Key Insights

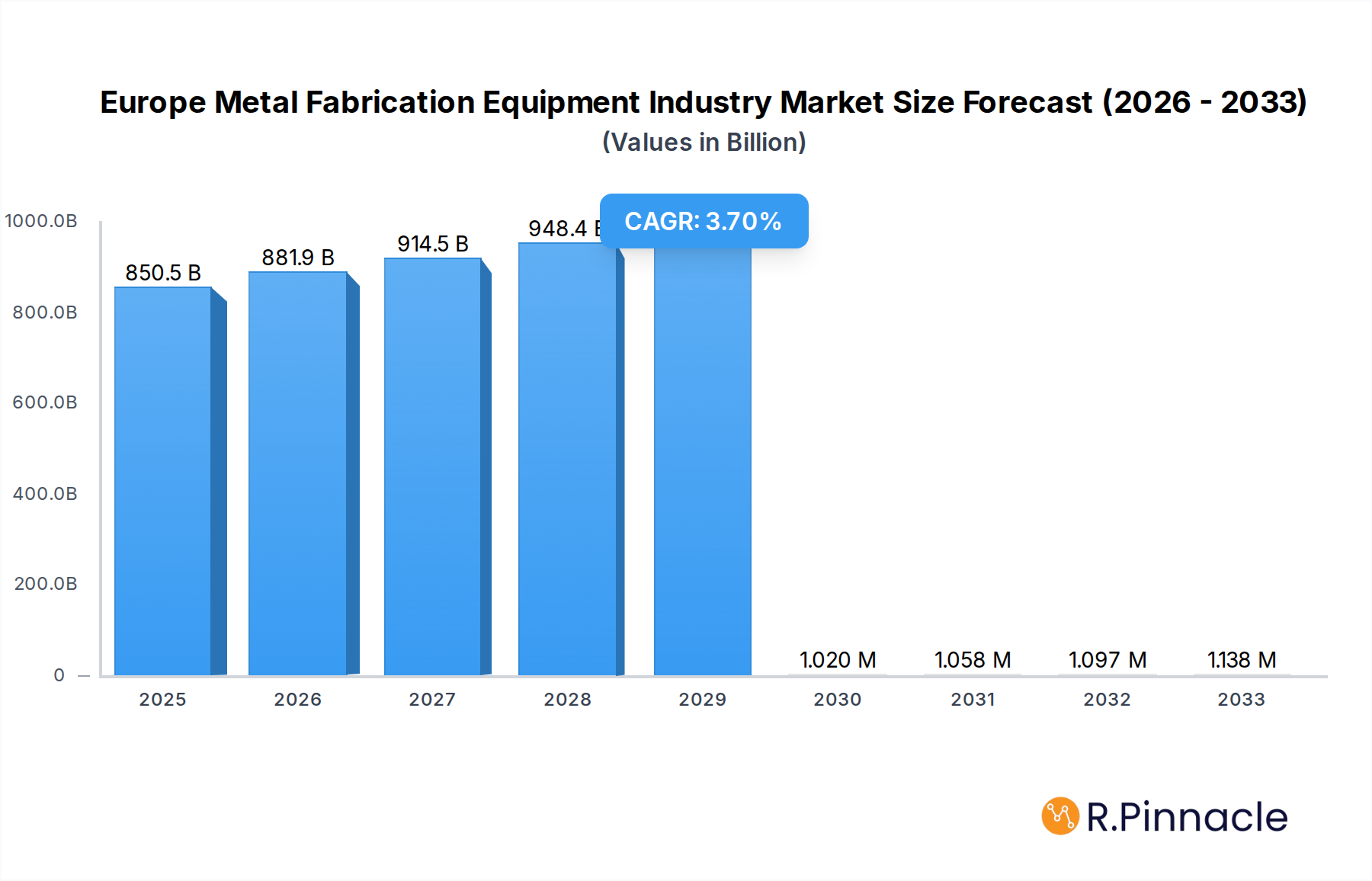

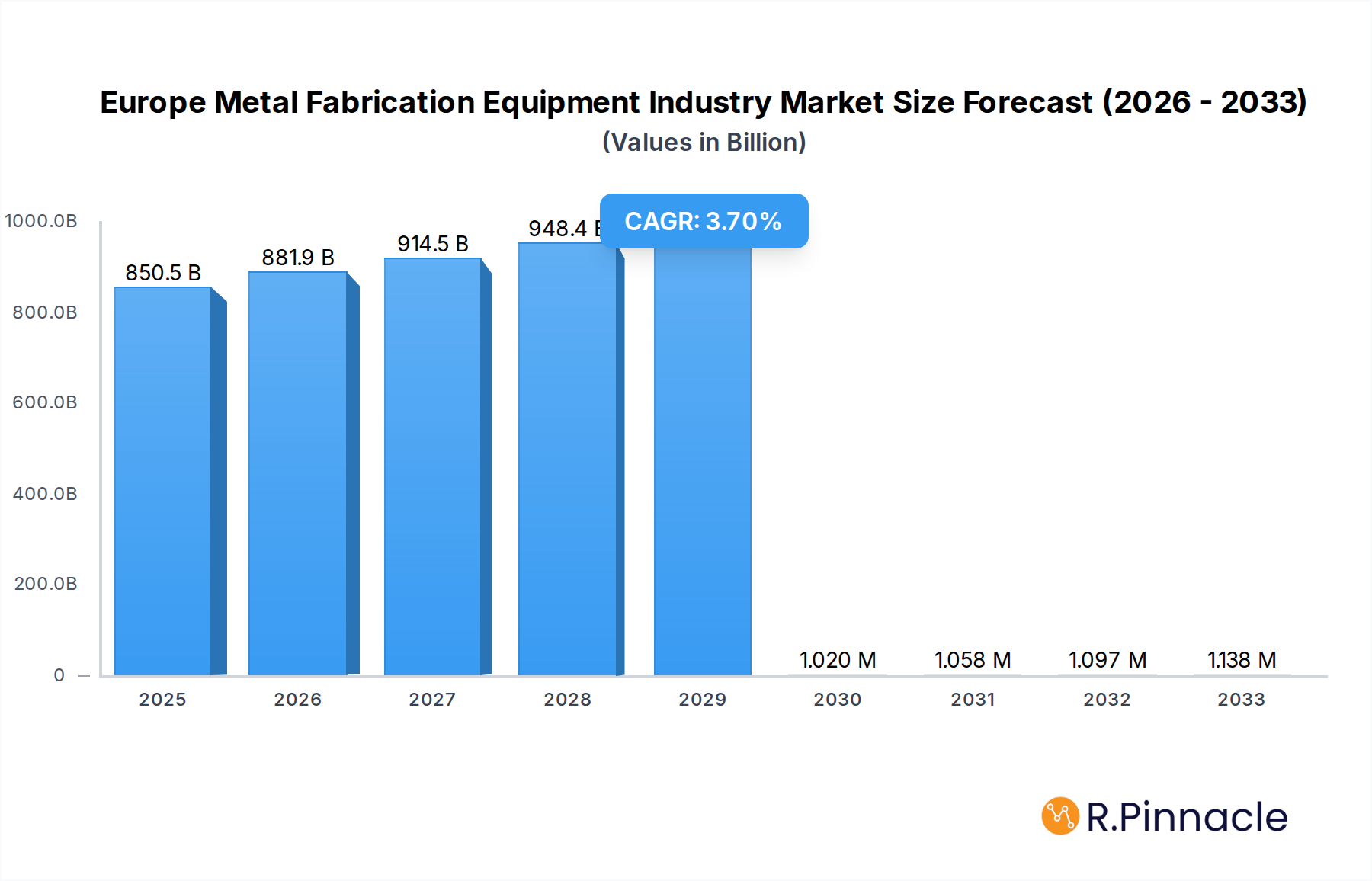

The Europe Metal Fabrication Equipment market is poised for steady expansion, projected to reach an estimated $850.5 billion in 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 3.7% anticipated from 2025 to 2033. Key drivers for this expansion include the persistent demand from the automotive sector, which is undergoing significant transformation with the rise of electric vehicles and lighter material usage, necessitating advanced fabrication techniques. The construction industry also continues to be a substantial contributor, fueled by ongoing infrastructure development and urban renewal projects across Europe. Furthermore, the aerospace sector's sustained need for high-precision components, coupled with the increasing adoption of sophisticated manufacturing technologies in electrical and electronics, are significant growth stimulants. Emerging trends such as the integration of Industry 4.0 principles, including automation, IoT, and AI in metal fabrication processes, are enhancing efficiency and precision, thereby driving market adoption of newer equipment. The focus on sustainable manufacturing practices and the demand for complex, multi-material parts are also shaping the landscape.

Europe Metal Fabrication Equipment Industry Market Size (In Billion)

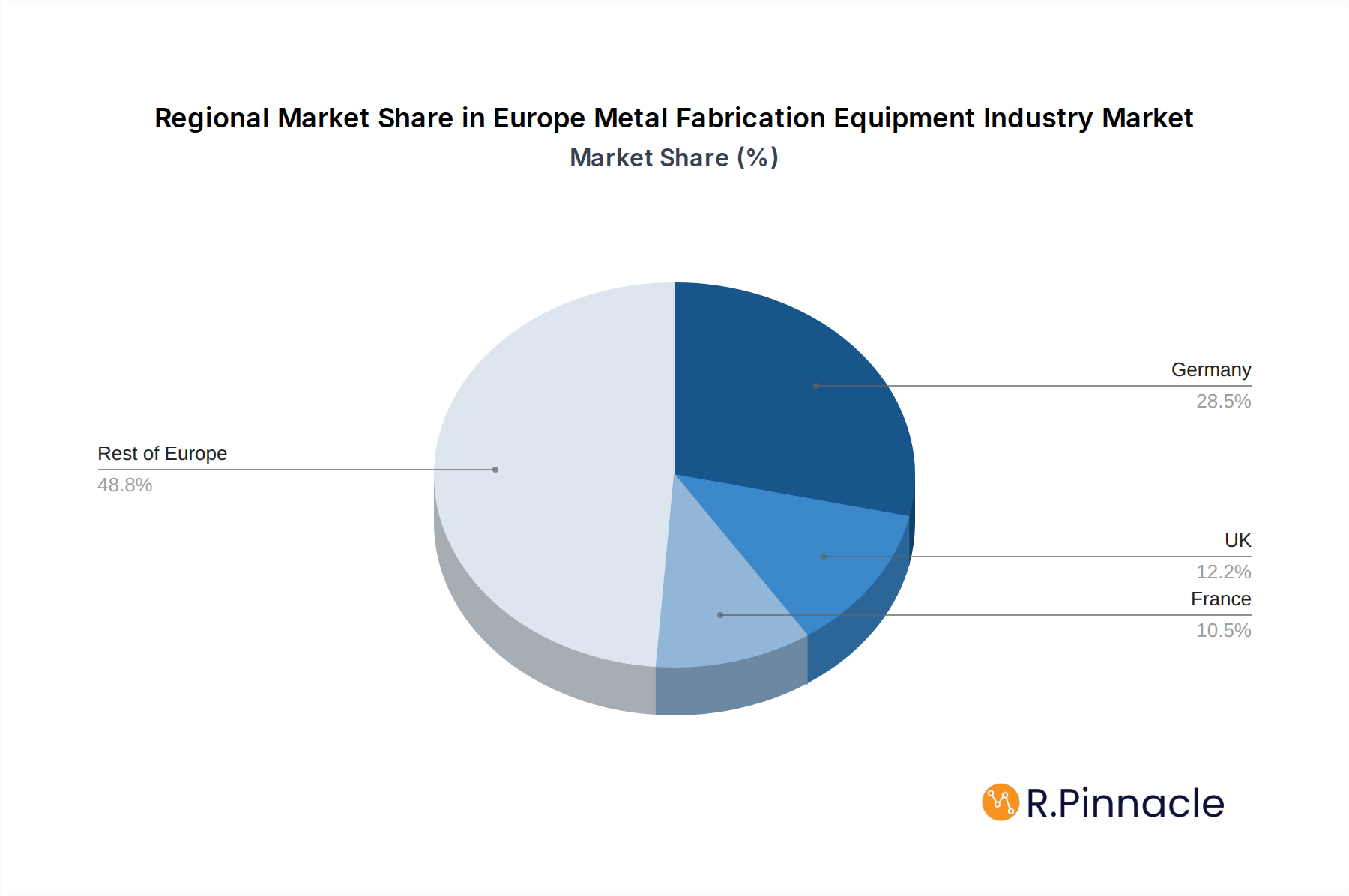

The market, however, is not without its restraints. High initial investment costs for state-of-the-art fabrication equipment can pose a barrier, particularly for small and medium-sized enterprises (SMEs). Moreover, the skilled labor shortage in specialized metalworking disciplines could impede the full utilization of advanced machinery. Despite these challenges, the market is segmented by service types like Machining, Cutting, Welding, and Forming, with each segment catering to distinct industrial needs. Leading companies such as TRUMPF GmbH + Co KG, Durr AG, Amada Europe, and DMG MORI are at the forefront, innovating and expanding their offerings to meet evolving industry demands. Geographically, Germany is expected to remain a dominant force due to its strong industrial base and technological leadership in metal fabrication. The UK, France, and the rest of Europe collectively represent significant markets with their own unique dynamics and growth potentials, driven by a combination of established industries and emerging technological adoption.

Europe Metal Fabrication Equipment Industry Company Market Share

Europe Metal Fabrication Equipment Industry Market Report: Insights, Trends, and Growth Forecast (2019-2033)

Dive deep into the dynamic Europe metal fabrication equipment market with our comprehensive report. This in-depth analysis provides critical intelligence for industry professionals, covering market structure, key trends, dominant regions, product innovations, and future outlook. Leverage actionable insights to navigate the evolving landscape of metalworking machinery, sheet metal fabrication, and advanced manufacturing solutions across Europe. With detailed segmentation and a focus on high-impact drivers, this report empowers strategic decision-making for stakeholders invested in industrial automation and precision engineering.

Europe Metal Fabrication Equipment Industry Market Structure & Innovation Trends

The Europe metal fabrication equipment industry exhibits a moderately concentrated market structure, with a few dominant players holding significant market share, estimated to be in the hundreds of billions of Euros. Innovation is a primary driver, fueled by increasing demand for automation, precision, and efficiency. Key innovation areas include advanced robotics integration, IoT-enabled machinery for predictive maintenance, and the development of more sustainable and energy-efficient equipment. Regulatory frameworks, particularly those concerning environmental impact and worker safety, play a crucial role in shaping product development and market entry strategies. The threat of product substitutes is relatively low due to the specialized nature of metal fabrication equipment, but advancements in alternative materials and manufacturing processes present a long-term consideration. End-user demographics are shifting towards more sophisticated manufacturing operations requiring higher levels of automation and data integration. Mergers and acquisitions (M&A) activity is moderate, driven by strategic consolidation and the pursuit of technological capabilities, with deal values ranging from tens to hundreds of millions of Euros.

- Market Share: Dominated by a few key players, with overall market value in the billions of Euros.

- Innovation Drivers: Automation, IoT integration, sustainability, energy efficiency, precision control.

- Regulatory Influence: Environmental standards, safety regulations, industry certifications.

- Product Substitutes: Limited in the short term, but evolving alternative manufacturing processes pose a long-term threat.

- End-User Demographics: Increasing demand for smart factory solutions and integrated production lines.

- M&A Activities: Strategic acquisitions focused on technology enhancement and market expansion, with significant deal values.

Europe Metal Fabrication Equipment Industry Market Dynamics & Trends

The Europe metal fabrication equipment market is poised for substantial growth, driven by a confluence of technological advancements, evolving consumer preferences, and robust industrial demand. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately XX%, reaching an estimated value of hundreds of billions of Euros by 2033. This expansion is primarily fueled by the automotive industry's continuous drive for lightweighting, electrification, and advanced manufacturing techniques, creating a strong demand for cutting-edge laser cutting machines, press brakes, and welding robots. The aerospace sector's pursuit of complex, high-performance components also significantly contributes to market penetration, necessitating sophisticated CNC machining centers and precision forming equipment. Furthermore, the growing emphasis on Industry 4.0 principles, including smart factories, artificial intelligence (AI) in manufacturing, and the Industrial Internet of Things (IIoT), is revolutionizing how metal fabrication is conducted. Manufacturers are investing in automated solutions, intelligent software, and data analytics to optimize production efficiency, reduce lead times, and enhance product quality. This technological disruption is leading to a significant shift in consumer preferences towards highly integrated, software-driven, and adaptable fabrication systems. Competitive dynamics are intense, characterized by product innovation, strategic partnerships, and a focus on providing comprehensive service and support packages. The increasing adoption of additive manufacturing technologies within traditional fabrication workflows also presents a new dimension of competition and collaboration. The construction sector's ongoing infrastructure development and modernization projects, coupled with the electrical and electronics industry's demand for intricate metal components, further bolster market growth. The overall trend is towards more intelligent, flexible, and sustainable metal fabrication solutions that cater to the evolving needs of modern industries.

Dominant Regions & Segments in Europe Metal Fabrication Equipment Industry

The Europe metal fabrication equipment industry is a multifaceted market, with distinct regional strengths and dominant segments driving its overall trajectory. Germany consistently emerges as the leading country, leveraging its strong industrial base, advanced technological capabilities, and a high concentration of key manufacturers. Its robust automotive and aerospace sectors, coupled with significant investment in R&D, solidify its position as the epicentre of metal fabrication innovation and consumption. Other influential countries include Italy, France, and the UK, each contributing significantly through specialized manufacturing hubs and distinct industrial demands.

The Machining segment, encompassing precision CNC machining centers, lathes, and milling machines, is a cornerstone of the market, driven by the stringent quality requirements of industries like aerospace and automotive. Its dominance is fueled by the need for intricate part production and tight tolerances. The Cutting segment, including laser cutting, plasma cutting, and waterjet cutting technologies, is also experiencing robust growth. This is attributed to the increasing demand for high-speed, precise, and versatile cutting solutions across various end-user industries, enabling the creation of complex shapes and designs.

The Automotive end-user industry remains the single largest driver of the metal fabrication equipment market in Europe. The relentless pursuit of electric vehicles (EVs), lightweight materials, and advanced driver-assistance systems (ADAS) necessitates sophisticated fabrication processes. The Construction industry, fueled by ongoing infrastructure projects and the demand for pre-fabricated metal components, also represents a significant and growing market. The Aerospace sector, with its exacting standards for performance and safety, consistently drives demand for high-precision metal forming equipment and advanced machining solutions. The Electrical and Electronics industry, while smaller in comparison, is crucial for the production of intricate components and enclosures, showcasing consistent demand for specialized fabrication equipment.

- Dominant Country: Germany, with its strong manufacturing heritage and technological leadership, leads the market.

- Leading Segments:

- Machining: Driven by precision requirements in automotive and aerospace.

- Cutting: Supported by the demand for versatile and high-speed solutions across industries.

- Key End-User Industries:

- Automotive: Major contributor due to EV production and lightweighting trends.

- Construction: Benefiting from infrastructure development and pre-fabrication needs.

- Aerospace: Consistently driving demand for high-precision equipment.

- Electrical and Electronics: Contributing through the need for intricate component fabrication.

Europe Metal Fabrication Equipment Industry Product Innovations

The Europe metal fabrication equipment industry is witnessing a surge in product innovations focused on enhancing efficiency, precision, and intelligence. Key advancements include the integration of AI and IoT for predictive maintenance and remote monitoring, leading to reduced downtime and optimized performance. Laser cutting technology is evolving with higher power outputs and improved beam quality for faster and cleaner cuts. Robotic automation is becoming more sophisticated, offering greater flexibility and integration into complex assembly lines. Smart welding solutions are employing advanced sensor technology for real-time quality control and process optimization. The development of energy-efficient machinery and sustainable manufacturing processes is also a significant trend, aligning with environmental regulations and industry demands.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Europe metal fabrication equipment industry, segmented by service type and end-user industries. The service types include Machining, Cutting, Welding, Forming, and Other Service Types, each contributing to the overall market value estimated in the billions of Euros. In terms of end-user industries, the analysis covers Automotive, Construction, Aerospace, Electrical and Electronics, and Other End-user Industries. The Automotive sector is projected to maintain its leading position, driven by electric vehicle production and lightweighting initiatives. The Construction sector's growth is fueled by infrastructure investments. The Aerospace segment's demand for high-precision components ensures its consistent contribution. The Electrical and Electronics industry, while a niche market, plays a vital role in the fabrication of specialized components.

Key Drivers of Europe Metal Fabrication Equipment Industry Growth

The Europe metal fabrication equipment industry is propelled by several powerful drivers. Technological advancements, particularly in automation, AI, and IoT, are revolutionizing manufacturing processes, enhancing efficiency and precision. The strong growth in key end-user industries such as automotive (especially EVs), construction (infrastructure development), and aerospace (advanced aircraft production) directly translates into increased demand for fabrication equipment. Furthermore, government initiatives supporting manufacturing upgrades, digitalization, and sustainability are providing a conducive environment for market expansion. The ongoing need for lightweight materials and complex component manufacturing across these sectors necessitates sophisticated and advanced metal fabrication solutions, further accelerating growth.

Challenges in the Europe Metal Fabrication Equipment Industry Sector

Despite robust growth, the Europe metal fabrication equipment industry faces several significant challenges. Stringent environmental regulations and the push for sustainability can lead to increased compliance costs for manufacturers. Supply chain disruptions, exacerbated by geopolitical factors and raw material price volatility, can impact production timelines and profitability. The skilled labor shortage in advanced manufacturing roles poses a considerable restraint, affecting the adoption of new technologies. Intense competition, both from established players and emerging low-cost manufacturers, pressures profit margins. The high initial investment cost for advanced fabrication equipment can also be a barrier for smaller enterprises, limiting market penetration in certain segments.

Emerging Opportunities in Europe Metal Fabrication Equipment Industry

The Europe metal fabrication equipment industry is rife with emerging opportunities. The accelerating adoption of Industry 4.0 and smart factory technologies presents significant potential for growth in integrated automation and data-driven manufacturing solutions. The burgeoning electric vehicle (EV) market is creating unprecedented demand for specialized fabrication equipment for battery components, lightweight chassis, and advanced thermal management systems. The growing emphasis on additive manufacturing (3D printing) alongside traditional fabrication methods opens avenues for hybrid solutions and innovative material processing. Furthermore, the drive towards a circular economy is spurring demand for equipment that facilitates efficient recycling and remanufacturing of metal components. Expansion into emerging markets within Europe and the development of more accessible, modular fabrication solutions offer further avenues for untapped potential.

Leading Players in the Europe Metal Fabrication Equipment Industry Market

- TRUMPF GmbH + Co KG

- Durr AG

- Amada Europe

- GF Machining Solutions

- DMG MORI

- Schuler AG

- GROB-WERKE GmbH

- Bystronic Maschinen AG

- Feintool International Holding AG

- Mazak U K Limited

- Reishauer AG

- Okuma Europe

- Gebr Heller Maschinenfabrik GmbH

- Starrag Group Holding AG

- Meusburger Georg GmbH

- Baileigh Industrial

Key Developments in Europe Metal Fabrication Equipment Industry Industry

- December 2022: STOPA, a leading producer of automated storage systems, and TRUMPF, a high-tech business, announced an expanded cooperation. This collaboration will enhance TRUMPF's smart-factory solutions by integrating STOPA's automated storage options, enabling customers to automatically load and unload machines, creating interconnected logistics networks and significantly reducing non-productive time for increased shop floor production.

- December 2022: Dürr, a top mechanical and plant engineering company, introduced a new generation of pneumatic vertical piston pumps, the EcoPump2 VP. These pumps are designed to improve process reliability while requiring substantially less maintenance. The EcoPump2 VP is suitable for a wide array of industries, including mechanical engineering, woodworking, metalworking, and the furniture sector, and is engineered to handle various industrial media.

Future Outlook for Europe Metal Fabrication Equipment Industry Market

The future outlook for the Europe metal fabrication equipment industry is highly promising, driven by the relentless march of technological innovation and the evolving demands of major industrial sectors. The continued integration of AI, IoT, and robotics will lead to increasingly intelligent and autonomous fabrication processes, pushing the boundaries of efficiency and precision. The ongoing transition to electric vehicles and sustainable energy solutions will continue to be a significant growth accelerator, demanding specialized sheet metal fabrication capabilities and advanced welding technologies. Investments in smart factories and digital manufacturing infrastructure are expected to rise, creating a fertile ground for sophisticated equipment and integrated solutions. Furthermore, the industry's commitment to sustainability will foster innovation in energy-efficient machinery and environmentally friendly production methods, positioning the sector for long-term, responsible growth.

Europe Metal Fabrication Equipment Industry Segmentation

-

1. Service type

- 1.1. Machining

- 1.2. Cutting

- 1.3. Welding

- 1.4. Forming

- 1.5. Other Service Types

-

2. End-user Industries

- 2.1. Automotive

- 2.2. Construction

- 2.3. Aerospace

- 2.4. Electrical and Electronics

- 2.5. Other End-user Industries

Europe Metal Fabrication Equipment Industry Segmentation By Geography

- 1. Germany

- 2. UK

- 3. France

- 4. Rest of the Europe

Europe Metal Fabrication Equipment Industry Regional Market Share

Geographic Coverage of Europe Metal Fabrication Equipment Industry

Europe Metal Fabrication Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service type

- 5.1.1. Machining

- 5.1.2. Cutting

- 5.1.3. Welding

- 5.1.4. Forming

- 5.1.5. Other Service Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industries

- 5.2.1. Automotive

- 5.2.2. Construction

- 5.2.3. Aerospace

- 5.2.4. Electrical and Electronics

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. UK

- 5.3.3. France

- 5.3.4. Rest of the Europe

- 5.1. Market Analysis, Insights and Forecast - by Service type

- 6. Global Europe Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service type

- 6.1.1. Machining

- 6.1.2. Cutting

- 6.1.3. Welding

- 6.1.4. Forming

- 6.1.5. Other Service Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industries

- 6.2.1. Automotive

- 6.2.2. Construction

- 6.2.3. Aerospace

- 6.2.4. Electrical and Electronics

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Service type

- 7. Germany Europe Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service type

- 7.1.1. Machining

- 7.1.2. Cutting

- 7.1.3. Welding

- 7.1.4. Forming

- 7.1.5. Other Service Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industries

- 7.2.1. Automotive

- 7.2.2. Construction

- 7.2.3. Aerospace

- 7.2.4. Electrical and Electronics

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Service type

- 8. UK Europe Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service type

- 8.1.1. Machining

- 8.1.2. Cutting

- 8.1.3. Welding

- 8.1.4. Forming

- 8.1.5. Other Service Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industries

- 8.2.1. Automotive

- 8.2.2. Construction

- 8.2.3. Aerospace

- 8.2.4. Electrical and Electronics

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Service type

- 9. France Europe Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service type

- 9.1.1. Machining

- 9.1.2. Cutting

- 9.1.3. Welding

- 9.1.4. Forming

- 9.1.5. Other Service Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industries

- 9.2.1. Automotive

- 9.2.2. Construction

- 9.2.3. Aerospace

- 9.2.4. Electrical and Electronics

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Service type

- 10. Rest of the Europe Europe Metal Fabrication Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service type

- 10.1.1. Machining

- 10.1.2. Cutting

- 10.1.3. Welding

- 10.1.4. Forming

- 10.1.5. Other Service Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industries

- 10.2.1. Automotive

- 10.2.2. Construction

- 10.2.3. Aerospace

- 10.2.4. Electrical and Electronics

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Service type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 TRUMPF GmbH + Co KG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Durr AG

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Amada Europe

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 GF Machining Solutions

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 DMG MORI

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Schuler AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 GROB-WERKE GmbH

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Bystronic Maschinen AG

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Feintool International Holding AG

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Mazak U K Limited**List Not Exhaustive 6 3 Other Companies (Reishauer AG Okuma Europe Gebr Heller Maschinenfabrik GmbH Starrag Group Holding AG Meusburger Georg Gmbh Baileigh Industrial

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 TRUMPF GmbH + Co KG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Europe Metal Fabrication Equipment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Germany Europe Metal Fabrication Equipment Industry Revenue (billion), by Service type 2025 & 2033

- Figure 3: Germany Europe Metal Fabrication Equipment Industry Revenue Share (%), by Service type 2025 & 2033

- Figure 4: Germany Europe Metal Fabrication Equipment Industry Revenue (billion), by End-user Industries 2025 & 2033

- Figure 5: Germany Europe Metal Fabrication Equipment Industry Revenue Share (%), by End-user Industries 2025 & 2033

- Figure 6: Germany Europe Metal Fabrication Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Germany Europe Metal Fabrication Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: UK Europe Metal Fabrication Equipment Industry Revenue (billion), by Service type 2025 & 2033

- Figure 9: UK Europe Metal Fabrication Equipment Industry Revenue Share (%), by Service type 2025 & 2033

- Figure 10: UK Europe Metal Fabrication Equipment Industry Revenue (billion), by End-user Industries 2025 & 2033

- Figure 11: UK Europe Metal Fabrication Equipment Industry Revenue Share (%), by End-user Industries 2025 & 2033

- Figure 12: UK Europe Metal Fabrication Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: UK Europe Metal Fabrication Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: France Europe Metal Fabrication Equipment Industry Revenue (billion), by Service type 2025 & 2033

- Figure 15: France Europe Metal Fabrication Equipment Industry Revenue Share (%), by Service type 2025 & 2033

- Figure 16: France Europe Metal Fabrication Equipment Industry Revenue (billion), by End-user Industries 2025 & 2033

- Figure 17: France Europe Metal Fabrication Equipment Industry Revenue Share (%), by End-user Industries 2025 & 2033

- Figure 18: France Europe Metal Fabrication Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: France Europe Metal Fabrication Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue (billion), by Service type 2025 & 2033

- Figure 21: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue Share (%), by Service type 2025 & 2033

- Figure 22: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue (billion), by End-user Industries 2025 & 2033

- Figure 23: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue Share (%), by End-user Industries 2025 & 2033

- Figure 24: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the Europe Europe Metal Fabrication Equipment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Service type 2020 & 2033

- Table 2: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by End-user Industries 2020 & 2033

- Table 3: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Service type 2020 & 2033

- Table 5: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by End-user Industries 2020 & 2033

- Table 6: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Service type 2020 & 2033

- Table 8: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by End-user Industries 2020 & 2033

- Table 9: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Service type 2020 & 2033

- Table 11: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by End-user Industries 2020 & 2033

- Table 12: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Service type 2020 & 2033

- Table 14: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by End-user Industries 2020 & 2033

- Table 15: Global Europe Metal Fabrication Equipment Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Metal Fabrication Equipment Industry?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the Europe Metal Fabrication Equipment Industry?

Key companies in the market include TRUMPF GmbH + Co KG, Durr AG, Amada Europe, GF Machining Solutions, DMG MORI, Schuler AG, GROB-WERKE GmbH, Bystronic Maschinen AG, Feintool International Holding AG, Mazak U K Limited**List Not Exhaustive 6 3 Other Companies (Reishauer AG Okuma Europe Gebr Heller Maschinenfabrik GmbH Starrag Group Holding AG Meusburger Georg Gmbh Baileigh Industrial.

3. What are the main segments of the Europe Metal Fabrication Equipment Industry?

The market segments include Service type, End-user Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 850.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Rising Technological Innovations in Metal Fabrication Industry.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

December 2022: One of the top producers of automated storage systems, STOPA, and the high-tech business TRUMPF have announced a deal to cooperate more in the future. Numerous applications, including TRUMPF's smart-factory solutions, leverage STOPA's automated storage options. Customers may automatically load and unload their machines with STOPA systems, and they can connect units to create logistics networks. This greatly reduces non-productive time, which increases shop floor production.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Metal Fabrication Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Metal Fabrication Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Metal Fabrication Equipment Industry?

To stay informed about further developments, trends, and reports in the Europe Metal Fabrication Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence