Key Insights

The 3D IC Packaging market is poised for significant expansion, driven by the escalating demand for enhanced electronic performance, miniaturization, and improved power efficiency. This advanced semiconductor packaging solution is integral to meeting the sophisticated requirements of sectors including consumer electronics, aerospace & defense, medical devices, and telecommunications. The proliferation of high-performance smartphones, wearables, advanced avionics, implantable medical devices, and 5G infrastructure are key contributors to this growth trajectory.

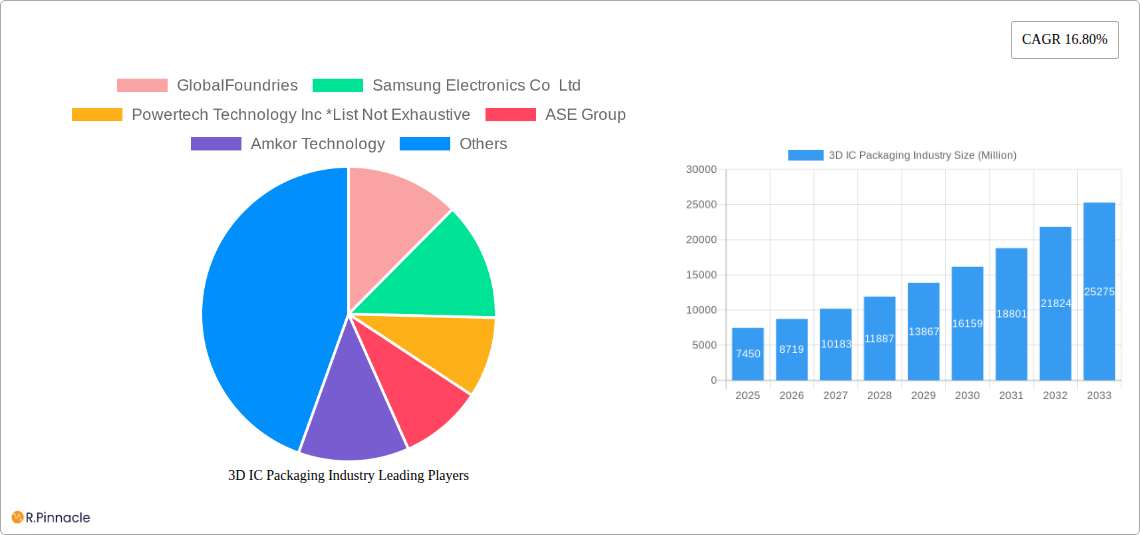

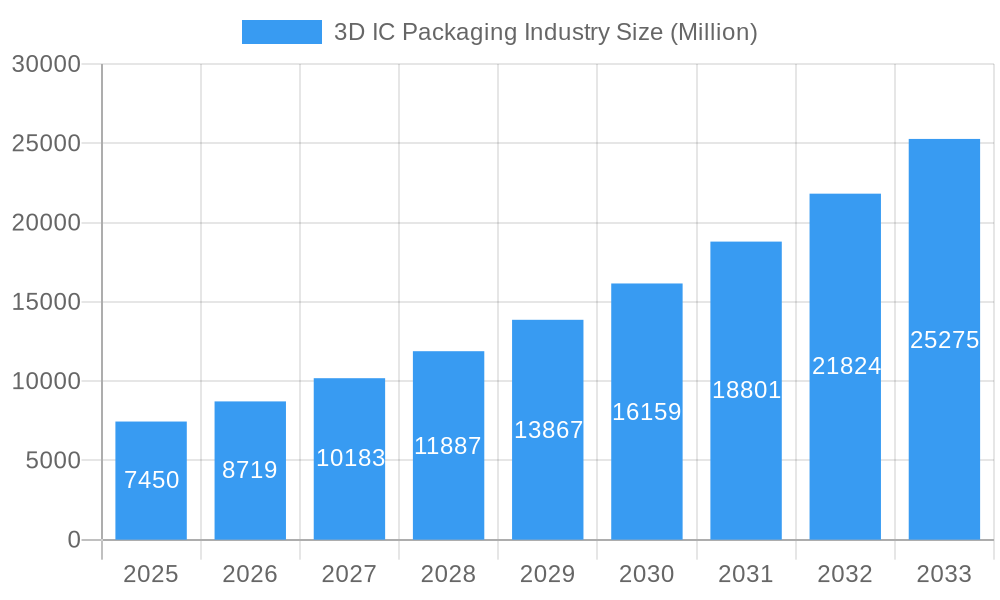

3D IC Packaging Industry Market Size (In Billion)

Key players such as Samsung Electronics, Intel Corporation, and TSMC are at the forefront of innovation in 3D IC packaging technologies like 3D TSV and wafer-level chip-scale packaging. While these advancements offer unprecedented integration density and performance, the market faces challenges including high manufacturing costs, design complexities, and the need for specialized expertise and equipment. Nevertheless, the inherent advantages of 3D ICs in addressing increasing data processing and miniaturization needs ensure sustained market expansion. The Asia Pacific region is anticipated to lead both production and consumption, leveraging its established electronics manufacturing ecosystem.

3D IC Packaging Industry Company Market Share

This comprehensive market research report offers in-depth analysis and strategic insights into the dynamic 3D IC packaging market. Covering the period from 2019 to 2033, with a base year of 2025, it provides critical data on market size, CAGR, technological advancements, regional trends, and future outlook. The report details a market size of $16.22 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 15.2% through 2033. This analysis is an indispensable resource for semiconductor manufacturers, packaging solution providers, and end-user industries seeking to navigate and capitalize on this high-growth sector.

3D IC Packaging Industry Market Structure & Innovation Trends

The 3D IC packaging industry exhibits a moderately consolidated market structure, characterized by a few dominant players and a growing number of specialized innovators. Key innovation drivers revolve around enhancing performance, reducing form factors, and improving power efficiency through advanced stacking technologies. Regulatory frameworks are evolving to support semiconductor manufacturing and advanced packaging initiatives globally, fostering a favorable environment for growth. Product substitutes, such as traditional 2D packaging, are increasingly being challenged by the superior capabilities of 3D ICs, particularly in high-performance computing and artificial intelligence applications. End-user demographics are shifting towards industries demanding miniaturization and enhanced functionality. Mergers and acquisitions (M&A) activities are significant, with deal values often reaching tens to hundreds of million dollars, driven by the need to acquire specialized expertise and expand market reach. For instance, strategic partnerships and acquisitions are crucial for companies aiming to secure their position in the advanced packaging value chain. The market share of leading companies in specific advanced packaging segments, such as 3D TSV, is steadily increasing.

3D IC Packaging Industry Market Dynamics & Trends

The 3D IC packaging market is experiencing robust growth, fueled by an insatiable demand for higher performance, increased functionality, and miniaturized electronic devices across a multitude of end-user industries. The CAGR for this sector is projected to be XX% over the forecast period (2025–2033), indicating a significant expansion trajectory. Technological disruptions are at the forefront of this growth, with advancements in Through-Silicon Via (TSV) technology, wafer-level chip-scale packaging, and heterogeneous integration enabling the stacking of multiple chips or chiplets in a single package. This allows for shorter interconnects, leading to substantial improvements in speed and a reduction in power consumption, crucial for applications in 5G communications, artificial intelligence, and the Internet of Things (IoT). Consumer preferences are increasingly leaning towards compact, powerful, and energy-efficient devices, directly driving the adoption of 3D IC packaging solutions. The competitive dynamics are intense, with established semiconductor giants and agile startups vying for market leadership. Companies are investing heavily in research and development to offer more sophisticated and cost-effective packaging solutions. Market penetration is steadily rising, particularly within the consumer electronics and telecommunications sectors, where the need for next-generation performance is paramount. The ability to integrate diverse functionalities into a single package without compromising performance is a key differentiator. The increasing complexity of semiconductor designs necessitates advanced packaging techniques that can accommodate these intricate architectures, making 3D IC packaging a critical enabler for future electronic innovation. The continuous miniaturization trend, coupled with the growing need for specialized functionalities, further propels the market forward, creating substantial opportunities for market players. The expansion of data centers and the burgeoning field of autonomous driving are also significant contributors to the market's upward momentum.

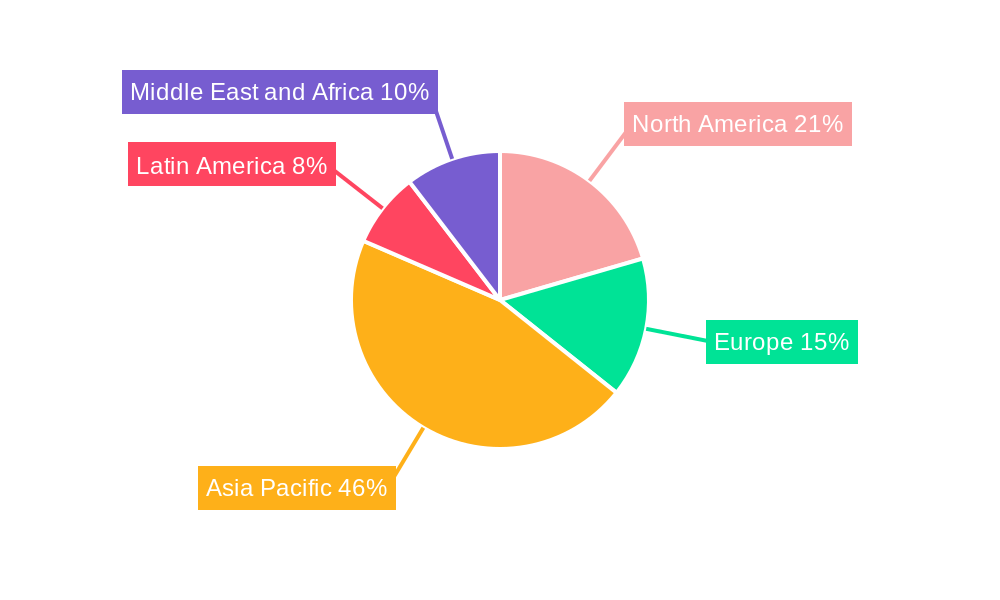

Dominant Regions & Segments in 3D IC Packaging Industry

The Asia-Pacific region stands as the dominant force in the global 3D IC packaging industry, driven by its extensive manufacturing infrastructure, a skilled workforce, and significant government support for the semiconductor sector. Countries like Taiwan, South Korea, and China are at the forefront, hosting major foundries and packaging houses. Economic policies promoting domestic semiconductor production and investments in advanced research and development facilities are key drivers.

Leading Segments:

Packaging Technology:

- 3D TSV (Through-Silicon Via): This technology leads due to its ability to enable high-density interconnects and stacked architectures, crucial for high-performance computing, AI accelerators, and advanced memory modules.

- Key Drivers: Demand for enhanced processing power, reduction in latency, and increased bandwidth in data-intensive applications. Government incentives for advanced manufacturing capabilities in key Asian nations.

- 3D Wafer-Level Chip-Scale Packaging (WLP): This segment is growing rapidly due to its cost-effectiveness and suitability for miniaturized applications, particularly in the consumer electronics sector.

- Key Drivers: Miniaturization trend in consumer devices, including smartphones and wearables. Advancements in wafer-level processing enabling higher yields and lower costs.

- 3D TSV (Through-Silicon Via): This technology leads due to its ability to enable high-density interconnects and stacked architectures, crucial for high-performance computing, AI accelerators, and advanced memory modules.

End-User Industry:

- Consumer Electronics: This segment dominates the market, driven by the constant innovation and demand for smartphones, wearables, gaming consoles, and advanced audio-visual equipment.

- Key Drivers: Proliferation of smart devices, increasing consumer spending on premium electronics, and the need for compact, high-performance devices.

- Communications and Telecom: This sector is a significant growth driver, propelled by the rollout of 5G networks and the increasing demand for high-speed data transfer and low latency communication devices.

- Key Drivers: Infrastructure investments in 5G deployment, development of advanced network equipment, and the growing IoT ecosystem.

- Consumer Electronics: This segment dominates the market, driven by the constant innovation and demand for smartphones, wearables, gaming consoles, and advanced audio-visual equipment.

The dominance of these segments is further reinforced by strategic investments in R&D and manufacturing capabilities. The concentration of semiconductor manufacturing power in Asia, coupled with robust demand from consumer and telecommunications markets, positions the region and these specific segments for continued leadership in the 3D IC packaging industry. The infrastructure supporting advanced packaging technologies, including specialized equipment and skilled labor, is heavily concentrated in these dominant regions, creating a self-reinforcing cycle of growth and innovation.

3D IC Packaging Industry Product Innovations

Product innovations in the 3D IC packaging industry are centered on enabling denser chip integration, improved thermal management, and enhanced electrical performance. Key developments include advanced stacking techniques for heterogeneous integration, allowing different types of chips (e.g., logic, memory, RF) to be combined in a single package. These innovations offer significant competitive advantages by reducing the overall footprint, lowering power consumption, and boosting processing speeds for applications in AI, 5G, and high-performance computing. The focus is on creating modular solutions that can be customized for specific end-user needs, thereby broadening market applicability and adoption.

3D IC Packaging Industry Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the 3D IC packaging market, segmented across key technologies and end-user industries. The Packaging Technology segments include 3D wafer-level chip-scale packaging and 3D TSV. The End-User Industry segments encompass Consumer electronics, Aerospace and Defense, Medical Devices, Communications and Telecom, Automotive, and Others.

- 3D Wafer-Level Chip-Scale Packaging: This segment is projected to experience substantial growth, driven by its cost-effectiveness and suitability for miniaturized consumer devices. Market size is estimated to reach several hundred million dollars in 2025, with strong competitive dynamics focused on yield optimization and process standardization.

- 3D TSV: This segment represents a significant market share, crucial for high-performance applications. Growth projections are robust, fueled by demand for advanced computing and AI. Competitive dynamics revolve around technological sophistication and reliability.

- Consumer Electronics: This is the largest end-user segment, with an estimated market size of several hundred million dollars in 2025. Continued innovation in smartphones and wearables ensures sustained growth.

- Communications and Telecom: This segment is a major growth engine, driven by 5G deployment. Competitive dynamics involve partnerships for integrated solutions to meet evolving network demands.

- Automotive: Emerging as a critical sector, this segment's market size is expected to grow significantly due to the increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies.

- Aerospace and Defense, Medical Devices, and Others: These segments, while smaller, represent niche but high-value opportunities, characterized by stringent performance and reliability requirements.

Key Drivers of 3D IC Packaging Industry Growth

The growth of the 3D IC packaging industry is propelled by several interconnected factors. Primarily, the insatiable demand for increased computational power and miniaturization across all electronic sectors acts as a significant catalyst. Technological advancements, particularly in Through-Silicon Via (TSV) technology and wafer-level chip-scale packaging, enable higher integration densities, leading to smaller and more powerful devices. The rapid expansion of 5G networks necessitates advanced packaging solutions to support higher frequencies and lower latency. Furthermore, the burgeoning adoption of Artificial Intelligence (AI) and Machine Learning (ML) requires specialized hardware accelerators that benefit immensely from 3D integration for improved performance. Economic policies supporting semiconductor manufacturing and R&D also play a crucial role in fostering growth.

Challenges in the 3D IC Packaging Industry Sector

Despite its promising trajectory, the 3D IC packaging industry faces several significant challenges. Manufacturing complexity and cost remain primary barriers, as advanced packaging techniques require specialized equipment and highly controlled environments. Thermal management issues in densely stacked chips can impact performance and reliability, necessitating innovative cooling solutions. Supply chain disruptions and the availability of critical raw materials can also pose significant risks. Furthermore, design and testing complexities increase with the intricate nature of 3D architectures. Competitive pressures from alternative packaging technologies and the need for continuous R&D investment to stay ahead of the technological curve are also substantial hurdles.

Emerging Opportunities in 3D IC Packaging Industry

The 3D IC packaging industry is ripe with emerging opportunities. The increasing demand for heterogeneous integration, where different types of chips are combined in a single package, presents a vast potential for customized solutions. The growth of the Internet of Things (IoT) ecosystem, with its diverse range of connected devices, requires compact and power-efficient packaging. The automotive sector, driven by autonomous driving and advanced driver-assistance systems (ADAS), is a rapidly expanding market for high-reliability 3D IC packaging. Furthermore, advancements in advanced cooling technologies will unlock new possibilities for even denser integration and higher performance.

Leading Players in the 3D IC Packaging Industry Market

- ASE Group

- Amkor Technology

- GlobalFoundries

- Intel Corporation

- Invensas

- Samsung Electronics Co Ltd

- Siliconware Precision Industries Co Ltd (SPIL)

- Taiwan Semiconductor Manufacturing Company Limited

- Powertech Technology Inc

Key Developments in 3D IC Packaging Industry Industry

- October 2021: Cadence Design Systems, Inc. announced the delivery of the Integrity 3D-IC platform, the industry's first high-capacity, comprehensive 3D-IC platform integrating 3D implementation, system analysis, and design planning in a unified cockpit. This development significantly streamlines the design process for complex 3D ICs, impacting market efficiency and adoption rates.

- July 2021: Singapore's Agency for Science, Technology, and Research (A*STAR's) Institute of Microelectronics (IME) announced a collaboration with Asahi-Kasei, GLOBALFOUNDRIES, Qorvo, and Toray to form a System-in-Package (SiP) consortium. This consortium aims to develop high-density SiP for heterogeneous chiplets integration, specifically targeting 5G applications and leveraging IME's FOWLP/2.5D/3D packaging expertise. This collaboration signifies a strategic push towards advanced SiP solutions for future communication technologies.

Future Outlook for 3D IC Packaging Industry Market

The future outlook for the 3D IC packaging industry is exceptionally bright, driven by sustained demand for enhanced performance and miniaturization. Advancements in heterogeneous integration and the widespread adoption of technologies like AI, 5G, and autonomous systems will continue to be key growth accelerators. Strategic investments in R&D, coupled with potential M&A activities, will further shape the competitive landscape. Opportunities in niche markets such as aerospace, defense, and medical devices, where high reliability and specialized functionalities are paramount, will also contribute to market expansion. The industry is poised for continued innovation, offering solutions that will power the next generation of electronic devices and systems.

3D IC Packaging Industry Segmentation

-

1. Packaging Technology

- 1.1. 3D wafer-level chip-scale packaging

- 1.2. 3D TSV

-

2. End-User Industry

- 2.1. Consumer electronics

- 2.2. Aerospace and Defense

- 2.3. Medical Devices

- 2.4. Communications and Telecom

- 2.5. Automotive

- 2.6. Others

3D IC Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

3D IC Packaging Industry Regional Market Share

Geographic Coverage of 3D IC Packaging Industry

3D IC Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 5.1.1. 3D wafer-level chip-scale packaging

- 5.1.2. 3D TSV

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Consumer electronics

- 5.2.2. Aerospace and Defense

- 5.2.3. Medical Devices

- 5.2.4. Communications and Telecom

- 5.2.5. Automotive

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 6. Global 3D IC Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 6.1.1. 3D wafer-level chip-scale packaging

- 6.1.2. 3D TSV

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Consumer electronics

- 6.2.2. Aerospace and Defense

- 6.2.3. Medical Devices

- 6.2.4. Communications and Telecom

- 6.2.5. Automotive

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 7. North America 3D IC Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 7.1.1. 3D wafer-level chip-scale packaging

- 7.1.2. 3D TSV

- 7.2. Market Analysis, Insights and Forecast - by End-User Industry

- 7.2.1. Consumer electronics

- 7.2.2. Aerospace and Defense

- 7.2.3. Medical Devices

- 7.2.4. Communications and Telecom

- 7.2.5. Automotive

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 8. Europe 3D IC Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 8.1.1. 3D wafer-level chip-scale packaging

- 8.1.2. 3D TSV

- 8.2. Market Analysis, Insights and Forecast - by End-User Industry

- 8.2.1. Consumer electronics

- 8.2.2. Aerospace and Defense

- 8.2.3. Medical Devices

- 8.2.4. Communications and Telecom

- 8.2.5. Automotive

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 9. Asia Pacific 3D IC Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 9.1.1. 3D wafer-level chip-scale packaging

- 9.1.2. 3D TSV

- 9.2. Market Analysis, Insights and Forecast - by End-User Industry

- 9.2.1. Consumer electronics

- 9.2.2. Aerospace and Defense

- 9.2.3. Medical Devices

- 9.2.4. Communications and Telecom

- 9.2.5. Automotive

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 10. Latin America 3D IC Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 10.1.1. 3D wafer-level chip-scale packaging

- 10.1.2. 3D TSV

- 10.2. Market Analysis, Insights and Forecast - by End-User Industry

- 10.2.1. Consumer electronics

- 10.2.2. Aerospace and Defense

- 10.2.3. Medical Devices

- 10.2.4. Communications and Telecom

- 10.2.5. Automotive

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 11. Middle East and Africa 3D IC Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 11.1.1. 3D wafer-level chip-scale packaging

- 11.1.2. 3D TSV

- 11.2. Market Analysis, Insights and Forecast - by End-User Industry

- 11.2.1. Consumer electronics

- 11.2.2. Aerospace and Defense

- 11.2.3. Medical Devices

- 11.2.4. Communications and Telecom

- 11.2.5. Automotive

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Packaging Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GlobalFoundries

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung Electronics Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Powertech Technology Inc *List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ASE Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Amkor Technology

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Invensas

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Siliconware Precision Industries Co Ltd (SPIL)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Taiwan Semiconductor Manufacturing Company Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Intel Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 GlobalFoundries

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global 3D IC Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America 3D IC Packaging Industry Revenue (billion), by Packaging Technology 2025 & 2033

- Figure 3: North America 3D IC Packaging Industry Revenue Share (%), by Packaging Technology 2025 & 2033

- Figure 4: North America 3D IC Packaging Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 5: North America 3D IC Packaging Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 6: North America 3D IC Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America 3D IC Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe 3D IC Packaging Industry Revenue (billion), by Packaging Technology 2025 & 2033

- Figure 9: Europe 3D IC Packaging Industry Revenue Share (%), by Packaging Technology 2025 & 2033

- Figure 10: Europe 3D IC Packaging Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 11: Europe 3D IC Packaging Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 12: Europe 3D IC Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe 3D IC Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific 3D IC Packaging Industry Revenue (billion), by Packaging Technology 2025 & 2033

- Figure 15: Asia Pacific 3D IC Packaging Industry Revenue Share (%), by Packaging Technology 2025 & 2033

- Figure 16: Asia Pacific 3D IC Packaging Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 17: Asia Pacific 3D IC Packaging Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 18: Asia Pacific 3D IC Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific 3D IC Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America 3D IC Packaging Industry Revenue (billion), by Packaging Technology 2025 & 2033

- Figure 21: Latin America 3D IC Packaging Industry Revenue Share (%), by Packaging Technology 2025 & 2033

- Figure 22: Latin America 3D IC Packaging Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 23: Latin America 3D IC Packaging Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 24: Latin America 3D IC Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America 3D IC Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa 3D IC Packaging Industry Revenue (billion), by Packaging Technology 2025 & 2033

- Figure 27: Middle East and Africa 3D IC Packaging Industry Revenue Share (%), by Packaging Technology 2025 & 2033

- Figure 28: Middle East and Africa 3D IC Packaging Industry Revenue (billion), by End-User Industry 2025 & 2033

- Figure 29: Middle East and Africa 3D IC Packaging Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 30: Middle East and Africa 3D IC Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa 3D IC Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 2: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: Global 3D IC Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 5: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: Global 3D IC Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 8: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 9: Global 3D IC Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 11: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 12: Global 3D IC Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 14: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 15: Global 3D IC Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global 3D IC Packaging Industry Revenue billion Forecast, by Packaging Technology 2020 & 2033

- Table 17: Global 3D IC Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 18: Global 3D IC Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D IC Packaging Industry?

The projected CAGR is approximately 15.2%.

2. Which companies are prominent players in the 3D IC Packaging Industry?

Key companies in the market include GlobalFoundries, Samsung Electronics Co Ltd, Powertech Technology Inc *List Not Exhaustive, ASE Group, Amkor Technology, Invensas, Siliconware Precision Industries Co Ltd (SPIL), Taiwan Semiconductor Manufacturing Company Limited, Intel Corporation.

3. What are the main segments of the 3D IC Packaging Industry?

The market segments include Packaging Technology, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.22 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Advanced Architecture in Electronic Products; Miniaturization of Electronics Devices.

6. What are the notable trends driving market growth?

IT & Telecommunication is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Manufacturing And Cost Challenges Associated with Production.

8. Can you provide examples of recent developments in the market?

In October 2021 - Cadence Design Systems, Inc. announced the delivery of the Integrity 3D-IC platform. It is the industry's first high-capacity, comprehensive 3D-IC platform that integrates 3D implementation, system analysis, and design planning in a single, unified cockpit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3D IC Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3D IC Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3D IC Packaging Industry?

To stay informed about further developments, trends, and reports in the 3D IC Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence