead times, and elevating product quality standards. Simultaneously, evolving consumer preferences for more effective and user-friendly drug delivery systems, alongside a burgeoning demand for personalized medicine tailored to individual patient needs, are actively shaping the market's trajectory and demanding greater manufacturing flexibility.

The competitive arena is characterized by intense dynamism, with key players strategically focusing on diversifying their service portfolios, expanding manufacturing capacities to meet growing demand, and investing heavily in cutting-edge technological capabilities. The market penetration of advanced manufacturing technologies like continuous manufacturing is steadily increasing. However, widespread adoption is currently tempered by the substantial initial capital investment required and the need for significant workforce retraining.

Dominant Regions & Segments in US Pharma Contract Manufacturing Industry

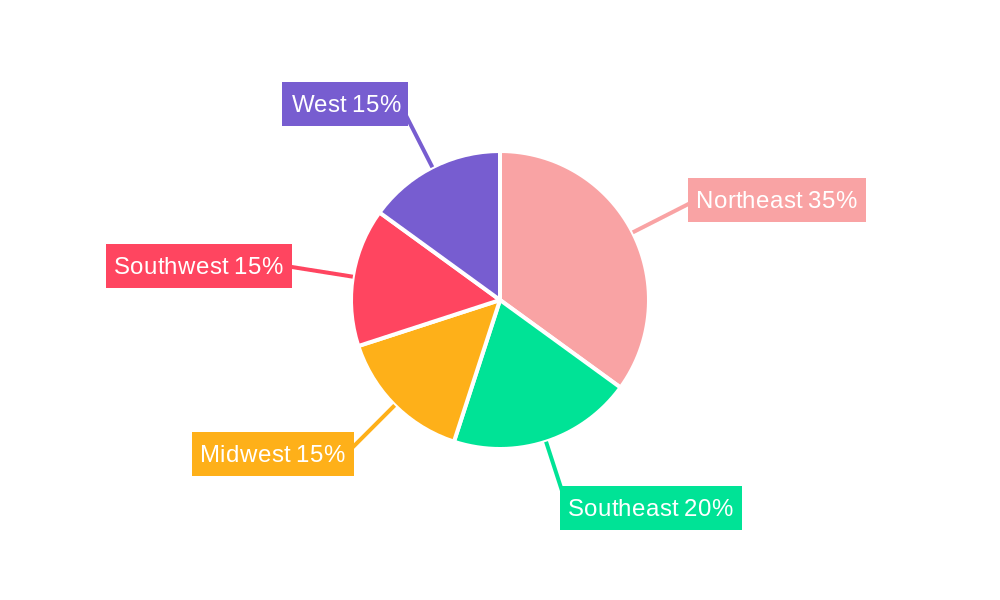

While precise granular data on geographic distribution across all US states is not always readily available, based on the well-established pharmaceutical ecosystems, manufacturing concentration, and accessibility to critical resources, key regions are emerging as dominant players within the US Pharma Contract Manufacturing industry. These likely include the Northeast, with its high concentration of R&D institutions and established pharma companies, and the Southeast, which has seen significant investment in life sciences infrastructure. This regional dominance is largely attributable to the presence of robust infrastructure, including specialized manufacturing facilities and efficient logistics networks, close proximity to major pharmaceutical companies facilitating collaboration and reducing lead times, and a deep reservoir of a highly skilled and experienced workforce adept in pharmaceutical manufacturing processes.

- By Service Type:

- Active Pharmaceutical Ingredient (API) Manufacturing: This foundational segment is poised for substantial and consistent growth. The increasing global demand for APIs, driven by both established large-cap pharmaceutical companies and agile smaller biotech firms, ensures a sustained need for specialized API production capabilities.

- High Potency API (HPAPI) Finished Dosage Formulation (FDF) Development and Manufacturing: This specialized and rapidly expanding segment is experiencing significant growth, fueled by the continuous influx of HPAPIs into the pharmaceutical development pipeline, particularly in oncology and other targeted therapies. Adherence to stringent safety protocols, containment measures, and specialized handling regulations are paramount and represent a key differentiator for CDMOs in this space.

- Injectable Dose Formulation: This segment benefits from evergreen demand and is further amplified by the transformative trends in biologics and the increasing focus on personalized medicine, which often requires injectable administration. The demand for comprehensive services extends to sterile fill-finish operations and secondary packaging solutions, adding further value and service complexity.

Key Factors Contributing to Regional Strength:

- Established Infrastructure: A mature network of advanced manufacturing facilities, specialized equipment, and well-developed logistics chains ensures operational efficiency and scalability.

- Skilled Workforce: Access to a highly trained and experienced workforce, encompassing scientists, engineers, technicians, and quality control professionals, is crucial for maintaining high product quality and driving innovation.

- Proximity to Pharmaceutical Companies: Geographic co-location with major pharmaceutical R&D hubs and corporate headquarters facilitates seamless communication, collaborative projects, and streamlined supply chain integration, leading to reduced transportation costs and faster project execution.

US Pharma Contract Manufacturing Industry Product Innovations

Recent product innovations focus on advanced drug delivery systems such as liposomes, nanoparticles, and sustained-release formulations. These innovations improve drug efficacy, reduce side effects, and enhance patient compliance. Furthermore, technological advancements in continuous manufacturing and process analytical technology (PAT) are leading to improved efficiency, reduced production costs, and enhanced quality control. These innovations are improving market fit by offering solutions to complex manufacturing challenges and allowing for faster time to market.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the US Pharma Contract Manufacturing market by key service offerings, providing deep-dive analysis into each vertical. The primary segmentation includes: Active Pharmaceutical Ingredient (API) Manufacturing, encompassing both small molecules and biologics; High Potency API (HPAPI) Finished Dosage Formulation (FDF) Development and Manufacturing, addressing the specialized needs of highly potent compounds; and Injectable Dose Formulation, which further extends to include secondary packaging services. For each identified segment, the report delivers in-depth market size assessments, detailed growth projections, and nuanced analyses of competitive dynamics. This granular approach offers stakeholders invaluable insights into prevailing market trends and future opportunities. Growth projections are carefully calibrated across segments, reflecting their unique market demand drivers, technological adoption rates, and inherent complexities. Competition within each segment is rigorously assessed, taking into account critical factors such as technological prowess, manufacturing capacity, specialized expertise, and the breadth and depth of integrated service offerings.

Key Drivers of US Pharma Contract Manufacturing Industry Growth

The growth of the US Pharma Contract Manufacturing industry is propelled by several key factors. Firstly, the increasing prevalence of chronic diseases fuels demand for pharmaceutical products. Secondly, the rising R&D expenditure by pharmaceutical companies results in a greater need for contract manufacturing services. Finally, the growing trend of outsourcing manufacturing processes due to cost optimization strategies and increased focus on core competencies significantly boosts the industry.

Challenges in the US Pharma Contract Manufacturing Industry Sector

The US Pharma Contract Manufacturing industry, while experiencing robust growth, navigates a complex landscape fraught with significant challenges. Paramount among these are the stringent and ever-evolving regulatory requirements mandated by agencies like the FDA. Compliance with these complex regulations significantly increases operational costs, demands meticulous documentation, and requires continuous investment in quality systems and personnel, thereby adding considerable complexity to manufacturing processes. Furthermore, supply chain disruptions remain a persistent threat, particularly concerning the availability and timely delivery of critical raw materials, intermediates, and specialized equipment. Shortages or delays can severely impact production schedules and the ability to meet client commitments. The need for a skilled and specialized workforce is also a growing concern, with a competitive market for experienced professionals in areas like aseptic processing, HPAPI handling, and advanced analytical testing. Finally, intense competition from both domestic and international CDMOs creates significant pricing pressure. This necessitates continuous innovation, investment in advanced technologies, and a relentless focus on operational efficiency to maintain market share and profitability.

Emerging Opportunities in US Pharma Contract Manufacturing Industry

The US Pharma Contract Manufacturing industry is at the cusp of significant expansion driven by a multitude of emerging opportunities. The burgeoning demand for personalized medicine, which requires highly flexible and agile manufacturing processes, presents a substantial growth avenue for CDMOs equipped with the right capabilities. Similarly, the development and manufacturing of advanced drug delivery systems, such as novel biologics, gene therapies, and complex injectables, are creating new niches for specialized manufacturing expertise. The strategic adoption of innovative technologies is another key opportunity. Embracing advanced manufacturing platforms like continuous manufacturing, which offers enhanced efficiency, quality control, and scalability, and leveraging AI-driven process optimization for predictive maintenance, yield improvement, and faster development cycles, can lead to significant competitive advantages and cost reductions for CDMOs and their clients. Furthermore, there is a compelling opportunity to expand into new and complex therapeutic areas, particularly those involving cutting-edge treatments like cell and gene therapy, which require highly specialized containment, handling, and manufacturing protocols. Building capabilities in these areas positions CDMOs at the forefront of pharmaceutical innovation.

Leading Players in the US Pharma Contract Manufacturing Industry Market

- Thermo Fisher Scientific Inc (Patheon Inc)

- Siegfried AG

- Aenova Group

- Lonza Group AG

- Pfizer CentreSource (Pfizer Inc)

- Jubilant Life Sciences Ltd

- Catalent Inc

- AbbVie Contract Manufacturing

- Boehringer Ingelheim Group

- Recipharm AB

- Baxter Biopharma Solutions (Baxter International Inc)

Key Developments in US Pharma Contract Manufacturing Industry Industry

- 2023 Q3: Catalent Inc. announced a significant investment in expanding its aseptic filling capacity.

- 2022 Q4: Lonza Group AG acquired a smaller contract manufacturer, expanding its service portfolio.

- 2021 Q2: Thermo Fisher Scientific (Patheon) launched a new advanced drug delivery platform. (Further developments need to be added here based on actual data.)

Future Outlook for US Pharma Contract Manufacturing Industry Market

The US Pharma Contract Manufacturing market is poised for continued growth, driven by the aforementioned trends. Strategic opportunities lie in investing in advanced technologies, expanding service offerings, and strategically forming partnerships to navigate the evolving regulatory landscape. The focus on efficiency, quality, and innovation will be crucial for success in this competitive market.

US Pharma Contract Manufacturing Industry Segmentation

-

1. Service Type

-

1.1. Active P

- 1.1.1. Small Molecule

- 1.1.2. Large Molecule

- 1.1.3. High Potency API (HPAPI)

-

1.2. Finished

- 1.2.1. Solid Dose Formulation

- 1.2.2. Liquid Dose Formulation

- 1.2.3. Injectable Dose Formulation

- 1.3. Secondary Packaging

-

1.1. Active P

US Pharma Contract Manufacturing Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Pharma Contract Manufacturing Industry Regional Market Share

Geographic Coverage of US Pharma Contract Manufacturing Industry

US Pharma Contract Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Active P

- 5.1.1.1. Small Molecule

- 5.1.1.2. Large Molecule

- 5.1.1.3. High Potency API (HPAPI)

- 5.1.2. Finished

- 5.1.2.1. Solid Dose Formulation

- 5.1.2.2. Liquid Dose Formulation

- 5.1.2.3. Injectable Dose Formulation

- 5.1.3. Secondary Packaging

- 5.1.1. Active P

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Active P

- 6.1.1.1. Small Molecule

- 6.1.1.2. Large Molecule

- 6.1.1.3. High Potency API (HPAPI)

- 6.1.2. Finished

- 6.1.2.1. Solid Dose Formulation

- 6.1.2.2. Liquid Dose Formulation

- 6.1.2.3. Injectable Dose Formulation

- 6.1.3. Secondary Packaging

- 6.1.1. Active P

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Active P

- 7.1.1.1. Small Molecule

- 7.1.1.2. Large Molecule

- 7.1.1.3. High Potency API (HPAPI)

- 7.1.2. Finished

- 7.1.2.1. Solid Dose Formulation

- 7.1.2.2. Liquid Dose Formulation

- 7.1.2.3. Injectable Dose Formulation

- 7.1.3. Secondary Packaging

- 7.1.1. Active P

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Active P

- 8.1.1.1. Small Molecule

- 8.1.1.2. Large Molecule

- 8.1.1.3. High Potency API (HPAPI)

- 8.1.2. Finished

- 8.1.2.1. Solid Dose Formulation

- 8.1.2.2. Liquid Dose Formulation

- 8.1.2.3. Injectable Dose Formulation

- 8.1.3. Secondary Packaging

- 8.1.1. Active P

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Active P

- 9.1.1.1. Small Molecule

- 9.1.1.2. Large Molecule

- 9.1.1.3. High Potency API (HPAPI)

- 9.1.2. Finished

- 9.1.2.1. Solid Dose Formulation

- 9.1.2.2. Liquid Dose Formulation

- 9.1.2.3. Injectable Dose Formulation

- 9.1.3. Secondary Packaging

- 9.1.1. Active P

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Active P

- 10.1.1.1. Small Molecule

- 10.1.1.2. Large Molecule

- 10.1.1.3. High Potency API (HPAPI)

- 10.1.2. Finished

- 10.1.2.1. Solid Dose Formulation

- 10.1.2.2. Liquid Dose Formulation

- 10.1.2.3. Injectable Dose Formulation

- 10.1.3. Secondary Packaging

- 10.1.1. Active P

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific US Pharma Contract Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Active P

- 11.1.1.1. Small Molecule

- 11.1.1.2. Large Molecule

- 11.1.1.3. High Potency API (HPAPI)

- 11.1.2. Finished

- 11.1.2.1. Solid Dose Formulation

- 11.1.2.2. Liquid Dose Formulation

- 11.1.2.3. Injectable Dose Formulation

- 11.1.3. Secondary Packaging

- 11.1.1. Active P

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Thermo Fisher Scientific Inc (Patheon Inc )

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siegfried AG*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Aenova Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lonza Group AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Pfizer CentreSource (Pfizer Inc )

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Jubilant Life Sciences Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Catalent Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 AbbVie Contract Manufacturing

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Boehringer Ingelheim Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Recipharm AB

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Baxter Biopharma Solutions (Baxter International Inc )

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Thermo Fisher Scientific Inc (Patheon Inc )

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Pharma Contract Manufacturing Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America US Pharma Contract Manufacturing Industry Revenue (Million), by Service Type 2025 & 2033

- Figure 3: North America US Pharma Contract Manufacturing Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 4: North America US Pharma Contract Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America US Pharma Contract Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America US Pharma Contract Manufacturing Industry Revenue (Million), by Service Type 2025 & 2033

- Figure 7: South America US Pharma Contract Manufacturing Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 8: South America US Pharma Contract Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: South America US Pharma Contract Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe US Pharma Contract Manufacturing Industry Revenue (Million), by Service Type 2025 & 2033

- Figure 11: Europe US Pharma Contract Manufacturing Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 12: Europe US Pharma Contract Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe US Pharma Contract Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa US Pharma Contract Manufacturing Industry Revenue (Million), by Service Type 2025 & 2033

- Figure 15: Middle East & Africa US Pharma Contract Manufacturing Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 16: Middle East & Africa US Pharma Contract Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East & Africa US Pharma Contract Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific US Pharma Contract Manufacturing Industry Revenue (Million), by Service Type 2025 & 2033

- Figure 19: Asia Pacific US Pharma Contract Manufacturing Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 20: Asia Pacific US Pharma Contract Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Asia Pacific US Pharma Contract Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 2: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 4: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 9: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Brazil US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Argentina US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 14: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russia US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Benelux US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Nordics US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 25: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Turkey US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Israel US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: GCC US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: North Africa US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Africa US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 33: Global US Pharma Contract Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: China US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: India US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Korea US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: ASEAN US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Oceania US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific US Pharma Contract Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Pharma Contract Manufacturing Industry?

The projected CAGR is approximately 5.00%.

2. Which companies are prominent players in the US Pharma Contract Manufacturing Industry?

Key companies in the market include Thermo Fisher Scientific Inc (Patheon Inc ), Siegfried AG*List Not Exhaustive, Aenova Group, Lonza Group AG, Pfizer CentreSource (Pfizer Inc ), Jubilant Life Sciences Ltd, Catalent Inc, AbbVie Contract Manufacturing, Boehringer Ingelheim Group, Recipharm AB, Baxter Biopharma Solutions (Baxter International Inc ).

3. What are the main segments of the US Pharma Contract Manufacturing Industry?

The market segments include Service Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Emphasis on Drug Discovery and Outsourcing of Manufacturing; Strong R&D Investments.

6. What are the notable trends driving market growth?

Increasing Demand of API to Witness Significant Market Growth.

7. Are there any restraints impacting market growth?

Increasing Lead Time and Logistics Costs; Stringent Regulatory Requirements; Capacity Utilization Issues Affecting the Profitability of CMOs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Pharma Contract Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Pharma Contract Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Pharma Contract Manufacturing Industry?

To stay informed about further developments, trends, and reports in the US Pharma Contract Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence