Key Insights

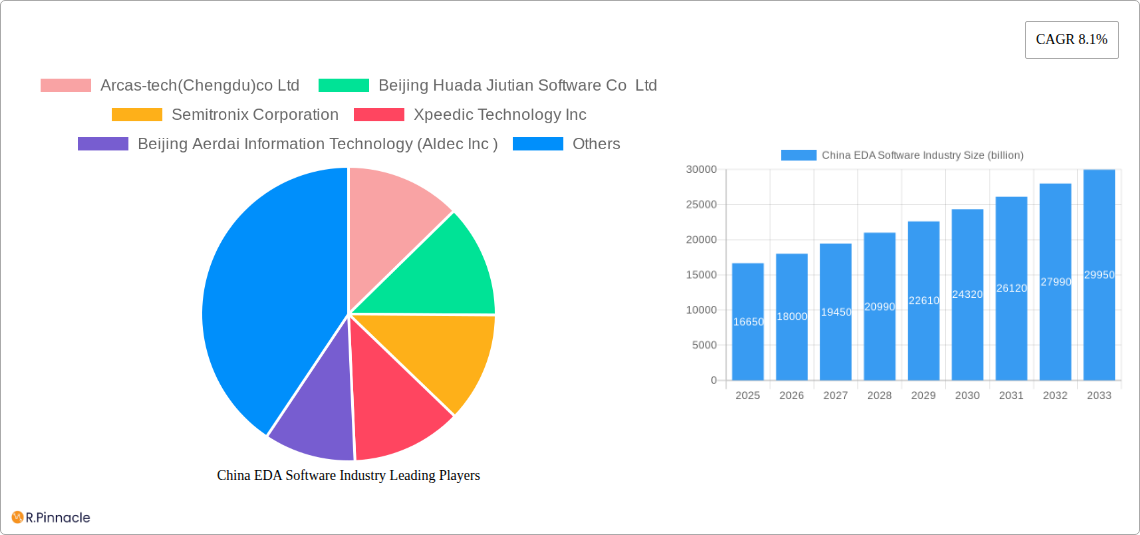

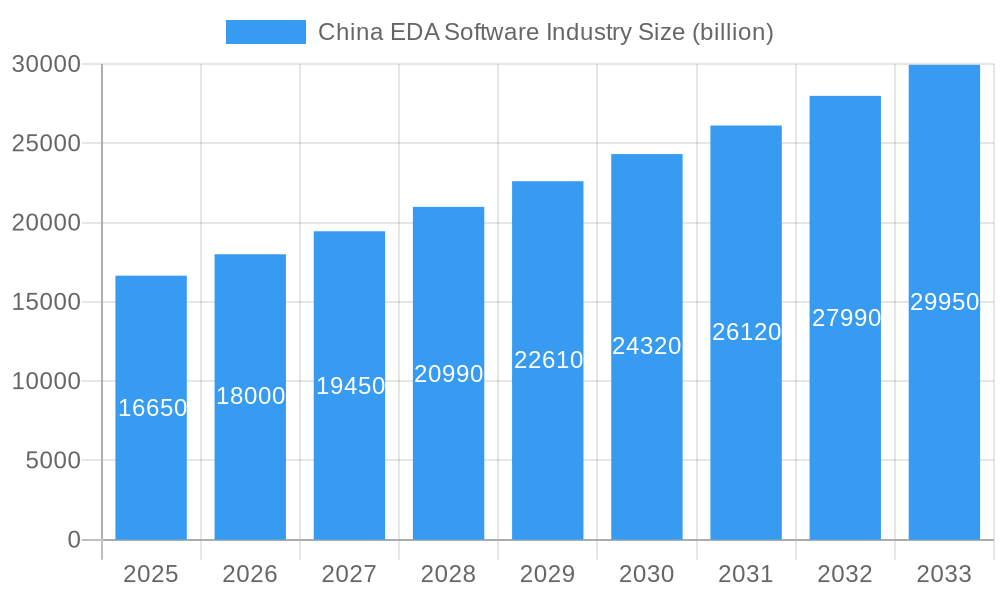

The China Electronic Design Automation (EDA) software market is poised for substantial expansion, projected to reach an estimated $16.65 billion in 2025. This growth will be propelled by a robust Compound Annual Growth Rate (CAGR) of 8.1% over the forecast period of 2025-2033. The primary drivers behind this upward trajectory include the escalating demand for advanced semiconductor chips across various applications, the rapid growth of China's domestic semiconductor industry, and government initiatives aimed at fostering self-sufficiency in critical technologies. The increasing complexity of integrated circuits (ICs) necessitates sophisticated EDA tools for efficient design, verification, and manufacturing, further fueling market expansion. Furthermore, the burgeoning adoption of Artificial Intelligence (AI) and Machine Learning (ML) in chip design is creating new opportunities for innovation and market penetration.

China EDA Software Industry Market Size (In Billion)

The market is segmented into key areas such as Computer-aided Engineering (CAE), IC Physical Design and Verification, Printed Circuit Board (PCB) design, and Semiconductor Intellectual Property (SIP). Applications span across crucial sectors like Communication, Consumer Electronics, Automotive, and Industrial, with "Other Applications" also contributing to the demand. Key players, including Synopsys Inc., Cadence Design Systems Inc., and Mentor Graphics Corporation (Siemens PLM Software), alongside emerging domestic companies like Arcas-tech (Chengdu) Co Ltd and Beijing Huada Jiutian Software Co Ltd, are actively shaping the competitive landscape. While significant growth is anticipated, potential restraints may include geopolitical factors, intellectual property protection concerns, and the ongoing need for skilled talent in the specialized field of EDA. Despite these challenges, the overall outlook for China's EDA software market remains exceptionally strong, driven by relentless innovation and strategic national development policies.

China EDA Software Industry Company Market Share

China EDA Software Industry: Comprehensive Market Analysis & Future Forecast (2019-2033)

This in-depth report provides a definitive analysis of the China Electronic Design Automation (EDA) software industry, projecting its trajectory from 2019 to 2033. With a base year of 2025 and a comprehensive forecast period of 2025-2033, this study delves into the intricate market structure, evolving dynamics, and critical growth drivers shaping this vital sector. We offer actionable insights for stakeholders, investors, and industry professionals seeking to navigate the complexities of China's rapidly advancing semiconductor and electronics ecosystem. Expect detailed segmentation analysis across critical applications and technology types, alongside an exhaustive examination of market trends, challenges, and emerging opportunities.

China EDA Software Industry Market Structure & Innovation Trends

The China EDA software industry exhibits a moderately concentrated market structure, with a significant presence of global giants alongside a growing cohort of domestic players. Innovation is primarily driven by intense R&D investment in advanced technologies like AI-driven design, formal verification, and cloud-based EDA solutions. Regulatory frameworks, particularly those aimed at fostering domestic semiconductor self-sufficiency, play a crucial role in shaping market access and competitive landscapes. Product substitutes, while nascent, include open-source EDA tools and in-house developed solutions by large integrated device manufacturers. End-user demographics are increasingly sophisticated, demanding higher performance, lower power consumption, and enhanced design efficiency. Mergers and acquisitions (M&A) are becoming more frequent as larger players seek to consolidate market share and acquire specialized technological capabilities. For instance, M&A deal values are projected to reach over $10 billion by 2033, reflecting the strategic importance of acquiring EDA IP and talent. Key market share is held by dominant global players, but domestic companies are steadily increasing their footprint.

China EDA Software Industry Market Dynamics & Trends

The China EDA software market is poised for substantial growth, driven by an insatiable demand for advanced semiconductor devices across a multitude of applications. The Compound Annual Growth Rate (CAGR) is projected to be a robust 18.5% during the forecast period. This expansion is fueled by China's strategic push for technological independence, massive government investment in the semiconductor industry, and the burgeoning digital economy. The increasing complexity of integrated circuits (ICs) necessitates sophisticated EDA tools for efficient design, verification, and manufacturing. Consumer electronics, particularly smartphones, wearables, and home appliances, continue to be primary demand drivers. The automotive sector's rapid electrification and the proliferation of Advanced Driver-Assistance Systems (ADAS) are creating significant new avenues for EDA software adoption. Furthermore, the ongoing development of 5G infrastructure and the expansion of the Internet of Things (IoT) ecosystem are generating a constant need for specialized ICs, thereby boosting EDA market penetration. Technological disruptions are primarily focused on the integration of artificial intelligence and machine learning into EDA workflows to accelerate design cycles and optimize chip performance. Cloud-native EDA platforms are also gaining traction, offering greater scalability and accessibility. Competitive dynamics are characterized by intense innovation, strategic partnerships, and a growing emphasis on localized support and customization by both global and domestic EDA vendors. The market penetration of advanced EDA solutions is expected to surpass 70% for high-end IC design by 2030.

Dominant Regions & Segments in China EDA Software Industry

The Eastern China region, particularly the Yangtze River Delta, stands as the dominant force in China's EDA software industry. This dominance is underpinned by a confluence of factors, including the concentration of leading semiconductor manufacturing facilities, extensive research and development centers, and a highly skilled workforce. The region benefits significantly from favorable economic policies and substantial government incentives aimed at fostering innovation and production in the high-tech sector.

Within the Type segmentation, IC Physical Design and Verification commands the largest market share. This is driven by the increasing complexity and miniaturization of semiconductor chips, necessitating sophisticated tools for layout, routing, parasitic extraction, and functional verification. The demand for high-performance and low-power designs in applications like AI accelerators and advanced processors directly fuels the growth of this segment.

The Printed segment, while smaller, is experiencing steady growth due to the increasing demand for complex Printed Circuit Boards (PCBs) in 5G infrastructure, automotive electronics, and industrial automation. Advances in PCB manufacturing technology require specialized EDA tools for design, simulation, and signal integrity analysis.

The Semiconductor Intellectual Property (SIP) segment is also a critical growth area. As Chinese companies aim to develop their own chip designs, the demand for reusable IP blocks and associated verification tools is escalating. This segment is intrinsically linked to the broader trend of indigenous innovation in China's semiconductor ecosystem.

In terms of Application segmentation, Communication remains a leading driver. The relentless expansion of 5G networks, the evolution of mobile devices, and the growing demand for high-speed data transmission across various industries necessitate continuous advancements in communication chip design, directly benefiting the EDA market.

Consumer Electronics continues to be a significant application, driven by the constant innovation and demand for new features in smartphones, smart home devices, and gaming consoles. The miniaturization and power efficiency requirements in this segment push the boundaries of EDA capabilities.

The Automotive sector is emerging as a powerful growth engine. The rapid electrification of vehicles, the development of autonomous driving technologies, and the integration of advanced infotainment systems create a substantial and growing demand for sophisticated semiconductor solutions, thus driving EDA adoption in this space.

Industrial applications, including automation, robotics, and smart manufacturing, also contribute significantly. The increasing adoption of Industry 4.0 principles requires advanced control systems and sensors, which rely on complex chip designs and, consequently, advanced EDA tools.

China EDA Software Industry Product Innovations

Product innovations in China's EDA software industry are sharply focused on enhancing design efficiency and performance. AI-powered design exploration and optimization tools are revolutionizing the IC design flow, enabling faster exploration of design spaces and identification of optimal solutions. Advancements in formal verification methodologies are critical for ensuring the functional correctness of increasingly complex chips. Cloud-based EDA platforms are offering unprecedented scalability and collaborative design capabilities, breaking down traditional hardware limitations. These innovations provide a significant competitive advantage by reducing design cycles, lowering power consumption, and improving overall chip performance, directly addressing the evolving market demands for faster and more efficient electronic devices.

Report Scope & Segmentation Analysis

This report meticulously analyzes the China EDA software industry across its key segmentation. The Computer-aided Engineering (CAE) segment encompasses simulation and analysis tools crucial for product performance validation, expected to grow at a CAGR of 16.2% to reach an estimated market size of $5.5 billion by 2033. IC Physical Design and Verification is the largest segment, projected to reach $12.8 billion by 2033 with a CAGR of 19.5%, driven by the demand for complex chip architectures. The Printed segment, focusing on PCB design, is forecast to reach $3.2 billion by 2033 with a CAGR of 15.8%, catering to the growing needs of high-density interconnect boards. The Semiconductor Intellectual Property (SIP) segment is anticipated to grow at a CAGR of 20.1% to $6.5 billion by 2033, fueled by the increasing reliance on pre-designed IP blocks for accelerated chip development.

The Communication application segment is expected to reach $10.2 billion by 2033 with a CAGR of 18.9%, driven by 5G and beyond. Consumer Electronics is projected to grow to $8.5 billion by 2033 at a CAGR of 17.5%, supported by continuous product innovation. The Automotive application segment is a high-growth area, forecast to reach $7.1 billion by 2033 with a CAGR of 22.0%, propelled by vehicle electrification and autonomous driving trends. The Industrial segment is estimated to reach $4.9 billion by 2033 with a CAGR of 19.8%, driven by smart manufacturing and automation. Other Applications are expected to contribute $1.8 billion by 2033 with a CAGR of 16.5%.

Key Drivers of China EDA Software Industry Growth

The primary drivers propelling the China EDA software industry are multifaceted. Government initiatives and strategic investments in the semiconductor sector, aimed at achieving technological self-sufficiency, are creating a fertile ground for EDA adoption. The exponential growth in demand for advanced electronic devices across communication, automotive, and consumer electronics sectors necessitates increasingly sophisticated chip designs, directly fueling the need for advanced EDA tools. Furthermore, the ongoing technological advancements in semiconductor manufacturing, such as smaller process nodes and advanced packaging techniques, require correspondingly advanced EDA solutions to manage their complexity. The rise of AI and machine learning within EDA workflows is also a significant growth accelerator, promising to optimize design processes and improve chip performance.

Challenges in the China EDA Software Industry Sector

Despite its robust growth, the China EDA software industry faces several significant challenges. Dependence on foreign technology and IP remains a considerable hurdle, particularly for advanced EDA tools, leading to potential supply chain vulnerabilities and intellectual property concerns. Talent shortages in specialized EDA design and verification engineers can hinder adoption and innovation. High initial investment costs associated with advanced EDA software licenses and hardware can be a barrier for smaller enterprises and startups. Regulatory complexities and geopolitical tensions can introduce uncertainty and impact market access and collaborations. Furthermore, ensuring the security and integrity of complex chip designs against cyber threats is an ever-growing concern.

Emerging Opportunities in China EDA Software Industry

Emerging opportunities within the China EDA software industry are abundant and promising. The rapid growth of the domestic AI chip market presents a substantial demand for specialized EDA tools for neural network acceleration and optimization. The burgeoning automotive electronics sector, with its focus on EVs and autonomous driving, offers immense potential for advanced EDA solutions for safety-critical systems. The expansion of IoT devices in smart cities, industrial automation, and healthcare requires a vast array of custom-designed chips, driving demand for flexible and cost-effective EDA workflows. Furthermore, the development of cloud-native EDA platforms and the integration of AI/ML are creating new paradigms for design collaboration and efficiency, offering opportunities for innovative service providers and tool developers.

Leading Players in the China EDA Software Industry Market

- Arcas-tech(Chengdu)co Ltd

- Beijing Huada Jiutian Software Co Ltd

- Semitronix Corporation

- Xpeedic Technology Inc

- Beijing Aerdai Information Technology (Aldec Inc )

- Zuken Ltd

- Altium Limited

- Shanghai Lomicro Information Technology Co Ltd (Agnisys Inc )

- Mentor Graphic Corporation (Siemens PLM Software)

- Synopsys Inc

- Cadence Design Systems Inc

- Platform Design Automation Inc

Key Developments in China EDA Software Industry Industry

- 2023/09: Synopsys Inc. announces significant advancements in its AI-driven design solutions, enhancing the efficiency of chip development for advanced applications.

- 2023/07: Cadence Design Systems Inc. expands its collaboration with leading Chinese foundries to accelerate the adoption of next-generation process technologies.

- 2023/05: Xpeedic Technology Inc. launches a new suite of electromagnetic simulation tools optimized for high-frequency designs, catering to the 5G and automotive sectors.

- 2023/03: Beijing Huada Jiutian Software Co Ltd announces a strategic partnership to integrate its EDA offerings with cloud computing platforms, enhancing accessibility and scalability.

- 2022/11: Mentor Graphic Corporation (Siemens PLM Software) unveils enhanced verification capabilities to address the increasing complexity of functional safety requirements in automotive ICs.

- 2022/08: Altium Limited introduces advanced PCB design features for heterogeneous integration, supporting the trend towards complex multi-chip modules.

- 2022/06: Platform Design Automation Inc. showcases its innovative approach to chiplet design and integration, enabling modular and flexible SoC development.

- 2022/04: Arcas-tech(Chengdu)co Ltd announces significant investments in R&D for AI-accelerated EDA, aiming to reduce design cycles by up to 30%.

- 2021/10: Semitronix Corporation expands its presence in the Chinese market with enhanced customer support and localized technical services.

- 2021/07: Shanghai Lomicro Information Technology Co Ltd (Agnisys Inc ) introduces new hardware description language tools to streamline the RTL design process.

Future Outlook for China EDA Software Industry Market

The future outlook for the China EDA software industry is exceptionally bright, characterized by sustained high growth and increasing strategic importance. The ongoing commitment of the Chinese government to fostering domestic semiconductor innovation will continue to be a primary growth accelerator. The accelerating demand for advanced chips in emerging technologies such as AI, 5G, autonomous vehicles, and IoT will drive the adoption of cutting-edge EDA solutions. Strategic opportunities lie in the development of highly integrated and AI-enabled EDA platforms, localized support and customization for the Chinese market, and the exploration of novel design methodologies that can overcome the physical limits of semiconductor scaling. The industry is expected to witness further consolidation and strategic alliances as players vie for market leadership in this critical technological domain.

China EDA Software Industry Segmentation

-

1. Type

- 1.1. Computer-aided Engineering (CAE)

- 1.2. IC Physical Design and Verification

- 1.3. Printed

- 1.4. Semiconductor Intellectual Property (SIP)

-

2. Application

- 2.1. Communication

- 2.2. Consumer Electronics

- 2.3. Automotive

- 2.4. Industrial

- 2.5. Other Applications

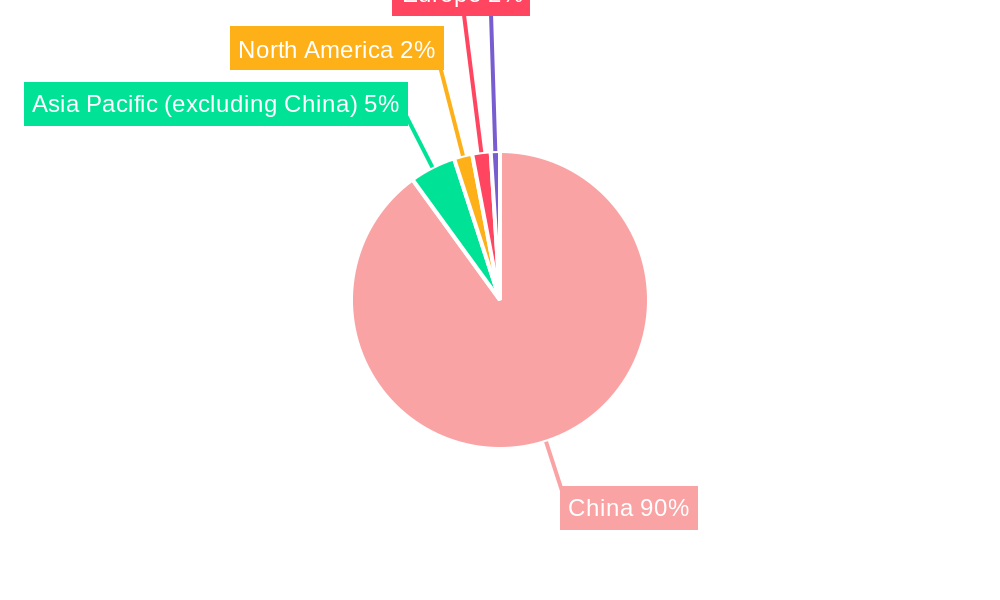

China EDA Software Industry Segmentation By Geography

- 1. China

China EDA Software Industry Regional Market Share

Geographic Coverage of China EDA Software Industry

China EDA Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Computer-aided Engineering (CAE)

- 5.1.2. IC Physical Design and Verification

- 5.1.3. Printed

- 5.1.4. Semiconductor Intellectual Property (SIP)

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Communication

- 5.2.2. Consumer Electronics

- 5.2.3. Automotive

- 5.2.4. Industrial

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China EDA Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Computer-aided Engineering (CAE)

- 6.1.2. IC Physical Design and Verification

- 6.1.3. Printed

- 6.1.4. Semiconductor Intellectual Property (SIP)

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Communication

- 6.2.2. Consumer Electronics

- 6.2.3. Automotive

- 6.2.4. Industrial

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Arcas-tech(Chengdu)co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Beijing Huada Jiutian Software Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Semitronix Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Xpeedic Technology Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Beijing Aerdai Information Technology (Aldec Inc )

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Zuken Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Altium Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shanghai Lomicro Information Technology Co Ltd (Agnisys Inc )

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mentor Graphic Corporation (Siemens PLM Software)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Synopsys Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Cadence Design Systems Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Platform Design Automation Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Arcas-tech(Chengdu)co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China EDA Software Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China EDA Software Industry Share (%) by Company 2025

List of Tables

- Table 1: China EDA Software Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: China EDA Software Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: China EDA Software Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: China EDA Software Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: China EDA Software Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: China EDA Software Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: China EDA Software Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: China EDA Software Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: China EDA Software Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: China EDA Software Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: China EDA Software Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: China EDA Software Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China EDA Software Industry?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the China EDA Software Industry?

Key companies in the market include Arcas-tech(Chengdu)co Ltd , Beijing Huada Jiutian Software Co Ltd, Semitronix Corporation, Xpeedic Technology Inc, Beijing Aerdai Information Technology (Aldec Inc ), Zuken Ltd, Altium Limited, Shanghai Lomicro Information Technology Co Ltd (Agnisys Inc ), Mentor Graphic Corporation (Siemens PLM Software), Synopsys Inc, Cadence Design Systems Inc, Platform Design Automation Inc.

3. What are the main segments of the China EDA Software Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.65 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Government Support for EDA Tool Development; Growing Prevalence of PCB Design. System Design and PL/FPGA Design.

6. What are the notable trends driving market growth?

Automotive Sector is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; Lack of Comprehensiveness of Chinese Digital Design Tools.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China EDA Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China EDA Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China EDA Software Industry?

To stay informed about further developments, trends, and reports in the China EDA Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence